All eyes turn to Brexit this week in what could be a crunch few days for the UK government. Additionally, as DB notes, a BoJ meeting and US CPI, PPI and retail sales data are also highlights. China’s NPC also enters its second week while European Parliament votes on a resolution about security threats linked to Chinese tech.

With just three weeks to go until the UK is scheduled to leave the EU, another “crunch” week awaits the UK government. On Tuesday the House of Commons is scheduled to hold a meaningful vote on the amended Withdrawal Agreement. If the vote is rejected, lawmakers will then be asked on Wednesday if the UK should take a no-deal Brexit option off the table in its negotiations. If that is rejected, then on Thursday Parliament will hold a vote on an extension to Article 50. Should the extension be accepted then this would likely result in it being signed off at the March 21/22 EU summit. Needless to say that newsflow in recent days has been less than encouraging for PM May, despite signs that the two sides are engaging. That said it appears that the two sides remain far apart. Talks are expected to continue over the weekend and into Monday, however should they fail then it’s likely Parliament will vote against the deal on Tuesday. That would make an extension likely. Much could depend on the next 72 hours however.

As for the BoJ on Friday, no change in policy is expected and the meeting also doesn’t include an outlook report so it’s likely to be mostly a non-event. There was a bit of interest in a Bloomberg report this week which suggested that the BoJ would discuss a possible downgrade in its view of overseas economies, production and exports. Deutsche Bank economists consider this appropriate given the disappointing production and export data for January. Nevertheless, they note that the output gap as measured by the BoJ remains positive, so even a downward revision in production and exports should not affect its overall evaluation of the economy. The team see a low likelihood of measures being eased further at the meeting. The ongoing decline in the yen is also a plus for the BoJ.

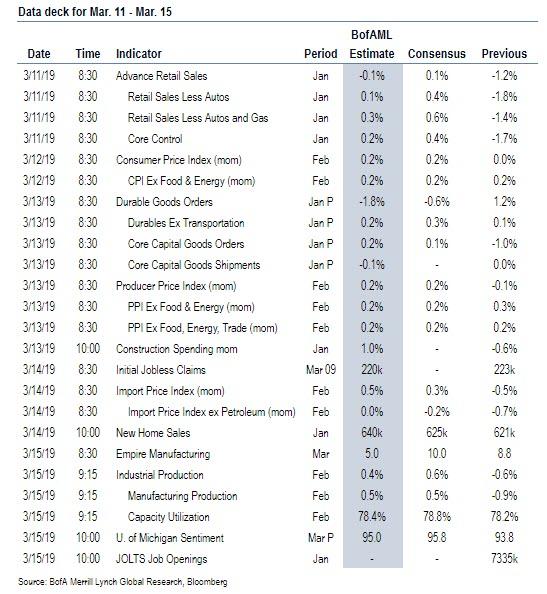

The top tier data releases in the US this week include January retail sales on Monday, February CPI on Tuesday and February PPI on Wednesday. We’ll also get important preliminary January durable and capital goods orders data on Wednesday and February industrial production on Friday. For retail sales, core sales are expected to have risen a solid +0.6% mom during the month following the very weak December stats. CPI is expected to have risen +0.2% mom at the core level which should hold the annual rate at +2.2% yoy and therefore comfortably within the Fed’s target. Meanwhile PPI is expected to also be up +0.2% mom at the core.

The highlights in Europe next week are January industrial production reports in Germany, UK and the Euro Area on Monday, Tuesday and Wednesday respectively, January GDP in the UK on Tuesday, and final February CPI revisions for Germany and France on Thursday and the Euro Area on Friday.

In China the NPC will begin its second week. The Congress will conclude with Premier Li Keqiang’s annual press conference on Friday.

Other things to potentially watch out for next week include President Trump’s proposed fiscal 2020 budget, expected on Monday. The partial government shutdown delayed its release. Euro Area finance ministers also meet on Monday and Tuesday to discuss progress on Greek reforms, the budget and tax on internet companies. European Parliament meets on Tuesday to vote on a security measure tied to Huawei titled “Security Threats Connected with the Rising Chinese Technological Presence”. The OPEC monthly report is out on Thursday while ECB speakers next week include Lautenschlaeger on Tuesday, Coeure on Wednesday and Rehn on Friday.

Summary of Key Events by Day

- Monday: The main data focus will be in the US where the January retail sales report is due to be released. Prior to that we’ll see the January industrial production and trade balance prints in Germany, and February industrial sentiment reading in France. December business inventories in the US will also be out. Meanwhile, President Trump is expected to release his proposed fiscal 2020 budget, Euro Area finance ministers are due to meet in Brussels and the BoE’s Haskel is due to speak.

- Tuesday: The February CPI report in the US is likely to be the highlight for data releases. In Europe we’ll see Q4 payrolls data in France and January GDP, trade and industrial production data in the UK. The February NFIB small business optimism reading will also be out in the US. Away from that the House of Commons is scheduled to vote on the revised Brexit deal, European Parliament votes on security measures tied to Huawei and the ECB’s Lautenschlaeger speaks in Basel.

- Wednesday: The early data release is the January industrial production report for the Euro Area, while data due in the US includes February PPI, preliminary January durable and capital goods orders, and January construction spending. Elsewhere, EU ambassadors discuss Brexit in Brussels, UK lawmakers may vote on legislation to leave the EU without a deal. Chancellor Hammond presents the Spring Statement and the ECB’s Coeure speaks in Milan.

- Thursday: The overnight focus should be in China where we’ll see February fixed asset investment, industrial production and retail sales data. In Europe we’ll get final February CPI revisions in Germany and France, while in the US we’ll get the February import price index print, latest weekly initial jobless claims and January new home sales. In the UK the House of Commons may vote on legislation to delay withdrawal from the EU. The OPEC monthly report is also due out.

- Friday: The main focus will likely be the BoJ monetary policy meeting. Also out overnight will be February new home prices data in China. In Europe we’ll get the final February CPI revisions for the Euro Area, while in the US we’ll get March empire manufacturing, February industrial production, January JOLTS job openings and the preliminary March University of Michigan consumer sentiment survey. The ECB’s Rehn is also due to speak

Finally, here is Goldman’s preview of key events in the US, which are the retail sales report on Monday, the CPI report on Tuesday, and the PPI and durable goods reports on Wednesday. We do not expect any policy-related speeches by Fed officials, reflecting the blackout period ahead of the March FOMC meeting.

Monday, March 11

- 08:30 AM Retail sales, January (GS +0.8%, consensus +0.1%, last -1.2%); Retail sales ex-auto, January (GS +0.7%, consensus +0.4%, last -1.8%); Retail sales ex-auto & gas, January (GS +1.0%, consensus +0.6%, -1.4%); Core retail sales, January (GS +1.1%, consensus +0.6%, last -1.7%): We estimate that core retail sales (ex-autos, gasoline, and building materials) rose at a strong pace in January (+1.1% mom sa), reflecting alternative data at odds with the weak December retail sales report and some scope for a boost from residual seasonality. We estimate a 0.8% increase in the headline measure, reflecting a modest rebound in auto sales and a further decline in gasoline prices, and a 0.7% increase in the ex-auto measure.

- 10:00 AM Business inventories, December (consensus +0.6%, last -0.1%)

Tuesday, March 12

- 06:00 AM NFIB small business optimism, February (consensus 102.5, last 101.2)

- 08:30 AM CPI (mom), February (GS +0.16%, consensus +0.2%, last flat); Core CPI (mom), February (GS +0.18%, consensus +0.2%, last +0.2%); CPI (yoy), February (GS +1.52%, consensus +1.6%, last +1.6%); Core CPI (yoy), February (GS +2.16%, consensus +2.2%, last +2.2%): We estimate a 0.18% increase in February core CPI (mom sa), which would leave the year-over-year rate stable at +2.2%. Our forecast reflects a boost from the end of last year’s prescription-drug price freezes. We also expect a stable pace of monthly shelter inflation, as alternative rent measures have picked back up, apartment completions have peaked, and aggregate vacancy rates declined further. On the negative side, we expect a drag from lower airfare and weaker used car auction prices. We look for a 0.16% increase in headline CPI (mom sa), reflecting lower gasoline prices but higher food costs.

Wednesday, March 13

- 08:30 AM PPI final demand, February (GS +0.2%, consensus +0.2%, last -0.1%); PPI ex-food and energy, February (GS +0.2%, consensus +0.2%, last +0.3%); PPI ex-food, energy, and trade, February (GS +0.2%, consensus + 0.2%, last +0.2%): We estimate a 0.2% increase in headline PPI in February, reflecting relatively firm core prices and energy prices. We expect a 0.2% increase in the core measure excluding food and energy, and also a 0.2% increase in the core measure excluding food, energy, and trade.

- 08:30 AM Durable goods orders, January preliminary (GS +0.4%, consensus -0.6%, last +1.2%); Durable goods orders ex-transportation, January preliminary (GS flat, consensus +0.3%, last +0.1%); Core capital goods orders, January preliminary (GS flat, consensus +0.1%, last -1.0%); Core capital goods shipments, January preliminary (GS -0.3%, consensus +0.1%, last flat): We expect durable goods orders to increase 0.4% in the preliminary January report, given higher-than-usual January commercial aircraft orders. Slowing global growth and declines in manufacturing surveys suggest a drag on core capital goods shipments, which we expect to decline by 0.3%.

- 10:00 AM Construction spending, January (GS +0.4%, consensus +0.4%, last -0.6%); We estimate a 0.4% increase in construction spending in January, with scope for a modest decline in private residential construction, but an increase in nonresidential construction.

Thursday, March 14

- 08:30 AM Import price index, February (consensus +0.3%, last -0.5%)

- 08:30 AM Initial jobless claims, week ended March 9 (GS 230k, consensus 225k, last 223k); Continuing jobless claims, week ended March 2 (last 1,755k): We estimate jobless claims increased by 7k to 230k in the week ended March 9, following a 3k decline in the prior week. The claims reports of recent weeks suggest that the pace of layoffs remains low, though it probably remains somewhat higher than in early fall.

- 10:00 AM New home sales, January (GS +0.8%, consensus +0.6%, last +3.7%): We estimate new home sales increased by 0.8% in January, following a 3.7% increase in the prior month. Single family starts increased sharply in January.

Friday, March 15

- 08:30 AM Empire State manufacturing index, March (consensus +10.0, last +8.8)

- 09:15 AM Industrial production, February (GS +0.3%, consensus +0.4%, last -0.6%); Manufacturing production, February (GS flat, consensus +0.1, last -0.9%); Capacity utilization, February (GS 78.3%, consensus 78.5%, last 78.2%); We estimate industrial production rose 0.3% in February, driven by strength in the utilities category and offset by weakness in auto manufacturing. We estimate capacity utilization edged up one tenth to 78.3%.

- 10:00 AM JOLTS Job Openings, January (consensus 7,250 last 7,335k)

- 10:00 AM University of Michigan consumer sentiment, March preliminary (GS 95.9, consensus 95.6, last 93.8); We expect the University of Michigan consumer sentiment index to increase by 2.1pt to 95.9, partially reflecting further increases in the stock market.

Source: DB, BofA, Goldman

via ZeroHedge News https://ift.tt/2SYnMvE Tyler Durden