Chinese Premier Li promised yet more stimulus measures overnight from tax cuts to focused rate reductions (but, he admitted, not blanket liquidity provision).

But, after over 60 different ‘stimulus’ measures in the last few months and last night’s promises, nothing seems to be working as China’s economic data continues to tumble.

As Goldman’s Andrew Tilton (Chief Asia Economist) suggested:

“There are reasons to be concerned [that easing is becoming less effective]. Local government officials who typically implement infrastructure spending and other forms of stimulus are facing conflicting pressures. The emphasis in recent years on reducing off-balance-sheet borrowing, selecting only higher-value projects, and eliminating corruption has made local officials more cautious. But at the same time, the authorities are now encouraging local officials to do more to support growth, like accelerate infrastructure projects. President Xi himself recently acknowledged the incentive problems and administrative burdens facing local officials.”

And Nomura’s Ting Lu has an explanation for why China stimulus i snot working…

Chinese easing- / stimulus- escalation being a likely requirement for any sort of “reflation” theme to work beyond a tactical trade:

yes, more RRR cuts are coming eventually (a better way for Chinese banks to obtain liquidity vs borrowing from MLF or TMLF, bc it’s cheaper and more stable)…

…but that the timing of such a cut is primarily dependent on the Chinese stock market, as the “re-bubbling” happening real-time in Chinese Equities (CSI 300 +26.8% YTD; SHCOMP +24.4%; SZCOMP +34.0%) likely then constrains the room and pace of Beijing’s policy easing / stimulus

This “Chinese Equities rally effectively holding further RRR cuts hostage” then could become a serious “fly in the ointment” for near-term / tactical “reflation” (or bear-steepening) themes, as Q2 is on-pace to see a significant liquidity shortage.

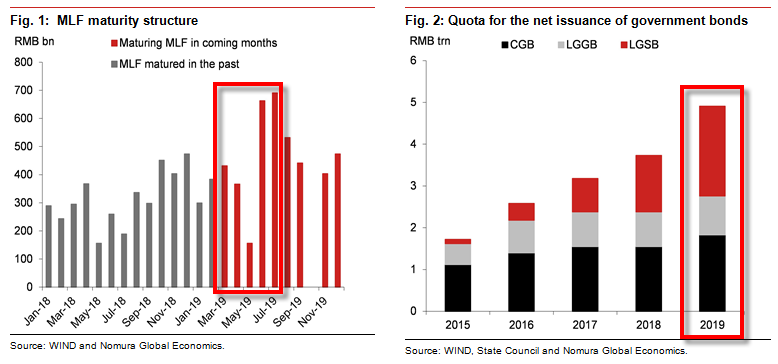

Ting estimates the liquidity gap could reach ~ RMB 1.7T in Q2 due to the following factors:

-

The size of the upcoming MLF maturities (est to be ~RMB 1.2T in Q2);

-

The size and pace of (both central and local) government bond issuance (Nomura ests a target of ~ RMB 1T for Q2);

-

Tax season effects; and

-

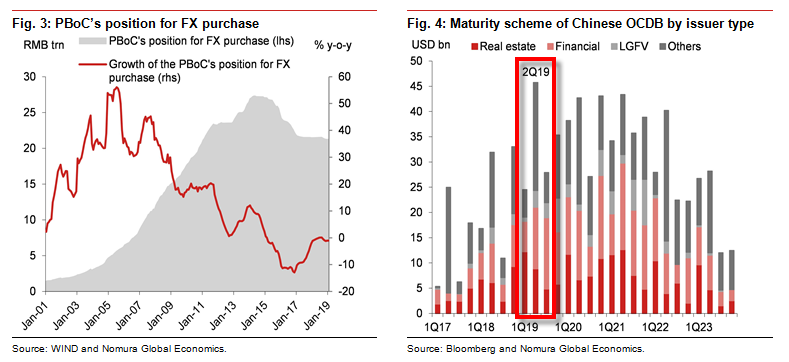

The shortage of money supply through the PBoC’s FX purchases

CHINA’S COMING Q2 LIQUIDITY-SHORTAGE:

So, simply put, China is merely refilling a rapidly leaking bucket of liquidity, as opposed to sloshing more into the bath of global risk – even if Chinese stocks were embracing it.

via ZeroHedge News https://ift.tt/2ClS8D9 Tyler Durden