For a brief period yesterday, it seemed the stock rally may stall just as the market settled into its comfortable, pre-FOMC melt up. To be sure, there were numerous catalysts to fade the current 5 month high with Nomura listing 6 reasons why stocks may fade as we enter the “pullback window.” Traders were additionally spooked by yesterday’s “spot up, VIX up, VVIX up” combo, which as Charlie McElligott notes, “always raises an eyebrow from market bystanders” although in retrospect it appeared to be largely due to systematic vol sellers covering some of their “short” inventory per the broker markets, as well as June SPX upside going very “bid” following Sunday night’s SCMP report that the meeting between Trump and Xi had been postponed to “June.”

However, the selling was just not meant to be and as has been the case ahead of most Fed meetings this decade, the popular “FOMC-drift” emerged right on cue, with stocks rallying as they always do the day into a Fed meeting. Meanwhile, as Nomura’s Charlie McElligott notes in his latest letter, the last remaining CTA US Equities “short” in the Russell was triggered to “cover and flip” on the close yesterday, and is once again “+100% Max Long.”

The overnight rally was also supported by the ongoing ramp in European equities with the Stoxx 50 now +3.5% MTD / +13.7% YTD, and just days after we said there is a “surprise upside” coming to Europe, BofA’s latest fund manager survey revealed that “short European stocks” was named the “Most Crowded Trade” with the shorts carted out in “market seeking max pain” fashion, as McElligott snydely remarks.

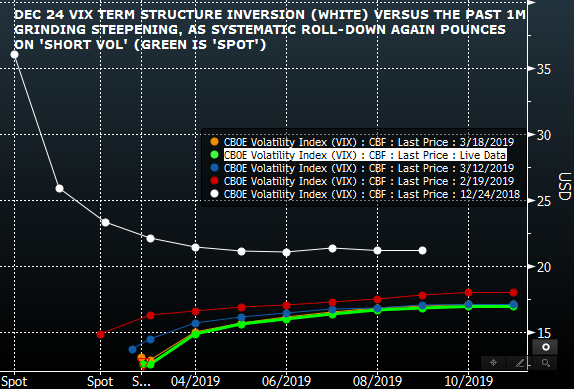

Looking back over the past 24 hours, in his latest note today, McElligott concedes that yesterday’s dynamic looks even more like a “mirage” as once again today we are seeing spot VIX hit lower, “with UXA term structure SO STEEP and traders seeing UX2 with ~2.2 vols of roll-down apparently just being too-good to pass up ( “short VXX” is the equivalent for day-traders / retail punters).”

And as the Nomura strategist points out, all this is taking place despite the Fed “event risk” tomorrow, which of course is “the joke here”, because as McElligott adds “there is no “event risk” with a Fed which has completely gone limp due to a singular focus on avoidance of contributing to “tighter financial conditions” and if anything, seeing global central banks now working to advocate an outright “reflationary” backdrop.“

In retrospect, all those who predicted that a Shanghai Accord 2.0 would emerge from the depths of the post Christmas crash were correct.

So as we levitate into the autopilot of the “FOMC drift” here is what else is happening according to the Nomura guru:

- U.S. Dollar is properly hit as some risk-positive Brexit headlines on a purported EU leader “contingent offer” on a delay extension—in turn we see nearly all G10 firmer (ex AUD—see below) and EMFX getting legs; Dollar too is reflecting the “very dovish” expected outcome priced-into rates markets ahead of the FOMC tomorrow

- Despite low volumes overnight as markets sit quietly ahead of Fed event-risk tomorrow (TY currently ‘unch’), USTs seemingly were initially supported by more global “dovishness” and “duration-demand,” with 1) heavy expectations growing for an RBA rate cut (weak housing data and the release of minutes which “checked the bank’s plumbing” as is typical ahead of potential easing sees AUD 3Y yields drop below the 1.5% cash rate for the first time since 2016) as well as 2) a very strong bid in the 20Y JGB auction overnight

- Yesterday’s early US yield curve steepening reversed over the course of the day (and despite heavy US IG calendar) to close meaningfully ‘flatter,’ which smelled-like profit-taking from said ‘steepener’ bets ahead of tomorrow’s Fed—ESPECIALLY in light of the “very dovish” expected outcome already priced-into the market (keep watching the 2020 ED$ calendar again nearing early Jan “peak inversion” / Red Pack back nearing highs)

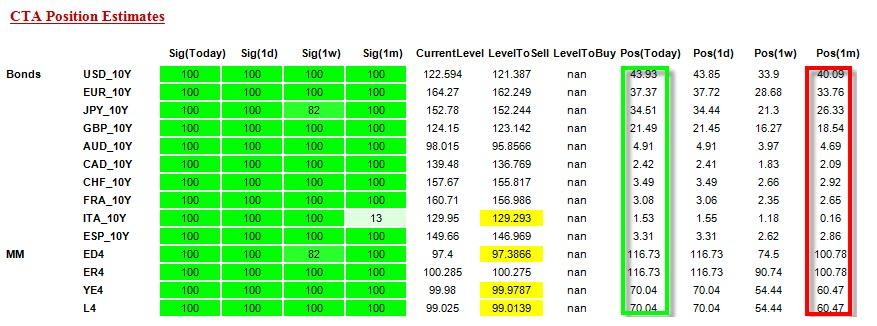

McElligott concludes by highlighting the growing trend of frontrunning QE4 by observed the “dovish/end-of-cycle/preemptive QE” market view expressed across Global DM Bonds, where all systematic strats are now showing “extreme longs” in relative Bond positioning size. Indeed, as the chart below shows, positioning among the Systematic Trend / CTA community is now “Max Long” in everything Bond/Rates (USD 10Y, EUR 10Y, JPY 10Y, GBP 10Y, AUD 10Y, CAD 10Y, CHF 10Y, FRA 10Y, ITA 10Y, ESP 10Y and ED4 / ER4 / YE4 and L4):

In other words, the buying panic in everything continues (just note the ongoing meltup in stocks) which is to be expected, now that “event risk” has become a joke.

via ZeroHedge News https://ift.tt/2Tkpd8d Tyler Durden