Global stocks and US equity futures rose in a broad rally to end the strongest quarter for global markets since 2012 (and for the S&P since 2009) while bond yields rebounded after a prolonged slide on growth worries amid renewed “trade talk optimism” after Bloomberg reported overnight that U.S. negotiators have been working “line-by-line” through the text of the trade truce agreement and Steven Mnuchin said he had a “productive working dinner” the previous night in Beijing.

On Friday, Treasury Secretary Steven Mnuchin and U.S. Trade Representative Robert Lighthizer held meetings in Beijing to ensure there were no discrepancies in the English and Chinese-language versions of the text, and also to balance the number of working visits to each capital,

.@USTradeRep and I concluded constructive trade talks in Beijing. I look forward to welcoming China’s Vice Premier Liu He to continue these important discussions in Washington next week. #USEmbassyChina pic.twitter.com/ikfcDZ10IL

— Steven Mnuchin (@stevenmnuchin1) March 29, 2019

And yet, while traders saw this as signs of optimism, the reality is that this was only necessary because the two sets of drafts appeared to differ substantially, and the focus on the joint wording “has become a key issue after U.S. officials complained that Chinese versions of the text had walked back or omitted commitments made by negotiators.” The two sides have very different understandings of certain words, according to one of the officials, who noted that China’s Vice Commerce Minister Wang Shouwen started his career as a translator at the ministry.

As always expect lots of noise on the trade front and little to no signal, although markets will look for any excuse to window dress stocks sharply higher today. Sure enough, futures on the S&P 500, Nasdaq and Dow Jones all rose, and despite recent turbulence, the S&P 500 gained 12.3% so far this quarter, on pace for the best quarterly performance since 2009.

The MSCI World Index was up 0.17% on the day, and was set to post its best quarterly performance since March 2012

European markets opened higher, with the European STOXX 600 index up 0.4 percent. France’s CAC 40 index led gains, up 0.77 percent, while Britain’s FTSE 100 index was up 0.6 percent. Germany’s DAX rose 0.4 percent with miners and retailers leading the way higher.

Earlier, stocks rose across Asia, with China stocks leading gains across regional equity markets with U.S.-China trade talks underway in Beijing; Shanghai Composite and CSI 300 indexes both on course for their best quarter since 2014; The MSCI Asia Pacific Index was up 9% in 1Q.

“Our base case is for the current tariff truce extension to yield only a partial resolution, including select U.S. tariff rollbacks in exchange for some Chinese concessions on imports, market access and intellectual property,” strategists at UBS wrote in a note to clients.

European sovereign bond yield were marginally higher and the euro slumped even as German unemployment fell to a fresh record low. Even so, German and French government bond yields were poised on for their biggest monthly falls since June 2016, ending a month where heightened anxiety about global growth prospects have sparked a flood into fixed income globally.

“We have moved a lot in the last two weeks so there is a bit of pause for now,” said Pooja Kumra, European rates strategist, TD Securities.

In the US, the 10Y Treasury yield edged up to 2.4263% from a 15-month low of 2.352% touched on Thursday after an almost relentless fall since the Federal Reserve’s dovish tone last week sparked worries about the U.S. economic outlook, after Thursday’s latest Q4 GDP revision showed U.S. economic growth was slower than initially thought growing a revised 2.2% from an earlier reading of 2.6%.

In overnight central bank news, Fed’s Bullard said the normalization process in US is at an end and suggested they have gone as far as they can. Bullard also commented that it is premature to consider a rate cut now and that he sees a likely rebound in economic growth during Q2 and the rest of 2019.

In the latest Brexit news, UK House of Commons speaker selects no amendments for debate today. A UK government source confirmed they were laying a motion to give MPs a vote on the withdrawal agreement only for Friday without the political declaration on the future relationship between the EU and the UK, while a government source said the vote to approve the withdrawal agreement would meet the EU’s test to extend A50 to May 22nd and is said to be substantially different to MV3. UK government ministers privately suggested a general election will be called if Friday’s vote is rejected or things “fall apart”, according HuffPost’s Paul Waugh. Elsewhere, there were comments from House Speaker Bercow that the new government motion meets his tests and only covers withdrawal agreement, while Sun’s Tom Newton Dunn reports it will occur at 14:30GMT/10:30EDT. In any case, there is little expectation in the EU today that the Withdrawal Agreement will pass and as such, the EU mood is one of resignation now, according to BBC’s Adler. However, a last minute burst of optimism emerged after SNP’s Gray says some Labour MP’s are preparing to back PM May’s agreement.

In FX, the Bloomberg Dollar Spot Index headed for its best week in seven amid stronger equity markets and optimism about a possible U.S.-China trade agreement. Quarter-end flows clouded the short-term outlook in the major currencies, providing choppy price action at times. The euro was initially lower, sliding as much as 1.121, before rebounding sharply to $1.1235, following speculation that today’s Brexit vote just may pass; even so it was headed for its worst month since October, weighed down by fears about economic growth and cautious signals from the European Central Bank. The Euro has also been weighed down by speculation the ECB will introduce a tiered deposit rate, providing a sign that policymakers plant to keep interest rates low for longer.

The Turkish lira continued its slid, dropping 1.7%, a day after it had plunged 4 percent. President Tayyip Erdogan blamed the currency’s weakness on attacks by the West ahead of nationwide local elections on Sunday. TD Securities recommended a lira short whereby it urged clients to buy USDTRY calls targeting 7.9 after this weekend’s elections pass.

The big mover, however, was the British pound, which fired slumped as low as $1.3004 after sliding more than 1 percent the previous day, before rebounding sharply higher above 1.31 on speculation that some Labour MPs may back May’s deal. It looks like it will be another nailbiter until the end.

Sterling had taken a knock as the prospect of a swift agreement on Brexit faded with the British parliament yet again failing to agree on a way forward.

In commodities, oil extended gains as the OPEC+ coalition’s production cuts supported prices, putting crude markets on track for their biggest quarterly rise since 2009. WTI trade at $59.76 per barrel, up 0.8 percent on the day and recovering from Thursday’s low of $58.20.

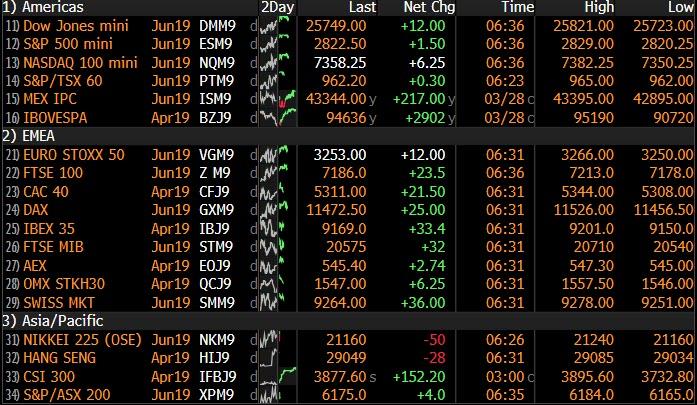

Market Snapshot

- S&P 500 futures up 0.4% to 2,832.25

- STOXX Europe 600 up 0.4% to 378.18

- German 10Y yield unchanged at -0.068%

- Euro up 0.06% to $1.1228

- Brent Futures up 0.4% to $68.08/bbl

- Italian 10Y yield rose 3.2 bps to 2.132%

- Spanish 10Y yield fell 0.4 bps to 1.086%

- MXAP up 0.6% to 159.47

- MXAPJ up 0.7% to 527.75

- Nikkei up 0.8% to 21,205.81

- Topix up 0.6% to 1,591.64

- Hang Seng Index up 1% to 29,051.36

- Shanghai Composite up 3.2% to 3,090.76

- Sensex up 0.1% to 38,595.64

- Australia S&P/ASX 200 up 0.08% to 6,180.73

- Kospi up 0.6% to 2,140.67

- Brent Futures up 0.4% to $68.08/bbl

- Gold spot down 0.1% to $1,288.79

- U.S. Dollar Index up 0.05% to 97.25

Top Overnight News from Bloomberg

- Chinese and U.S. negotiators are working line-by-line through the text of an agreement that can be put before President Donald Trump and counterpart Xi Jinping to defuse a nearly year-long trade war, according to officials familiar with the matter

- Federal Reserve Bank of New York President John Williams, one of the U.S. central bank’s top policy makers, downplayed fears of recession risks being signaled by bond markets. James Bullard, president of the St. Louis Fed, said he expected second-quarter growth to rebound after a sluggish start to the year and calls for a rate cut were “premature.”

- White House economic adviser Larry Kudlow said Thursday the Trump administration is prepared to keep negotiating with China for weeks or even months to reach a trade deal that will ensure the world’s second- largest economy improves market access and intellectual-property policies for U.S. companies

- Japan’s industrial production rose in February, though it wasn’t enough to signal a turnaround from months of declines as weak overseas demand weighs

- Oil heads for its best quarter in almost 10 years as the OPEC+ coalition’s production cuts and the loss of barrels due to U.S. sanctions on Iran and Venezuela outweighed a wobbly demand outlook

- With overseas holdings already at record levels, the April 1 inclusion of a slice of China’s near-$13 trillion of onshore bonds in a Bloomberg Barclays index will usher in fund managers who use the benchmark. Strategists see $100 billion or more flowing in in 2019 and for years to come

- A jumbo wager on an Australian interest-rate cut has emerged again, stoking speculation the same trader is hoping to strike gold at the third attempt.A splurge of buying has seen open interest in Australia’s April bank bill futures jump almost 30 percent so far this week to the highest since May 2016, suggesting sizable new longs are being built

- London continued to lead the U.K.’s weakening property market at the start of 2019, with values falling the most since the financial crisis a decade ago

- German unemployment fell to a fresh record low, suggesting that the country’s buoyant services sector is offsetting weakness in manufacturing

- Russia and Iran’s energy ministers will discuss a possible extension of the OPEC+ agreement to curb oil production when they meet in Moscow next week

- As Treasury issuance outstrips crisis-era records, the rising share of government bonds in market-weighted fixed-income indexes is pulling in more global investors

Asian equity markets were higher across the board as the region took impetus from the US, where all major indices finished positive and trade-sensitive sectors outperformed on optimism as US-China high-level talks resumed in Beijing. ASX 200 (+0.1%) eked mild gain as most sectors remained afloat heading into quarter-end although gold miners were heavily weighed after the precious metal succumbed to the pressure from a firmer greenback. Nikkei 225 (+0.8%) was driven by currency weakness with Daiichi Sankyo surging nearly 16% to hit limit up and a record high after it signed a USD 6.9bln collaboration and commercialization deal for its cancer drug with AstraZeneca in which it will receive an upfront payment of USD 1.35bln. Elsewhere, Hang Seng (+1.0%) conformed to the upbeat tone and the Shanghai Comp. (+3.2%) outperformed as trade discussions continued in Beijing and after China announced electricity and fuel costs reductions ahead of incoming VAT cuts. Huawei also supported the risk appetite after it posted a 25% increase in annual profits despite the ongoing US tiff, although not all stocks benefitted as some contended with disappointing earnings including China’s largest lender ICBC which fell short of FY net forecasts after flat Q4 profits. Finally, 10yr JGBs were lower as the fixed income complex eased from the rampant inflows seen this week and as gains in stocks dampened demand for safe-haven assets, although downside was limited with the BoJ also in the market for JPY 710bln of JGBs in the belly to super long-end.

Top Asian News

- Japan’s Job Outlook Brightest in Decades. Pity About the Wages

- Foreigners Dive Back Into China Stocks, Buy Most Since December

- Bet on Philippine Boom Pays Off for This Top-Performing Manager

- Jet Airways Is Said to Miss Paying $109 Million Loan From HSBC

A relatively upbeat start for European equities [Euro Stoxx 50 +0.5%] following on from a stellar performance in Asia, wherein the Shanghai Composite ended the week higher in excess of 3% as US-Sino talks concluded on a seemingly positive note. Broad based gains are seen across major indices, UK’s FTSE (+0.5%) is keeping its composure amid the Brexit-induced weakness in the Sterling and as heavyweight mining names benefit from the surge in base metal prices: [Antofagasta (+2.6%), Glencore (+2.4%), Anglo American (+2.1%) and Rio Tinto (+2.0%)]. Sector-wise, material names lead the gains, whilst consumer discretionary names benefit from positive broker moves for Kering (+1.4%), LVMH (+1.2%) and Richemont (+0.9%). Looking at individual movers, Wirecard (-6.9%) shares plumb the depths following yet another FT article which noted that half the company’s revenues come from partners whilst noting that at some of them there is a mismatch with reality on the ground. A Wirecard executive has noted the article in incorrect and misleading. Elsewhere, yet more trouble for Scandi banks with Swedbank (-9.5%), Nordea Bank (-9.8%) lower after New York regulators reportedly expanded money laundering scandal probe into Nordea Bank.

Top European News

- H&M Surges as Earnings Beat Analyst Estimates on Fewer Discounts

- Altice Jumps as Drahi’s Carrier Predicts Higher French Growth

- Italy’s Nexi Says IPO Offering Value Seen at EU1.9b- EU2.2b

- Pound Reverses Gains as Chance May’s Brexit Deal Passes Seen Low

In FX, USD – The Greenback remains firm overall, but has lost a bit of momentum against a few G10 and other counterparts at the start of the final trading session of the week, month and quarter as latest US-China trade talk reports suggest more progress made. However, the DXY has nudged above the 97.300 level that capped its advances yesterday and in doing so crossed a key Fib at 97.245 (76.4% retrace of the fall from 97.711 to 95.735), which bodes well from a chart standpoint ahead of potentially pivotal data including Chicago PMI and a trio of Fed speakers (Williams, Kaplan and Quarles).

- NZD/AUD/CAD – Bucking the broad trend on the aforementioned constructive US-China vibes, but with the Kiwi also getting a much needed fillip from ANZ’s consumer sentiment survey overnight showing an improvement in March. Nzd/Usd rebounded to just over 0.6800 at one stage, but then pared gains on more dovish RBNZ impulses, albeit indirectly as JPM updated its 2019 outlook for NZ rates with back-to-back cuts now seen in May and June. Similar story for the Aussie that briefly reclaimed 0.7100 before fading, while the Loonie is still relatively rangebound between 1.3420-45 ahead of Canadian PPI data.

- JPY/EUR/CHF/GBP – All softer vs the Usd, with the Jpy extending its retreat from a fraction shy of 110.00 to circa 110.92 amidst reports of Japanese selling for FY end on top of the general improvement in risk sentiment. However, supply is said to be sitting at 111.00 and the recent 110.96 peak is still providing technical resistance. The single currency is holding just above 1.1200 with buying interest touted from 1.1210 down to the figure and decent option expiry interest also supporting as 1.5 bn rolls off at the NY cut vs 1.2 bn from 1.1250-60. The Franc is essentially flat vs the Buck and Euro around 0.9950 and within 1.1190-65 parameters respectively following SNB comments on Thursday reinforcing the commitment to maintain NIRP and intervention given the Chf’s ongoing high valuation and fragility in the currency markets. Last, but by no means least heading into yet another crucial Brexit vote in the HoC, the Pound is depressed with Cable almost losing the 1.3000 handle despite a big buy order at 1.3010 and Eur/Gbp pivoting 0.8600 where a sizeable 1 bn expiries reside and run-off only 30 minutes or so before the Parliament decide whether to back the WA.

- EM – In contrast to partial recoveries elsewhere, the Lira has lurched to new lows vs the Dollar not far from 5.6600 as the run continues almost relentlessly, and with little last respite from a narrower than forecast Turkish trade deficit.

In commodities, WTI (+0.8%) and Brent (+0.6%) futures are on the front foot thus far amid the overall positive risk sentiment around the market as US-China talks are to continue next week after concluding in Beijung on a positive note. WTI futures extended gains above USD 59.00/bbl and remain in relatively close proximity to USD 60.00/bbl whilst Brent futures reside around USD 67.50/bbl. In the month of March, Brent Crude advanced around 1.6% whilst WTI crude posted gains in excess of 4%. In terms of recent energy news-flow Russian Energy Minister denied the report that Russia will only agree to extend output cut deal by 3 months and said Russia and Iran potential extension of OPEC+ deal. This follows source reports yesterday that OPEC and Russia could agree to a 3-month extension of the current agreement at the June meeting. Elsewhere, Gold ekes mild gains following yesterday’s slump below USD 1300/oz. Meanwhile, copper and iron are extending on earlier gains as optimism surrounding trade talks bolster the base metals. Russia Energy Minister denies report that Russia will only agree to extend output cut deal by 3 months and said Russia and Iran potential extension of OPEC+ deal. (Newswires) This follows source reports yesterday that OPEC and Russian could agree to a 3-month extension of the current agreement at the June meeting.

US Event Calendar

- 8:30am: Personal Income, est. 0.3%, prior -0.1%; Personal Spending, est. 0.3%, prior -0.5%

- 8:30am: PCE Deflator YoY, est. 1.4%, prior 1.7%; PCE Core YoY, est. 1.9%, prior 1.9%

- 9:45am: MNI Chicago PMI, est. 61, prior 64.7

- 10am: New Home Sales, est. 619,500, prior 607,000; New Home Sales MoM, est. 2.06%, prior -6.9%

- 10am: U. of Mich. Sentiment, est. 97.8, prior 97.8; Mich. Current Conditions, prior 111.2; Expectations, prior 89.2

DB’s Jim Reid concludes the overnight wrap

Welcome to the last business day of Q1, a quarter that most market participants will remember more fondly than Q4 2018. Craig is skiing at the moment but assuming he’s not like me and doesn’t get injured every time he steps foot on the snow, he’ll be doing the usual performance review when he’s back on Monday. Today is also the day that 1008 days after the Brexit vote, the UK was supposed to leave the EU. However if I had to make a spread as to how many more days the UK will continue to be in the EU I don’t think I’d quite know where to start. Anywhere from 14 to infinity. I’m happy to trade on this spread if anyone wants to. I’ve ordered a bit of furniture for our new house from Italy and yesterday I enquired as to when it might arrive. The guy on the other end of the phone then proceeded to tell me that there was something called Brexit that was going on and told me all about how it was going, his views on every politician involved, and that the risks to his business (and to my table) of a no deal Brexit. By the end of the conversation I was none the wiser about when it will arrive. Suffice to say that if you’re reading this in Italy and you need a new table and there’s a no deal Brexit, then I may be in a position to do business.

Today we will get a fresh vote on the Withdrawal Agreement (WA) at about 2:30pm but only the WA part and not the Political Declaration on the Future Relationship as with the two previous votes. Maybe I’ll get my chairs but not my table then. The government hopes that by separating out the two, the WA could have a greater chance of success. Furthermore, it satisfies Speaker Bercow’s criteria that the vote must be on something different to last time. The other thing it satisfies is the EU’s criteria from their European Council meeting last week that in order to get an extension of the Brexit deadline from the 12 April to 22 May (the day before the European Parliament elections begin), the House of Commons just needs to approve the WA.

However, it’s not obvious that this will help the government win, with Labour’s shadow Brexit Secretary, Sir Keir Starmer, saying that if the two were separated, “that would mean leaving the EU with absolutely no idea where we’re heading. That cannot be acceptable, and we wouldn’t vote for that.” And on the other side, one of the main reasons the ERG and DUP MPs have been opposed to the deal has been the backstop, which is a part of the WA.

Another issue is that this risks complicating the ratification process, as in UK law under the European Union (Withdrawal) Act 2018, to ratify the WA it requires that both the WA and the framework for the future relationship have been approved in a motion by the House of Commons. Therefore, unless new legislation were passed that changed this requirement, the political declaration on the future relationship would still need to be approved in a motion by the House of Commons before the WA could be ratified. Maybe the benchmark for any defeat today will be how it compares to the indicative votes supporting a second referendum and the Customs Union – the two that got closest to a majority.

Sterling weakened against every other G10 currency yesterday (-1.10% vs USD but +0.2% this morning), although other UK assets performed strongly, with sterling’s decline supporting the FTSE 100 (+0.56%) to outperform other European indices yesterday, while UK 10yr gilt yields fell -1.2bps yesterday, the only major European country to see ten-year debt yields fall.

In the US-China trade negotiations, Trade Representative Lighthizer and Secretary Mnuchin will be continuing talks today, before China’s Vice Premier, Liu He, returns to Washington for further talks next week. Treasury Secretary Mnuchin has said overnight that they had a “very productive” working dinner yesterday with Chinese negotiators. National Economic Council Director Kudlow said yesterday that they are willing to extend the talks if necessary, saying that “If it takes a few more weeks, or if it takes months, so be it.” Kudlow also addressed the Commerce Department’s report on auto tariffs, which President Trump is currently reviewing. A decision on whether or not to impose broad import tariffs on the sector was supposed to come within 90 days of the report’s submission. That would put the deadline at May 19 for an announcement, but Kudlow said that Trump “could take longer” to reach a final decision.

Asian markets are responding to the Mnuchin headline and the positive Wall Street lead this morning with China’s bourses leading the advance – the Shanghai Comp (+2.54%), CSI (+3.21%) and Shenzhen Comp (+2.60%) are all up. The Nikkei (+0.78%), Hang Seng (+0.77%) and Kospi (+0.42%) are also up. Elsewhere, futures on the S&P 500 are up +0.18%. In terms of overnight data releases, we saw Japan’s February industrial production in line with consensus at +1.4% mom, marking the first gain after three consecutive negative readings while the February unemployment rate came in at 2.3% yoy (vs. 2.5% yoy expected), matching the 25 year low set in May 2018. February retail sales came in at +0.2% mom (vs. +1.0% mom expected) with an upward revision to the previous month to -1.8% mom from -2.3% mom. South Korea’s February industrial production was at -2.6% mom (vs. -0.7% mom expected), the largest decline since February 2017, due to a drop in the production of cars and transportation equipment. Meanwhile the UK’s March GfK consumer confidence number was unchanged compared to prior month at -13 (vs. -14 expected).

Before this US equities advanced yesterday perhaps helped by some slightly positive real-time economic data (more below). The S&P 500, DOW, and NASDAQ rose +0.36%, +0.36%, and +0.34%, with gains fairly broad-based. The main laggard was utilities, as rising rates pressured the bond-proxy sectors. Earlier in the day, European indexes had a mostly negative day, with the STOXX 600 down -0.12%, though the DAX did eke out a +0.08% gain. Bund and treasury yields rose +1.2bps and +2.3bps, respectively, and the US move was encouragingly driven entirely by inflation breakevens. The 10y breakeven rate rose +3.3bps, its biggest rise since January, though at 1.86%, it’s likely still a bit low for the Fed to be completely comfortable. Notably, Japanese 10-year yields are down to -0.094%. The Bank of Japan’s stated policy is to keep them “around zero percent,” so they’re approaching the edge of the potential policy range, though it’s not clear how concerned the BoJ would be at falling yields, as opposed to rising yields.

Early yesterday, President Trump asked in a tweet that “OPEC increase the flow of Oil” because “price of Oil (is) getting too high.” That initially caused WTI oil prices to drop -2.04%, but they subsequently retraced higher as the session continued to end the day near flat at $59.38 per barrel. Energy sector stocks performed in-line with the broader index, rising +0.37%. The rebound was especially striking, since it coincided with a further rally for the dollar, with the DXY index gaining +0.47%. That sent an index of emerging market currencies to its lowest level since January 3, falling -0.16% on the day.

The Turkish Lira plunged again against the dollar, down -4.16% yesterday to reach 5.5603. The central bank announced that its foreign exchange reserves rose by $2.4bn last week, easing some concerns that it was using up its firepower trying to prevent currency depreciation, which helped the currency strengthen around +1.07% off its trough. Funding markets normalized a bit, with overnight liquidity back down to 32%, down from Wednesday’s peak of over 1,300%. This morning lira is down further -0.43%.

Turning to the Fed Speakers, James Bullard, president of the St. Louis Fed, said that he expects growth to rebound in second-quarter after a sluggish start to the year while adding that calls for a rate cut were “premature.” Elsewhere, John Williams, president of the New York Fed, said that “the most likely case” was for U.S. growth of 2% with the economy continuing to add jobs amid low unemployment and added that “I still see the probability of a recession this year or next year as being not elevated relative to any year.” On inversion of the yield curve, he said that “there’s a lot of reasons to think that it has been a recession predictor for reasons in the past that kind of don’t apply today,” and “I think it’s telling us that growth will be pretty modest” in the U.S. and global economies going forward.

Data releases were mixed yesterday but there was some positive more real-time signs in the US. US Q4 GDP saw a downward revision to an annualised QoQ rate of 2.2% (vs. 2.6% in the previous estimate), while the personal consumption reading was revised down to 2.5% from 2.8%. Pending home sales also fell by -1.0% in February (vs. -0.5% expected), bringing the YoY total to -5.0%. However, initial jobless claims came in beneath expectations at 211k (vs. 220k expected), the lowest reading in nine weeks, while the previous reading was also revised down by 5k. Furthermore, the Kansas City Fed manufacturing index rose sharply to 10 in March (vs. 0 expected), with the 9 point increase being the largest since December 2016.

In the Eurozone, the economic sentiment indicator released by the European Commission fell once again in March, reaching 105.5 (vs. 105.9 expected), its lowest level since October 2016 and the 9th consecutive monthly decline. Meanwhile, German consumer prices rose by 1.5% in March (vs. 1.6% expected), the lowest level for 11 months. It’ll be interesting to see whether today’s French and Italian inflation data and Monday’s for the Eurozone paint a similar picture.

Looking to the day ahead, we have the latest big Brexit vote as well as more trade talks in Beijing between the US and China. It’s also another busy day for data. From Europe, we’ve got French and Italian CPI readings for March, in Germany we’ve got February’s retail sales figures and March’s change in unemployment, and from the UK, we’ll get the latest reading of Q4 GDP, along with February’s mortgage approvals, consumer credit, and M4 money supply. From the US, we’ll get the final University of Michigan sentiment reading for March, personal income for February, personal spending for January, the MNI Chicago PMI for March, along with February’s new home sales. In Canada, we’ll get January’s GDP figure.

via ZeroHedge News https://ift.tt/2FHnchA Tyler Durden