Another day, another round of “US-China trade talk optimism.”

Global stocks continued their drift higher to close the week, with the MSCI World Index on track for a second straight week of gains while emerging-market stocks extended their winning streak to seven days, the longest stretch in more than a year, as both China and the U.S. claimed progress in trade talks.

“Buy algos” were encouraged after both China and the US claimed progress in talks to end their trade war, with President Xi Jinping pushing for a rapid conclusion and President Donald Trump talking up prospects for a “monumental” agreement that might be announced within four weeks, although he warned that it would be difficult to allow trade to continue without an agreement. Benchmark bond yields ground higher and the dollar reached a three-week high against the yen before U.S. job data. Better-than expected industrial output data out of Germany and receding fears of a disorderly Brexit also helped perk up sentiment.

While Chinese markets were closed, US equity-index futures advanced alongside Asian stocks, European bourses and Chinese stock futures after a Xinhua report that President Xi Jinping said substantial progress had been made on the text for a trade deal. “The main overnight news, which is positive if not very substantial, is around the U.S.-China trade deal,” said Mizuho strategist Antoine Bouvet. “German industrial orders yesterday added to worries in the manufacturing sector, but industrial production today actually surprised to the upside.”

“There’s a little bit of a risk that it’s a sell-on-the-news event,” Ann Miletti, a fund manager at Wells Fargo Asset Management, said of U.S.-China trade talks. “The devil is really in the details – how good is this deal going to look?”

Europe’s Stoxx 600 traded sideways, shrugging off trade optimism and Brexit news ahead of today’s U.S. payrolls. Eurostoxx 50 is little changed, Markets in Paris and London added 0.1%. German stocks were treading water, with modest gains in basic resources and autos sectors offset by weakness in real estate and telecoms, though the index was on track for its best week since December 2016. German industrial output rose by 0% percent in February, better than the 0.5% expected, as mild weather helped a surge in construction activity. But manufacturing production dipped as Germany continues to suffer from trade friction with China and Brexit angst after narrowly avoiding recession last year. Leading economic institutes slashed their forecasts for 2019 growth on Thursday and warned a long-term upswing had come to an end.

Earlier in the session, trading volumes throughout Asia were muted, with cash markets in China and Hong Kong shut for a holiday.

S&P futures pointed to modest gains for stocks on Friday, with S&P 500 edging up 0.16% to 2,887, only 1.75% away from its Sept 2019 closing high, which is prompting some caution: “Share markets have run hard and fast from their December lows and are vulnerable to a short-term pullback,” said Shane Oliver, head of investment strategy at AMP Capital. “But valuations are okay, global growth is expected to improve into the second half of the year, monetary and fiscal policy has become more supportive of markets and the trade war threat is receding.”

Attention now turns to the March payrolls report, which is forecast to rebound to 180,000 in March, following February’s surprisingly low 20,000 rise. In focus will be hourly earnings, which climbed to 3.4% in February, the fastest pace since April 2009. Hopes for a solid number were boosted by data on jobless claims, which fell to a 50-year low last week. With traders betting that the next Fed move will be to lower interest rates, not raise them, the fixed-income market could be affected by any signs of wage strength in today’s report.

In other overnight news, President Trump commented that there would be a 25% tariff on car imports from Mexico if he decides to apply tariffs but also said that Mexico has done good regarding the border during past 4 days, while he added that he did not say the border would stay open for a year but that he would place tariffs first. Trump also confirmed he has recommended Herman Cain to the Fed board.

In the latest Brexit news, UK PM May sent a letter to EU’s Tusk proposing an extension for Brexit until 30th June 2019 with potential to terminate early should a deal be ratified before then. Letter states that the UK will begin to prepare to host European elections and that the UK needs to provide a clear plan by Tuesday (the day before the EU Council meeting). Separately, there were reports EU’s Tusk is preparing to offer the UK a 12-month flexible extension, according to a senior EU source; which has since been confirmd by a Senior EU Official. EU Council President Tusk’s proposal of a year long extension to Brexit would permit the UK to leave as early as 1st July if the UK has passed with Withdrawal Agreement by that point, according to a senior EU official.

The optimistic mood again weighed on safe-haven debt, with government bond yields in Europe and the United States rising in early trade. 10 Year US and German bond yields climbed to a two-week high, the latter just above zero, the former rising to 2.535%.

In currencies, the progress on trade was enough to keep the safe-haven yen under pressure and lift the dollar to a three-week high of 111.79. The dollar steadied before the release of U.S. payrolls data, while sterling initially advanced after the U.K. asked the EU to kick the Brexit can down the road once again, only to sink below Thursday lows after.

An index of developing-nation currencies was little changed, with Indonesia’s rupiah leading gains versus the dollar along with South Africa’s rand and Mexico’s peso. President Xi Jinping reportedly said substantial progress had been made on the text for a trade deal, raising hopes of a swift end to the dispute that has weighed on the global economy

In commodities, Brent crude futures were off 23 cents at $69.17 after touching $70 a barrel for the first time since November, as expectations of tight global supply outweighed rising U.S. production. WTI priced at $62.16 a barrel. Spot gold dipped to $1,291.61 per ounce but held above a near 10-week low hit overnight.

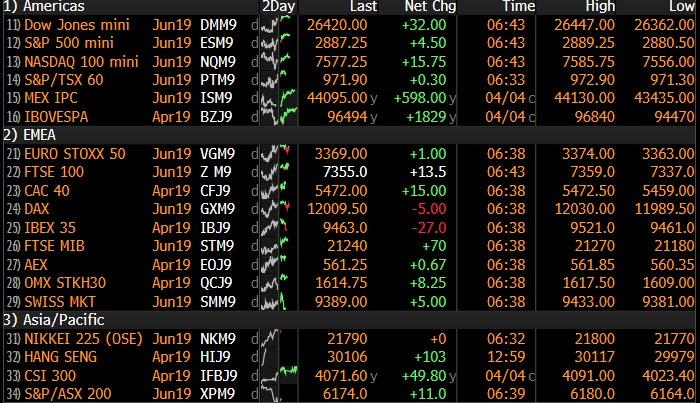

Market Snapshot

- S&P 500 futures up 0.2% to 2,887.00

- STOXX Europe 600 unchanged at 387.88

- MXAP up 0.02% to 162.40

- MXAPJ down 0.1% to 538.85

- Nikkei up 0.4% to 21,807.50

- Topix up 0.4% to 1,625.75

- Hang Seng Index down 0.2% to 29,936.32

- Shanghai Composite up 0.9% to 3,246.57

- Sensex up 0.3% to 38,802.54

- Australia S&P/ASX 200 down 0.8% to 6,181.26

- Kospi up 0.1% to 2,209.61

- German 10Y yield rose 1.5 bps to 0.009%

- Euro up 0.05% to $1.1227

- Brent Futures down 0.5% to $69.08/bbl

- Italian 10Y yield fell 2.1 bps to 2.165%

- Spanish 10Y yield rose 0.7 bps to 1.117%

- Brent Futures down 0.1% to $69.35/bbl

- Gold spot down 0.2% to $1,289.19

- U.S. Dollar Index little changed at 97.27

Top Overnight News

- Through a message passed to U.S. President Donald Trump via Chinese Vice Premier Liu He, President Xi called for an early conclusion to trade negotiations, the official Xinhua News Agency said. Liu, who took part in talks this week in Washington, said the two sides had “reached new consensus on such important issues as the text” of a trade agreement, according to Xinhua

- A potential U.S.- China trade agreement could face challenges from other World Trade Organization members depending on the details and whether other nations feel it unfairly hurts them, the group’s chief said.

- May’s request for another Brexit postponement sets up a battle with the EU ahead of a key summit next week. Tusk favors a 12-month extension that could be ended early if a withdrawal deal is approved before the year is up, according to an EU official

- German Chancellor Angela Merkel reiterated her vow to do everything she could to avoid a no-deal Brexit, while maintaining solidarity with Ireland

- Cleveland Fed President Loretta Mester, answering a question about the likelihood the next policy move will be a cut rather than a hike, says “I’m biased to either keeping rates where they are or moving them up a little bit”

- President Trump intends to nominate Herman Cain, the former pizza company executive who ran for the 2012 Republican presidential nomination, for a seat on the Fed Board, according to people familiar

- China has drafted rules to regulate the nation’s $109 billion peer-to-peer lending sector as part of a plan to clean up the market by 2020, according to a document seen by Bloomberg

- Norway’s $1 trillion sovereign wealth fund got the go-ahead to cut emerging markets from its fixed income holdings as part of an overhaul of its $310 billion bond portfolio

- Italy’s cabinet approved a series of measures to boost the economy, even as the Treasury prepares to slash growth forecasts for the year and raise its projected budget deficit

Asian equity markets traded slightly mixed following a similar indecisive lead from Wall St. as US-China trade optimism was partially offset by pre-NFP caution and holiday thinned conditions from closures across the Greater China region. ASX 200 (-0.8%) was the laggard and extended on its pullback from 7-month highs, with the declines led by tech which mirrored the underperformance of the sector stateside. Nikkei 225 (+0.4%) was positive with the index underpinned by favourable currency moves and trade-related hopes, while the KOSPI (+0.1%) remained afloat as index giant Samsung Electronics weathered a miss on its Q1 earnings guidance. Chinese markets were shut for national holidays although there was certainly no lack of relevant news flow with trade talks remaining in the limelight, in which leaders from both sides noted substantial progress was made and President Trump suggested that a deal could be announced in the next 4 weeks. Finally, 10yr JGBs were pressured amid spill-over selling from T-notes and as stocks in Japan remained afloat, while the BoJ were only present in the market today for T-bills. US President Trump said rapid progress is being made in trade discussions with China and we’re getting very close to trade deal, but added it is not yet made and could be announced in the next 4 weeks, maybe more or less. Furthermore, US President Trump said he will hold a summit with Chinese President XI in Washington if there is a deal and that he will discuss tariffs with Chinese Vice Premier Liu He, while he cited tariffs as well as IP theft when asked about sticking points.

Top Asian News

- Jokowi Gambles on Rural Voters as Discontent Grows in Cities

- India Didn’t Shoot Down Pakistan’s F-16, U.S. Magazine Says

- Energy Tycoon $1 Billion Richer as Vietnam Bet Boosts Stock

- Lucrative Coal Trade Beckons Those Bold Enough to Test China

A cautious start for European equities [Euro Stoxx 50 Unch] after a relatively mixed Asia-Pac session, as is usually the case ahead of US jobs data. Italy’s FTSE MIB (+0.4%) modestly outperforms its peers as Saipem (+3.0%) rose to the top of the Stoxx 600 on the back of a positive JP Morgan broker move. Sectors are mixed with no clear standout.

Top European News

- May Writes to Tusk Seeking to Delay Brexit to June 30

- France Backs Banking Consolidation Amid German Merger Talks

- Swedbank Chairman Quits as Scandal Rips Through Top Ranks

- There Is an Art to Issuing a ‘Good’ Profit Warning, RBC Argues

In FX, AUD/NZD/GBP/EUR all bucked the broader trend of consolidation and sideways trading into NFP and Canada’s latest employment report, albeit not by much in terms of moves vs the Greenback. However, the Aussie has extended its rebound from post-RBA lows and outperformance vs the Kiwi in the process. Aud/Usd has retested recent 0.7100+ peaks as Aud/Nzd advances through 1.0550 towards 1.0575 and Nzd/Usd declines to new early April lows below 0.6740. The catalysts, more momentum towards a US-China trade agreement, per latest reports from Beijing especially, another rise in iron ore prices and a supportive Aussie note from GS that Is going against the grain with an unchanged RBA policy call to support its revised forecasts for Aud/Usd over 3 and 6 month horizons (0.7400 and 0.7500 from 0.7200 and 0.7300 respectively). Recall, the US bank also went long of Aud/Nzd yesterday and decent option expiry interest sits at the 0.7100 strike (1.6 bn). Elsewhere, Cable remains volatile and fixated on Brexit headlines around the 1.3100 handle amidst latest reports about a potential lengthier A 50 extension to mid-year or end March 2020 with a flexible early termination option. Eur/Usd is still rangebound between 1.1200-50 after topping out not far above a 1.1246 Fib again on Thursday, but deriving some underlying support from better than expected German IP data and Italy’s ISTAT suggesting that its leading economic indicator points to signs of a recovery or base. Note also, hefty option expiries may be keeping the headline pair in check, as 2 bn resides between 1.1185-1.1200 and 2.5 bn from 1.1240-50.

- CHF/CAD/JPY – Minimal deviation against the Usd that is equally restrained pre-US and Canadian labour updates, with the DXY firm, but confined between 97.177-331. The Franc is pivoting parity and Loonie straddling 1.3350, while Usd/Jpy is just off a marginal new wtd high of 111.80 having breached its 200 DMA (111.49).

- EM – Contrasting fortunes for regional currencies as the Lira continues to lick wounds amidst the ongoing political contention following local Turkish elections and wrangling with the US over its S-400 order from Russia. Moreover, Usd/Try remains elevated near 5.6000 ahead of next week’s Economic Plan and the next CBRT policy meeting, in contrast to Usd/Zar below 14.1000 and not far from the 100 DMA (14.0625) in wake of SA’s ratings reprieve for the Rand by Moody’s earlier this week.

In commodities, tentative trade in the energy complex as WTI (Unch) and Brent (-0.3%) gear up for this week’s US jobs data. WTI rests just above its 200 DMA at 61.38, whilst its global counterpart straddles just below its 200 DMA at 69.54. Oil is on track for its longest weekly winning streak since the back-end of 2017, overall supported by the output decline in Venezuela coupled with growing hope of a US-Sino trade truce. Crude has advanced around 40% this year thus far as OPEC+ supply curbs counter record high US shale production. As a reminder, tonight will see the release of the Baker Hughes rig count, although price-action may be muted amidst macro-newsflow. Not much price action in the metals complex (thus far) with gold (U/C) treading water around yesterday’s close after briefly breaching its 200 DMA (1283) to the downside yesterday, whilst copper (-0.1%) remains tentative amidst the cautious risk-tone. Finally, Australia’s Port Hedland’s iron ore shipments to China declined by 8% M/M, totalling 30.7mln tonnes vs. 33.5mln tonnes in February after the port was shut for almost 4 days due to cyclones hitting Western Australia.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 177,000, prior 20,000

- Unemployment Rate, est. 3.8%, prior 3.8%

- Average Hourly Earnings MoM, est. 0.3%, prior 0.4%; YoY, est. 3.4%, prior 3.4%

- Average Weekly Hours All Employees, est. 34.5, prior 34.4

- 3pm: Consumer Credit, est. $17.0b, prior $17.0b

DB’s Jim Reid concludes the overnight wrap

Good morning from Munich, one of my favourite cities in Europe and not just because Liverpool beat them in the Champions League last month. It always brings back memories when I pass the Bayerischer Hof in Munich as when I was staying there in 2002 on a work trip unbeknown to me Liam Gallagher of Oasis was also there at the same time and evidently required some major dental work after a fracas in the hotel nightclub. It was all over the newspapers on my return. Fortunately I was long tucked up in bed when it happened.

Markets were certainly waiting for something to get their teeth stuck into for most of yesterday as everyone awaited the news of the Trump-China VP Liu He meeting and also held fire ahead of today’s payrolls. The former ended after the US markets closed last night. The officials announced no major breakthrough on trade talks but the direction of travel seems to continue to be positive. Trump did float a potential timeline: four more weeks of talks, then two weeks to schedule and attend a summit with President Xi. He said that IP protections, certain tariffs, and enforcement are all still being negotiated. In the meantime, Chinese President Xi Jinping said that substantial progress has been made in trade talks with the US and called for an early conclusion of the US-China trade text.

Equity markets in the US were already shut by the time those headlines hit however sentiment overnight in Asia is slightly on the positive side with the Nikkei (+0.41%) up and Kospi (+0.04%) flatish. Markets in China and Hong Kong are closed for a holiday. Elsewhere futures on the S&P 500 are up +0.15% and 2y and 10y treasury yields are up c. 1bps this morning.

How markets fare today will likely be dictated by the March employment report in the US this afternoon. A reminder that last month we had that huge plunge in payroll growth to just +20k which was the lowest since September 2017 and the third lowest since January 2011. Expectations are for a bounce back 177k print however that is still below the average of the last three (186k), six (190k) and twelve (212k) months. To be fair there is a decent range on the Bloomberg survey at 110k to 277k. Our US economists have a 165k forecast and they note that the hostile weather in mid-March also raises the risk of another downside miss. As for earnings, the consensus is for a solid +0.3% mom reading (DB at +0.2% mom) which should keep the annual rate at +3.4% yoy. The unemployment rate is also expected to hold steady at 3.8%. So lots to look out for as ever.

Back to yesterday and it wasn’t an overly exciting day in markets with the S&P 500 (+0.21%) advancing a bit as gains for energy and materials were offset by losses for utilities and tech. The index has traded in a tight 0.93% range over the last three sessions, its second tightest of the year. The NASDAQ closed -0.05% to leave the winning run behind at five days with Tesla (-8.23%) doing some of the damage, however the DOW (+0.64%) did outperform helped by gains for Boeing (+2.89%). In Europe the STOXX 600 (-0.27%) faded to a small loss. WTI oil remained tame (-0.58%), capping its narrowest three-day trading range since last September. The moderate risk off lifted bonds with 10y Treasuries down -1.1bps and Bunds (-0.6bps) back into negative territory again. At my Munich dinner last night of 10-15 clients, I asked who thought Germany should take advantage of ultra low yields and borrow 50yr or 100yr money and invest it in their economy. Everyone raised their hands. I thought there would be a more conservative balanced response and was therefore pleasantly surprised.

Elsewhere the USD (+0.20%) was firmer which weighed on some EM currencies. The Turkish lira outperformed, advancing +0.64% (down -0.48% this morning) after Bloomberg reported that the European Bank for Reconstruction and Development as well as the World Bank’s International Finance Corporation are looking at increasing their Turkish NPL portfolios. It wasn’t clear if this was a policy change or just consistent with their standard operating procedure, but the currency rallied sharply on the headlines.

The fact that it’s taken this many paragraphs to get to Brexit suggests that there’s been a dip in the newsflow. Indeed, perhaps fitting of the current state of affairs in Parliament, the most entertaining story was a water leak forcing a debate on tax legislation in the Commons to be suspended yesterday. So a rare chance for MPs to discuss a non-Brexit topic was scuppered by rusty pipes. The only notable Brexit news was the suggestion that any more votes on Brexit proposals might not take place before PM May travels to Brussels next week. That raises the risks that Mrs May goes to Brussels next Wednesday and asks for an extension with no firm plan. That will increase the risks of a hard Brexit a week from today. I still think that’s unlikely but it will put the EU in a difficult position if no progress has been made. Talks between May and Corbyn are ongoing with Tories saying they were “productive” whereas Labour didn’t offer up any descriptive word about them. One gets the sense that both sides realise they have a lot to lose by agreeing a grand bargain however both BBC’s Laura Kuenssberg and ITV’s Robert Peston tweeted last night that their sources suggested the talks are credible and could result in something. It’s possible we’ll learn more this afternoon. Sterling closed -0.62% yesterday as the stakes were raised.

In other news, it’s worth flagging another ECB deposit tiering story yesterday, this time from the FT. The article suggested that the arguments in favour of tiering are building within the ECB camp. The story made the point that the key argument is the increasing likelihood of rates remaining at current low levels for an extended period of time. As such, tiering could be part of a package in which the ECB adjusts its forward guidance to endorse market pricing, which is no hikes until at least later in 2020.

Speaking of the ECB and tiering, the minutes from the March meeting which were out yesterday didn’t offer much in the way of new hints. The text revealed that “concerns were voiced that over time the effects of persistently low rates could depress banks’ interest margins and profitability with negative effects on bank intermediation and financial stability in the longer run. It was recalled that the consequences of low rates differed across the maturity spectrum and across banks, depending on their business models and the structure of their assets and liabilities”. Crucially, there was no direct reference to tiering.

As a final point on Europe, there were a couple of GDP downgrade headlines which hit the screens early yesterday. The first was Germany where “institutes” revised down their 2019 growth forecast to 0.8% from 1.9%. However it turned out that the 1.9% was from back in September so it wasn’t all that surprising given the six months of slowing data since then, and compares to the IFO forecast at 0.6%. Shortly after, Bloomberg reported that the Italian Treasury is set to slash its 2019 growth forecast to 0.1% from a 1.0% forecast previously. Again though, this is closer to where the market is. So both headlines were really more noise than anything else.

Turning quickly to yesterday’s Fedspeak, where the overall message was consistent with the existing policy stance. NY Fed President Williams said that “policy is in the right place” and that growth should slow to around 2% this year. Separately, two of the more hawkish committee members, Cleveland’s Mester and Philadelphia’s Harker, maintained their positions for a pause in policy for now, with Mester arguing for “no urgency to change our policy stance” and Harker saying “I continue to be in wait-and-see mode.” They both left the door open for future hikes though. Mester said if the economy evolves as she expects, then “rates may need to move a bit higher” and Harker said “my outlook for rates remains, at most, one hike for 2019 and one for 2020.” Finally, Bloomberg reported that President Trump plans to nominate former presidential candidate Herman Cain for one of the vacant Fed Governorships. He would need to be confirmed by the senate.

Wrapping up the few data prints that were out yesterday. In the US claims continued their trend of reversing the Q4 spike, dropping 10k to 202k (vs. 215k expected) and in fact to a new 49-year low. The four-week moving average is now down to 214k and the lowest since October. Prior to this, we had another disappointing factory orders print in Germany where orders fell -4.2% mom versus expectations for a +0.3% mom lift.

Finally to the day ahead now, where this morning we’ve got more data out of Germany with the February industrial production print, followed by the February trade balance print and March house price data and Q4 labour costs data in the UK. The aforementioned March employment report in the US is the highlight today while late this evening we’ll get the February consumer credit print for the US. Away from that, the Fed’s Bostic speaks this evening while the big US banks will today submit their capital plans with stress test results announced in June.

via ZeroHedge News http://bit.ly/2UlkKYb Tyler Durden