Given that the embarrassment of Lyft’s post-IPO belly flop is still fresh, the notion that Wall Street analysts are approaching Uber’s upcoming $100 billion debut with anything other than trepidation is simply baffling to us.

Didn’t Uber just admit in its S-1 that there’s a real possibility that it might never achieve profitability? And though Uber is, we supposed, the ride-share “market leader” (in both market share AND operating losses), the notion that the supposed ‘professionals’ aren’t at least a little bit skeptical of the valuation that Uber and its bankers are pushing shouldn’t be surprising.

However, for the editors at CNBC.com – who we imagine risk the dreaded “tap on the shoulder” should they publish a story that’s not at least implicitly bullish – framing the company’s coverage of the Uber IPO must have presented a particularly difficult problem, requiring them to tread carefully lest they violate the company’s reporting mandate.

Are analysts, who get paid millions of dollars a year to pick apart company’s valuations, parsing every conceivable metric, simply too conflicted to make a call on the Uber IPO?

From what we can tell, the answer is no. Because even in an industry where analysts’ opinions are occasionally influenced by the business considerations of their employer, several analysts have urged anybody thinking about buying at the IPO to think carefully about their decision before they buy.

One analyst, who was quoted by CNBC, argued that if you ignore the hype and simply evaluate Uber on its numbers, the picture isn’t so rosy.

Valuing the company at six times sales – a generous valuation, even for an established tech firm – Uber would be worth $73 billion. That would mean a $100 billion valuation is roughly 40% above fair value. And given the market’s response to the Lyft IPO, this might be a fair assessment.

Wireless Fund Lead Portfolio Manager Paul Meeks said the best way to understand the valuation is through its sales numbers. Pricing the stock at six-times sales, which he said would be “a pretty healthy valuation even for an established tech company,” Uber’s value should really be about $73 billion. Similarly, he estimated Lyft should be priced at $50 per share with a valuation of $14 billion.

Right now, Uber is going public at a time when its losses continue to grow, and the company has no clear path to profitability. And though its high valuation is largely driven by what Wedbush Securities analyst Dan Ives, widely regarded for his analysis of Apple, loosely describes as ‘Amazon-inspired FOMO’ – that is, the fear that investors might be missing out on the next Amazon, which also posted operating losses for years before finally becoming profitable – comparing Uber to Amazon is pretty tenuous.

While Ives said Uber represents the first stock in the past few years that investors view as having the potential of Amazon-level growth, comparing the two is still a fool’s errand.

“That path to profitability is fuzzy. And also comparing Uber to Amazon, it’s like comparing a great high school basketball player to LeBron James,” Ives said.

For Meeks, the comparison seems to serve as more of a warning for Uber. He noted that offering Amazon Web Services, Amazon’s cloud product, was the turning point for the stock and now is key to its profitability. As of its Q4 2018, AWS represented 58% of Amazon’s overall operating income.

But Meeks sees less opportunity in Uber’s bets outside of its core ridesharing business, like Uber Eats and Uber Freight.

“They’ll try to leverage their platform into other things, but the other things will be transport because that’s their gig and the transport business has a lot of established players,” Meeks said. Eventually, he said, “all freight will be transported by Amazon.”

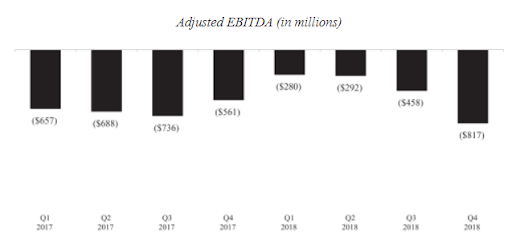

To be sure, Uber’s adjusted losses briefly improved during the first three quarters of last year, Uber’s disastrous fourth quarter mitigated any prior improvements (and as we pointed out, they it made $1 billion last year on paper, that profit was driven by the divestiture of its Southeast Asia business).

And isn’t the logic of buying Uber because you think it will be the next Amazon the same logic that crypto investors in 2017 used to justify buying every ICO because they hoped it would be ‘the next bitcoin?’

Just some food for thought.

Whether Uber soars or flops during its trading debut remains to be seen. And there are certainly analysts out there who would tell you that the company is a solid buy. But based on the contents of this CNBC article, maybe a better headline would be something like: “Analysts have serious doubts about Uber’s $100 billion valuation”.

via ZeroHedge News http://bit.ly/2v5hzVc Tyler Durden

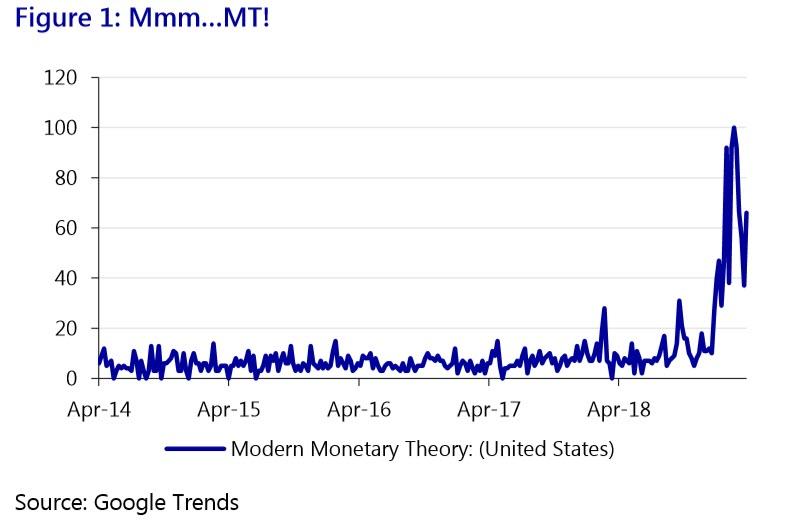

After years in obscurity, MMT is now being discussed –and dismissed– in high policy circles

Many would argue its eventual introduction in some form is inevitable

When looked at in detail MMT is not the simplistic argument its critics present it as

Some of its fresh, if old, ideas may offer new ways of looking at our present problems

However, MMT will also risk creating as many problems as it solves

As such, just try saying MMT without saying ‘Mmm’!

Mmm…MT

For those who haven’t noticed, there has been a lot of discussion about Modern Monetary Theory (MMT) in the press of late. The following headlines have appeared in the past few weeks alone:

Clearly MMT, which has actually been around for decades, is currently a hot topic at the highest levels. However, even a cursory glance above shows that it is not something there is any agreement over. By contrast, it’s divisive and very controversial.

One can also see that public interest in MMT is spiking too. Google Trends interest over time in “Modern Monetary Theory” has shot up since the end of 2018 (see Figure 1) despite it being an obscure, dry, theoretical–and yet controversial– economic-policy framework.

That is arguably the case in the US because MMT is now politically linked to US Democratic Congresswoman Alexandria Ocasio-Cortez’s “Green New Deal”, with its multi-trillion USD price-tag and radically transformative agenda.

But what is MMT?

We can agree interest in MMT is picking up, and not everyone likes it, but what exactly is it?

The answer is complicated as there is no central MMT textbook. Neither is it an accepted school of thought within market economics, or in orthodox economics departments at universities. As such, most working economists have only a passing familiarity with the name at best, and there is misunderstanding about what MMT does and doesn’t actually encompass.

So let’s start with some basics of what MMT believes before proceeding any further. As we shall see, the premises of MMT are very simple – but the implications for policy and for markets are staggering.

Don’t tax, but spend

Fundamentally. MMT argues the following three things:

Sovereign currency-issuing governments, such as the US, are financially unconstrained;

Taxes are not needed to finance government spending; and

The role of taxes is to drain money out of the economy after the government has spent it in order to manage aggregate demand and keep it in line with available supply of resources.

In short, MMT argues the government can finance any budget deficit by de facto monetization and hence has no monetary limits. That might sound ridiculous in Eurozone countries because they no longer have monetary sovereignty. However, technically this is true for economies that control their own currency. Their governments do not need to raise taxes before spending: they spend first and then tax. Moreover, such governments can provide an unlimited stock of their own currency, if needed.

For example, if a major war were to break out tomorrow, governments would immediately run very large budget deficits without worrying about how to finance them via taxation first. History shows this to be the case. So the issue is then political: what constitutes an emergency that society should focus its resources on?

Following on, if taxation is not required to finance state spending then tax is a quasi-hydraulic act to drain liquidity similar to central-bank Open Market Operations. Indeed, MMT argues that tax that is thus drained is effectively ‘destroyed’ rather than being saved, as is the case when liquidity injections are returned to the central bank via quantitative tightening (QT) after quantitative easing (QE). (Note after injecting trillions of USD into markets, the Fed’s QT is proving impossible to sustain for exactly that reason.)

From a sectoral balances perspective Godley (2005) also shows a public deficit allows the private sector to run an off-setting surplus; conversely, public austerity means the private sector must borrow. Given the public sector can monetize its debts and the private sector can’t, MMT says governments should deficit spend. (Though there is also an international dimension to this we will touch on ahead.)

Of course, this is highly controversial in an age defined by worries over high public debt levels and a push for ‘prudence’ and austerity; and readers who pay taxes will not be happy with the idea that these are destroyed rather than spent!

ProbleMMs?

So is MMT a “magic money tree”? No. MMT is more nuanced than that. For example, it recognizes that there are indeed limitations to what a government can do fiscally.

Primary is a real resource constraint: if there is no spare capacity in the economy, or the materials the government wishes to procure do not exist, fiscal sovereignty is an illusion. A poor country with no natural resources or industry and with an uneducated population cannot simply print money to build infrastructure or good universities. However, if a developed economy is suffering from high unemployment and/or a low level of capacity utilisation the same argument clearly does not apply.

MMT also recognises there is another limit to the government’s ability to finance itself: inflation. MMT fully recognises inflation is not desirable above a certain level and once self-financed fiscal stimulus exceeds what the real economy can supply such spending would have to be cut back to avoid damaging wage-price spirals – or taxation would have to increase.

Even so, from a traditional economic point of view there are still many obvious criticisms of MMT.

First, is the argument that governments cannot create money because true money is exogenous: the public being able to conjure up money is ‘voodoo’. Anyone believing there is no such thing as a free lunch has a powerful gut reaction to MMT.

Money for nothing?

Although we use the word ‘Modern’ in MMT, this is a very old debate. Plato argued money was a representation of value rather than real, while Aristotle countered money should be a real commodity itself. In our age of fiat currencies, credit cards, and now digital currencies, economics textbooks still teach the history of money as being barter > gold > credit. In other words, we are Platonic but like to think we are still Aristotelian.

By contrast, MMT is based on chartalists such as Knapp (1925), Lerner (1943), who argue money is always a political construct. Polanyi (1944) and Graeber (2011) also demonstrate the actual historical record of money is chartalist: there was never a transition barter > gold > credit; with the exception of the gold standard (18151931) the norm across human societies has been to start with local credit, rarely repaid, in order to keep the economy moving. That is a tradition which MMT builds on.

That is also a red pill/blue pill moment for many!

More ProbleMMs

Second is the argument that MMT is simply “Keynesian” fiscal stimulus via bond issuance renamed, already a well-established theory even if has become politically unacceptable in many countries obsessed with austerity. However, the ‘taxation is not needed’ argument takes us well beyond simple Keynesian fiscal multipliers.

MMT notably also does not believe in the ‘loanable funds’ view that bank loans require savings first, and that banks intermediate between savers and borrowers rather than creating money (in the form of debt) when they make loans de novo. Notably, while economics textbooks still teach loanable funds, the Bank of England admits this is not how money creation and banking operates – it is de novo; MMT then posits the government has greater powers of money creation than banks in this regard given public liquidity does not require a liability to be created at the same time. If a bond is issued under Keynesian theory then a liability and an asset are created; but that bond can be bought by the central bank with electronically ‘printed’ money and the liability de facto removed under MMT. Just think of the trillions of USD of QE injected by central banks, which is now NOT to be reversed by QT.

Yet that leads to the third criticism, the government is not the actor that would finance itself: that role falls to the central bank. Naturally, central bank independence would have to end under MMT. While a dual inflation and fullemployment mandate already exists at key central banks such as the Fed, and inflation-targeting might still be built into a new MMT policy framework, clearly the central bank would be primarily focused on aggregate demand by providing blank cheques to government spending, not CPI.

Fourth, and a crucial corollary, interest rates become largely irrelevant under MMT. The cost of money would not matter as much as the quantity of money (i.e., the supply of funds into the real economy fiscally). Indeed, MMT suggests that interest rates should be set to zero. If not, mixed fiscal-monetary targets would prove confusing.

Yet a fifth issue then emerges: how would the government yield curve respond under MMT? The curve would start very low and flat. However, what if MMT succeeds in achieving inflation? Bond yields would rise – and could the government then cover higher debt-servicing costs if the resources/inflation threshold has been successfully breached, meaning MMT must be ‘turned off’? If so, the economy would lurch back into recession again – necessitating more MMT!

And MMore ProbleMMs

Or would we instead need to see bond yields capped – as in Japan today under their policy of Yield Curve Control (YCC)? If so, that would likely destroy a real market for benchmark government bonds.

Of course, the government yield curve is not the only one that matters. How would the corporate bond market respond to this kind of MMT environment? Would the state have to step in and cap private-sector bond yields too? And what about asset prices such as property? What would be done there?

There are also other issues. Consider that a key part of MMT is a commonly-linked policy of funds being used for a public Employer of Last Resort or Jobs Guarantee programme to generate non-inflationary full employment. That is certainly part of the proposed US Green New Deal, for example.

The issues here should be obvious. While the Phillips curve is broken under our present global model that strengthens capital vis-à-vis labour bargaining power, under MMT it would rapidly return. Wage inflation would then rise again – and all of the interest rate/yield curve issues mentioned above would arise with it.

At the same time, as the government plays a larger role in the economy, as in the proposed Green New Deal, it risks genuinely crowding out the private sector, not from a financing perspective but in physical terms. Even if the state is merely financing private firms to do the required work, in infrastructure, for example, elements of political direction would no doubt still occur over time.

Clearly, the overarching question that needs to be answered is what kind of institutional architecture can be created for MMT to work through the economic cycle without warping markets (further than QE already has)? How can one ensure that fiscal taps are turned off once inflation appears, and that the state does not distort both the real economy and financial markets? Fiscal policy has far longer lag times than interest rates, for example: would it really be more efficient to build half a bridge and then stop because inflation rose too fast?

In short, this would require an entirely new political economy that remains elusive in its definition if not in its ambition: that has been clear since Lerner (1943) and Kalecki (1943). Yet as shown, that utopian new institutional framework could produce its own instability even as it cures our present New Normal.

Zero rates, zero alternatives?

While this is a strong theoretical rebuttal of MMT, interest rates in Japan and Europe are nonetheless already negative, and in other economies the drift towards ‘Japan-ification’ seems inexorable. In short, we seem to be heading in the direction for an MMT starting base (zero rates) whether we like it or not. Once the US Fed starts cutting interest rates again, that dynamic will become even more obvious. This is no surprise to MMT: Kalecki (1943) recognised giving capital too much power relative to labour would ultimately lead to such outcomes decades ago.

For MMT sceptics consider that the BoJ, despite its denials of using such a policy, already holds around 43% of the JGB market and effectively finances Japan’s permanent, large fiscal deficits. Likewise, the Chinese economy is a quasi-MMT experiment given its quantitynot-price fiscal-monetary policy mix has been responsible for much of its growth since 2008 (e.g., Chinese total social financing was 9% of GDP in Q1 2019).

At the same time, there is a broadening consensus that even extraordinary central-bank monetary policy has done all it can do and more fiscal measures will be required going forwards.

In turn, that is linked to growing concern that our current socio-economic paradigm is unsustainable. Such a pessimistic view was also stated at Davos in January; hedge-fund manager Ray Dalio has argued US capitalism is structurally broken and its wealth and income inequality is a “national emergency”; and the OECD states “Today the middle class looks increasingly like a boat in rocky waters. Governments must listen to people’s concerns and protect and promote middle class living standards,” arguing in favour of significant fiscal expansion despite zero rates and high debt levels.

The IMF’s latest Global Economic Outlook also posits “This is a delicate moment for the global economy. If…any of the major risks materialize…policymakers will need to adjust. Depending on circumstances, this may require synchronized though country-specific fiscal stimulus across economies, complemented by accommodative monetary policy.”

In short, all these paths seem to lead us back towards MMT one way or another, politically, even if there is a refusal to accept the broader implications and assumptions of that framework.

Yes, but (and it’s a big but)

Of course, there is one other huge issue to address: external restraints.

If we were to see a larger MMT-financed public-sector deficit this would suggest that there will be a current account deficit too. That is because of the following known identity: Current account balance = Public-sector balance + Private-sector balance.

It is possible a large public-sector deficit could see the private sector run an offsetting surplus as profits and wages rise rapidly – as MMT sectoral balances imply. However, at the microeconomic level that implies the need for protectionist policies to keep the benefits of extra domestic liquidity at home, e.g., tariffs, subsidies, or non-tariff barriers – just as we see in China today. Without that, MMT leans towards larger current-account deficits.

Crucially, current-account deficits represent the kind of resource constraint that limits MMT. The US, with its “exorbitant privilege” of the USD as global reserve currency, would be able to use MMT to expand its fiscal deficit: it can borrow in its own currency; and MMT would see it importing more from other countries who would need to hold USD reserves as a result.

Yet smaller economies/emerging markets could not use MMT without being punished by financial markets. Their current-account deficits would have to covered with foreign borrowing, and the more MMT they used, the more their currency would weaken. Recent volatility in the Turkish currency after a period of fiscal stimulus and external borrowing, absent MMT, shows the dangers.

Crucially, the only way to avoid such risks would be to run a private-sector surplus resulting in a currentaccount surplus. Consequently, in a global downturn requiring MMT smaller economies would have to choose between no MMT; using MMT and protectionism; or coming under the wing of currency blocks who can run MMT. Notably, that was a development we saw in the 1930s when global trade fragmented into gold, Sterling, Nazi, Communist, and Yen blocks.

As such, MMT appears to offer a painless way to address inequality within the US economy, but it could reinforce an international pecking-order of winners and losers, worsen global inequality, and break-up global trade.

Indeed, MMT could even cause the USD to lose its “privilege” over time, which would again risk fragmenting global markets. That is unlikely, at least near-term given the lack of any credible USD alternatives, but it remains a longer-term risk one cannot ignore lightly.

Conclusion

Like it or not, after decades in obscurity MMT is now is now being openly discussed –and dismissed– in high policy circles. Yet many would argue that MMT’s eventual introduction in some form is inevitable given other economic alternatives appear to have failed. As Gandhi said: “First they ignore you. Then they laugh at you. Then you win.”

Indeed, Japan and China are already heading down the MMT road, even if they deny it; the inability of central banks to reverse QE via QT suggests the same underlying dynamic; and once the Fed starts cutting, the volume of these discussions will only increase further.

Of course, the rise of global political populism is likely to accelerate that development given MMT promises easy answers to complex socio-economic problems.

Certainly, when looked at in detail MMT is not the simplistic ‘free money’ argument that some of its critics present it as, and arguably contains some fresh, if old, economic thinking that could provide some solutions to some of our structural problems. At the very least, an MMT critique of our current paradigm is a useful staring base for everyone.

However, it can also be seen that MMT could create as many problems as it solves when dealing with our New Normal. From increasing market volatility to destroying functioning bond markets; and from revolutionising our entire political economy to potentially shattering world trade, the risks are there to be seen if one looks carefully enough.

MMT is arguably not something to be dismissed out of hand; but neither is it something to be embraced without question.

Indeed, just try saying MMT without saying ‘Mmm’!

via ZeroHedge News http://bit.ly/2Ugfy2U Tyler Durden

House Speaker Nancy Pelosi seems to be having a hard time accepting Rep. Alexandria Ocasio-Cortez being the “new face” of the Democratic party.

In a 60 Minutes interview this weekend, interviewer Lesley Stahl asked Pelosi about whether the different factions within the Democratic party are fractured, singling out

Stahl: “You are contending with a group in Congress. Over here on the left flank are these self-described socialists. On the right these moderates. You yourself said that you’re the only one who can unify everybody. And the questions is – can you?

Pelosi: By in large, whatever orientation they came to Congress with, they know that we have to hold the center. That we have to go down the mainstream.

Stahl: They know that?

Pelosi: They do

Stahl: But it doesn’t look like that. It looks as if it’s fractured…. You have these wings – AOC and her group on one side

Pelosi interjects: “well that’s like five people.”

The Congressional Progressive Caucus has 98 members, making it the second largest group in Congress, according to the New NY Post, which notes that AOC is one of the group’s most prominent freshmen members.

Seven Democratic House members, including Ocasio-Cortez, are supported by the progressive political action the Justice Democrats, which Pelosi could also have been referring to.

On several occasions now, Pelosi has downplayed any splits within her ranks — and also tried to dim some of Ocasio-Cortez’s star power.

“While there are people who have a large number of Twitter followers, what’s important is that we have a large number of votes on the floor of the House,” said Pelosi.

What’s not to love Nancy?

via ZeroHedge News http://bit.ly/2UfRoFL Tyler Durden

Fewer than 40 percent of Americans surveyed think they’ve seen a tax cut since 2017, when President Donald Trump signed the “Tax Cuts and Jobs Act.” In fact, most people think their personal tax burden has gone up. But “independent analyses have consistently found that a large majority of Americans would owe less because of the law” and “preliminary data based on tax filings has shown the same,” reportsThe New York Times. Meanwhile, “not even one in 10 households actually got a tax increase.”

Data from the Tax Policy Center show 64.8 percent of Americans got a tax cut, while SurveyMonkey/New York Times data found only 39.6 percent thought they got a tax cut.

People with household incomes of less than $30,000 were the most likely to accurately perceive the situation (32.1 percent got a tax cut, and 30 percent think they did). Much larger tax-cut perception and reality gaps exist at higher household income levels:

About 69 percent of people with a household income of $30,000 to $50,000 got a tax cut, but just 36.1 percent think they did.

Nearly 82 percent of those in the $50,000 to $75,000 range got a tax cut; 41.5 percent think they did.

86.6 percent of households making $75,000 to $100,000 saw a tax cut, but just 47.9 percent think they did.

And 89.5 percent of those in the $100,000 or more bracket got a tax cut, while just 46.4 percent think they did.

“To a large degree, the gap between perception and reality on the tax cuts appears to flow from a sustained—and misleading—effort by liberal opponents of the law to brand it as a broad middle-class tax increase,” write the Times‘ Ben Casselman and Jim Tankersley.

FREE MINDS

FUCT at the trademark office. The clothing company FRIENDS U CAN’T TRUST—that’s FUCT, for short—has taken its battle with the U.S. Patent and Trademark Office all the way to the Supreme Court. The office denied founder Erik Brunetti’s request, citing a federal rule against registering “scandalous” trademarks. “Now the Supreme Court on Monday, for the second time in two years, will review whether provisions of a federal law, the Lanham Act, violate the First Amendment,” reports CNN. The first case, from 2017, involved a band called The Slants. Read (or watch) more about that case here.

FREE MARKETS

Silk Road 2.0 creator sentenced. Ross Ulbricht, creator of the original darknet digital marketplace Silk Road, was relegated to two consecutive lifetimes in federal prison. But after the federal government seized Silk Road in 2013, a Silk Road 2.0 quickly took its place, thanks to the efforts of “Dread Pirate Roberts 2” Thomas White.

“White was arrested in 2014” by the U.K.’s National Crime Agency, writes Tim Cushing, “but his sentence has only now been handed down.” And “the creator of Silk Road 2.0—doing double the business of Silk Road 1.0 at its peak—is looking to be out of prison years before his inspiration sees freedom.”

White was sentenced to 5 years and four months in prison. “There’s your compare-and-contrast. In the US, drug crimes are the worst crimes,” Cushing writes.

“Our government argues lengthy sentences for drug cases are needed to deter others from drug dealing. Seeing how quickly the new Silk Road replaced Ulbricht’s version makes it clear lengthy sentences aren’t deterring anything.”

Whole Earth’s “3 Nut Butter” clearly contains the word nut in its name. Its label lits “Peanut, Pecan & Walnut” under that. But because Whole Earth didn’t use the specific nut-warning language required by U.K. regulators (“contains nuts”), the country’s Food Standards Agency has recalled the product.

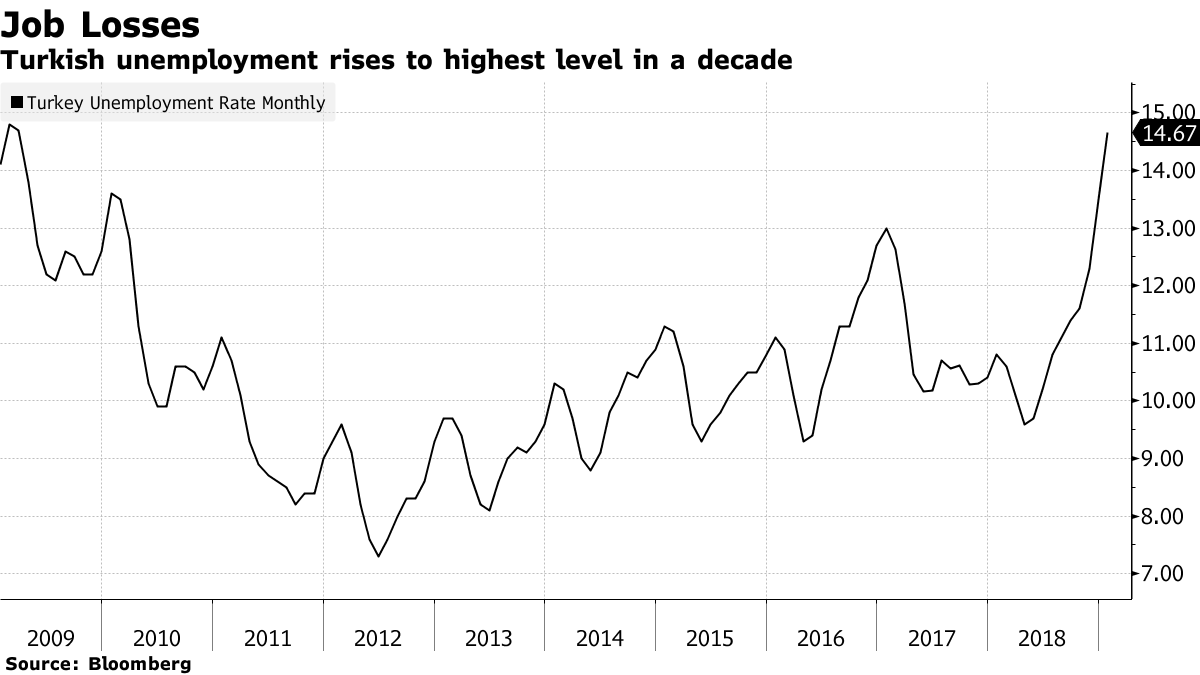

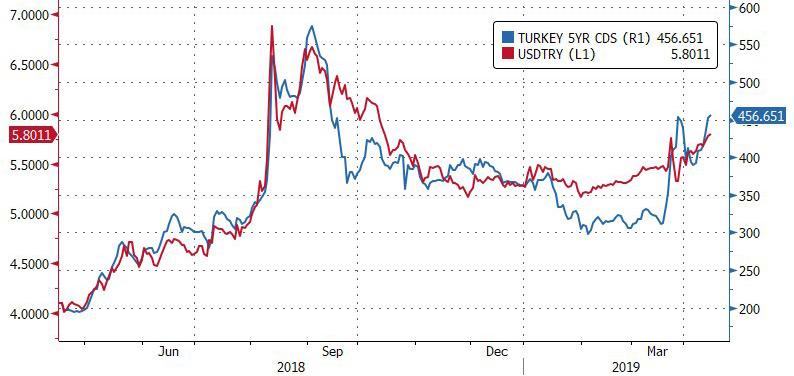

The collapse in the Turkish lira is accelerating this morning, with the USDTRY rising above 5.80 for the first time since last October and CDS pushing to September highs, as the Turkish economy continues to slide ever deeper into recession, with the country on Monday reporting that a whopping 366,000 people became unemployed in the last month, sending the country’s jobless rate to the highest level in a decade.

With Ankara trapped, unwilling to let the lira devalue on fears of capital outflows even as inflation surges while the economy is urgently in need of a weaker currency, unemployment rose far more than forecast, rising to 14.7% in January – the highest since 2009 – from 13.5% a month earlier, according to Turkstat data; the number of people without jobs has reached 4.7 million people, with youth unemployment jumping to 26.7% as Turkey is facing another labor crisis.

As Bloomberg summarizes “the severity of the job losses despite a last-ditch spending blitz by the government underscores the economic challenges facing Turkey after it entered its first recession in a decade following a currency rout last year that touched off inflation.”

The most recent dismal economic data comes at a time when Erdogan’s undisputed control over Turkey appears to be slipping following the recent local elections, where many of the municipalities won by the opposition from the ruling party were those where unemployment is running in double digits, official data show. As such, the political headache for the “executive president” is only set to grow as the country finds itself deeper and deeper in what is rapidly developing as a full-blown economic depression.

Meanwhile, investors were also concerned by ongoing speculation that the ruling AKP will challenge the Istanbul election outcome which saw Turkey’s most important city flip control to the opposition, after Erdogan’s candidate lost the mayoral race in Turkey’s largest city to Ekrem Imamoglu, a blow for Islamists who had controlled Istanbul since 1994. “We are going to ask for fresh elections in Istanbul by using our right to make an extraordinary objection,” said Ali Ihsan Yavuz, a deputy head of the AKP.

Erdogan’s refusal to concede defeat in Turkey’s commercial hub has been condemned by political opponents as an attack on Turkey’s democratic foundations. Among the vocal critics of the AKP’s reaction to losses at the ballot box was Mustafa Sonmez, an economist known for opposing the government’s policies.

Sonmez was detained on Sunday and later released after being questioned largely over his tweets over his tweets following the vote, according to his lawyer, Husniye Aydin. In his latest posts on Twitter, Sonmez criticized authorities for not recognizing the opposition’s candidate as the winner of Istanbul’s mayoral race.

Making matters worse for Lira bulls, there is little hope for any near-term turnaround: “The rise in unemployment will continue – albeit at a slowing pace,” said Muammer Komurcuoglu, an Istanbul-based economist at IS Investment. “A sharp monthly deterioration in job creation continues to take place across all the sub-sectors. We are seeing very clearly the impact of the economic slowdown on unemployment.”

But beside the collapsing Turkish economy, which was to be largely expected following last summer’s financial crisis, what has mostly spooked investors is that even as Turkey rolled out a recapitalization plan for state banks, the program unveiled by Treasury & Finance Minister Berat Albayrak last week has underwhelmed investors.

In fact, as Axios reports, Turkish Finance Minister Berat Albayrak – Erdogan’s son-in-law who replaced 2 highly respected ministers, despite having virtually no qualifications – held a closed-door meeting with hundreds of investors during the IMF-World Bank meetings in Washington last week, “and some who attended called it the worst they’ve ever had with a high-ranking government official.”

“It was an absolute shit show,” one emerging market fund manager who attended the meeting told Axios. “I’ve literally never seen someone from an administration that unprepared,” another investor said.

And, as Axios correctly notes, the disastrous meetings “could not have come at a worse time for Turkey. Investors are growing more anxious as the country heads toward recession and President Recep Tayyip Erdogan is seeing his popularity erode.”

Incidentally, what this means is that starting tomorrow, Axios will most likely be banned in Turkey.

Meanwhile, as Turkey faces growing headwinds both domestically, as the economy slides deeper into recession, and internationally where critical foreign capital is increasingly diverting to other emerging markets, locals are accelerating their shifting toward conducting business in hard currencies such as dollars and euros, and away from the Turkish lira.

As Michael Cornelius, an EM portfolio manager at T. Rowe Price, told Axios his biggest takeaway from the week’s events was that he became more pessimistic about chances for a turnaround in Turkey.

“Not only are the fundamentals not improving, Erdogan is doing worse, investor sentiment is very, very bearish and they still have significant refinancing needs… This could be a systemic issue for emerging markets.”

The silver lining: as investors once again shun Turkey, its currency still remains solidly higher than the lows it plumbed last August. The not so silver lining: this will likely not be the case for long, with the lira sliding to 6 months lows as Turkish CDS continue to blow out ever wider…

via ZeroHedge News http://bit.ly/2v5pAcP Tyler Durden

Columbus, Ohio, police searching for a missing woman found her body in her car, which happened to be a police impound lot. Officials say they don’t yet know how Falyce A. Yuill, 61, died or whether she was already dead when her car was towed or if she died at the impound lot. An initial autopsy found no signs of trauma or foul play.

from Latest – Reason.com http://bit.ly/2UCQ84s

via IFTTT

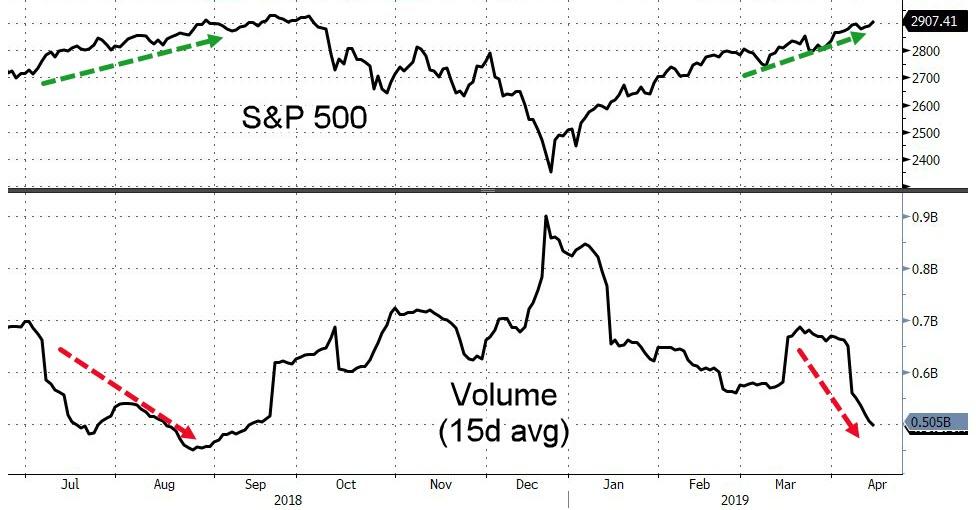

As stocks hit their 2019 highs on Friday, trading volumes collapsed to their weakest since the similar ramping equity gains in August that marked the previous peak…

But, as former fund manager Richard Breslow notes, it hasn’t been quite as calm as a cursory look at the overnight ranges and trading volumes might suggest.

But it should have been.

For every trading thesis out there, there is a counterpoint making the rounds.

Not in the sense of, it takes two to make a market.

Rather, as in, the global economic and geopolitical situation is so opaque that it’s getting harder and harder to gauge just how committed investors will remain to anything but short-term views.

It’s common to declare oneself to be data-dependent. But there is no consensus about what data we are meant to be watching.

The IMF continues to lower growth forecasts and warn about downside risks. Meanwhile, private economists continue to expect a second-half pick-up. The market is said to be priced too pessimistically and is getting ahead of itself on the possibility of rate cuts. Traders aren’t buying it. For them, “patience” isn’t a calming word.

Progress on trade is promised on an almost daily basis. Yet the various fronts where the battle may be fought keep demonstrating that a solution isn’t so straightforward as a single bilateral negotiation. Just ask the Japanese as they come to the U.S. this week. Or better yet, try to figure out what was going through the minds of people trading Japanese assets last night.

It was a strange day for the Topix index to decide to play catch-up with better performing exchanges elsewhere, the economic number beats out of China, notwithstanding. Ironically, the explosive gap higher for the Shanghai index on trade optimism, supposedly gave way in large part because traders posited that better numbers could make the PBOC less generous with stimulus. There is a lot of circular logic going on.

One hot topic where there is broad consensus concerns central bank independence. Partially because the efforts to influence the Fed have been so ham-fisted. And there are few things that economists like to debate quite as much as something they all agree on. It’s an important issue, nonetheless. But only the threat it’s being portrayed as if the legislature and the FOMC allow themselves to be seen, let alone act, as enablers. Politicians trying to influence policy is certainly nothing new. Undue efforts, however, are unacceptable. And they don’t, in all cases, warrant extreme politeness in response.

In a developed world desperately in search of inflation, it is a bad argument to warn that meddling might turn investors back into bond vigilantes. No one is going to sell 10-year Treasuries because of a rant. But they might if their Chairman meets with partisan politicians behind closed doors. Isn’t avoiding the appearance of improper influence an important part of the whole issue?

I was looking at charts this morning. And one thing that struck me was the number of cases where the asset at hand looks like potential reversals of recent trends are a real possibility. But I can’t make the case that there is some generalized risk-on or off move coming. When you take a look, don’t focus on crowded trades. Emerging markets, for instance, still look reasonable. Even if not every opportunity within the asset class was created equally. Look for the trades, that everyone takes for granted. Oil might be a good place to start. Or go for the ones, like the dollar, that just haven’t been trading well lately. Whatever the story associated with it.

via ZeroHedge News http://bit.ly/2IwPyOt Tyler Durden

Despite Trade Rep. Robert Lighthizer’s insistence that Washington leverage its position of advantage – i.e. the unassailable fact that its tariffs had contributed to a precarious deceleration in Chinese economic growth – the Trump Administration’s trade team has repeatedly caved to Beijing. First, the administration compromised on enforcement (the administration has reportedly punted it to 2025) to the currency manipulation. And now it has reportedly softened its demands for the ‘structural economic reforms’ that Trump had insisted on as part of the final deal.

According to Reuters, US negotiators have ‘tempered’ their demands that Beijing roll back some of its industrial state subsidies as part of the trade deal. Washington’s demands were reportedly met with ‘strong resistance’ from Beijing.

The issue is a thorny one because China’s brand of state-directed capitalism is deeply tied up with the tax breaks and other advantages that Beijing bestows on state-owned firms, and it’s possible that many of these firms could fail without the government’s support, potentially setting off a destabilizing chain reaction.

The issue of industrial subsidies is thorny because they are intertwined with the Chinese government’s industrial policy. Beijing grants subsidies and tax breaks to state-owned firms and to sectors seen as strategic for long-term development. Chinese President Xi Jinping has strengthened the state’s role in parts of the economy.

And as the Trump administration looks to secure a deal in the next month or so, expect them to cave on more of their demands and focus on priorities that they consider “achievable.”

These include: Ending forced technology transfers, improving intellectual property protection, expanding access to Chinese markets for American firms (and in particular American tech firms).

In what sounded like an attempt to spin Washington’s walk-backs on subsidies and enforcement, Treasury Secretary Steve Mnuchin – one of the officials tasked with leading the trade delegation – said during a Monday morning interview that there was “more work to do” including on the issue of enforcement, after saying last week that the two sides had agreed to opening ‘enforcement offices’.

When it comes to restrictions on state subsidies, expect any language in the deal to be vague, allowing Beijing substantial wiggle room to largely maintain the status quo.

So, if China’s economy is in such dire straits, why is the US caving? Well, because President Xi can’t accept a deal that would make him look weak, which gives him very little room to concede.

Washington has detailed more than 500 different subsidies it has said China applies in notifications to the WTO.

“It’s not that there won’t be some language on it, but it is not going to be very detailed or specific,” one source familiar with the talks said in reference to the subsidies issue.

“If U.S. negotiators define success as changing the way China’s economy operates, that will never happen,” said the other source with knowledge of the trade talks.

“A deal that makes Xi look weak is not a worthwhile deal for Xi. Whatever deal we get, it’s going to be better than what we’ve had, and it’s not going to be sufficient for some people. But that’s politics,” that source said.

China promised to end its subsidies earlier this year, but never said how it would accomplish this. To be sure, as Reuters points out, there are ways that maintaining subsidies could work to America’s advantage, since most of the firms that would be making the tens of billions of dollars of annual agricultural purchases are mostly recipients of these subsidies.

One of the key sticking points in the negotiations is the removal of the $250 billion in U.S. tariffs. It is broadly expected in the trade community that U.S. negotiators want to keep some tariffs on Chinese goods, which Washington sees as retaliation for the years of damage done to its economy by Beijing’s unfair trade practices.

The role of the state firms may benefit the United States in another part of the trade deal. The Trump administration wants China to make big-ticket purchases of over a trillion dollars of U.S. goods in the next six years to reduce its trade surplus. The companies likely to make the purchases are the state-run firms, both sources said.

“The purchasing, for example, reinforces the role of the state sector because the purchasing is all being done through state enterprises,” one of the sources said.

Another point of contention between the two countries, telecommunications, may drive China to increase the state’s role rather than reduce it, the source said.

In a separate report, Bloomberg said that China is weighing a request from Washington to shift some tariffs on key agricultural goods to other products to help the administration sell the trade deal to farmers, a key voting bloc for Trump, ahead of the 2020 election. While the exact nature of the arrangement proposed by the US wasn’t reported, it shows that political considerations are increasingly becoming a factor as the talks enter their final stretch.

While some have argued that Trump could tout any deal as a win, even if China refuses to meet Washington’s core demands and instead focuses on agricultural purchases, the political problem could become a serious Catch-22 for Trump.

via ZeroHedge News http://bit.ly/2IkfBsL Tyler Durden

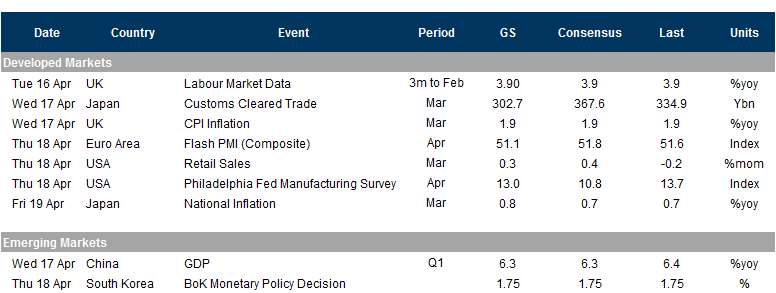

With the Easter holidays looming, markets look forward to a burst in economic and data highlights including the release of Chinese Q1 GDP data, preliminary April PMIs for the Eurozone and the US, US retail sales data for March and a barrage of Q1 earnings. From central banks, we’ll get the Fed’s Beige Book and a decision from the Bank of Korea, along with various speakers. Politically, there’ll be elections in Finland and Indonesia, along with trade talks between the US and Japan. At the end of the week, a number of countries have the Good Friday bank holiday.

As Deutsche’s Craig Nicol writes, a major data release for markets will be Chinese GDP for Q1 on Wednesday, where the consensus is that the year-on-year reading will fall slightly to 6.3%, from the previous quarter’s 6.4%. That day will also see the release of March’s industrial production and retail sales data for China, so there’ll be a number of things to look out for. Also from Asia, we’ll get the March Japanese CPI reading on Thursday, where the consensus expectation is for a rise in the year-on-year reading to 0.5%, up from the previous month’s 0.2%.

Another main highlight will be the preliminary April PMIs on Thursday, with releases for the Eurozone, Germany, France and the United States. It’ll be particularly interesting to see the manufacturing PMI for the Eurozone, which fell for an eighth consecutive month in March, moving deeper into contractionary territory with a 47.5 reading. The German manufacturing PMI was even more contractionary last month, with a 44.1 reading.

In the US, the key economic data releases this week are the retail sales report and the Philadelphia Fed manufacturing index on Thursday.

Other releases to watch out for include US retail sales for March, which are coming out on Thursday, as well as the German ZEW survey for April, which is coming out on Tuesday. In March, the ZEW survey of current expectations fell to 11.1, its lowest level since December 2014, although the expectation reading rose to -3.6, which was its highest since March 2018, so it’ll be worth looking to see if there are any signs of stabilisation. There’ll also be a number of important data releases in the UK, with employment data on Tuesday, inflation data on Wednesday and retail sales data on Thursday. Last month’s employment release saw the UK unemployment rate fall to 3.9% in the November-January period, the first time since 1975 that the UK unemployment rate had fallen below 4%.

After this week’s ECB meeting and the release of the FOMC minutes from March, this week will be a quieter one from central banks. In terms of decisions, the main event this week will be from South Korea, where the Bank of Korea will be making their interest rate decision on Thursday. No change is expected in the main interest rate, which is currently at 1.75%. We’ll also get the release of the minutes of the Reserve Bank of Australia’s April policy meeting on Tuesday, as well as the Fed’s Beige Book on Wednesday.

In terms of central bank speakers, on Monday there’ll be the BoJ’s Wakatabe, the BoE’s Haskel, the ECB’s Villeroy and the Fed’s Evans. On Tuesday, we have the Fed’s Rosengren and Kaplan, as well as the ECB’s Nowotny. On Wednesday, we have the BoE’s Carney and the ECB’s Villeroy de Galhau speaking in Paris, while from the Fed both Harker and Bullard will be speaking. On Thursday, the Fed’s Bostic will be speaking.

In terms of politics, we should see somewhat less of Brexit in the headlines over the coming week as the House of Commons in the UK will not be sitting with the Easter recess, not returning until 23 April. At this week’s European Council summit the EU granted the UK an extension of Article 50 from the previous 12 April deadline to 31 October, although if a deal is passed the UK would be able to leave the EU earlier. Elsewhere, we have various elections this week. On Sunday, Finland held parliamentary elections, and on Wednesday the Indonesian presidential election will be taking place, where incumbent President Joko Widodo is running for a second term in office. There’ll also be continued voting in the Indian general election, with the second round of voting taking place on Wednesday, as Prime Minister Narendra Modi also seeks a second term. Looking at ongoing trade talks, the Japanese economy minister, Toshimitsu Motegi, will be visiting the US for talks on Monday.

We’ll also get a number of company earnings as earnings season gets into full swing. On Monday, we got Goldman Sachs and Citigroup continuing the banks reporting results, with the former disappointing and the latter reporting stronger than expected fixed income trading. On Tuesday, there’ll be earning releases from Bank of America, Netflix, IBM and Johnson & Johnson. On Wednesday, there’ll be Morgan Stanley and PepsiCo, and on Thursday, there’ll be Philip Morris International and American Express.

It’s also the Good Friday holiday at the end of the week, so we’ll see a number of markets closed in the US and Europe.

A look at key events in the coming week:

Monday: It’s a fairly light start to the week with scheduled data releases including the UK’s April Rightmove house prices followed by the release of April Empire manufacturing and February TIC flows both in the US. Away from the data, the BoJ’s Wakatabe, BoE’s Haskel, the ECB’s Villeroy and the Fed’s Evans are all due to speak. The Japanese economy minister will also be visiting the US for trade talks. Goldman Sachs and Citigroup will release earnings.

Tuesday: It’s another quiet day for data with key highlights being the release of March new home prices in China followed by the release of employment data in the UK for the December-February period, as well as the March claimant count rate. We’ll also get February construction output in the Eurozone and the April ZEW survey results in Germany and the Eurozone. In the US, we’ll get March industrial production and capacity utilisation along with April’s NAHB housing market index, as well as Canada’s manufacturing sales for February. In addition to the data releases, the Fed’s Rosengren and Kaplan are due to speak, as well as the ECB’s Nowotny. Bank of America, Netflix, IBM and Johnson & Johnson will release earnings.

Wednesday: It’s a very busy day for data with the key highlight likely to be the release of Q1 GDP in China (overnight). We will also get Japan’s March trade balance and China’s March macro data dump including retail sales, followed by the release of March new car registrations in the Eurozone along with the February trade balance, final March CPI in Italy and the Eurozone and the UK’s March inflation data. In the US, we will get the latest weekly MBA mortgage applications, February trade balance and wholesale inventories data along with the Fed’s latest Beige Book. Away from the data, the BoE’s Carney, ECB’s Villeroy and the Fed’s Harker, Bullard and Logan are all due to speak. Meanwhile, the Indonesian presidential election will be taking place. Morgan Stanley and PepsiCo will release earnings.

Thursday: The key highlight of the day is the release of preliminary April PMIs in France, Germany, the Eurozone and the US. Besides that we will get employment data from Australia for March, March PPI in Germany, March retail sales and the BoE’s credit conditions and bank liabilities surveys in the UK along with the release of March retail sales, April Philadelphia Fed business outlook, the latest weekly initial jobless and continuing claims, March leading index and February business inventories all in the US, and Canadian retail sales for February. Away from the data, the Bank of Korea will be making their latest decision on interest rates and the Fed’s Bostic is due to speak. Philip Morris International and American Express will release earnings.

Friday: It’s a very quiet day for data with March CPI due in Japan and March housing starts and building permits due in the US. Most markets are likely to remain closed on account of Good Friday holiday including the UK, France and Germany. In the US, stock markets are also going to remain closed.

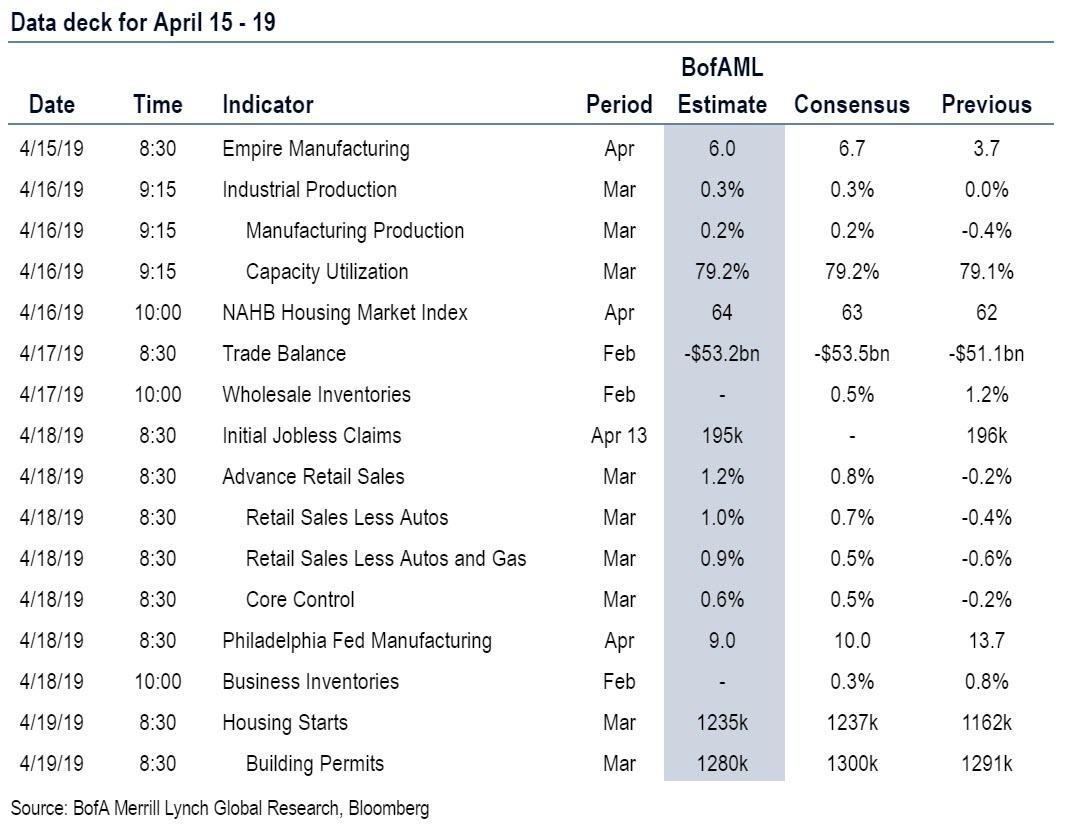

Finally, looking at just the US, Goldman notes that the key economic data releases this week are the retail sales report and the Philadelphia Fed manufacturing index on Thursday. There are several scheduled speaking engagements by Fed officials this week.

Monday, April 15

08:30 AM Empire State manufacturing index, April (consensus +8.0, last +3.7)

1:00 PM Chicago Fed President Charles Evans (FOMC voter) speaks: Chicago Fed President Charles Evans will discuss the US economy and monetary policy with the New York Association for Business Economics. Audience and media Q&A are expected.

8:00 PM Boston Fed President Eric Rosengren (FOMC voter) speaks: Boston Fed President Eric Rosengren will give a lecture at Davidson College. Prepared text is expected.

Tuesday, April 16

09:15 AM Industrial production, March (GS +0.1%, consensus +0.2%, last flat); Manufacturing production, March (GS flat, consensus +0.1%, last -0.4%); Capacity utilization, March (GS 79.0%, consensus 79.2%, last 79.1%): We estimate industrial production was flat in March, driven by strength in the utilities category and offset by weakness in auto manufacturing. We estimate capacity utilization edged down one tenth to 79.0%.

10:00 AM NAHB housing market index, April (consensus 63, last 62)

2:00 PM Dallas Fed President Robert Kaplan (FOMC non-voter) speaks: Dallas Fed President Robert Kaplan will speak at a community forum hosted by the El Paso branch of the Dallas Fed in Hobbs, New Mexico. Audience and media Q&A are expected.

Wednesday, April 17

08:30AM Trade balance, February (GS -$54.1bn, consensus -$53.5bn, last -$51.1bn): We estimate the trade deficit increased to $54.1bn in February, reflecting a rebound in inbound container traffic but softer outbound trends.

10:00 AM Wholesale inventories, February (consensus +0.4%, last +1.2%)

12:30 PM Philadelphia Fed President Patrick Harker (FOMC non-voter) speaks: Philadelphia Fed President Patrick Harker will discuss the economic outlook at a Greater Vineland Chamber of Commerce event in Vineland, New Jersey. Audience Q&A is expected.

12:30 PM St. Louis Fed President James Bullard (FOMC voter) speaks: St. Louis Fed President James Bullard will give a speech at the annual Hyman P. Minsky Conference on the US and Global Economy at Bard College.

02:00 PM Beige Book, April/May FOMC meeting period: The Fed’s Beige Book is a summary of regional economic anecdotes from the 12 Federal Reserve districts. The March Beige Book reported growth at an overall slight to moderate pace across most Districts. Contacts retained an optimistic outlook overall, but concerns on tariffs, slowing global growth, and trade policy uncertainty continued to weigh on optimism. In the April Beige Book, we look for additional anecdotes related to growth, labor markets, wages, price inflation, and the economic impacts of slowing global growth.

Thursday, April 18

8:30 AM Retail sales, March (GS +1.0%, consensus +1.0%, last -0.2%); Retail sales ex-auto, March (GS +0.7%, consensus +0.7%, last -0.4%); Retail sales ex-auto & gas, March (GS +0.4%, consensus +0.4%, -0.6%); Core retail sales, March (GS +0.3%, consensus +0.4%, last -0.2%): We estimate that core retail sales (ex-autos, gasoline, and building materials) rose 0.4% in March (mom sa), reflecting a lackluster rebound in retail spending data and lower than usual tax refunds. We estimate a 1.0% increase in the headline measure, reflecting a sharp rebound in gasoline prices and auto sales, and a 0.4% increase in the ex-auto measure.

08:30 AM Philadelphia Fed manufacturing index, April (GS +13.0, consensus +10.8, last +13.7): We estimate that the Philadelphia Fed manufacturing index declined by 0.7pt to +13.0 in April after a 17.8pt rebound in March.

08:30 AM Initial jobless claims, week ended April 13 (GS 205k, consensus 205k, last 196k): Continuing jobless claims, week ended April 6 (last 1,713k); We estimate jobless claims increased by 9k to 205k in the week ended April 13, following an 8k decline in the prior week.

09:45 AM Markit Flash US manufacturing PMI, April preliminary (consensus 52.7, last 52.4)

09:45 AM Markit Flash US services PMI, April preliminary (consensus 55.0, last 55.3)

10:00 AM Business inventories, February (consensus +0.3%, last +0.8%)

12:10 PM Atlanta Fed President Raphael Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will speak at the Economic Roundtable of Jacksonville. Audience Q&A is expected.

Friday, April 19

US equity and bond markets will be closed in observance of Good Friday.

08:30 AM Housing starts, March (GS +6.0%, consensus +5.9%, last -8.7%); Building permits, March (consensus +0.7%, last -1.6%): We estimate housing starts rose 6.0% in March following last month’s 8.7% decline. Our forecast incorporates boosts from a likely catch-up of single-family starts with firmer permits, lower mortgage rates and stronger construction job growth but a drag from likely mean reversion in the noisy multifamily category.

Source: Deutsche Bank, Goldman, Bank of America

via ZeroHedge News http://bit.ly/2UAdebY Tyler Durden

Michael Knowles, a writer for the conservative Daily Wire, attempted to speak at the University of Missouri-Kansas City on Thursday. Protesters heckled him, and one hurled a liquid that smelled like bleach at him.

The substance was not actually bleach. Police arrested the attacker immediately. According toCampus Reform:

UMKC responded to the incident in a tweet, saying, “we have a responsibility to allow free speech, but we cannot condone physical disruptions of peaceful activities. We believe free speech can be exercised constructively in a way that doesn’t put people at risk. We are gathering facts and will review campus policies & procedures.”

Knowles was on campus to give a talk called “Men Are Not Women,” presumably about his views on the transgender community.

Knowles is a professional provocateur and decidedly trollish rightwing figure. (His book Reasons to Vote for Democrats is just 266 blank pages.) It seems obvious that the best thing to do is ignore his talks, which are quite intentionally designed to get a rise out of lefties and trick them into making themselves look intolerant and cartoonish. True to form, the activist left greeted Knowles with the kind of stupid, self-defeating behavior that Knowles’ ilk thrives on.

from Latest – Reason.com http://bit.ly/2Dg2lBp

via IFTTT