“The market has had a correction. Of sorts. But this feels nothing like last December,” noted former fund manager and FX trader Richard Breslow this morning.

However, while the size of the decline is not the same scale, Bloomberg notes that the speed with which investors are hitting the ‘sell’ button is more aggressive than during the December rout.

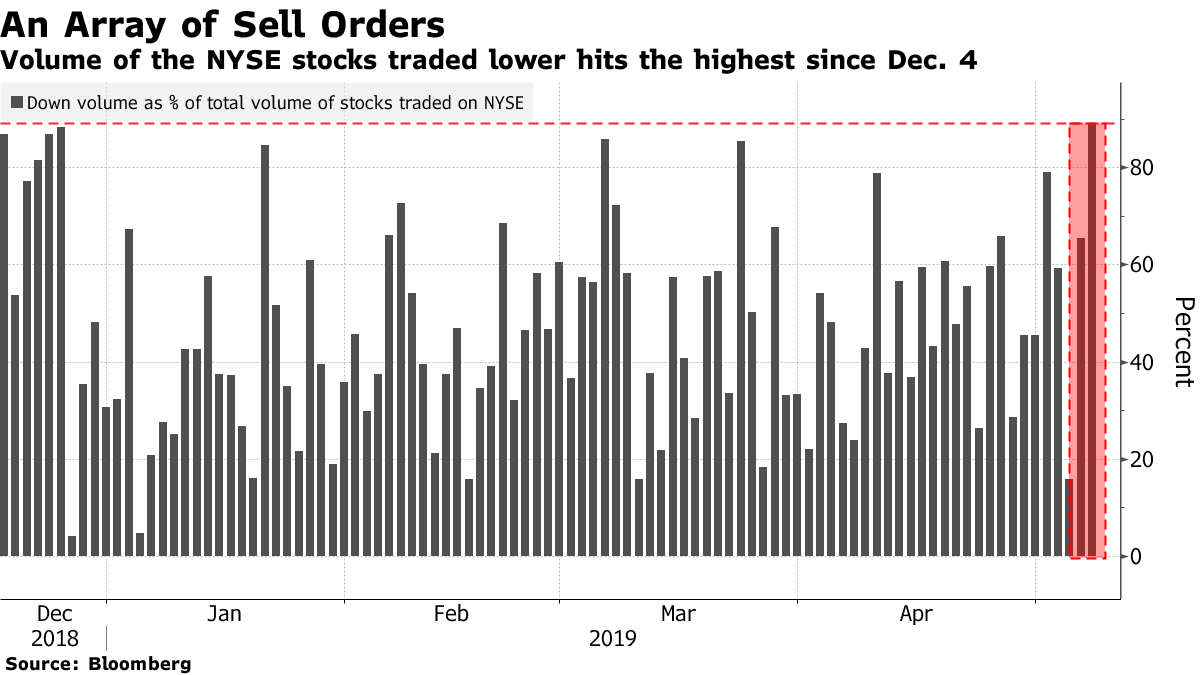

“This is what it looks like when the market starts to price in an escalation in tariffs,” said Michael Antonelli, managing director and market strategist at Robert W. Baird & Co.

“We would not want a 90 percent down day, it would be hard to argue that this is a healthy sideways correction if that happens.”

However, Breslow points out that for one thing, no one is frantically wondering just what is going on. And that feeling of being lost is a horrible one when you are losing money.

This time around, the tariff demon caught people at all-time highs with bullishness as strong as ever. Yet, I’ve heard a lot more talk this morning about nibbling on the long side than searching for a bid, any bid. There are tweets, leaks and short-term price action. Then there are the base-case scenarios.

We’re complacent. Most traders admit it. Now we’ll get a chance to find out whether that will be rewarded or not.

Via Bloomberg,

It was only a few weeks ago that investors watched the Chinese equity market completely run out of momentum after its more than impressive first-quarter rally. And then tell themselves all the reasons it wouldn’t affect indexes elsewhere. We know how that usually works out. It took another week or so, but other exchanges have followed suit.

That makes it entirely reasonable to look where potential support could come into play in the Shanghai Composite while assessing whether the 55-day moving average of the S&P 500 will end up being the line in this sell-off’s sand. It has been a good big-picture guide. The area SHCOMP needs to hold is down at 2800, a level we blasted off from in February.

It will be interesting to see who is buying and who is selling should we manage to get down there. Don’t imagine that is an easy question to answer. For all the talk about other stock markets, especially European ones, having more upside than those of the U.S., they look more vulnerable should things continue to head south. Which makes perfect sense. Like it or not, admit it or not: Europe’s economy is following, not leading, events elsewhere.

As equities get hit, bond yields, not surprisingly, have been slipping. For 10-year Treasuries to get back below 2.40% would be a big deal. Especially if the dollar continues to languish and, suddenly, buying un-hedged dollar bonds doesn’t look like such an easy trade.

I’d keep a close eye on USD/JPY as it explores what is down at this 110 level. Safe havens have had much-discussed limited usefulness, but the yen has caught a bid. And it isn’t because the BOJ has been surprising to the hawkish side. But, as a note of caution, that long Japanese holiday makes coming to quick conclusions from the charts of their asset prices a bit suspect.

The trade negotiations are the story of this week. No getting around that. But Fed Chairman Jerome Powell talked about “transitory” factors suppressing the recent dip in inflation. Which was another way of saying, the market has gotten ahead of itself on the subject of rate cuts.

He got an assist yesterday from Vice Chairman Richard Clarida. This evolving messaging will make Friday’s CPI numbers compelling reading and either way, it will be hard for the market to explain away any number that doesn’t suit

via ZeroHedge News http://bit.ly/2HaHsKp Tyler Durden