After yesterday’s bizarre, gamma-chasing rally, the week was set to close in a sea of red as world markets suffered a fresh bout of risk aversion on Friday after China doused hopes for a quick deal when its state media signaled a lack of interest in resuming trade talks with the U.S. under the current threat to escalate tariffs, while the government said stimulus will be stepped up to buttress the domestic economy. Meanwhile bets on a new pro-Brexit leader in Britain whipped the pound towards its worst week since October.

After an initial advance, Asian stocks erased most gains for the day with the MSCI index of Asia-Pacific shares outside Japan sliding to 15-week lows and down 2.6% for the week at the end of trading. An advance in Japanese stocks failed to offset falling Chinese shares. The Topix Index rose 1.1%, led by electric appliances, while China’s Shanghai Composite Index fell 2.5% after a front page commentary in the Communist Party’s People’s Daily evoked the patriotic spirit of past wars, saying the trade war would never bring China down.

“The China state media commentaries fueled concerns that the U.S.-China trade disputes will prolong, deterring risk-taking,” said Koji Fukaya, CEO of Japan’s FPG Securities. “This issue will probably be one of the major market drivers for a while as U.S.-China trade war influences global economic conditions.”

In terms of how the trade conflict plays out, “the next fortnight will be very, very important,” UniCredit strategist Kiran Kowshik said. “Chinese counter-tariffs are due on June 1 and if those get effective, I think markets will price in the risk of the U.S. imposing its additional $300 billion of tariffs ahead of the G20 meeting (near the end of June).”

Elsewhere, stocks retreated in South Korea and Hong Kong, while India’s S&P BSE Sensex Index extended a rebound into the second day and the main Australian index climbed to an 11-year peak as higher commodity prices boosted miners.

As Bloomberg notes, “traders are reassessing prospects for a trade deal after commentary on the blog Taoran Notes, which was carried by state-run Xinhua News Agency and the People’s Daily, the Communist Party’s mouthpiece, accused the U.S. of playing “tricks to disrupt the atmosphere.” Indications that the talks are paused will focus attention on the next opportunity for Presidents Xi Jinping and Donald Trump to meet — at the Group of Twenty meeting in Japan next month.”

As a result of the collapse in trade “optimism”, US equity futures including the S&P 500, Dow Jones and Nasdaq signaled a lower U.S. open after yesterday’s gains, while the Stoxx Europe 600 Index fell for the first time in four days, led by autos, with most sectors in red. Germany’s exporter-heavy DAX fell the most, auto stocks lost as much as 1.6%. Easyjet was a standout of the gauge after releasing earnings, while takeaway food delivery firms including Just Eat and Delivery Hero tumbled after Amazon confirmed an investment in rival Deliveroo.

Sentiment on Thursday was briefly, if erroneously soothed by better U.S. economic news, with housing starts surprisingly strong and a welcome pickup in the Philadelphia Federal Reserve’s manufacturing survey. Upbeat results from Walmart burnished the outlook for retail spending, though the chain also warned that tariffs would raise prices for U.S. consumers.

As the US earnings season winds down, of the 457 S&P 500 companies reporting about 75% have beaten profit expectations, according to Reuters data.

In rates, the sudden trade wind chilling helped Treasuries, with the 10-year yield down at 2.37% after a second strong week running for bond markets. Yields on Spanish 10-year debt fell to a record as bonds across the euro region firmed.

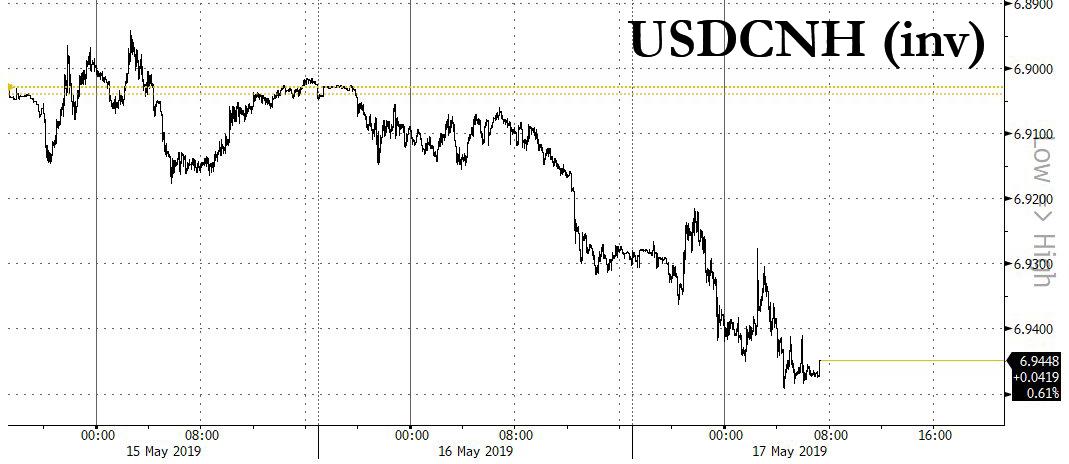

In FX, the standout mover was the yuan, which was already trading at five-month lows, and smashed support after stops were triggered once the offshore Yuan tumbled below 6.92 yesterday, prompting Deutsche Bank to suggest “Stairway to Seven” is in the cards. The USDCNH hit a multi month high of 6.9491 even though Reuters reported again that the PBOC would not allow the currency to drop below 7.00.

Elsewhere in FX, the dollar lost a little of its shine against the safe-haven yen to stand at 109.64 from a top of 110.03. Against a basket of currencies, it was a shade softer at 96.824. Yet the euro could make no ground and held at $1.1173, down 0.5% for the week so far. Sterling was one of the worst performers as Britain’s Prime Minister Theresa May battled to keep her Brexit deal, and her premiership, intact amid growing fears of a disorderly departure from the European Union. The pound touched a three-month low of $1.2783 and was down 1.6% for the week so far. Also under pressure was the Australian dollar, losing 1.5% for the week to $0.6880 as investors piled into bets that interest rates would be cut in June.

Of note, after soaring 100% in two weeks, Bitcoin tumbled over 20% at one stage after what appeared to be a flash crash. It was last down 7%, albeit back on course for its third week of gains and having doubled in value this year.

In commodity markets, spot gold steadied at $1,287 per ounce as risk sentiment soured. Crude oil gained, as rising tensions in the Middle East stoked fears of potential supply disruptions, while iron ore rose to its highest level in almost five years on supply woes. WTI was last up 33 cents at $63.20 a barrel, while Brent crude futures rose 19 cents to $72.81. OPEC and non-OPEC producers will meet in Saudi Arabia this weekend over whether to continue with supply cuts that have boosted prices more than 30% so far this year.

Expected data include Leading Index and University of Michigan Consumer Sentiment Index. CAE and Deere report earnings.

Market Snapshot

- S&P 500 futures down 0.5% to 2,864.25

- STOXX Europe 600 down 0.6% to 380.63

- MXAP down 0.02% to 154.55

- MXAPJ down 0.8% to 504.53

- Nikkei up 0.9% to 21,250.09

- Topix up 1.1% to 1,554.25

- Hang Seng Index down 1.2% to 27,946.46

- Shanghai Composite down 2.5% to 2,882.30

- Sensex up 1% to 37,777.24

- Australia S&P/ASX 200 up 0.6% to 6,365.30

- Kospi down 0.6% to 2,055.80

- German 10Y yield fell 1.1 bps to -0.106%

- Euro unchanged at $1.1174

- Italian 10Y yield fell 6.2 bps to 2.311%

- Spanish 10Y yield fell 4.7 bps to 0.858%

- Brent futures up 0.2% to $72.74/bbl

- Gold spot little changed at $1,286.67

- U.S. Dollar Index little changed at 97.90

Top Overnight News from Bloomberg

- China’s state media signaled a lack of interest in resuming trade talks with the U.S. under the current threat to escalate tariffs and without new moves that show the U.S. is sincere. The Chinese government said stimulus will be stepped up to buttress the domestic economy.

- Without new moves that show the U.S. is sincere, it is meaningless for its officials to come to China and have trade talks, according to a commentary by the blog Taoran Notes, which was carried by state-run Xinhua News Agency and the People’s Daily, the Communist Party’s mouthpiece

- Theresa May is confronting the end of her premiership after her own party forced her to agree to set a timeline to quit as U.K. prime minister. Before announcing the schedule for her departure, May will try one last time to finish the job she started and get her Brexit deal approved in a vote in Parliament at the beginning of June

- The pound headed for the longest losing streak against the euro since the turn of the century as rising U.K. political risks fanned concern about the nation’s ability to achieve an orderly Brexit.

- President Donald Trump is wary of drawing the U.S. into a war with Iran, in part out of concern that an armed conflict with the Islamic Republic would imperil his chances at winning a second term, according to people familiar with the matter. U.S.’s evidence of Iran threat readied for release by Pentagon

- The U.S. announced a rollback of steel tariffs against Turkey that it originally levied in August as trade and diplomatic relations deteriorated because of Turkey’s economic crisis and a row over the Turkish government’s detention of an American pastor.

- Italy’s Matteo Salvini has a new medicine to fix his country, and he calls it “the Trump cure.” After being the steady hand in Rome’s populist coalition government for most of the past year, the deputy prime minister and anti-immigrant League party leader projected himself as the country’s Donald Trump on Thursday

- Amazon.com Inc. is leading a $575 million investment in Deliveroo, buying a slice of the fast-growing startup to propel its drive into the European food and groceries business. U.K.-based Deliveroo has raised $1.53 billion to date.

- Deputy prime minister and anti-immigrant League party leader Matteo Salvini projected himself as the country’s Donald Trump during intense campaigning for the European Parliamentary elections on May 26.

- European Central Bank officials dragging their feet over a potential revamp of their negative interest rates might be shutting off one way to convince investors they are serious on stoking inflation.

Asian equity markets were mostly higher as the region took impetus from the positive performance on Wall St, where all major indices notched a 3rd consecutive win streak with risk sentiment underpinned by encouraging earnings from Walmart and Cisco. ASX 200 (+0.6%) and Nikkei 225 (+0.9%) traded positive with Australia led by continued strength in tech and amid the growing list of calls for a rate cut next month including notorious RBA watcher McCrann, while Japanese exporters were buoyed by recent favourable currency moves and as Sony shares surged over 10% after the announcement of a JPY 200bln share buyback. Hang Seng (-1.2%) and Shanghai Comp. (-2.5%) were pressured after a lack of PBoC reverse repo operations throughout the week resulted to net weekly drain of CNY 50bln. In addition, China cancelled orders of 3247 tons of pork from US which was the largest cancellation in more than a year and was seen to be another fallout of the ongoing US-China trade dispute, while commentary in Chinese state media suggested China may have no interest in resuming trade discussions with the US for now. Finally, 10yr JGBs were lower amid the upbeat risk tone in Japan and on spill-over selling from the bear flattening stateside, while the BoJ’s Rinban announcement was for a reserved JPY 200bln of long to super-long JGBs.

Top European News

- Europe Could Reap Silver Lining From U.S.-China Trade Dispute

- Euro-Area Core Inflation Revised Up to 1.3%, Highest Since 2017

- LetterOne Wins Enough Shareholder Backing to Take Over DIA

- EasyJet Gains After Insulating Against Drop in Summer Fares

- Spanish Yield Drops to a Record as Nation’s Debt Allure Grows

A relatively downbeat session thus far for major European stocks [Eurostoxx 50 -0.5%], following on from a mixed lead in Asia where the Shanghai Composite shed 2.5% as hopes for a trade deal dwindled amid reports that China may not want to continue trade talks with the US for now. Major indices are broadly lower by around 0.5-0.7%, although, the FTSE 100 outperforms as UK exports benefit from the weaker Sterling. Sectors are showing broad-based losses with the exceptions of utilities (defensive sector) and energy names due to price action in the complex. Elsewhere, Thomas Cook (-24.8%) shares slumped for a second consecutive day, with traders citing the downside to a downgrade at Citi with a price target of zero. Finally, GVC Holdings (+2.5%) remain near the top of the Stoxx 600 after the Co. cut its potential impact from the FOBT GBP 2 limit from GBP 120mln to GBP 105mln. Notable pre-market US earnings this morning from Deere & Co (DE), who missed on EPS but beat on revenue and lowered their net income guidance.

Top Asian News

- China Traders Snap Up Most Hong Kong Stocks Since Early 2018

- Nissan Adds Renault’s Bollore to Board as Part of Overhaul

- Taiwan Parliament Approves Gay Marriage Law in First for Asia

- Offshore Yuan Smashing Support Level Brings Record Low in Sight

In FX, the Greenback has held onto the bulk of its post-US data/survey gains by virtue of advances against riskier/high beta counterparts as safer-havens within the G10 community are outperforming in wake of pretty defiant comments from China revealing a reluctance to pursue talks further given recent actions taken by the US. The index is hovering just below the 98.000 level after an apparent clean break of Fib resistance at 97.842 within a 97.953-759 range. To recap, 98.102 is the mtd DXY high and then the 2019 peak at 98.346 comes into focus.

- JPY/CHF – As noted, the Yen and Franc are back in favour on US-China trade stains, but also as Brexit, Italian budget and geopolitical issues weigh on broad risk sentiment, with Usd/Jpy retreating from circa 110.00 highs back towards 109.50 and away from decent option expiries at the big figure (1.2 bn). Usd/Chf is holding around 1.0100, but Eur/Chf is back below 1.1300 and near recent lows not far from key chart supports and levels that may prompt some form of SNB action.

- CAD/AUD/GBP – All on the back foot due to the aforementioned bearish/negative factors, as the Loonie revisits recent lows around 1.3500 and Aussie extends losses through 0.6900 to 0.6873 following latest jobs data that heightens the prospect of a June RBA rate cut after this month’s dovish hold. Similarly, the Pound continues to slide, and Cable has now hit fresh lows since the Valentine’s Day base of 1.2773 at 1.2755 on confirmation that cross party talks have come to a conclusion with no collusion in terms of an alternative WA. Note also, Gbp/Jpy has tripped stops on a break of the psychological 140.00 level.

- EUR/NZD – Also victims of the ongoing Usd revival and overall downturn in risk appetite, with the single currency declining to fresh weekly lows and testing bids said to be sitting at 1.1160 and protecting 1.1150 ahead of the current 1.1135 May base, while the Kiwi is slipping further away from 0.6550 and closer to 0.6525 given only scant support from Aud/Nzd cross flows within 1.0550-25 parameters.

- EM – Mixed blessings for the Turkish Lira as the US halved its tariff on steel, but removed preferential status on metals overall, while the AKP is still reportedly on a mission to tap CBRT reserves. Usd/Try extending above 6.0000 and testing resistance at 6.1000 before paring back, while the Yuan is not taking much heed of reports that 7.0000 is the PBoC’s line in the sand as the US-China tariff spat shows no sign of improving.

In commodities, choppy trade in the energy complex, although WTI (+1.1%) and Brent (+0.7%) futures are ultimately higher ahead of this week’s JMMC meeting in Saudi Arabia, which sets the stage for the OPEC/OPEC+ meeting in June. Focus will be on Iran’s situation amidst US sanctions and the expiry of waivers and whether there is scope to extend the current output cut deal between OPEC and its allies. Ship tracking data showed that Iranian oil shipments in May thus far has fallen to zero, however, ING highlights that a large number of Iranian tankers turn off their transponders. This follows reports of a tanker carrying Iranian oil reportedly unloading its cargo of almost 130k tonnes of oil near Zhousan, in China, Iran’s largest customer. Furthermore, comments from Iran’s revolutionary guard emphasis rising tensions between the country and the US, with the latest stating that “even short-range missiles can reach US warships in the Gulf”. Market participants will be on the lookout for how US President Trump reacts to these threats from Iran. In terms of weekly price action so far, WTI futures are poised for a positive week after having breached its 50 WMA (61.81) to the upside whilst similarly, Brent futures are set for a week of gains, after having dipped below USD 70/bbl (and its 50 WMA at the figure) earlier in the week. Elsewhere, precious metals are little changed with spot gold (-0.2%) meandering further below the 1300/oz level after having lost more ground to yesterday’s rising Buck.

US Event Calendar

- 10am: Leading Index, est. 0.2%, prior 0.4%

- 10am: U. of Mich. Sentiment, est. 97.2, prior 97.2; Current Conditions, est. 112.2, prior 112.3

DB’s Jim Reid concludes the overnight wrap

It’s a bit of a teary eyed trip down memory lane coming up this weekend as I’m playing my first proper gig in over a decade. The cricket club that I’m President of is having a fund raiser and although there are discussions that they’d raise more money if I didn’t sing and play live, I have offered up my services nevertheless. We haven’t rehearsed so we’re doing almost the identical covers set to our last gig and even then it was out of date. Given that the average age of the cricket club is probably early 20s I wonder how many of our set will have been released before these guys were born. So I’m a bit worried they won’t know any of them. Tragically this also means I’ll miss Britain coming near the bottom of the pile at Eurovision tomorrow night. Nul points!!!

Unlike voters unfairly shunning Britain’s annual song contest entry, markets have been surprisingly well behaved over the last few sessions and have seemingly become becalmed about the current trade spat regardless of the fact that a resolution anytime soon is very unlikely. That was even despite the latest Huawei developments late on Wednesday night. A +0.89% gain for the S&P 500 yesterday means that the index is up for three days in a row and has retraced to being down only -2.65% from the recent highs now. That being said more trade-sensitive sectors and stocks are still struggling. The semi-conductor index for example – which fell -1.68% yesterday – is down -10.00% from the highs of last month, while Apple is still down -10.23% over the past two weeks. Nevertheless, the VIX index continues to slide lower, falling -1.1pts yesterday to back below 16 for the first time in eight sessions.

Yesterday we saw China’s Global Times Editor Hu Xijin – a must follow now on Twitter – tweet that “Since the US has made unfair requests with China, we are willing to accompany the US suffering more and more negative impact though China may take greater pain. We have no choice.” Although grammatically the tweet doesn’t quite make sense it leaves you with the impressions that pride is as important as the economic impact to the Chinese at the moment. On the other side White House Commerce Secretary Wilbur Ross said that President Trump has a “wide range of actions” he could take on auto tariffs. On that, Bloomberg ran a story suggesting that Trump would give the EU and Japan 6 months to curb auto sales into the US in return for delaying new tariffs. So that is a tentative November timetable which means that the uncertainty window has the potential to run for some time now. Imagine if we had Auto tariffs and a hard Brexit occurring within days of each other!! European Autos declined -0.48% yesterday and underperformed the broader STOXX 600 index (+1.27%).

As for other markets, there were decent gains for the likes of the NASDAQ (+0.97%), DOW (+0.84%) and DAX (+1.74x%). High yield credit spreads were -7bps tighter in the US while in bond markets we saw Bunds hold steady at -0.097% while Treasuries weakened +2.5bps to touch 2.40% again. However Europe wasn’t all one-way traffic with BTPs (-6.2bps) standing out and reversing some of the recent underperformance. That appeared to partly reflect comments from the 5SM’s Di Maio who suggested that Italy’s debt-to-GDP ratio won’t breach 140%. On the flip side the League’s Salvini said that the government will “tear apart every single rule butchering Italy” should the League do well in the EU elections. There’s a real good-cop-bad-cop dynamic going on in Italy right now with much of it political posturing ahead of the EU elections. As for currencies, EM FX finished -0.32%, with high yielders like the Brazilian real (-0.98%) and Turkish lira (-0.69%) underperforming. Weak currencies pressured EM equities, with MSCI EM down -0.44%. In other FX space, the euro (-0.24%) was a shade weaker and the dollar rallied +0.28% for its third consecutive advance. Sterling was a bigger mover though, falling -0.37% and below $1.280 following the latest Brexit developments – more on that below.

Overnight, the Trump administration has said that new restrictions on Huawei announced earlier in the week would take effect today, with the parent company and 67 affiliates in 26 countries placed on a blacklist that will limit Huawei’s access to US suppliers, according to the Federal Register notice. The US Commerce Secretary Wilbur Ross also said that Trump has given his department 150 days to establish a process to screen US companies’ purchases of equipment from Huawei, and other equipment providers with which officials have concerns. In the meantime, China’s Toran Notes, a WeChat blog run by state-owned Economic Daily, reported today that if the US doesn’t make any new moves that truly show sincerity, then it is meaningless for its officials to come to China and have trade talks. The blog added that “We can’t see the U.S. has any substantial sincerity in pushing forward the talks. Rather, it is expanding extreme pressure,” citing Trump’s steps this week to curb Chinese telecom giant Huawei while reiterating that China has three main concerns including tariff removal, achievable purchase plans and a balanced agreement text. The blog went on to say, “In addition, if anyone thinks the Chinese side is just bluffing, that will be the most significant misjudgement since Korean War”. The same article was also carried by state-run Xinhua News Agency and the People’s Daily (Communist Party’s mouthpiece). So, rhetoric and actions continues to indicate that neither side is in any rush to temper the recent escalation. Elsewhere, China’s National Development and Reform Commission spokeswoman Meng Wei said that China will “study the possible impact of US tariffs on the Chinese economy, and roll out responsive measures when necessary,” possibly hinting that more stimulus is likely to come.

The above rhetoric from China on not being interested in talking to the US if attitudes don’t change is weighing on Chinese and Hong Kong markets this morning with the CSI (-1.67%), Shanghai Comp (-1.46%) and Shenzhen Comp (-1.66%) all down over 1% while the Hang Seng is down a relatively modest -0.77%. The Nikkei (+1.02%) and Kospi (+0.14%) are both up but they are off their highs since China’s state media reports started filtering in. It’s noteworthy that CNH didn’t rally alongside equities yesterday as it weakened another -0.35% (a further -0.15% this morning), highlighting the continued fears over trade despite the improvement in risk appetite. Elsewhere, futures on the S&P 500 are down -0.28% this morning erasing earlier gains.

Back to yesterday, where our FX strategists published their latest Blueprint report entitled “Stairway to Seven”. With Brexit, trade tensions and geopolitical issues still in play, their bias is for higher volatility and weaker risk appetite. In terms of their trade recommendations, with Europe – and especially Germany – particularly exposed to global risks the team are abandoning their positive view on the euro and see EUR/USD potentially breaking 1.10 through the summer. They are also becoming even more concerned on Asia and see USD/CNY breaking through 7. They do not see a quick resolution to the trade war and argue that Chinese authorities will become more amenable to currency weakness. The JPY should be a continued beneficiary of global volatility and they forecast a move down to 105 in USD/JPY. See their full report here .

Over to Brexit, where Prime Minister May is under ever increasing pressure from within her own party. She met yesterday with the 1922 Committee, which governs the Conservative party’s internal rules and could greenlight a leadership challenge against her via a change in rules. Though she survived without an immediate threat, May also agreed to meet with the Committee again after her WA gets put to another vote. That vote, likely to be held the week of June 3, will be key. As it currently stands, it looks likely to fail. Now that May looks likely to depart if it fails, that lowers the incentive for Labour to cooperate. The odds of a Tory leadership struggle resulting in a hard-Brexit Prime Minister and a subsequent general election have risen. Indeed, that’s why our FX team remains bearish the pound in yesterday’s FX blueprint.

In the US, Fed Governor Brainard, viewed as a good representative of the centre of the FOMC’s thinking, was the latest Fed official to toe the party line on inflation dynamics, calling the latest misses “transitory” and citing the trimmed mean as a truer measure of underlying pressures. However, she did also discuss the potential benefits of letting inflation rise above 2%, in order to “demonstrate to the public our commitment to our inflation goal on a symmetric basis.” That sounds like she would likely support a shift to average inflation targeting or a similar regime next year. Separately, Minneapolis Fed President Kashkari, one of the more dovish FOMC members, echoed her comments, saying the Fed should “actually allow inflation to climb modestly above 2 percent in order to demonstrate that we are serious about symmetry.”

As for the data, given that the releases at the moment are still covering the pre-trade escalation period they are somewhat being taken with a pinch of salt for now. For completeness though, the May Philly Fed PMI rose +8.1pts and far more than expected to 16.6 (vs. 9.0 expected). The details were a bit more mixed though with employment stronger but new orders weaker. As for the April housing data, starts (+5.7% mom vs. +6.2% expected) and permits (+0.6% mom vs. +0.1% expected) missed and beat respectively however both benefited from upward revisions to the prior month. Finally claims declined 16k to 212k and a little bit more than expected following a holiday related spike. No particularly big takeaways overall therefore.

Looking at the day ahead, this morning we’ve got final April CPI revisions due for the Euro Area (no change from the preliminary core reading of +1.2% yoy expected) and March construction output data. In the US the April leading index and preliminary May University of Michigan consumer sentiment survey is due. Away from that the Fed’s Williams is due to meet community leaders at 4.15pm BST and 7pm BST while Clarida is due to speak at a ‘Fed Listens’ event at 6.40pm BST. The BoE’s Brazier is also due to speak at 1pm BST. Elsewhere, EU finance ministers are due to meet in Brussels to discuss a plan for the Euro Area budget.

via ZeroHedge News http://bit.ly/2JNnfMu Tyler Durden