How the U.S.-China trade war plays out is key to the future of U.S. stocks, and while hope is rife on every ‘inspirational’ “constructive” headline, Bloomberg macro strategist Mark Cudmore clarifies the way forward by applying Occam’s razor to the situation, leaving him no choice but to be bearish.

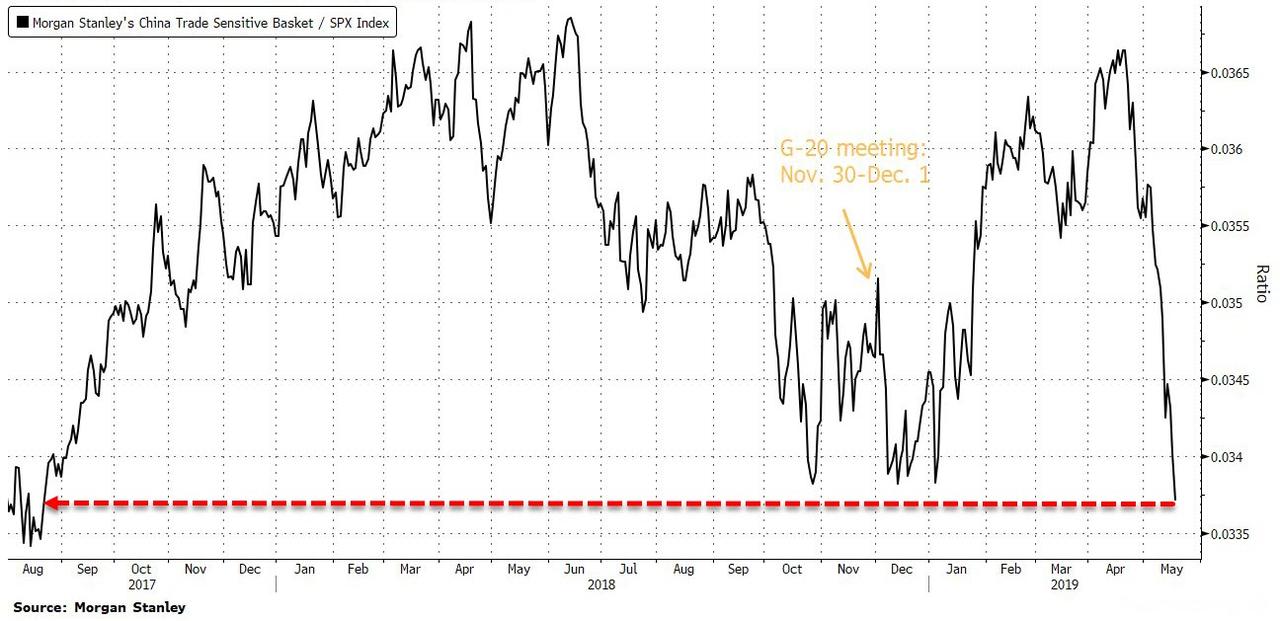

And while headline indices may be rallying overnight on Huawei reprieve hopes, the trend in China-sensitive stocks is not your friend…

Via Bloomberg,

As Cudmore explains, there are obviously a host of other macro inputs. Most that are likely are largely priced and therefore relatively marginal. Unforeseen events, or black swans, significantly skew toward being negative surprises since uncertainty and volatility reduce the risk-reward of having cash tied up in investments.

The trade war is not the only driver of U.S. stocks, but it’s a very large one where the status quo isn’t yet priced and the uncertainty remains high. This arguably makes it the key driver for the rest of 2019 that we can strategize for right now.

There are essentially three scenarios:

1) The trade war escalates further and more barriers are implemented; clearly bad news for stocks

2) The trade war ameliorates and already-implemented measures are lifted; good news for stocks

3) There’s no change to the current situation; equities have a long way to fall as they have not priced in the hit to earnings and the economy from the recently implemented tariffs being a permanent part of the landscape.

I have no extra insight on which way the trade war will play out. Occam’s razor dictates that the outcome that requires the least speculation is most likely to be correct. That means the one where there’s no major shift from the present U.S.-China trading relationship that exists today. That suggests S&P 500 downside, as outlined below…

The recent escalation in the U.S.-China trade war is a game-changer which could put overvalued American stocks through months of pain — for at least the rest of the year.

A few months ago, an increase in bilateral tariffs was seen as 2019’s negative tail-risk. In hindsight, that looks optimistic and U.S. stocks have yet to price in the resulting slowdown in growth and earnings

There’s an assumption it’s just part of negotiations and will soon be resolved. The evidence provides little support for such complacency

The tone in state-sponsored Chinese media has shifted markedly more belligerent this month. Anti-U.S. sentiment is growing rapidly, as shown by a trade war song going viral in Beijing

And the trade tensions are no longer just about tariffs and their drag on growth: The targeting of tech giant Huawei is directly disrupting supply chains. The impact here is perhaps even more damaging for a U.S. equity bull market that has been so dependent on the tech sector

Many U.S.-based investors seem to be slow in registering where the world’s consumer power now lies. Asia has more than 50% of the world’s population, with almost 20% in China alone. This is a tech-savvy, consumption-focused middle-class population with a rising disposable income

Focusing on just the hit to U.S growth misses a large chunk of the negative earnings impact to come for all those Amercian multinationals

After being very bullish U.S. equities for 2019, I turned bearish on April 30 via this column. I highlighted stretched valuations but expected only a multi-week correction before fresh highs later in the year

That was before the trade war escalated. The landscape has changed enormously and those valuations now look far more out of whack

The Bloomberg U.S. economic surprise index has been below zero for almost five months — during a time when most were optimistic toward the trade negotiations. The months ahead will see the outlook deteriorate further

The S&P 500’s blended 12-month forward-looking price-earnings ratio stands at 16.3 versus the 10-year average of 15. Worryingly, that’s before analysts slash estimates further, meaning an even longer way to fall to hit that long-term average

The price-to-book ratio is 3.3, versus the 10-year average of 2.6. The price-to-free-cash-flow ratio is 22 versus the 10-year average of 16.5

And these frighteningly expensive valuations are for just the S&P 500, let alone some of the more-tenuously priced unicorns and tech stocks

It’s not that the world economy is set to collapse. It’s not even that positioning is overly stretched or liquidity conditions are particularly tight. It’s just the value proposition in U.S. equities has suddenly vanished and will only look more negative by the week

When you add in the fact the credit cycle is turning, it gets a little more scary. Then you consider that any Fed power to support financial assets has been significantly diminished with rate cuts already well-priced into markets

At best, the Fed delivers the monetary easing that’s priced, but that’s no guarantee. And how will investors react to the signal of a rate-cutting cycle? The last time they experienced one was in 2008, so it may spark some worrying flashbacks

Cudmore concludes rather ominously:

“I’ve been a structural bull on U.S. equities for many years. I’ve had periods of being tactically bearish that have lasted for several months. The most recent one began April 30. But, for the first time since long before I joined Bloomberg News in 2014, I’m wondering if it’s time to become a structural bear on U.S. stocks.

All I know for sure is that the game has changed significantly and investors have not yet realized. That makes me very nervous…”

But there is a silver lining (of sorts) as Bloomberg’s Richard Breslow reminds investors, it’s not the economy, it’s not the trade-deal, and it’s not earnings… It’s the central banks, stupid!!

Here’s what’s on the other side of the ledger from a stock market that is easy to hate but continuously holds the levels it has to: dovish central bankers who are receiving very little pushback, trillions of dollars worth of negative-yielding debt, and credit swaps that look like they have taken a pause from tightening. Add to that emerging markets that are looking decidedly squishy and a dollar that has remained stubbornly bid.

It’s certainly reasonable to argue that equities may have put in a top for now. Maybe for longer than now. But it is too early to call the market broken until it breaks. Easy for me to say, I know, because there is a lot to be pessimistic about. Maybe we’ll finally see an episode where political risk does overwhelm the rate-setters. It just hasn’t happened yet with lasting effect. While the indexes sometimes look ugly and the news sounds even worse, the fact remains that the strong hands are still the ones most constructive for the long haul.

Equities have dealt with non-believers for years during the whole way up. The bulls put it down to skill and the bears describe a less flattering view of things. Every time the market holds a level and the dip is bought, Willie Nelson’s lyrics come to mind: “The winners tell jokes and the losers say deal. Lady Luck rides a stallion tonight. And she smiles at the winners and she laughs at the losers. And the losers say now that just ain’t right.”

All sounds a little bit ‘Dirty Harry’ to us: “Do you feel lucky, punk?”

via ZeroHedge News http://bit.ly/2HunA59 Tyler Durden