Submitted by DataTrekResearch.com,

An acquaintance of ours is in the plate and glassware trade, supplying luxury hotels and resorts in the US with Chinese-made tableware. From our conversations over the years we have learned this is a really good business. Orders tend to be custom made since the hotel/resort typically wants their name on the items. That means nice margins for our friend. And, of course, plates and glasses break during normal usage in a commercial setting. So demand is pretty constant, even outside of replacement/upgrade cycles.

When the US and China first started levying tariffs, we asked him what he was doing to offset the incremental expense. His reply: “No man… I don’t have to deal with that. Plates and glasses aren’t on the tariff list. All my customers think it’s because your President buys a lot of plates for his resorts and hotels.”

With that, he changed the topic to why Hermes men’s loafers are so much better than comparable Gucci footwear. As we said, he does well with plates and glasses.

That exchange has stuck with us, and a recent World Trade Organization report on global value chains reminded us that things are rarely as straightforward as our friend portrayed. Plates and glasses are an example of simple value chain: discreet products produced in one country and bought by another. But in reality that’s not how global trade typically works, as the report shows.

Here are our 3 key takeaways from the WTO report of interest to investors just now (link at the end of this section):

#1. “More than two thirds of global trade occurs through global value chains (GVCs), in which production crosses at least one border, and typically many borders, before final assembly.” The historical growth patterns for these multi-country value chains look like this:

- “From 2000-2007, GVCs (especially complex ones) were expanding at a faster rate than other components of GDP.”

- “During the global financial crisis there was naturally some retrenchment of GVCs, followed by quick recovery (2010 – 2011) but since then, with the exception of 2017, growth has, in the main, slowed.”

Takeaway: as with so many other things the Financial Crisis left a lasting mark on global trade, slowing the growth of complex multinational supply chains. You’ve probably seen some scary charts recently about the decline in global trade over the last few years – the slowing expansion of GVCs plays an important part in that.

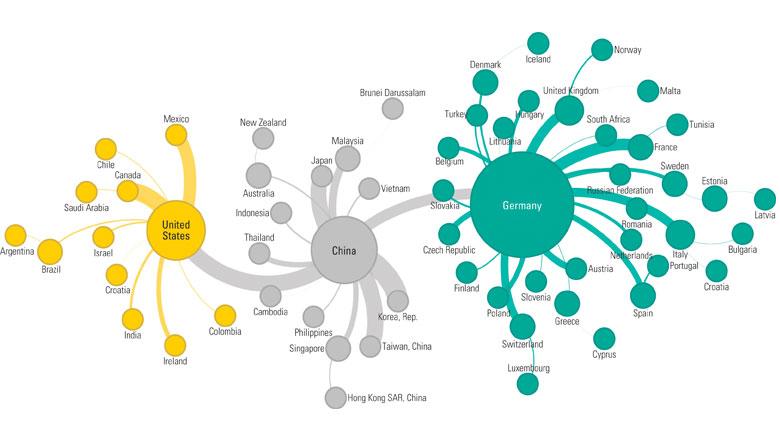

#2: There are distinct loci of GVC concentration, both by industry and geography:

- “GVC linkages are especially important for high-tech sectors and it is in these areas that we see highly complex value chains involving many countries.”

- “Between 2000 and 2017, the weight of intra-regional GVC activities in “Factory Asia” came to exceed that of “Factory North America”. Over the same time, however, both North America and Europe became more interconnected via GVCs with China.”

- The WTO paper makes a distinction between “complex” GVCs, where the US and Germany are the most important hubs, and “simple” GVCs where China has the lead because it is both a source of demand and supply.

Takeaway: to the degree to which the current US-China trade war forces a reassessment of global value chains, Tech as an industry and the US, China and Germany have the most exposure.

#3: Since most global trade is parts and components en route to eventual final assembly, simple bi-lateral trade numbers tell an incomplete picture.

- “China happens to be at the end of many Asian value chains, taking sophisticated components from Japan, the Republic of Korea, and Chinese Taipei and assembling these into final products.”

- “the Chinese domestic value content of their exports of ICT (information and communication technology) products accounts for only around half the total export value.”

- “the US trade deficit in ICT products with China is cut roughly in half if the calculation is made in value added terms.”

Takeaway: the current US-China trade war may look like a two-country dispute about trade deficits but its effects are far broader. A smartphone or laptop made in China may have components from Korea and Japan, be assembled in a factory owned by a Taiwanese company, and use US designed software. Increase tariffs on those products, and lower demand will ripple through the entire supply chain.

Final thought: the WTO report is a useful reminder of the complexities of global trade. So far, capital markets have focused on the first-order effects like today’s Tech sector selloff on the Huawei news. That’s fair enough – Tech is very exposed, as the WTO work highlights. But the uncomfortable truth is that complex global value chains simply have a life of their own. We won’t know what effects a disruptive trade war will have until they bubble up to the surface.

Source: WTO Report

via ZeroHedge News http://bit.ly/2JzuQ1z Tyler Durden