According to conventional wisdom, anybody who has remained bearish on global markets since the financial crisis has not only lost a boatload of money, but has missed out on the opportunity to cash in on one of the most torrid bull markets in recent memory. They should also be out of business, insolvent or both.

However, as Horseman Global’s Russell Clark has proven over and over again, this is not the case at all. . A few years back, we anointed Horseman “The world’s most bearish hedge fund” for a very simple reason: Of all existing asset managers, Horseman may be the one with the biggest and longest net short position in history. Just look at the chart below, which shows not only that Clark’s net exposure was a remarkable $-60.58% (after -88.14% in March), with a gross short position of 108%, but that he had been effectively net short since 2011.

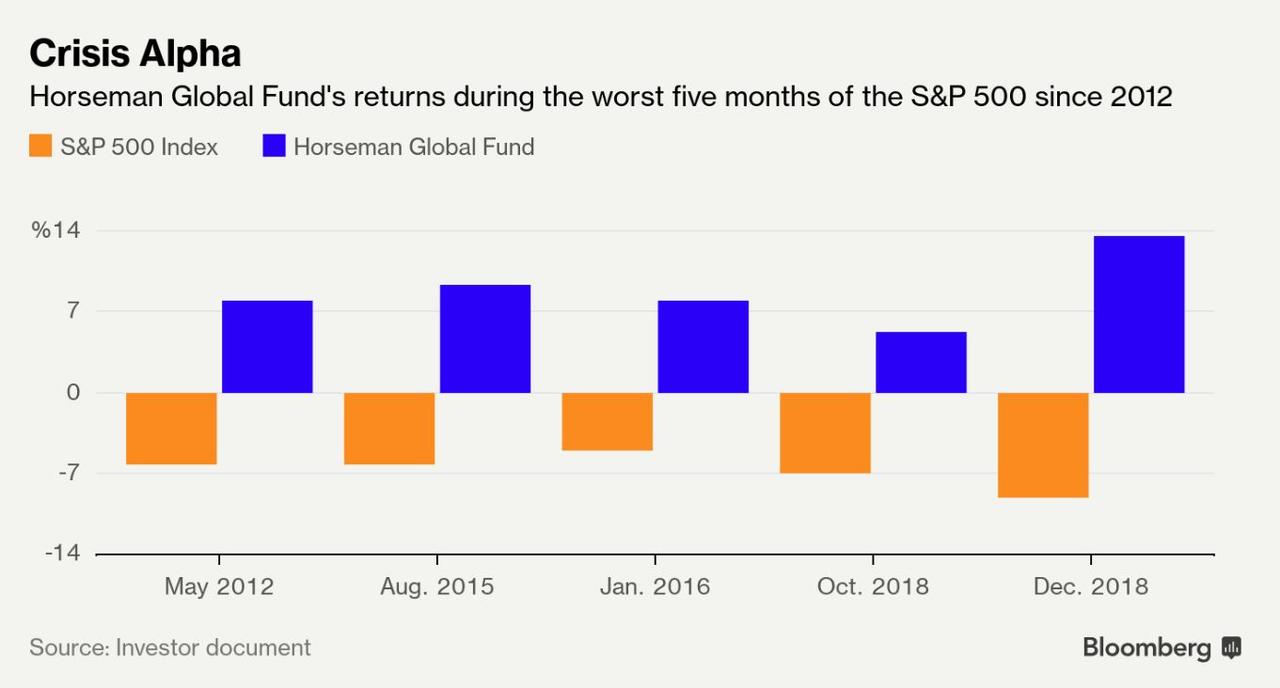

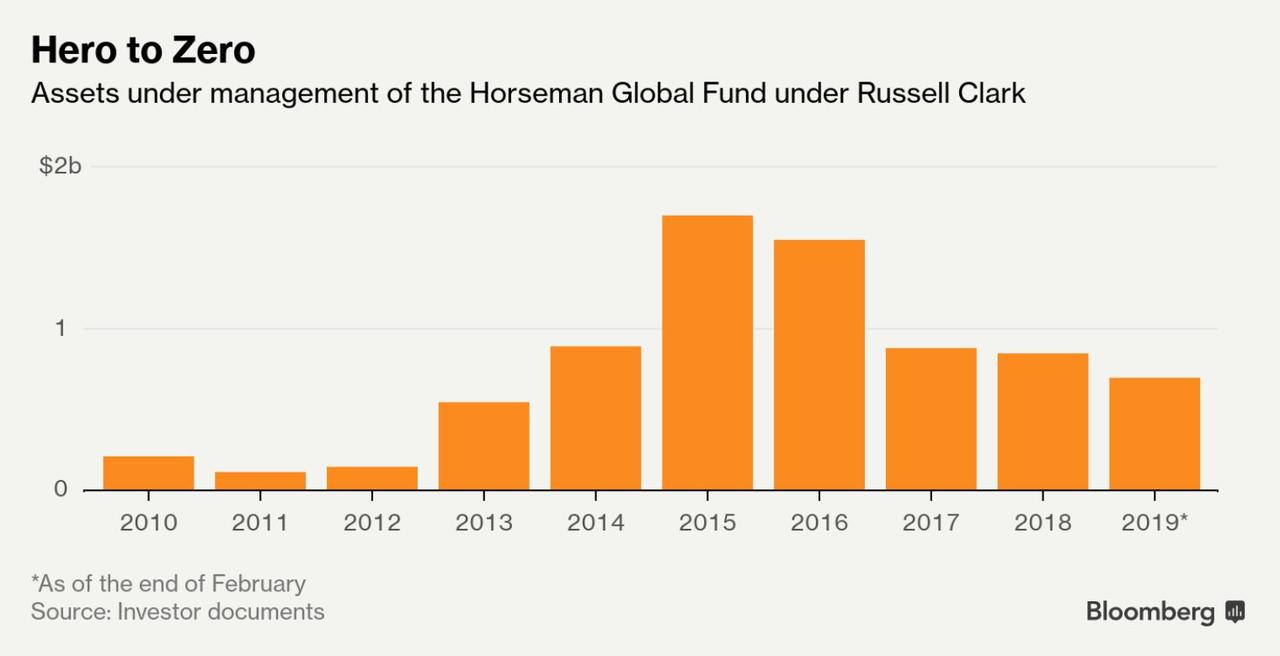

Yet, to assume that Clark has either thrown in the bearish towel, or somehow lost his shirt over the past ten years would be a mistake. Actually, his fund outperformed the S&P 500 for the period between 2012 – when he first went net short – until the end of 2018, only underperforming in 2016. In 2014, Clark posted double-digit returns when oil prices cratered (he was short). In 2013, he made money shorting Brazilian equities. He started with just $111 million when he took over the fund in January 2011, but AUM peaked at $1.5 billion in 2015.

However, the fund’s inconsistent performance (it’s not unusual for Horseman to be up or down 5% in a single month) has alienated some investors who are uncomfortable with the volatility, even as Horseman has bested most other hedge funds in terms of performance, as one former investor told Bloomberg.

Tim Ng, chief investment officer of Princeton, N.J.-based Clearbrook Global Advisors LLC, says his fund pulled its money for similar reasons. “The stretches of negative performance and the high volatility of monthly returns became a consistent drag on our portfolio’s overall return, which prompted us to redeem,” he says.

But after a bruising Q1, when Clark got crushed by the torrid rally in US equities, more LPs have pulled out, and AUM has shrunk to just $713 million.

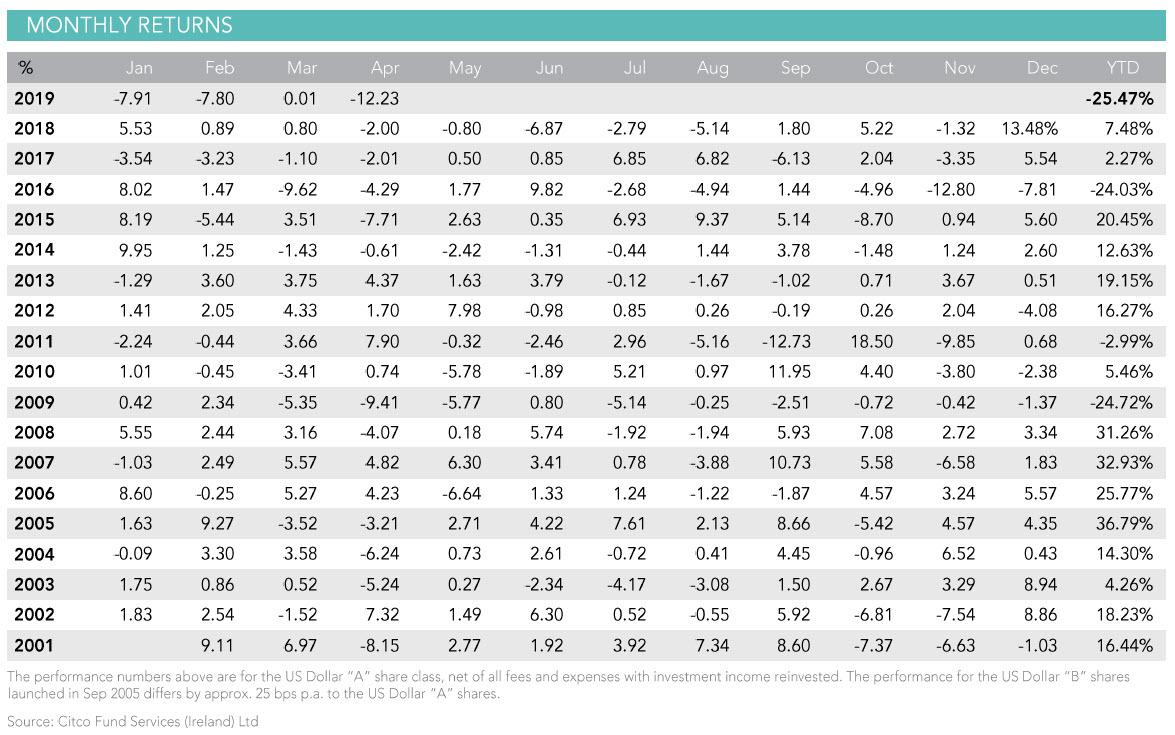

And unfortunately for Clark, after a dismal Q1, the fund’s losses more than doubled in April, when the Fund was down a was a staggering 12%, which has brought its total loss YTD to more than 25%.

Unfortunately for Horseman investors, in April the fund suffered a 12.23% drop as the market melted up just ahead of Trump’s renewed trade and tech war on Beijing and Huawei. The drop was the second worst month in the hedge fund’s history after it lost 12.73% in September 2011, when the market ripped as many shorts (Clark included) pressed their positions after the US downgrade by S&P.

So what happens next? Well, as we noted two weeks ago, Clark is convinced that the crash is almost upon us, warning recently that “the stars are aligning, and the markets are complacent,” and urging clients to “get the popcorn ready, it’s showtime.”

But not quite yet, because as Clark wrote in his latest investor letter, “your fund lost 12.23% this month. Losses came mainly from the short book.“

What follows are excerpts from Clark’s latest letter to investors explaining just what happened in April, and also why the fund may be in for a remarkable recovery in May:

The fund went seriously wrong this month. And as it went wrong, I could see that this was going to be very bad news for me. Not only was I losing a large amount of my own money, I was losing investors’, friends’ and family’s money. I was also losing trust and respect and causing untold problems to the very small group of people out there who are still willing to back macro funds, or funds that are willing to use a short book.

Normally when the fund is performing poorly, it is easy for me to pick out what went wrong and why. What went wrong, is that the semiconductor stocks have been the best performing sector this year. The problem is, it is hard to understand why these stocks have rallied so hard. Earnings are poor, chip prices are falling, Chinese capacity is coming on stream and inventories are high. These are not the conditions for new highs. It is very unusual behavior.

To be sure, we posted our own observations on the bizarre outperformance of semiconductor stocks in early 2019, especially in the context of what the March Beige Book said was “semiconductor orders from China plunging the most since the collapse of Lehman”, predicting the SOX party should have been long over.

A subsequent report by IHS Markit also found the semiconductor market was lurching into the worst-in-a-decade downturn in 2019, and noted that the 7.4% decline in semi revenue will mark the semiconductor industry’s biggest annual percentage decrease since the Great Recession year of 2009, when chip sales plunged by nearly 11%:

Going back to the Horseman letter, Clark writes that “one reason we were so heavily short semiconductors was because I felt I had a good hedge to the semis in a large short USD position, and a long basic materials position, often in areas that had large shorts against them. I typically choose a long book that is meant to protect the fund from the short book as markets are squeezed higher. But in this case the long book was not working.”

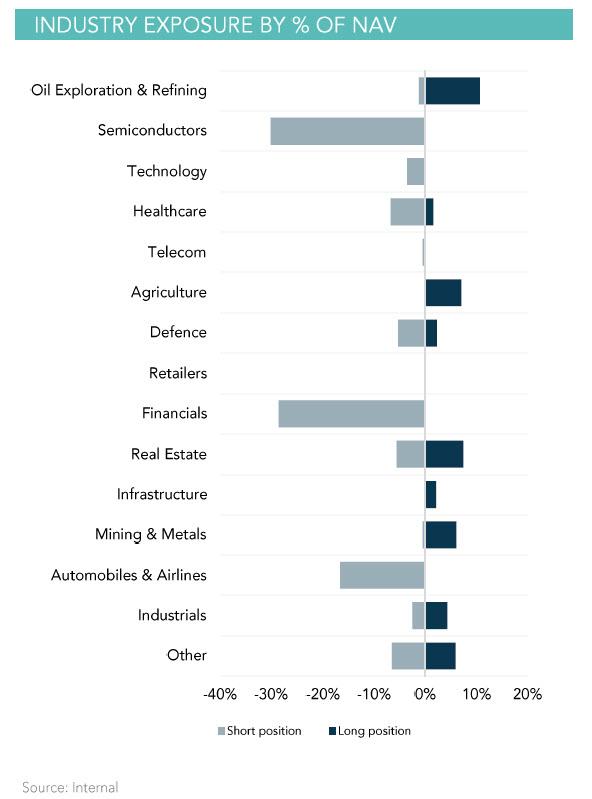

And when he says “heavily short”, he isn’t kidding: as the next chart shows, even more so than his financial short, Horseman’s biggest short was a massive -30% net position in semis. No wonder the fund got crushed in April, if only due to semis.

Clark continues, writing that instead of dwelling “on why semiconductors were going up, I looked at why our long book was not doing so well. On a day to day basis, materials look great. Iron ore prices are back to 2008 highs, oil has bounced with markets and Chinese cement prices are strong. I decided to dig deeper and look at the global steel market. And here was where I was most surprised. Chinese steel production was growing at 9% year on year, while the rest of the world was contracting. When I looked at the Chinese property sector, USD debt has returned to the leading companies. Suddenly everything became clear.”

And just in case it isn’t clear to everyone, he explains:

Markets turned around in 2016 when it became obvious that the Chinese policy of cutting capacity and pushing up commodity prices was the real deal. This was Chinese policy to create inflation internally to the benefit of corporates and the financial sector. However, it seems these polices have been reversed, and share prices of Chinese steel companies and banks are beginning to reflect these problems again. If the US dollar stays strong, and China cannot create inflation internally, then they are going to be forced to devalue. Many of the long positions of the fund began to reflect this at the end of April, including mining stocks and currencies.

This Chinese weakness explains the move in tech and semis this year. Investors are busy rotating out of classic emerging market assets such as commodities, steel, capital goods and autos, and moving it to “secular” growth stories like tech, utilities, healthcare and staples. Semis are pushed higher by these flows, even with bad earnings and worse outlooks.

So what does that mean for portfolio of “the world’s most bearish hedge fund”? While we already know the bad news, here’s some good news: On the core themes of higher volatility and autocallables blowing up, both are made more likely according to Clark, who notes that “semis are also still shorts, and so are autos, financials and aerospace. But commodities are a problem. And so we are selling large chunks of the long book.”

This began in April and will continue in May. I have a rule that when I cut a profitable position (which is most of the commodity longs) I cut a loss-making position (which has mainly been in the short book) so the gross is falling, even as the net stays very short. We have also cut the longs Australian dollar, Euro and Chinese yuan positions from the FX book.

Finally, now that doubts are emerging that 2019 is a mirror image of 2016 and the first Shanghai Accord with Chinese policy beginning and attempts to reflate the world failing, “the likelihood of sustained inflation is beginning to disappear” according to Horseman. As a result, “deflation again looks more likely, just as it did from 2011 to 2016.” The punchline:

And just like we did back then, it’s time to move the portfolio back to a deflationary positioning. We have begun to add 30-year treasuries to our existing Japanese Government Bond position. Your fund is long bonds and short equities (and long volatility).

As for whether the disastrous April plunge in the fund’s P&L will repeat, the best new for Clark is that after a relentless ramp higher, none other than Donald Trump came to Horseman’s rescue, with the recent return of US-China trade – and the most violent escalation in global tech war – meaning that much if not all of the April losses are now revered, and Horseman will have a far better YTD performance after May.

The question, as always, is whether LPs will have the patience to keep invested in such a volatile, stomach-churning hedge funds as the one which, with its money where its mouth is, claims month after month that the Fed is not only wrong, but on the verge of failure.

* * *

One final point: Clark’s assiduously dedicated contrarianism has earned him a cult following among professional investors. Though his name isn’t as widely known as an Ackman or a Loeb, his interview with RealVision was one of the company’s most requested videos from 2018, largely thanks to his reputation built up on these pages over the past 5 years as the “world’s most bearish hedge fund”, yet one which stubbornly refuses to throw in the towel.

Despite a wave of redemptions in 2016, 2017 and 2018, Clark, who keeps the bulk of his own wealth in Horseman, has retained an unflappable confidence in his investing view: “When people hate you and write terrible things about you, it tends to be the best time to invest.“

via ZeroHedge News http://bit.ly/2K1ZobO Tyler Durden