It is a sea of green in global markets today, with European stocks rallying as Germany’s carmakers outperformed, following a torrid session in Asia where the Shanghai Composite soared by 2.6%, as risk appetite refuses to go away after the United States stepped back from imposing tariffs on Mexico, while losses in treasuries and gold accelerated.

Advances in European miners and carmakers pushed Europe’s Stoxx 600 Index almost 1% higher, on course for a sixth day of gains in the last seven, with Frankfurt’s DAX racing up 1.2% as German investors returned from a one-day holiday, even as investor confidence in its economy fell to the lowest since 2010. BMW, Daimler and VW – seen as sensitive to trade tariffs – all gained between 1.8%-2%, mirroring a 1.9% gain for the auto sector.

Emini futures also continued their relentless June surge, with the S&P set to open above 2,900 for the first time in over a month.

“It looks like we will have to wait to see at the end of the month, to see what the next move will be,” said David Madden, an analyst at CMC Markets. “In that time, if nothing is said, stocks could press on higher – the belief that the Fed will all of a sudden become dovish is really driving markets.”

The MSCI world equity index, which tracks shares in 47 countries, advanced 0.24%. Wall Street futures were also seen opening higher, with S&P500 mini futures up 0.26%.

Earlier in the session, in Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan gained 0.9% hitting the highest level since May 8, with Shanghai’s bourse climbing 2.6% after news that the country’s finance ministry said that it would loosen restrictions on how local governments spend money on infrastructure raised from selling special bonds helping offset the threat by President Donald Trump to raise tariffs again if President Xi Jinping doesn’t meet with him at the Group of 20 summit at month’s end. As a result, Asian stocks were set to post their biggest three-day gain since January as the risk-on mood spread across the region. Australian stocks also contributed to today’s strong climb. The S&P/ASX 200 Index closed 1.6% higher and reached fresh high for this year, as Vocus Group Ltd. soared after AGL Energy Ltd. offered to buy the company for about $2 billion. India’s S&P BSE Sensex also extended its gains into the third day. In emerging markets, stocks gained and currencies strengthened the most in a week. Oil edged up near $54 a barrel in New York.

Iron ore futures surged on the China spending plan, and the onshore yuan recovered after closing at its weakest level of the year. In emerging markets, stocks gained and currencies strengthened the most in a week. Oil edged up near $54 a barrel in New York.

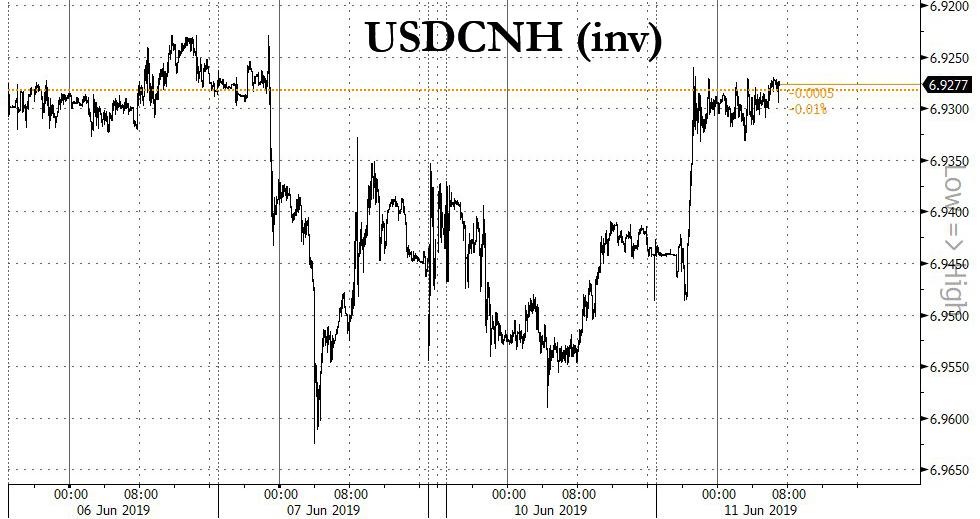

After hitting its lowest level for 2019, with the “redline” level of 7.00 looming, China’s yuan jumped as much as 0.27%, the most in three weeks, as the central bank set its daily fixing at a stronger-than-expected level. The onshore currency was headed for its first gain in five sessions after the People’s Bank of China fixed its reference rate at 6.8930 per dollar, stronger than the average forecast of 6.9089 in Bloomberg’s survey of 21 traders and analysts. The central bank also said it plans to sell bills in Hong Kong in late June to improve the yield curve of yuan bonds. This comes after the yuan weakened to its weakest level since November on Monday, bringing it closer to 7 per dollar, a level it hasn’t breached since the financial crisis.

PBOC Governor Yi Gang said last week he was not wedded to defending the currency at a particular level. The fixing shows “China will still manage the pace of depreciation and the yuan will not break 7 so soon,” said Tommy Xie, an economist at Oversea-Chinese Banking Corp. “Even though the door has opened, China needs a proper catalyst.”

PBOC’s plan to sell bills in Hong Kong in late June and its stronger-than-expected fixings are a clear message it will defend the yuan at 7 per dollar, according to Standard Chartered. “The purpose is very very clear, that they just want to defend the currency regardless of the G-20 meeting” outcome, said Becky Liu, head of China macro strategy in Hong Kong. This new bill issuance is set to be around the G-20 meeting; if those talks are positive, the market will likely steady and the bill issuance size will be smaller; however, if the meeting disappoints, the PBOC can step up the amount and frequency of bill issuance in Hong Kong as “a very practical way to defend the currency.”

Elsewhere in FX, the dollar held steady above a 2-1/2 month low with rising expectations for a Fed rate cut tempered by a reluctance to close positions before the G20. “The markets are pricing in a 25-basis-point rate cut in July,” said Peter Schaffrik, head of European rates strategy at RBC Capital Markets, adding that expectations of looser policy would likely continue. “When you see the narrative that the market is painting, that it is all down to the negative implications from the trade war and the reduction of global trade,” he said. “It’s difficult to see how any one data point will change the entire picture.”

In rates, US Treasuries edged lower, with the 10 Yield rising to 2.17% after hitting a 2 year low of 2.05% on Friday. Amid the cautious optimism, a rally in longer-dated euro zone government bonds stalled as the pick-up in risk sentiment globally sparked a sell-off in the bloc. Germany’s 10-year bond yield, seen as a benchmark for government debt, was up 3 basis points at minus 0.23% – still a smidgeon away from last week’s record lows. Thirty-year bond yields in Germany and France were up as much as 8 basis points in early trade.

In commodities, oil prices rose, bolstered by firmer financial markets and expectations that producer group OPEC and its allies will keep withholding supply. Brent crude futures were at $62.67, up 0.4%. As noted above, gold (-0.4%) continues to fall at the whim of a firmer risk appetite, whilst in terms of base metals, copper (+0.9%) extends on its gains aided by the risk tone and Dalian iron ore surged 6% on supply woes amid expectations that miners will be unable to expand output to meet higher steel demand. Subsequently, JPM modestly upgraded its Chinese steel demand and iron ore price forecasts, noting that the peak disruption “is likely behind us”.

Today’s economic data include small business optimism. HD Supply, Wiley are due to report earnings

Market Snapshot

- S&P 500 futures up 0.4% to 2,901.75

- STOXX Europe 600 up 0.6% to 380.64

- MXAP up 0.7% to 157.13

- MXAPJ up 0.9% to 514.11

- Nikkei up 0.3% to 21,204.28

- Topix up 0.5% to 1,561.32

- Hang Seng Index up 0.8% to 27,789.34

- Shanghai Composite up 2.6% to 2,925.72

- Sensex up 0.5% to 39,990.92

- Australia S&P/ASX 200 up 1.6% to 6,546.29

- Kospi up 0.6% to 2,111.81

- German 10Y yield fell 0.2 bps to -0.221%

- Euro up 0.07% to $1.1320

- Brent Futures up 0.1% to $62.35/bbl

- Italian 10Y yield unchanged at 1.991%

- Spanish 10Y yield fell 2.1 bps to 0.583%

- Brent Futures up 0.1% to $62.35/bbl

- Gold spot down 0.4% to $1,322.97

- U.S. Dollar Index down 0.01% to 96.75

Top Overnight News from Bloomberg

- Chinese stocks posted their best gains in weeks on the news that local governments will have more room to spend on infrastructure, offsetting U.S. President Donald Trump’s latest threat to raise tariffs on China if President Xi Jinping doesn’t meet with him at the upcoming Group-of-20 summit in Japan

- China’s central bank moved to shore up the yuan with a stronger-than- expected fixing and a planned bond sale in Hong Kong

- Citigroup was suspended from the primary group of dealers that participate at certain Japanese government bond auctions after it was found to have manipulated futures prices

- The Bank of England doesn’t have to wait until all political uncertainty around Brexit is resolved to raise interest rates, according to policy maker Michael Saunders

- A record 10 British Conservatives will fight each other to replace Theresa May as prime minister. All agree that Britain has to leave the European Union, but most of them vow to renegotiate. Current favorite Boris Johnson says he will deliver Brexit in October with or without a deal

- The Bank of England doesn’t have to wait until all political uncertainty around Brexit is resolved to raise interest rates, according to policy maker Michael Saunders

- Australian business confidence surged after Prime Minister Scott Morrison’s shock election win, while conditions again deteriorated, providing further grist to the central bank’s decision to cut interest rates

- The U.S. expressed “grave concern” over Hong Kong legislation that would for the first time allow extraditions to mainland China, raising pressure on Beijing as the city braced for a potentially historic showdown over the proposal

- The Trump administration’s fight against China’s Huawei Technologies Co. justifies Russia’s decision to build a “sovereign internet” to protect its domestic network from external threats, according to Russian Deputy Prime Minister Maxim Akimov

Asian equity markets were higher across the board after a similar lead from US where sentiment was underpinned by the US-Mexico tariff relief which lifted the S&P 500 and DJIA to a 5-day and 6-day win streak respectively, although gains in the region were initially capped amid a lack of fresh catalysts. ASX 200 (+1.6%) and Nikkei 225 (+0.3%) traded positively with early outperformance in Australia as it played catch up on return from the extended weekend and with Vocus Group the largest gainer following a takeover offer from AGL Energy, while the Japanese benchmark was just about kept afloat by a weaker currency. Elsewhere, Hang Seng (+0.8%) and Shanghai Comp. (+2.6%) conformed to the upbeat tone despite another net liquidity drain by the PBoC and mixed comments by US President Trump who stated that a trade deal with China will work out because of tariffs but warned the next USD 300bln of tariffs will come into effect if Chinese President Xi does not come to the G20. Nonetheless, mainland China outperformed after China issued notice encouraging investment in local government special bonds issuance for project financing and amid reports that the PBoC may continue to support banks through various tools. Finally, 10yr JGBs were lower as yields tracked the rebound in their US counterparts and with demand for Japanese bonds also sapped by gains in stocks and after weaker demand in the enhanced liquidity auction for longer-dated bonds.

Top Asian News

- China Car Slump Extends to a Year With No Rebound In Sight

- China Sets Yuan Fixing Stronger Than Expected in Sign of Defense

- When This Chinese Newspaper Editor Tweets, Wall Street Listens

- India’s World-Beating Growth May Not Be so Fast After All

European equities are higher across the board [Eurostoxx 50 +0.9%] following on from a similar lead in Asia wherein Mainland China closed with gains in excess of 2.5%. Germany’s DAX (+1.3%) is outperforming its peers as the index plays catch-up following yesterday’s holiday. Sectors are broadly in the green with the exception of defensive sectors amid the current “risk on” mood, whilst material names are outperforming as Dalian iron ore futures spiked 6% higher on supply concerns and copper prices rose almost 1% on the firmer risk sentiment. In terms of in individual movers, Thyssenkrupp (+5.5%) sits near the top of the Stoxx 600 as the steel name benefits from the aforementioned iron ore spike. Elsewhere, German autos are supported (BMW +1.6%, Daimler +1.8%, Volkswagen +1.8%) as the stocks react to the weekend US-Mexico developments for the first time. Finally, Hugo Boss (+4.3%) shares were bolstered amid an upgrade at Morgan Stanley.

Top European News

- Lloyds Tests U.K. Utility Industry Exposure as Corbyn Risk Looms

- Alitalia Rescue Stalled as Govt Eyes New Deadline: Repubblica

- Novo Nordisk Climbs After Rival Lilly’s Disappointing Trial Data

- Danske Tells Debt Issuers to Act Fast as Orders Get Erratic

In FX, GBP rose on more hawkish leaning BoE rhetoric, as Saunders follows Haldane on the rate hike path has been validated to a degree by the latest UK labour report revealing firmer than forecast wages, and in particular an unexpected pick-up in ex-bonus earnings, in stark contrast to Monday’s dismal GDP and industrial output figures. Hence, the Pound has rebounded across the board with Cable back above 1.2700 and testing yesterday’s pre-data peaks ahead of resistance seen around 1.2740, while Eur/Gbp has reversed from fresh multi-week highs circa 0.8932 through 0.8900.

- NZD/JPY/CHF/AUD – In contrast to Sterling’s revival, the Kiwi has extended losses to 0.6588 vs its US counterpart and 1.0550+ against the Aussie, which is also weak compared to the Buck but holding up better around 0.6950 ahead of jobs data on Thursday. Nzd/Usd saw accelerated selling on a break of 0.6600 and market participants also noted stops in Nzd/Jpy when 71.81 failed to hold, with a variety of model and spec offers pushing the cross down to 71.54. Similarly, the Yen and Franc have weakened a bit further vs the Dollar as the DXY sits tight between 96.832-673, with Usd/Jpy hovering above 108.50 within a 108.36-73 range and Usd/Chf holding closer to the upper end of a 0.9923-0.9893 band. Note, however, Usd/Jpy may well be drawn towards decent option expiry interest at 108.50 in 1.1 bn.

- CAD/EUR – The Loonie continues to outperform, as technical impulses turn increasingly bullish and Usd/Cad trade below the 200 DMA (1.3273) towards 1.3250 and post-NA jobs data lows of 1.3225, while the single currency remains above 1.1300 where more expiries lie (1.1 bn) even though Eurozone Sentix sentiment soured significantly and ECB’s Rehn reiterated that all monetary stimulus options will be available if growth weakens further. On the flip-side, Eur/Usd is still butting up against resistance ahead of 1.1350 and the 200 DMA (1.1365), including option barriers and more expiries, like 2.3 bn from 1.1340 to 1.1350 and 2.8 bn at 1.1360.

- NOK – The Norwegian Crown slipped in wake of considerably sub-consensus CPI metrics that called into question firm Norges Bank guidance for a rate hike at this month’s policy meeting, but Eur/Nok reversed from a probe over resistance around 9.8300 to revisit pre-inflation data levels sub-9.7800 on the back of an upbeat regional survey that restored June tightening expectations. Conversely, Eur/Sek has seen more upside towards 10.6900 ahead of Sweden’s inflation update on Friday and potential pointers from Prospera’s expectations survey tomorrow.

In commodities, WTI (+0.8%) and Brent (-0.3%) futures are choppy as the benchmarks are benefitting from the improved risk tone,with the former around USD 62.50/bbl and the latter hitting a session peak just under USD 54.00/bbl. News flow has been light for the complex as participants eye tonight’s EIA Short term Energy Outlook report and API inventories release with the street looking for a headline draw of 1.25mln barrels. Elsewhere, Energy Intel’s Senior Correspondent notes that Russian Energy Minister Novak requested a delay to the OPEC/OPEC+ meeting (originally scheduled for June 25/26) as a later date would give key participants the chance to discuss the issue more at the G-20 summit on June 28. The correspondent also notes of that Iranian officials are yet to agree on the new proposed dates to move the OPEC meeting from June to early July, according to sources and the current secretariat is looking at the option of holding OPEC meet in June and the non-OPEC in July. Elsewhere, gold (-0.4%) continues to fall at the whim of a firmer risk appetite, whilst in terms of base metals, copper (+0.9%) extends on its gains aided by the risk tone and Dalian iron ore surged 6% on supply woes amid expectations that miners will be unable to expand output to meet higher steel demand. Subsequently, JPM modestly upgraded its Chinese steel demand and iron ore price forecasts, noting that the peak disruption “is likely behind us”.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 102, prior 103.5

- 8:30am: PPI Final Demand MoM, est. 0.1%, prior 0.2%; PPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%

- 8:30am: PPI Final Demand YoY, est. 1.95%, prior 2.2%; PPI Ex Food and Energy YoY, est. 2.3%, prior 2.4%

DB’s Jim Reid concludes the overnight wrap

Since I moved out of London 9.5 years ago I’ve had a 1 to 3 mile commute to the station depending on whether I use the local or mainline station. I’m proud of the fact that outside of my leg being in a brace I’ve walked or cycled pretty much every day over that period. I’ve seen heavy rain, hail, lightening, snow and even Saharan sand fall from the skies whilst getting to and from the station. However I have to say that yesterday I took one look out the window first thing and also at the forecast and really didn’t fancy it so I drove. It proved to be one of the best decisions I’ve ever made as the rain was biblical in London and the surrounds yesterday with no real respite all day. I can’t remember a summer day like it. I’m back on my bike today and hopefully I’ll remember to change out of my Lycra in time to appear live on Bloomberg TV this morning at 10am. So catch me if you are able.

I suspect (and hope) the appearance won’t be as memorable as President Trump’s live phone interview with CNBC yesterday which drove much of the conversation around markets. To say that the interview was wide-ranging would be an understatement. While Trump proudly touted his weekend agreement with Mexico which averted higher tariffs, he also emphasised how his threats were key to reaching an agreement. He said “tariffs are a beautiful thing” and that “without tariffs, we would be captive to every country.” Trump did go on to say that China is “going to make a deal because they’re going to have to make a deal,” though he said that no bilateral meeting with President Xi was yet scheduled for the G-20 at the end of June. After US markets closed, headlines from the Chinese media broke suggesting that the two leaders will meet, but the details have yet to be hammered out. Meanwhile, Trump said to reporters outside the White House after the CNBC interview that he could impose tariffs of 25%, or “much higher than 25%” on $300 billion in Chinese goods, if Chinese President Xi Jinping doesn’t meet with him at the upcoming G-20 summit in Japan. Elsewhere, the US VP Pence said overnight that the US is going to stand firm on China while adding we are in a very strong position on the country.

Back to the CNBC interview, Trump also criticised the Federal Reserve, saying they have been “very disruptive to us,” and spoke admiringly of China’s system where President Xi has more direct influence on the PBoC. Two-year Treasury yields fell -2.8bps while Trump was speaking, but ultimately retraced to end the day +5.0bps higher at 1.90%.

Apart from the move in Treasuries, risk assets barely budged during his comments, as they were still being helped higher by the halo effect of no Mexican tariffs being imposed after the announcement late last Friday night. The +0.45% gain for the S&P 500 last night, although down from the +1.09% session highs, means that the index has risen for five consecutive days – the first time that has happened since April. It has now posted a +4.88% return for June to date so far which is the best start to a month since October 2011, taking the index to just 2.01% below its all-time peak. The NASDAQ also rallied +1.05% yesterday which means it’s up by an even larger amount this month (+4.96%), while semiconductors are the real standout after rising +2.54% yesterday (+9.08% in June). In Europe a +0.21% gain for the STOXX 600 means that index is up a solid +2.50% so far in June too. Meanwhile it’s been a much more sideways 10 days for rates following that fairly decent rally through May. For example, 10y yields are +2.0bps higher now following a +6.4bps climb yesterday, while the yield curve is +4.3bps steeper in June at 24.3bps following yesterday’s +1.6bps move. Bund yields rose +3.7bps to -0.219%, the first time in five sessions that they didn’t close at a new all-time low. Germany was on a public holiday though so trading was thin.

This morning in Asia markets are following Wall Street’s Lead with the Nikkei (+0.29%), Hang Seng (+0.76%) and Kospi (+0.31%) all up while Chinese bourses are up c.2% with the CSI 300 +2.33%, Shanghai Comp +1.87% and Shenzhen Comp +2.82%. Elsewhere, futures on the S&P 500 are up +0.17%.

In other overnight news, the PBoC fixed a higher reference rate for the yuan today at 6.8930 (vs. expectations of 6.9089). The move comes after the onshore yuan traded at weakest level of the year yesterday at 6.9311. The central bank has also said that it plans to sell bills in Hong Kong later this month, a move that will drain liquidity and support the currency. The onshore yuan is trading up +0.20% at 6.9170.

Moving on. Once again Italian assets traded to their own beat again yesterday with the FTSE MIB opening higher, then wiping out those gains by late morning before ultimately closing +0.61%. In bonds, 10y BTP yields closed flat, despite rising as much as +7.6bps earlier in the session. Italian PM Conte grabbed the early attention on the wires, telling Corriere della Sera that the Italian government would be effectively over if Italy can’t make a budget compromise with the EU. Deputy PM Salvini, who admittedly has regularly shifted his positions depending on circumstances, said that a confrontation with the EU “is the last thing we want to do.” Data in Italy also showed a big slump in industrial production in April of -0.7% mom (vs. 0.0% expected). It’s worth noting that despite the ongoing and justified concerns around Italy, 10y BTPs are still trading at around the lowest yield (2.358%) since the new government was elected last year.

Meanwhile, news from the UK economy was nearly as bleak as the weather yesterday following a weak April GDP reading of -0.4% mom (vs. -0.1% expected). While the extent of the drop was a surprise, the slump being led by a big drop in autos output was less so with car companies closing production plants preparing for a no deal Brexit last month. Sterling dropped -0.35% yesterday which helped the FTSE 100 to a +0.59% gain. It’s worth noting that we get the April and May employment stats in the UK today so that should be worth watching in light of yesterday’s data. After that attention will shift to Thursday’s first ballot for the Conservative leadership contest. The field is officially set with 10 contenders, with Boris Johnson leading according to the bookmakers, who give him around a 56% chance of winning the contest. Jeremy Hunt and Andrea Leadsom are next in line with roughly 17% and 10% chances, according to the betting markets. Elsewhere, the BoE MPC member Michael Saunders, a hawk, said in an overnight speech that “The MPC does not necessarily have to keep rates on hold until all Brexit uncertainties are resolved, the MPC has already raised rates twice since the Brexit vote. We will act again if needed to ensure a sustained return of inflation to target over time.” Our UK economists, however, changed their view last week forecasting that the BoE will no longer hike rates this year and see rising risks that the Bank rate has reached its terminal point, with the weak April GDP reading further reinforcing their view. To read their complete note click here .

Over in the US, the JOLTS report on the condition of the US labour market was released, showing still-robust conditions despite the disappointing nonfarm payrolls report. The quits rate, which has led wage growth fairly reliably, stayed at its cyclical high of 2.6%, while the hiring rate also stayed high at 4.3%. Separately, the New York Fed published its Survey of Consumer Expectations, which showed that 3-year inflation expectations have fallen to 2.59%, their lowest level since May 2017.

Looking at the day ahead, as well as the employment data in the UK this morning we’ll also get the May Bank of France industrial sentiment reading and Sentix investor confidence reading for the Euro Area. In the US we’ll get the May NFIB small business optimism reading, before the focus turns to the May PPI report. Away from that the ECB’s Nowotny and Rehn are due to speak this morning while over at the BoE we’re due to hear from Saunders, Tenreyro and Broadbent.

via ZeroHedge News http://bit.ly/2R4LEyB Tyler Durden