This may be the shortest post-G-20 “trade truce rally” yet, because one day after global markets jumped, with the S&P hitting record highs even though nothing material was announced in the aftermath of US-China trade talks, the rally fizzled and global stocks eked out only meager gains, while US equity futures dropped in the red, following a fresh escalation in the US trade conflict with the EU, and amid renewed worries the global economy was faltering after data showed manufacturing activity slowed last month, snuffing appetite for risk.

The MSCI All Country World Index was barely higher in early trading, up for a fourth straight day, although should the US open in the red, the rally will likely end. On Monday, stocks rallied enthusiastically after the US postponed imposing another round of tariffs on Chinese products and the two countries agreed to continue negotiations on trade.

But just one day later, skepticism of further gains emerged after discouraging manufacturing surveys in the past 24 hours and a threat of additional US tariffs on European goods. “It’s clear that the tariffs already in place will continue to take a toll on global and domestic growth and with Trump now turning his attention on Europe, the early bullish bias seems to ease again,” said Konstantinos Anthis, head of research at ADSS.

As reported last night, the U.S. Trade Rep’s office released a list of additional products – including olives, Italian cheese and Scotch whiskey – that could be subject to tariffs, on top of products worth $21 billion that were announced in April. The new U.S. tariff threats against Europe also point to a worrisome prospect of a broadening trade dispute, said Michael McCarthy, chief markets strategist at CMC Markets in Sydney, in a note to clients.

“The problem is the widening of the dispute. Europe, the U.S. and China account for almost two thirds of global GDP,” he said. “An ongoing disruption to trade between these three major economies, prosecuted for domestic political purposes, could sink global growth.”

Despite being the subject of Lightlizer’s latest wrath, the European Stoxx 600 index managed a modest 0.2% advance, although Airbus dropped 1% as the United States stepped up pressure in the long-running dispute over aircraft subsidies. The euro climbed after Bloomberg reported ECB policy makers don’t see a need to rush into a July rate cut.

European bonds advanced alongside U.S. notes, and the yield on two-year Italian debt dropped below zero for the first time since the coalition government was formed in May 2018.

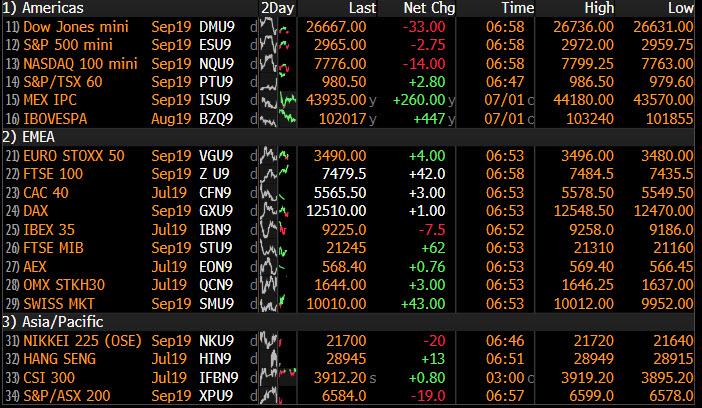

![]()

Earlier in the session Asian shares gained for a second day led by communications and utilities, as Washington and Beijing prepare for a new round of trade negotiations, with the MSCI index of Asia-Pacific shares ex-Japan adding 0.28%, helped by a 1.23% gain in Hong Kong shares as investors caught up to Monday’s global rally. Markets in Hong Kong had been closed on for a holiday. Most markets in the region edged higher after Trump said new trade talks with China is underway, ending a stalemate between the two countries amid escalating tariffs. The Topix gauge rose 0.3% for its best two-day advance since February, with technology firms among the biggest boosts; Japan’s Nikkei finished up 0.11%. The Shanghai Composite Index fluctuated and closed flat, as China Shipbuilding Industry jumped on restructuring talks, countering declines in Kweichow Moutai. The S&P/ASX 200 index pared earlier gains to close 0.1% higher after Australia executed its first back-to-back rate cuts in seven years. The S&P BSE Sensex Index edged up 0.1%, driven by Housing Development Finance and Infosys

Australian shares were flat, pulling back from earlier gains after the Reserve Bank of Australia cut its benchmark interest rate by 25 basis points to a record low 1.0%, as expected, which curiously sent the AUD sharply higher. However, the RBA left limited room for more cuts, raising the possibility of unconventional policy easing.

In FX, the dollar fell against most G-10 peers, paring Monday’s rally, which was the best in more than two months. The Australian dollar led gains, climbing after the central bank cut rates as expected – its first back-to-back rate cuts in seven years – and said further policy adjustments depended on growth and inflation data. The euro rose above $1.13 after ECB policy makers were said to be not ready to rush into additional monetary stimulus at this month’s meeting. The safe-haven yen strengthened against the dollar, which fell 0.2% to 108.24 yen per dollar, and the euro was flat at $1.1288. Most Asian currencies dropped, with the won leading declines.

In debt markets, Italian government bonds rallied after Italy cut its 2019 budget deficit target to avoid European Union disciplinary action, potentially easing another major concern for markets.

In commodity markets, oil gained as OPEC agreed to extend supply cuts until next March, although prices were pressured by worries demand may ease amid hints of a slowdown in the global economy. Treasuries climbed amid mixed trading in global stocks.

In commodities, oil fluctuated as investors weighed OPEC’s extension of output cuts into 2020. Spot gold added over half a percent to $1,392.11 per ounce. Bitcoin crashed, tumbling below $10,000 after rising to $13,000 less than a week ago.

No major economic data is expected today. Acuity Brands and Simply Good Foods are reporting earnings, while Ford, Tesla, and other carmakers release their U.S. monthly sales.

Market Snapshot

- S&P 500 futures down 0.1% to 2,963.50

- STOXX Europe 600 up 0.09% to 388.22

- MXAP up 0.3% to 162.04

- MXAPJ up 0.3% to 532.45

- Nikkei up 0.1% to 21,754.27

- Topix up 0.3% to 1,589.84

- Hang Seng Index up 1.2% to 28,875.56

- Shanghai Composite down 0.03% to 3,043.94

- Sensex up 0.2% to 39,778.57

- Australia S&P/ASX 200 up 0.08% to 6,653.21

- Kospi down 0.4% to 2,122.02

- German 10Y yield fell 0.3 bps to -0.36%

- Euro up 0.04% to $1.1291

- Italian 10Y yield fell 13.3 bps to 1.607%

- Spanish 10Y yield fell 1.9 bps to 0.317%

- Brent futures down 0.3% to $64.88/bbl

- Gold spot up 0.6% to $1,393.11

- U.S. Dollar Index down 0.1% to 96.79

Top Overnight News from Bloomberg

- While ECB Governing Council members agree that they could act on July 25 if the outlook deteriorates, they are said to be currently leaning toward the following meeting when they’ll have updated economic forecasts to back up their decision. The council might tweak its policy language this month to signal more stimulus is imminent

- The U.S. added more European Union products to a list of goods it could hit with retaliatory tariffs in a long-running trans-Atlantic subsidy dispute between Boeing Co. and Airbus SE. The Trade Representative’s office in Washington on Monday published a list of $4 billion worth of EU goods to target

- China will scrap ownership limit for securities, futures and life insurance companies by 2020, one year ahead of the original plan of 2021, Premier Li Keqiang says at the World Economic Forum in Dalian. China will keep yuan at a reasonable and equilibrium level and won’t resort to competitive depreciation

- Jeremy Hunt said he would “100% not” suspend Parliament to force through a no-deal Brexit, drawing a dividing line with Boris Johnson as the two men entered the last days of campaigning before Tory activists start voting for the U.K.’s next prime minister.

- OPEC will extend production cuts into 2020, attempting to buoy oil prices as the world’s leading exporters fret about the outlook for global demand growth and the relentless rise in output from America’s shale fields. Oil edged lower as investors weighed troubling economic data from around the world against OPEC’s extension of output cuts into 2020.

- Iran said it had exceeded limits set on its enriched-uranium stockpile, a move that risks the collapse of the 2015 nuclear accord and raises concerns that a standoff with the U.S. could lead to military action

- Italy’s populist government lowered its 2019 budget deficit goal to 2% in a bid to comply with European Union rules and avoid sanctions for failing to rein in debt. Market relief drove Italian bonds higher

- Australia’s central bank governor signaled he’ll stand pat in coming months to observe the impact of back-to-back interest rate cuts, while standing ready to resume easing should the outlook at home or abroad take a turn for the worse

- London bankers are bracing for thousands of job cuts. Nomura Holdings Inc., Japan’s biggest brokerage, let go of 30 people in April. HSBC Holdings Plc and Deutsche Bank AG are cutting jobs. In an atmosphere that may be the gloomiest since the financial crisis, some are jumping before they’re pushed

Asian equity markets traded indecisive as the euphoria from the US-China trade truce began to wane and with the region looking ahead to this week’s key risk events. ASX 200 (U/C) was underpinned by strength in mining names and amid a widely anticipated back-to-back rate cut from the RBA, while Nikkei 225 (+0.1%) was choppy and largely reflected the price action in the domestic currency. Elsewhere, Hang Seng (+1.2%) and Shanghai Comp. (U/C) were mixed with the mainland dampened after another liquidity drain by the PBoC, while Hong Kong outperformed as it played catch up on return from the extended weekend and amid declines in money market rates, with casino stocks among the biggest gainers following the strong growth in Macau gaming revenue. Finally, 10yr JGBs were subdued by the indecisive risk tone and after mixed results at the 10yr JGB auction failed to spur prices.

Top Asia News

- Credit Suisse Hires UBS Veteran as Asia Head of Equity Research

Major European indices are mixed and overall largely unchanged [Euro Stoxx 50 U/C] as sentiment deteriorated overnight with the notable development being that the US Trade Representative Office has proposed increasing tariffs on EU products as a result of the aircraft subsidies; with a proposed USD 4.0bln of additional tariffs being added. The tariffs would be on-top of the USD 21bln worth of tariffs announced by the USTR in April, with the products in question encompassing a vast range including whisky, iron tubes and cheese; a public hearing on these additions is scheduled for August 5th. Airbus (-0.9%) are afflicted on these additions as they are at the center of the European aircraft subsidies. Similarly, sectors are mixed with utilities and consumer staples outperforming on the day. In terms of this mornings notable movers, Adidas (-0.4%) opened lower after a downgrade at HSBC. Separately, but still within the Dax (-0.2%), Deutsche Bank (-0.7%) have slipped into negative territory as the broader index deteriorates on the back of negative comments from the VDMA this morning; however, the Co. did open around 1.1% higher on reports that they are considering lowering their capital buffer in order to fund the Co’s overhaul. Finally, Casino (+2.0%) are higher after selling 8 stores.

Top European News

- Italy Cuts 2019 Deficit Goal to 2% in Bid to Avoid EU Procedure

- Salvini Seizes Economic Reins to Take on EU in Budget Battle

- U.K. Construction Posts Worst Month Since 2009 on Brexit Worries

- Polish Banks Warn of $16 Billion Risk From EU Ruling, Puls Says

In FX, the Aussie has staged another strong rebound from fleeting overnight lows as bears quickly seized the opportunity to book profits in wake of the RBA’s decision to cut the OCR by another 25 bp, and other short positions were covered/squeezed on the accompanying statement suggesting no rush to ease again at the next policy meeting. Subsequently, comments from Governor Lowe appear to affirm a wait-and-see stance given back-to-back moves and Aud/Usd is inching closer to 0.7000 from 0.6958 lows, while Aud/Nzd has rebounded from sub-1.0450 towards 1.0500, with the Kiwi independently hampered by a further deterioration in NZIER business sentiment and ASB’s call for 2 more RNBZ rate reductions. Consequently, Nzd/Usd is hovering closer to the bottom of a 0.6657-80 range and eyeing the latest GDT auction next.

- GBP/EUR – The Pound has tumbled to the base of the G10 pile on the back of June’s UK construction PMI that confounded expectations for a modest recovery and slumped even deeper into contraction at 43.1, much worse than the manufacturing miss on Monday. Moreover, components like housing and new orders were bleak, as the former fell below zero for the first time in 17 months and the latter weakened the most in over a decade. Cable is clinging to 1.2600 and Eur/Gbp is edging up towards 0.8960 as the single currency rebounds further from daily chart support vs the Dollar ahead of a Fib (circa 1.1277 and 1.1259 respectively) on ECB sourced reports downplaying July rate cut speculation. However, Eur/Usd faded around 1.1320 and could be drawn back towards decent option expiry interest between 1.1295-1.1300 (1 bn), especially after considerably weaker than forecast German retail sales data and some bleak numbers/outlooks from the likes of the DIHK and VDMA.

- JPY – The Yen retains a relatively firm underlying bid on safe-haven grounds as the initial post-G20 euphoria dissipates and attention shifts back to the global slowdown and geopolitical factors, like the ongoing US-Iran spat. Hence, Usd/Jpy remains capped around 108.50 and the 30 DMA (108.55), but also confined on the downside at 108.00 given a generally firm Greenback as the DXY has bounced further from recent lows and back over the 200 DMA (96.690) into a loftier 96.624-879 band.

- RBA lowered the Cash Rate by 25bps to a record low 1.00% as expected and stated that it cut rates to support employment growth, as well as provide greater confidence on inflation. RBA noted that the economy can sustain a lower rate of unemployment and that employment growth remains strong, while it added that the outlook for the global economy remains reasonable and that there are signs house prices are stabilizing in Sydney and Melbourne. (Newswires)

In commodities, the oil complex is somewhat subdued as the G20-driven positive sentiment waned. Brent (-0.4%) and WTI (-0.4%) have failed to find much support this morning on OPEC agreeing to extend the oil output cut by 9-months; with the OPEC+ meeting commencing today and the press conference expected at around 12:00 BST. In terms of recent commentary sources indicate that Russian Energy Minister Novak has given his support to the extension, with the deal to be signed soon. Nonetheless, markets will remain on guard for any dissent at today’s meeting from the non-OPEC members, with the joint verdict on an extension not expected until the OPEC+ press conference. From a technical perspective for WTI, PVM highlight that USD 59.07/bbl and USD 58.57/bbl are the two ‘pivot points’ to keep an eye on. Looking ahead, aside from the OPEC+ meeting we have the API report which last week posted a headline draw of -7.55mln BPD. Gold (+0.5%) has reverted back towards the USD 1400/oz level after yesterday’s G20-induced decline; with today’s reversion stemming from a decidedly less-positive market sentiment than yesterday. However, the USD 1400/oz level remains elusive for the yellow metal this morning, for reference session high is currently just over USD 1397/oz. In contrast to yesterday’s gains, copper has remained largely negative throughout the session as risk sentiment turning negative is weighing on the red metal.

US Event Calendar

- Wards Total Vehicle Sales, est. 17m, prior 17.3m

- 6:35am: Fed’s Williams Speaks on Global Economic and Policy Outlook

- 11am: Fed’s Mester to Speak on Economy in London

DB’s Jim Reid concludes the overnight wrap

Before the weekend we sent birthday party invites out to Maisie’s new classmates for September when she starts full time nursery. Yesterday we got over 10 acceptances from parents we don’t know yet and it makes me very worried that this is going to start an endless cycle of party invites that I’m going to increasingly find it hard to plan my weekends around. So my question to parents out there with more experience is what’s the best I can get away with in terms of party/round of golf ratio? Is 1:10 a bit optimistic? Maybe I’ll request to home school the twins to avoid the next round of this in a year or so’s time. My wife has promised a children’s entertainer but without booking one yet. So all recommendations as to what will go down well with 4 year olds are very welcome!

It wasn’t a full on risk party yesterday as markets shifted between optimism over the weekend developments on the trade war and renewed macro concerns yesterday, but ultimately the S&P 500 still closed +0.76% at a fresh all-time high. That was below its opening level of +1.23%, but is nevertheless just 35pts from the psychologically significant 3,000 level. Sentiment did fade from the early highs possibly as the aftermath of the Trump/Xi talks was light on details after deeper inspection. Indeed, China has not actually confirmed any details and markets are a little confused as to what happens next. Also the offshore yuan, a very trade war-exposed asset, has actually reversed all of its rally from Sunday night.

The NASDAQ and DOW also traded down from their opening highs of +1.80% and +1.09% to end the day at +1.06% and +0.44%, respectively. Semiconductor stocks rallied +2.65%, boosted by the trade headlines and the apparent de-escalation against Huawei, while energy stocks lagged at +0.10% as oil prices declined after the OPEC meeting (more below). European bourses also peaked at their open but held onto decent gains by the close, with the STOXX 600 rising +0.78% and DAX +0.99%. The DAX is also up +20.61% from the December lows now which means it’s entered a bull market if that’s your definition of one!

Overnight one of the main stories has been the US Trade Representative’s office publishing a list of $4 bn worth of EU goods that the US could hit with duties as retaliation for European aircraft subsides, particularly to Airbus. It adds to a list of EU products valued at $21 bn that the USTR published in April, according to the release. The USTR said a public hearing on the proposed additional $4 billion worth of products will be held on August 5th and added that, “the final list will take into account the report of the WTO Arbitrator on the appropriate level of countermeasures to be authorized by the WTO.” As a reminder, the WTO has found that the EU subsidies violate international trade rules and it’s expected to decide this summer on the amount of countermeasures the US can impose. Staying with trade, President Trump said that a new round of trade talks with China is already underway as negotiators are speaking on the phone.

This morning in Asia markets are trading mixed with the Nikkei (+0.09%) up while the Shanghai Comp (-0.06%) and Kospi (-0.27%) are down. The Hang Seng is up +1.35% as Hong Kong’s market reopened after a holiday to catch up with yesterday’s move in markets. Elsewhere, futures on the S&P 500 are up +0.12%.

In other news, China’s Premier Li Keqiang said in a speech at the WEF this morning that China will scrap ownership limits for securities firms, futures businesses and life insurance companies by 2020, one year ahead of the original target of 2021. The rule change would mean foreign entities could wholly own firms in those sectors. Li also said that China is working on deeper tax cuts for businesses and it should reach CNY 2tn while adding that China remains concerned about prohibitive financing costs for smaller and medium sized businesses and will work towards the need for more monetary and fiscal support for these companies.

Back to yesterday and credit also had a good day with HY spreads 7bps tighter in the US and -6bps tighter in Europe. EM performed well with the MSCI EM equity index climbing +1.19% and EM FX +0.15%. In bonds, the big move was BTPs which rallied -13.5bps and closed at 1.967% after catching a bid with the wider risk on move, though they were also helped by unconfirmed reports that the European Commission will not recommend an excessive deficit procedure against the country as was possible as early as today (per Bloomberg). Clemente De Lucia has a writeup on the current state of play available here . The rally pushed BTP yields below 2% for the first time since May last year and with Bunds ‘only’ -3.0bps lower (albeit to a new low of -0.357%) – the BTP-Bund spread is now at 232bps and the lowest since last September. The global stock of negative yielding debt is now at $12.83tn with yesterday’s moves in rates and remains close to recent all time high of $13.01tn.

Meanwhile Treasuries were quiet all things considered, with 10y yields rising +2.4bps and back above Italian yields. Two-year yields rose +3.2bps, as markets continued to price out the odds of a 50bps cut at the Fed’s meeting later this month. The current odds are now just 20%, from 44% last week. That caused the 2st10s curve to flatten -0.7bps. In commodities, oil prices slipped -2.40% after OPEC announced an extension of its production cuts through next March but failed to reach an agreement on deeper cuts. There were also unconfirmed reports of disagreements within the cartel as well, which caused the meeting’s press conference to be delayed and sent a negative signal about future cooperation.

Moving onto the data, the general risk on came despite what was a pretty weak set of PMIs across the globe yesterday. In fact, over Sunday and Monday we counted 35 different manufacturing PMIs of which 19 came in below 50 and a worrying 27 dropped month on month. The hope will be that a trade truce can stabilise things but there’s obviously concern that the damage has already been done and will need firmer resolution to reverse it.

Notwithstanding these numbers it was the ISM manufacturing in the US which was most anticipated and to be fair the reading was better than expected at 51.7 (vs. 51.0 consensus) even if it was down -0.4pts from May. Less positive was the new orders component which dropped -2.7pts to 50.0 – the lowest since December 2015 – although employment rather encouragingly rose 0.8pts to 54.5. A few moving parts but it’s hard to ignore the fact that this was still the lowest headline ISM manufacturing reading since October 2016.

Just coming back to the final manufacturing PMIs in Europe, the Eurozone reading was revised down -0.2pts to 47.6 from the flash print and was -0.1pts lower than May. Germany (45.0 vs. 45.4 flash) and to a lesser extent France (51.9 vs. 52.0 flash) also saw downward revisions while the biggest miss was reserved for Spain (47.9 vs. 49.5 expected) which fell -2.2pts from May and also hit the lowest level since April 2013. Italy (48.4 vs. 48.7 expected) also disappointed with output and new orders falling for the eleventh consecutive month too. That also marks the ninth successive sub-50 reading. Of the 13 EU countries that reported manufacturing PMIs yesterday, only 5 posted a reading of greater than 50 with Hungary (54.4) leading the way.

Indeed the weakness includes the UK where the manufacturing PMI slumped to 48.0 last month versus expectations for a 49.5 reading. That is also a drop of-1.4pts from May and the lowest reading since February 2013. The details showed that output fell and new orders remained in negative territory too. In fact most of the sub-indices were lower with the associated text noting that “the stranglehold of sustained Brexit-related uncertainty and disruption also weighed heavily on business confidence and employment, as optimism ebbed to one of its lowest levels in the survey history”. Our UK economists noted that current levels are now consistent with prior BoE easing so this will likely increase the scrutiny of the BoE maintaining a tightening bias in the communication. We should also note that consumer credit data for May also slipped yesterday to £0.8bn. Sterling fell -0.46% yesterday while 10y Gilts ended -1.9bps lower.

As for the remaining US data, the final June manufacturing PMI was revised up +0.5pts to 50.6 which actually means it was up 0.1pts from May. Finally construction spending in May was confirmed as falling -0.8% mom, though the April figure was revised up 0.4pp.

In other news, the ECB’s new chief economists Lane made fairly dovish comments during a speech in Helsinki. This was notable as the market is still fairly new to Lane. He said that “the effectiveness of the policy toolkit means that we can add further monetary accommodation if it is required to deliver our objective” and that “it is essential that a central bank shows consistency in its monetary policy decisions by proactively responding to shocks that might delay convergence to the target or move inflation dynamics in an adverse direction”.

Meanwhile, the ECB’s Knot, one of the more hawkish members on the Governing Council, said that it is “indisputable” that inflation is too low in the euro area. He went on to say that it’s “important to underline the Governing Council stands ready to act decisively” if necessary. This contrasts with his remarks from earlier this year, where he said that price appreciation in the Dutch housing market was “exuberant” and advocated for “doing something about this.”

To the day ahead now, where this morning we’ll get the May retail sales data in Germany, June construction PMI in the UK and May PPI reading for the Euro Area. In the US the only data due is the June vehicle sales numbers. Away from the data we’ve also got scheduled comments due from the Fed’s Williams at 11.35am BST and the Fed’s Mester at 4pm BST. The ECB’s Knot and BoE’s Carney are also due to speak today. The other event is the OPEC+ meeting in Vienna where a press conference is expected at the end, however with output cuts being extended it’s unlikely that we’ll get much new news.

via ZeroHedge News https://ift.tt/2NBGfkC Tyler Durden