First it was the shocking junk bond fiasco at Third Avenue which led to a premature end for the asset manager, then the three largest UK property funds suddenly froze over $12 billion in assets in the aftermath of the Brexit vote; two years later the Swiss multi-billion fund manager GAM blocked redemptions, followed by iconic UK investor Neil Woodford also suddenly gating investors despite representations of solid returns and liquid assets, and most recently the ill-named, Nataxis-owned H20 Asset Management decided to freeze redemptions.

By this point, a pattern had emerged, one which Bank of England Governor Mark Carney described best when he said last month that investment funds that promise to allow customers to withdraw their money on a daily basis are “built on a lie.”

And now, the chief investment officer of Europe’s biggest independent asset manager agrees with him, because while for much of 2019 the biggest risk bogeymen were corporate credit, leveraged loans, and trillions in negative yielding debt, gradually consensus is emerging that investment funds may be the basis for the next liquidity crisis.

“There is no point denying we are faced with a looming liquidity mismatch problem,” said Pascal Blanque, who oversees more than 1.4 trillion euros ($1.6 trillion) as the CIO of Amundi SA, according to Bloomberg’s Mark Gilbert who in a Bloomberg View piece writes that Blanque told him that the prospect of melting liquidity is one of “various things keeping me awake at night.”

Continuing the discussion of illiquid institutions, Blanque said that market making, where firms generate prices at which they are willing to either buy or sell financial products, is effectively “a public good” (or “public bad”, if it is being done by HFTs who disappear at the first sign of volatility, and them having to take on real positional risk). Of course, as that activity declines, the drop in turnover reduces the banking industry’s exposure to a collapse in prices or a surge in volatility. But the dangers are simply transferred, rather than diminished.

“Market making is falling off a cliff at the level of individual banks, but creating a systemic problem,” Blanque told Gilbert. “The banks are less risky – but the risks have been shifted to the buy side.”

As we have discussed extensively in the past, and as Gilbert reminds us, following the global financial crisis, as part of their macroprudential duties, regulators forced investment banks to bolster their balance sheets, which in turn reduced the amount of capital those institutions are able to commit to the securities markets, resulting in a creeping shortage of liquidity when it comes to market making, not only at buyside institutions but also market making banks.

“Market making is falling off a cliff at the level of individual banks, but creating a systemic problem,” Blanque says. “The banks are less risky – but the risks have been shifted to the buy side.”

Blanque is probably referring to a recent report from Deutsche Bank (which should know systemic risks better than anyone), which last month published a report titled “Investment Funds – The next liquidity crisis”, in which it wrote that recent events, i.e. the abovementioned collapse of GAM, Woodford and H20, have been “a timely reminder of the potential risks of illiquid securities within open-ended mutual funds offering daily liquidity.” Citing the FSB (Financial Stability Board), Deutsche Bank noted that over half of global intermediation now happens outside the banking system, and that the assets of NBFIs (Non-bank financial Institutions) have grown by over 50% since 2008.

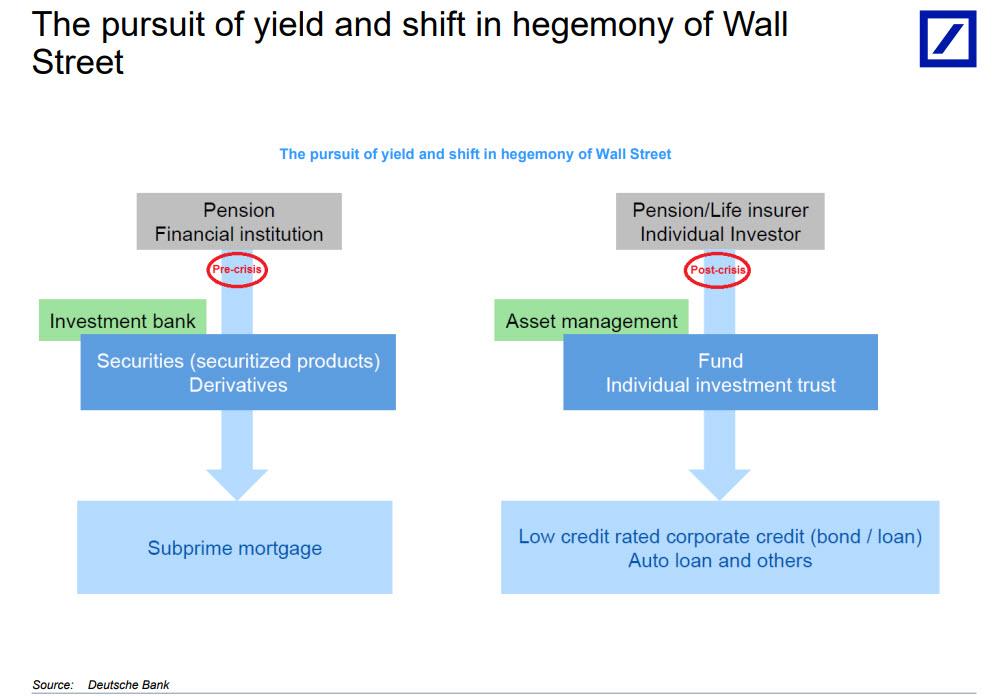

The bank showed this transformation in the pursuit of yield and “shift in the hegemony of Wall Street” in the following chart showing the transition from pension and financial institutions (mediated by investment banks), to pension insurers and individual investors (mediated by at times extremely illiquid asset managers) in the following chart.

Deutsche goes on to show how liquidity risks have shifted, highlighting – like Blanque noted – that while post-crisis banking regulations have materially reduced liquidity (and other) risks within the banking system, some of these risks have been merely transferred to the unregulated NBFI ecosystem, notably mutual funds.

And this is where sudden, unexpected blow ups like Woodford, GAM and H20 are especially jarring as they are an indication of what to expect once the broader market locks up.

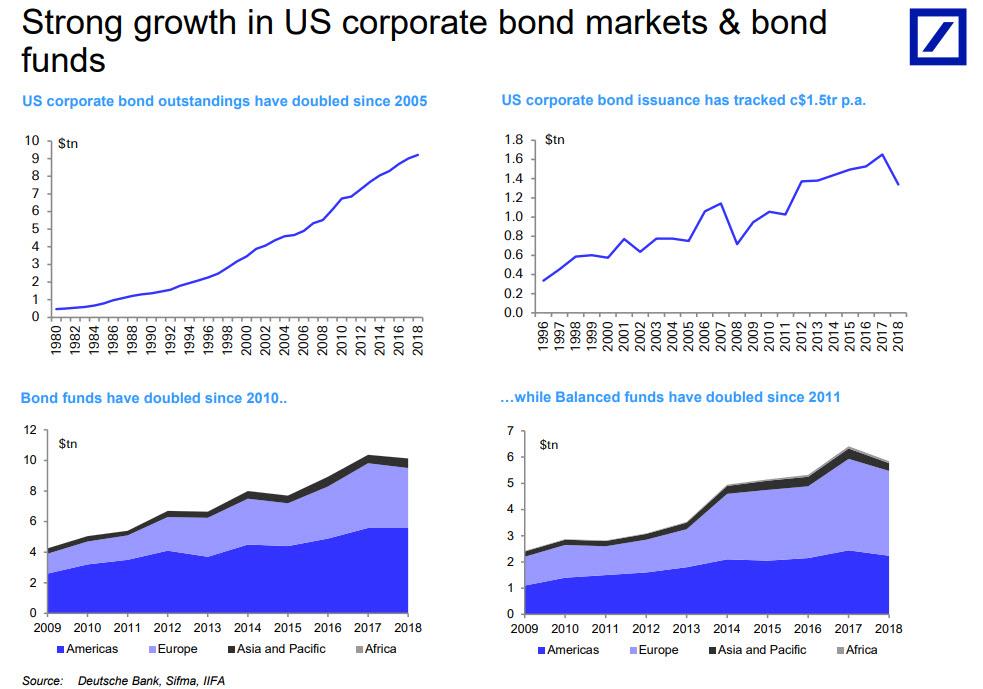

And speaking of the above funds, there is a reason why they are went from liquid to illiquid overnight: they have all geared into corporate bonds. As DB notes, US corporate bond outstandings have doubled since 2005 with recent issuance running at $1.5trn each year.

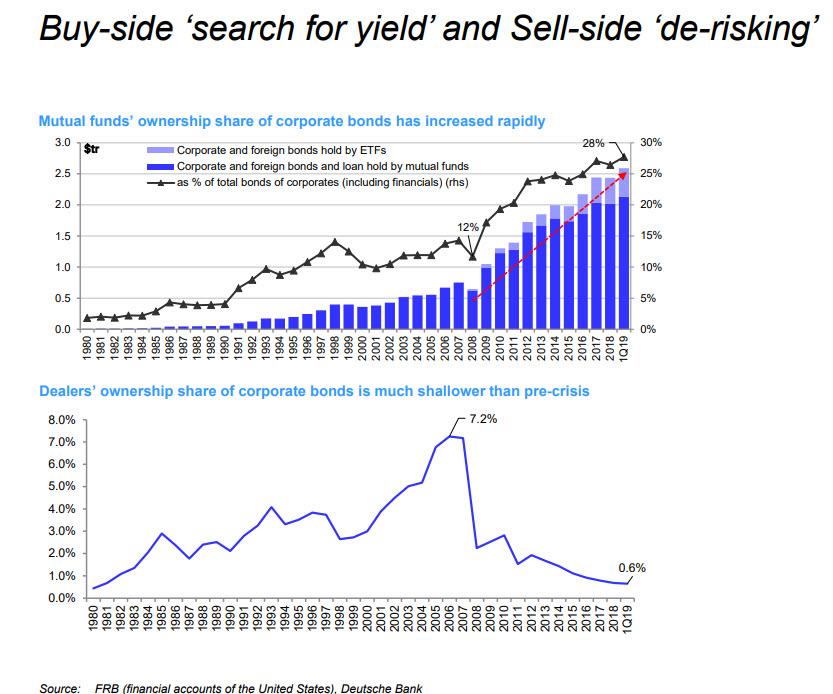

Over the same period, mutual funds’ ownership of corporate bonds has increased from 12% to almost 30%, or $2.6 trillion…

… with the balance is largely held by insurance and pension funds 45%.

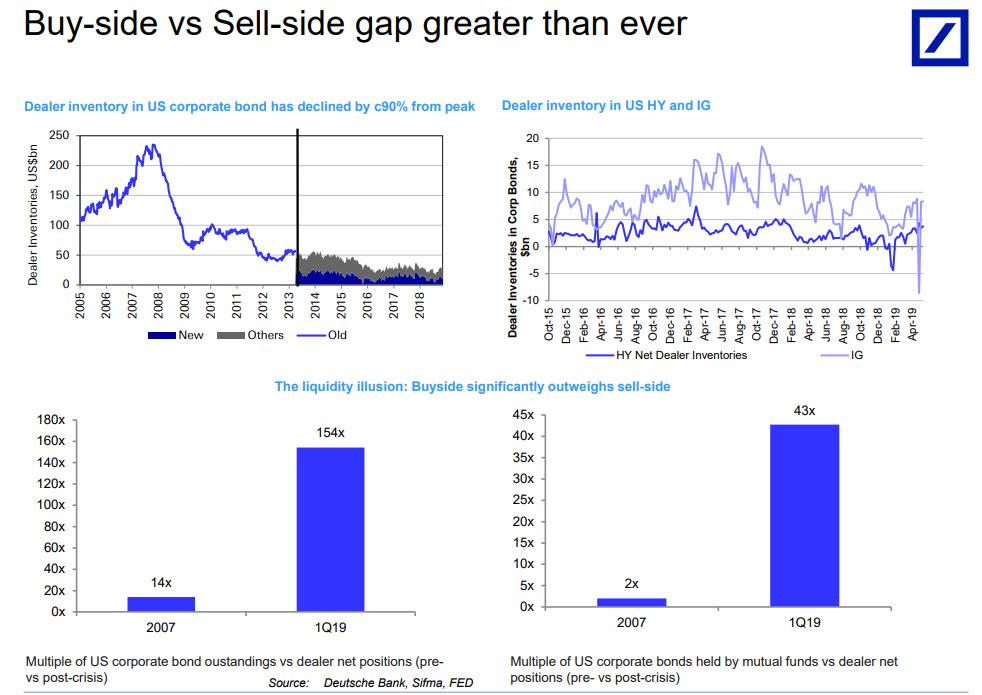

But the biggest reason why liquidity has become an illusion (or rather mass delusion), is that while the dealer inventory of corporate bonds has declined by 90%…

… the ratio of corporate bonds held by mutual funds vs dealer inventory has increased from 2x in 2007 to 43x currently.

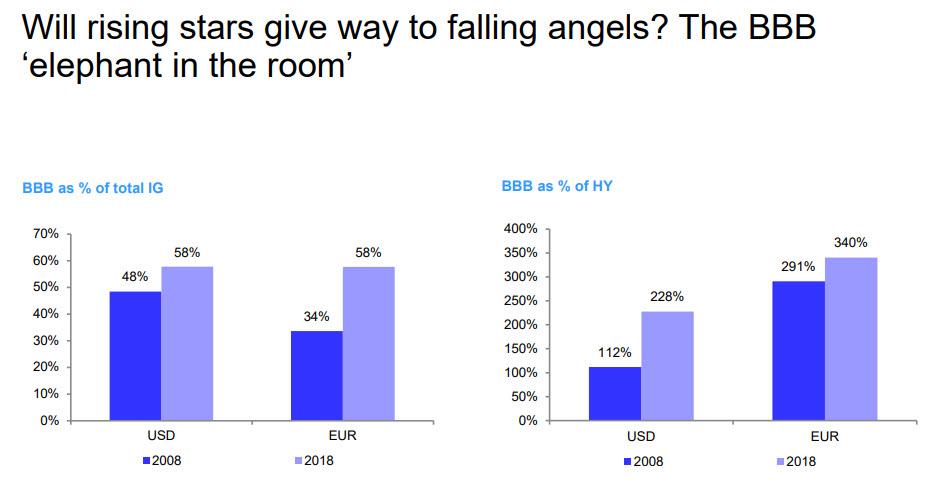

In short, as DB highlights, the buy-side significantly outweighs the sell-side and the gap has never been bigger. Worse, this comes at a time when BBB represents 60% of the Investment Grade and 250-300% of the High Yield market.

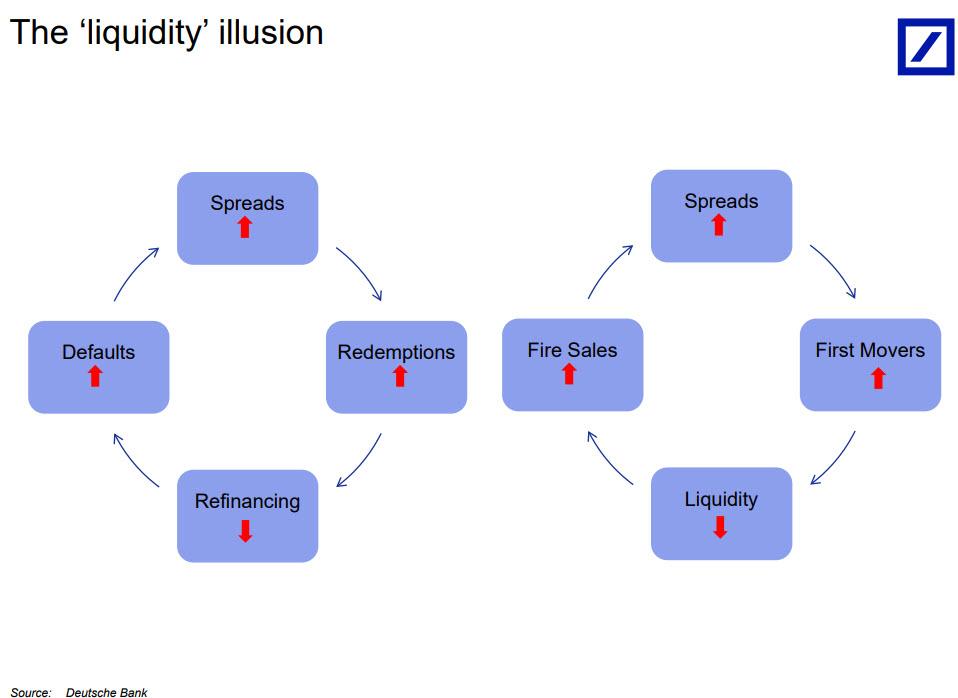

Incidentally, for those wondering if liquidity remains an illusion – a test that can only be confirmed when there is a crash and the market is indefinitely halted, an outcome that is now virtually inevitable – Deutsche has a simple test: it all has to do with the sequence of events unleashed by widening spreads, where redemptions and first movers rush to sell, collapsing the market’s liquidity, freezing refinancings, and resulting in a surge in defaults and firesales, which in turn leads to even wider spreads and so on, until central banks have to step in to short circuit this toxic loop.

This also explains why GAM, Woodford, H20 and many more funds (in the near future), will be similarly gated once their investors discover there is no liquidity to sell into and the only “real time” liquidity is offered to those who have a “first seller mover advantage”, to wit:

- If investors anticipate severe losses on the fund’s investments, they could be incentivised to “run for the exit” to be the first to redeem their shares.

- The first-mover advantage in open-ended funds arises because losses on asset sales to meet redemptions are incurred by investors which remain in the fund.

- As in a ‘bank run’, the asset manager is, in principle, forced to sell assets in a fire sale in order to meet its short-dated liabilities

As an aside, while the above is 100% correct,we find it ironic that it comes from none other than Deutsche Bank, a financial institution which due to a similar considerations among its clients, has itself become the target of a mini “bank run” one targeting the bank’s prime brokerage assets, and which as we explained last week, is reportedly draining roughly $1 billion per day from the German lender.

In any case, this dramatic imbalance of asset holdings at market making banks and buyside “bagholders” of illiquid securities, is now posing a major problem for regulators, something the Bank of England acknowledged in a working paper published earlier this month, and highlighted by Mark Gilber, to wit: “as the funds industry has supplanted banks as a source of credit in the past decade, households and companies have benefited from a useful alternative source of financing. But, the report warned, we don’t know how this market-based system will respond under stress.”

Modelling such a scenario “can generate an adverse feedback loop in which lower asset prices cause solvency/liquidity constraints to bind, pushing asset prices lower still,” the BOE found. In other words, the new market structure may be worse than the old.

The feedback loop discussed by the BOE is the one we showed above. Here it is again:

And, as recent notable fund “gates” and/or collapses have shown, the difficulty for asset managers in such an eventuality is finding sufficient cash to repay exiting investors while preserving the structure of the portfolio without distorting market prices, according to Amundi’s Blanque.

According to Bloomberg, part of Amundi’s response to this seemingly intractable issue is to include liquidity buffers in its portfolios, which may mean holding securities such as German bunds and U.S. Treasuries, which should always trade freely. But the industry needs to come up with a common definition so that liquidity is included along with risk and return when assessing a portfolio’s robustness, Blanque says. Additionally, this band aid only works for modest redemptions. A wholesale liquidation would crush even the most “buffered” up fund.

For now, asset managers have to cope with what Blanque called “the sacred cow” – although a better phrase would be “constant risk” of allowing clients to withdraw funds on a daily basis.

“It is a bomb, given the risks of liquidity mismatch,” he warns. “We don’t know if what is sellable today will be sellable in six months’ time.”

That’s not the only we don’t know. As Blanque concluded, “we don’t know the channels of transmission, we don’t know how the actors will act. It is uncharted territory.”

And that, precisely, is why central banks can never again allow risk asset prices to drop: the alternative means gating not one, or two, or a hundred funds, but halting the entire market, because once everyone start selling and price discovery finally returns to a market that has been dominated by central banks for the past decade, several generations of traders and investors who have grown up without price discovery will be shocked to discover just where “fair” market prices reside.

via ZeroHedge News https://ift.tt/2SDcjn2 Tyler Durden