In case readers have been burried under a pile of negative yielding debt for the past 6 months, today is the long-awaited Fed decision day, where markets are fully pricing in what is expected to be the first rate cut since December 2008.

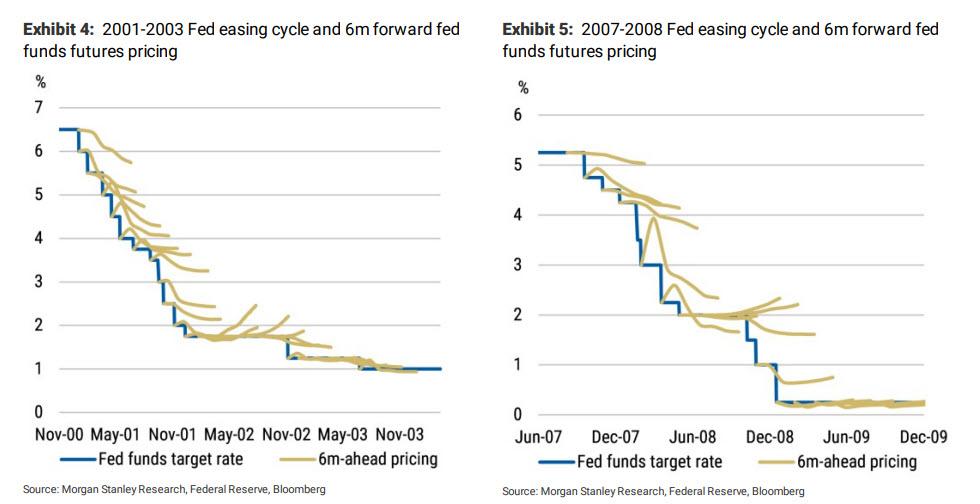

But, as Deutsche Bank’s Jim Reid notes, exactly what happens today is far from a foregone conclusion, as the question still on investors’ minds is by how much the Fed will cut, and whether there’ll be any messages about the future path of rates going forward. The market currently fully prices a 25bp cut and implies an 16% chance of a larger 50bp cut. And as we discussed last night, although the Fed have given no real encouragement to the notion of a 50bps cut it’s worth noting that the last time the Fed began a series of rate cuts, in September 2007, their opening move was a 50bp cut (with a recession following three months later), and a similar 50bp cut happened when the Fed began cutting in January 2001 (a recession followed in March).

Of course, rates were higher back then though so the Fed had much more space before hitting the infamous zero lower bound. The last time the Fed started an easing cycle with a 25bps “insurance” cut was in September 1998, when they ultimately cut rates 3 times and successfully prolonged the expansion… until the dot com bubble and recession in 2001.

So in their preview of what the FOMC will do, Deutsche Bank economists predict a 25bp cut, but they say that “the key question is how Chair Powell and the Committee frame the narrative for further easing through year end.” With this in mind, investors will be paying close attention to Chair Powell’s press conference. DB’s economists write that they “do not expect the Committee to pre-commit to another cut in September”, but instead the amount of further easing is going to be data dependent. “Will a market hungry for stimulus accept this”, asks Jim Reid, who then notes that:

Indeed we’re at a fascinating juncture in markets.

Reid goes on to summarize the zeitgeist: “It feels like the global macro risks are building for late summer/autumn (hard Brexit, US/China trade uncertainty, US/EU trade issues to come before year-end and global manufacturing effectively in recession) but all of us are reluctant to fight the central banks. Is this a trap? Indeed even our traditionally bullish Binky Chadha has some reservations about the risk/reward from this starting point.”

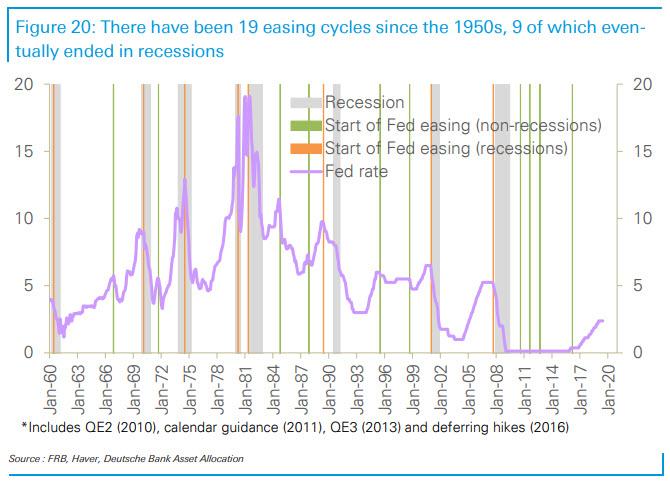

Referring to a note we highlighted on Monday, Reid notes that as Chadha pointed out, there have been 19 Fed easing cycles since the 1950s and this one fits almost exactly inline timing wise with the average slowdown in ISMs and LEIs through history. However, where it differs markedly is that only once (in 1995) has a rate cut occurred when the S&P 500 was around record highs. On average, the market has peaked 4 months before the cutting cycle started and was down a median -12% in between the two points.

Also, he pointed out that 9 of the 19 rate cutting cycles failed to avert a recession.

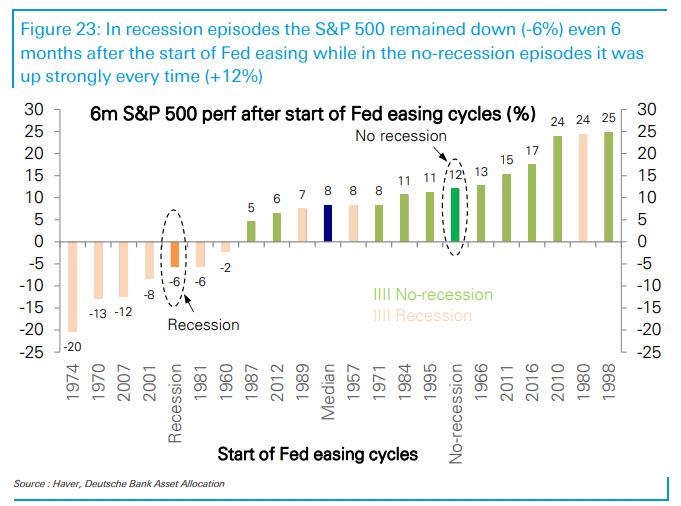

The recessions typically saw a -27% peak to trough drawdown in the S&P (mostly after the first cut) and on average bottomed 5 months after the Fed started cutting. Of the 10 that didn’t end in recessions, growth rebounded quickly – on average after 2-3 months – and although the S&P still fell around -7%, within 6 months of the first cut they had gained 12% from the lows and sat comfortably above pre-cut levels.

So history would suggest quite a binary outcome from here and based on this alone one would have to say that the risk/reward doesn’t look particularly compelling especially as we’re at record highs.

So, as Reid concludes, “while don’t fight the Fed is a famous refrain but nearly 50% of the time they’ve been powerless to stop negative economic and market momentum in a growth slowdown.”

via ZeroHedge News https://ift.tt/2LR6Msf Tyler Durden