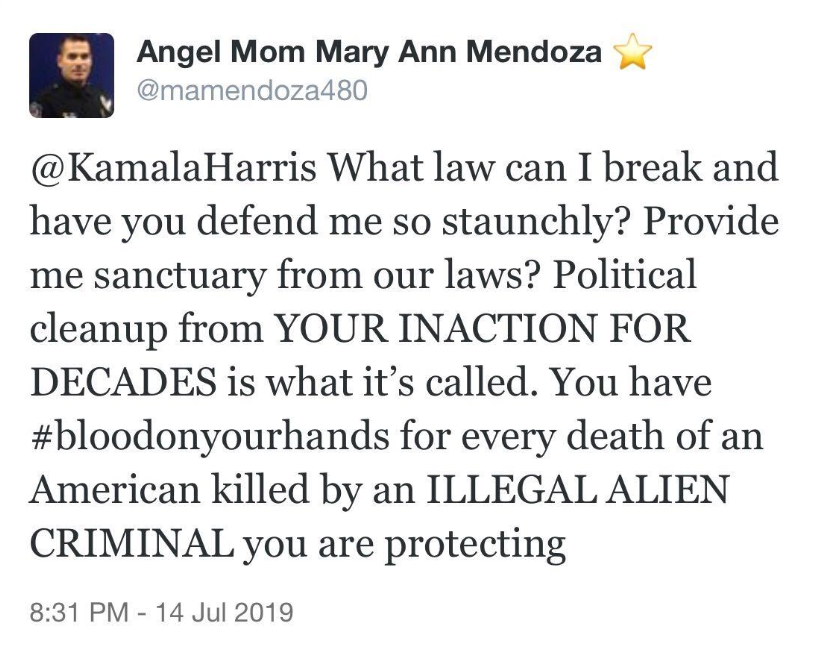

Twitter briefly suspended the twitter account of “Angel Mom” Mary Ann Mendoza” over a tweet she sent attacking presidential candidate Kamala Harris, then reinstated it after President Trump tweeted that he would “help” with the situation.

On Saturday, Twitter suspended Mendoza’s account after she sent the following tweet:

The company said Mendoza had violated its policy on hate speech by using the term “illegal” to describe “undocumented” migrants, and said it wouldn’t reinstate Mendoza’s account until she agreed to delete several tweets with this hateful language. She refused.

Mendoza’s son, 32-year-old police officer Brandon Mendoza, was killed in May 2014 by a drunk illegal immigrant who was driving drunk down the wrong lane on the high way.

Several conservative media outlets reported on the story, though it was largely ignored by the mainstream press, and early on Sunday morning, President Trump tweeted that he would intercede on Mendoza’s behalf and insisted that she “should never be silenced.”

I will help Angel Mom (and great woman) Mary Ann Mendoza with Twitter. I know Mary Ann from the beginning, and she should never be silenced. She is a winner who has lost so much, her child. Twitter, if you’re watching, please do what you have to do, NOW! @foxandfriends

Trump first met Mendoza during a campaign stop in Arizona during 2016. She was later invited to the White House.

Mendoza delivered a lengthy statement to Brietbart News.

“I’m disgusted and disappointed that Twitter is trying to silence me,” Mendoza told Breitbart News. “I had my world ripped out from under me the day my son was killed by a repeat illegal alien criminal. I am the ‘other’ side of this crisis and the end result of open borders and the careless release of illegal aliens at our borders because of time restraints.”

[…]

“I will not be silenced in my warning calls of what could happen to any American citizen in the blink of an eye as it did to me,” Mendoza said. “As an American citizen whose beautiful son was collateral damage to the ineptness if our elected officials, I will continue to bring my words to them in whatever platform I can. They owe it to me and every other Angel Family to have a hearing for our voices. Their fellow American citizens and our loved ones killed by their inactions. My voice is my son’s voice, never to be silenced by anyone.”

As of noon ET on Sunday, Mendoza’s twitter account was active, but the offending tweets had been deleted.

via ZeroHedge News https://ift.tt/30HIT9O Tyler Durden

Markets are engaged in a clear battle for control:An active Fed eager to extend the business cycle using asset price inflation as its primary means to generate further debt financed growth on the one hand and deteriorating fundamentals and technicals gnawing at an artificial market construct on the other.

Let’s call a spade a spade: Markets would not be anywhere near new highs were it not for a Fed flip flopping and racing from dovish media event to dovish media event. I’ve been very vocal in my criticisms of their efforts and sense they are playing a dangerous gamehere. Hence I don’t want to belabor the point here today. But as a follow up: Friday’s desperate efforts on the side of the Fed to backtrack market expectations for a 50bp rate cut at the coming July meeting, which they themselves caused on Thursday with multiple Fed speakers, has revealed again the Fed’s singular role it has to devolved into: The market’s primary price discovery mechanism. As markets dropped below $SPX 3,000 this week dovish Fed speakers caused a renewed rally above 3,000 and as soon as they tried to walk it back with a conspicuous WSJ Journal article on Friday markets again soon rolled over.

That’s the circus atmosphere they have created and appear to be supportive of. The Fed is very aware of its role in all of this and it’s shameful. Like Alan Greenspan or not, but at least he was a cryptic speaker that left markets guessing and played his cards close to the vest. But over the years the Fed has devolved itself into this clown show we have now, a day to day manager of markets. And markets have learned to react to every single pronouncement and utterance.

Just stop:

Free advice to the @federalreserve:

Stop talking.

Just stop.

Seriously, just stop. It’s embarrassing and it’s not your charter to manage markets. Nobody elected you to do that. Well, then nobody elected you in the first place. You’re appointed. By politicians. And now we have politicians that overtly want to dictate policy to the Fed. A toxic mix as the Fed’s independence is risking utter bankruptcy and is already lost in the eyes of many.

But as with cheap money, once you go down that road of daily massaging markets it’s hard to extract yourself from that mess. Now markets expect daily soothing and when they don’t get it they react, as did futures Friday following close when Rosengren uttered slightly less dovish words. “I think we should wait”.

Yes, this is what our markets have devolved into. A giant Fed gaming operation and it’s safe to say that the entire month price action will be greatly influenced by what the Fed does on July 31, the last day of the month.

But by setting expectations they have cornered themselves into a position where they constantly need to feed the appetite of the beast they themselves have created: A Fed dependent market that needs and wants more stimulus.

And now here we are, at some of the highest valuations:

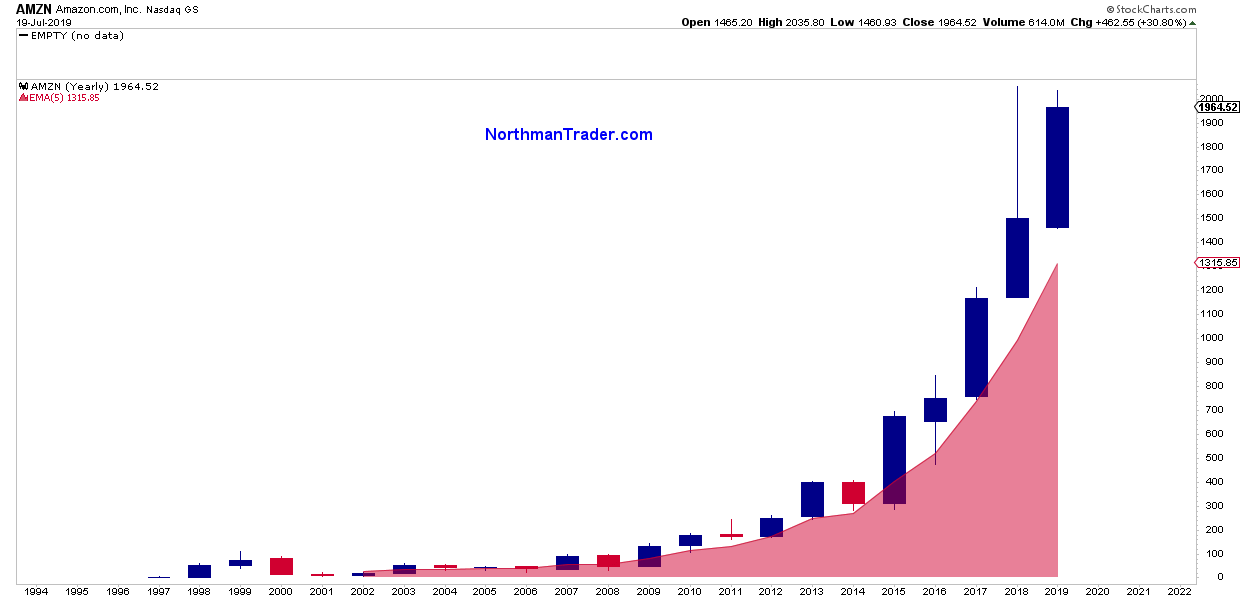

With come key stocks massively technically extended (see also: To the stars):

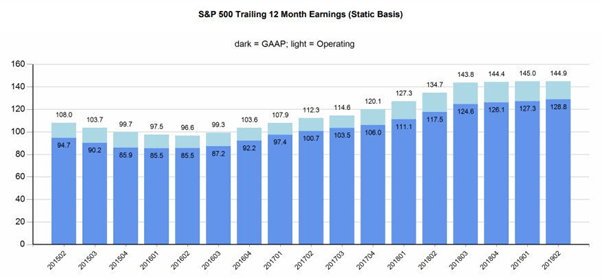

Yet earnings growth having ground to a halt:

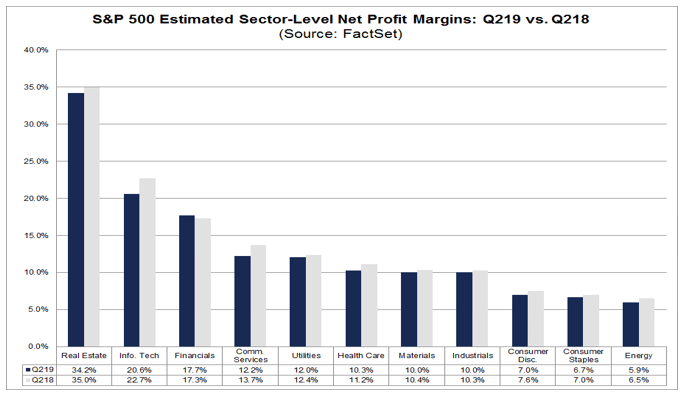

While profit margins have started shrinking:

Not the recipe for multiple expansion. But nevertheless here we are near all time highs once again, thanks to the Fed’s, so far, successful efforts.

But this is where the technicals come in and they put a at least temporary red line in the bull sand.

I am probably one of the few out there that has outlined the potential for a larger sell case on equities at this stage. The vast majority of analysts are looking for a massive expansion in prices primarily due to the Fed. From what I’ve seen earnings growth is really no longer part of the calculus. Easy money is. Fine. It may happen, I can’t deny that possibility and I’ve outlined in my weekly briefs when the sell case would be void.

And let’s be clear: Putting out technical setups in public is not an easy task. Especially on the sell side. Technical setups are about risk/reward and they are not guaranteed, they can be invalidated and if they don’t work out one gets hammered with ridicule and hate. And I’ve been wrong before. But I’ve also been right plenty of time.

Last year it was Lying Highs, a sell call which culminated in a 20% sell-off. But the call came out in September and markets didn’t top until early October. Sells are processes, bottoms are events. Like the one in December. I talked about Imbalance on December 23rd and called for a major technical rally into MA reconnects, worked nicely. Did I expect new highs on deteriorating fundamentals? No, but then this is where the Fed comes in, jawboning things higher. Yet again Lying Highs II informed us of another sell set-up coming and indeed we saw a larger sell-off into May before the Fed once again came to the rescue at the beginning of June.

No, sell calls are much harder than buy calls. After all you have an entire market machine designed to levitate asset prices higher and most people are bullish all the time, so a sell call is what the majority doesn’t want to hear. Indeed you can even make a great technical sell call, be right and still get hate, as I saw with Boeing when I called for a sell at $441. It dropped 6% in the week after the call, but then the plane crash happened and I got accused of taking joy in people dying. What nonsense, but still there it is. The stock was massively technically extended and the fundamentals took over (for the worst reason) and the stock plummeted 25% from the sell call. But it wasn’t the crash that was the problem, it was the underpinning design flaws that were the trigger and the technicals said that the long side was dangerous. And it was.

In some cases technicals are cleaner, like Gold when we called for a big rally when Gold was trading at 1270 in May, it hit 1450 on Friday a 14% rally from that bullish call.

I’m pointing all these things out to highlight how complex sell calls are, yet technicals matter and they mattered again big time this week.

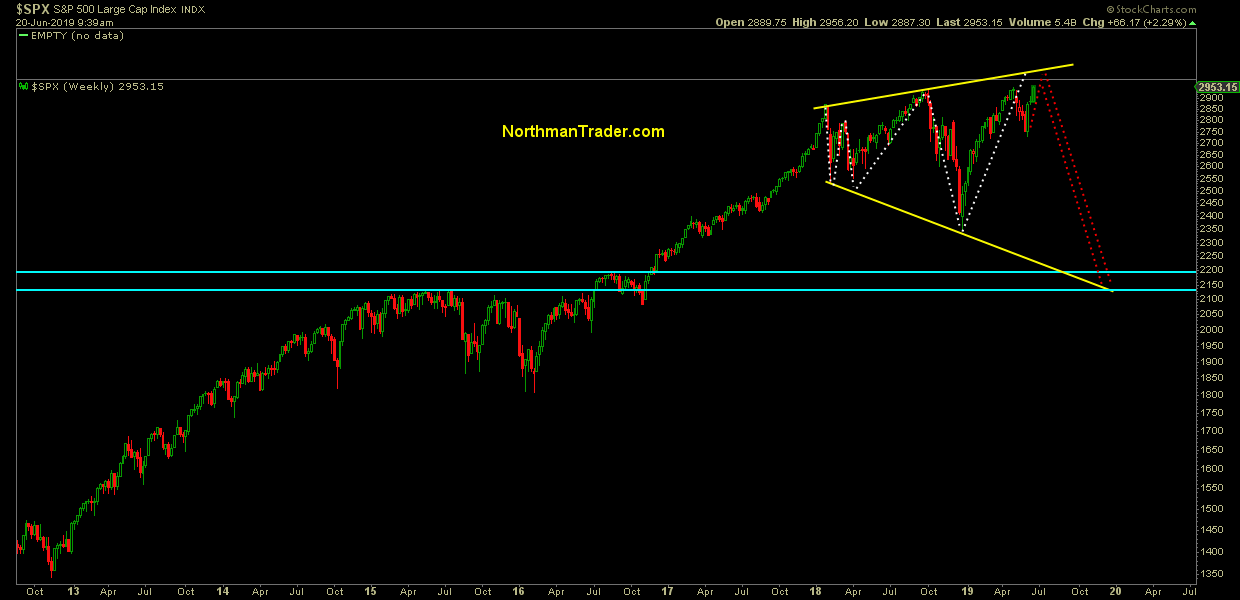

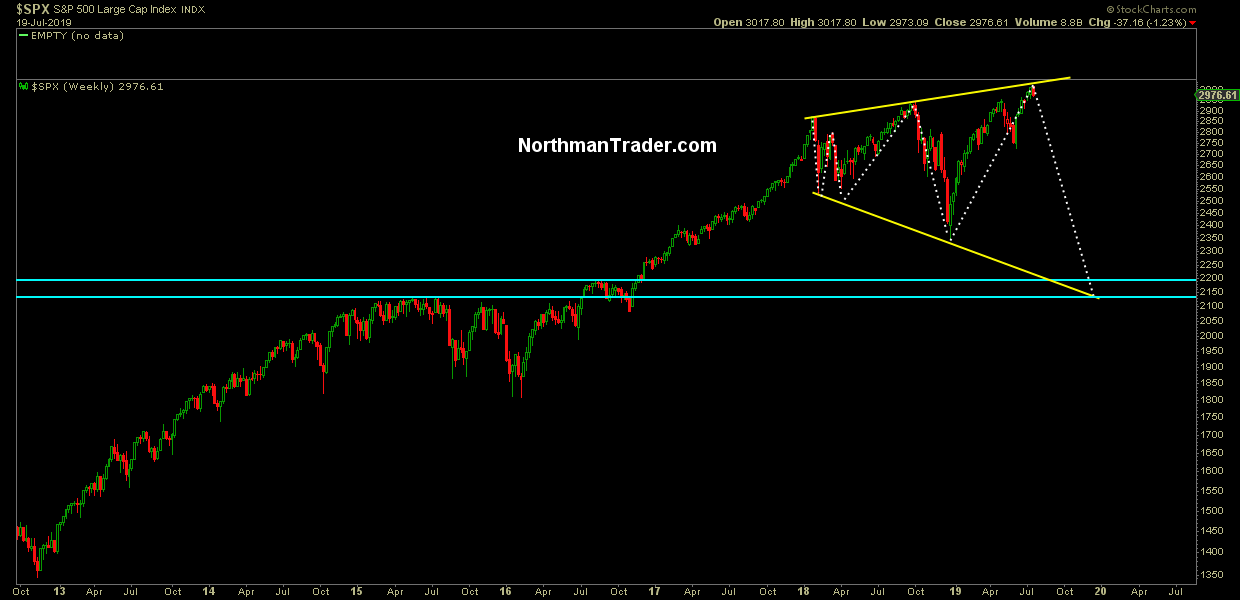

Since June and into early July I presented a potential major sell case on $SPX. In June (It’s different this time, Sell Zone, Distortion) and again last week in The ChoiceI’ve pointed to the chart below allowing for the possibility of an upper trend line tag on a megaphone pattern that could lead to a major sell-off. This is the chart shown in June:

Indeed we saw this tag on Monday this last week which then reversed:

In fact I pointed to it first thing on Monday morning:

This does not mean the larger sell case is validated yet, it’s not, but the 2990-3050 sell zone case I had outlined in my writings and on CNBC has so far produced a result.

But as it is a battle for control between the Fed and a still needed technical confirmation the jury is still out.

For a run down of the technicals please see the video below:

* * *

To get notified of future videos feel free to subscribe to our YouTube Channel. For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2XYmJ6z Tyler Durden

A 41-year-old man arrested on suspicion of Japan’s worst mass killing in nearly 20 years told police that the Kyoto Animation studio had plagiarized his work, according to CNN.

Police identified the man as Shinji Aoba during a Friday press conference, however Kyoto Fushimi Police spokesperson Ryoji Nishiyama said that they had not yet established a link with the studio in Kyoto’s Fushimi-ku district.

34 people were killed after the suspect began pouring gasoline on the first floor of the studio before setting it on fire, shouting “You die” as he spilled the liquid, according to a witness.

The three-story building quickly became engulfed in flames, killing 20 men, 20 women and another individual of ‘unknown gender.’ 35 people were injured in the blaze.

After dousing flames, firefighters entered the building and found 20 bodies lying on the staircase leading to the roof exit. Another team found 11 bodies on the second floor of the building and two on the ground floor.

Police said that 74 people were inside the building at the time of the blaze.

The fire spread so rapidly that many inside did not have time to escape, Kyoto Prefectural police told CNN. Several people jumped out of the second and third floor windows and suffered bone fractures. –CNN

Aoba was arrested and is currently heavily sedated as physicians treat him for severe burns sustained during the attack. Police added that he has unspecified mental health issues.

As CNN notes, the arson marks Japan’s deadlies mass murder since a 2001 arson attack on a building in Tokyo’s Kabukicho district which killed 44 people.

via ZeroHedge News https://ift.tt/2JZkqGv Tyler Durden

Last week, we laid out the bull and bear case for the market:

The Bull Case For 3300

Momentum

Stock Buybacks

Fed Rate Cuts

Stoppage of QT

Trade Deal

The Bear Case Against 3300

Earnings Deterioration

Recession

No Trade Deal/Higher Tariffs

Credit-Related Event (Junk Bonds)

Mean Reversion

Volatility / Loss Of Confidence

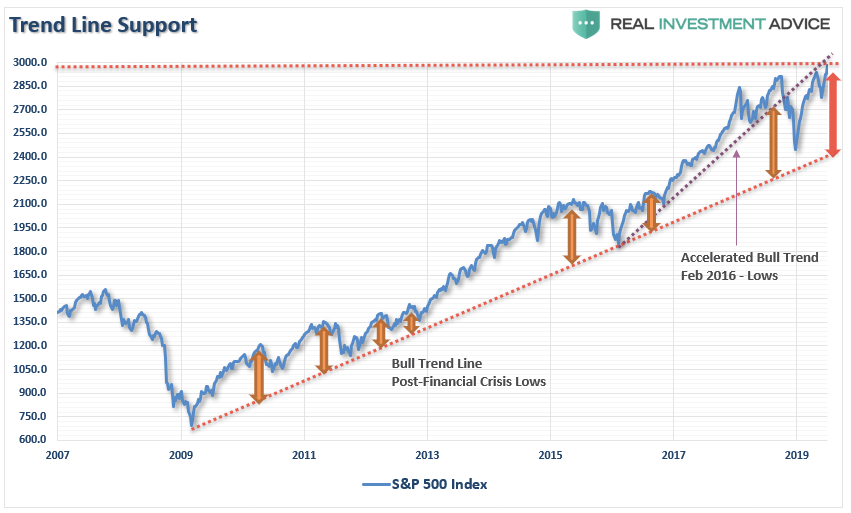

We laid out the case for a near-term mean reversion because of the massive extension above the long-term mean. To wit:

“There is also just the simple issue that markets are very extended above their long-term trends, as shown in the chart below. A geopolitical event, a shift in expectations, or an acceleration in economic weakness in the U.S. could spark a mean-reverting event which would be quite the norm of what we have seen in recent years.”

This analysis led us to take action for our RIAPRO subscribers last week (30-Day Free Trial), as we added a 2x-short S&P 500 index fund to Equity Long-Short Account to hedge our longs against a potential mean reversion.(on Friday that portfolio was UP .03% while the market FELL by 0.62%)

“This morning, we are adding a small 2x S&P 500 short position to the trading portfolio to hedge our core long positions against a retracement over the next few weeks. We will remove the short if the market can regain its footing and move higher, or the market sells off and reaches oversold conditions.”

This is the purpose of hedging, as it reduces volatility over time, which inherently reduces the risk of emotionally based trading mistakes.

The correction this past week was not surprising as we wrote previously:

“With a majority of short-term technical indicators extremely overbought, look for a correction next week. What will be important is that any correction does not fall below the early May highs.”

While the market is still hanging above the May highs, further corrective actions are likely next week as the short-term oversold conditions have not been resolved as of yet. The deviation above the long-term mean is also only starting to reverse as well.

Importantly, once we get past the end of the month, and assuming the Fed does indeed cut rates and no “trade deal” with China, the markets will return their focus to economics and earnings. As we stated previously:

“Such continues to suggest the August/September time frame for a larger corrective cycle is still in play.”

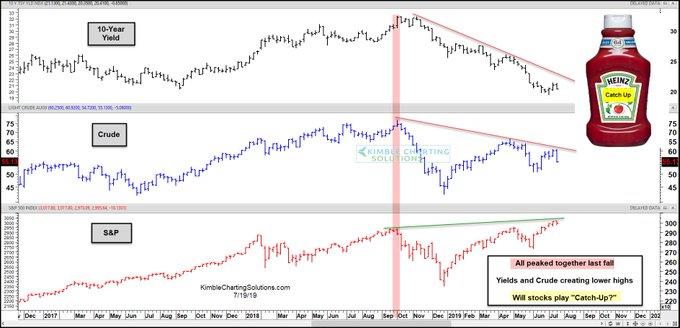

More importantly, as Chris Kimble noted on Friday, the market is continuing to ignore the economic warnings being sent by bonds and commodities.

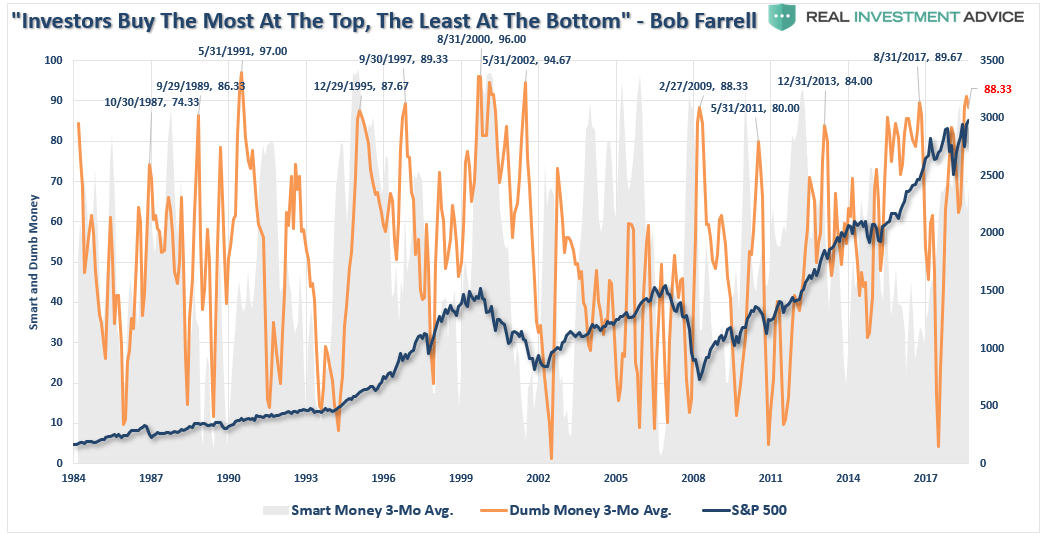

Moreover, the “Dumb Money” is now all the way back in.

These last two charts confirm the old Wall Street axiom:

“Individuals buy the most at the top, and the least at the bottom.”

This is why we are hedging our risk, carrying a higher level of cash, and holding onto our bonds as if they were the last lifeboat on the Titanic.

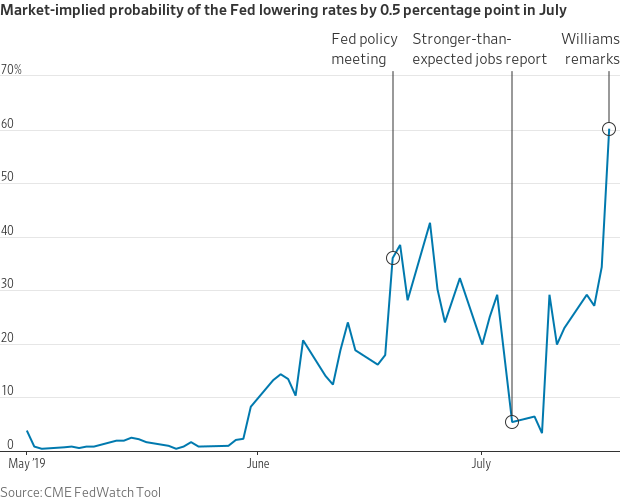

Why The Fed Will Cut By 50bps

It is now widely expected the Fed will cut rates at the end of the month following comments by Fed officials last week. Per the WSJ:

“New York Fed President John Williams on Thursday stoked expectations for a hefty cut. Already-low interest rates are a big reason to cut aggressively at the first sign of economic distress, he said. ‘Don’t keep your powder dry—that is, move more quickly to add monetary stimulus than you otherwise might.’ But a bank spokesman later walked that back, saying Mr. Williams didn’t intend to suggest the central bank might make a large cut this month.”

“However, in an unprecedented move, the NY Fed subsequently released a statement stating that President Williams’s speech on Thursday afternoon was not intended to send a signal that the Fed might make a large interest rate cut this month but rather it was “an academic speech on 20 years of research.”

Why did the NY Fed do this?

Simple: as BofA explains, ‘the FOMC was uncomfortable with the market moving toward a 50bp cut and wanted to push the market back to a 25bp baseline.’ In other words, as Meyer puts it, ‘Williams unintentionally misguided the markets.’”

With the markets pushing record highs, recent employment and regional manufacturing surveys showing improvement, and retail sales rebounding, it certainly suggests the Fed should remain patient on hiking rates for now at least until more data becomes available. Patience would also seem logical given very limited room to lower rates before returning to the “zero bound.”

However, there is also support for rate cuts. This is the point we will discuss today.

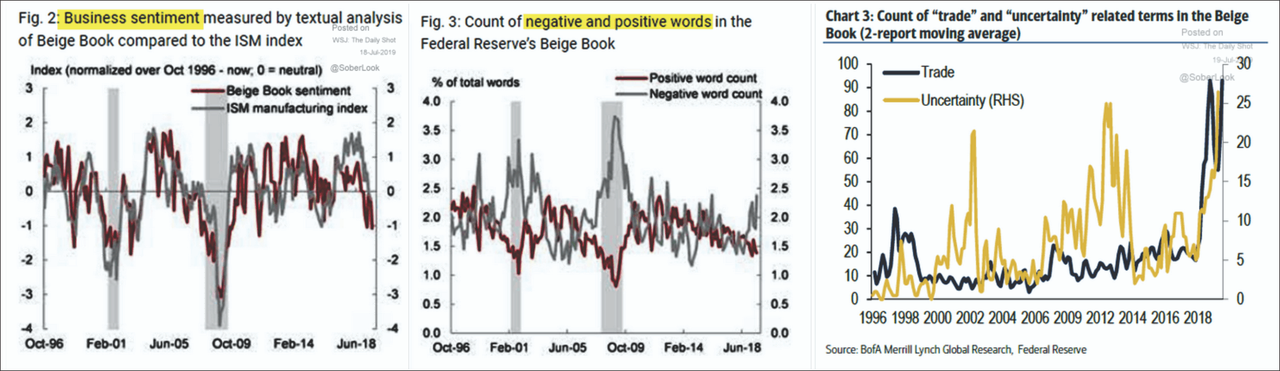

Labor markets remained tight, with contacts across the country experiencing difficulties filling open positions. The reports noted continued worker shortages across most sectors, especially in construction, information technology, and health care. (Tighter job market leads to higher costs, which impacts profitability.)

Compensation grew at a modest-to-moderate pace, although some contacts emphasized significant increases in entry-level wages. Most District reports also noted that employers expanded benefits packages in response to the tight labor market conditions. (Note: cost of labor is rising, which will impede corporate profit margins. Increases in labor costs ALWAYS precede the onset of a recession.)

Tariffs were mentioned 49 times in the report.

Districts generally saw some increases in input costs, stemming from higher tariffs and rising labor costs. However, firms’ ability to pass on cost increases to final prices was restrained by brisk competition. (Note: higher input costs without the ability to pass it on impacts profitability.)

Click to Enlarge

Recession Probabilities

The Fed’s own recession probabilities index has spiked to levels historically coincident with the onset of a recession. (Yes, this time could be different, but probably not a bet the Fed is willing to take.)

“Given the structural backdrops to the economy, there is an inability to increase rates of productivity substantially, output, wage growth, savings, or consumption, which would lead to stronger rates of economic growth. In fact, we are currently running some of the weakest rates of economic growth, productivity, and wages on record.”

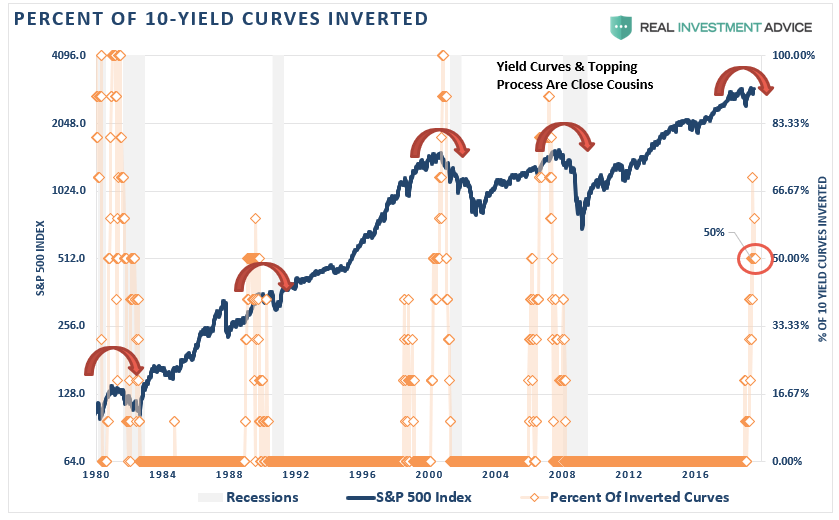

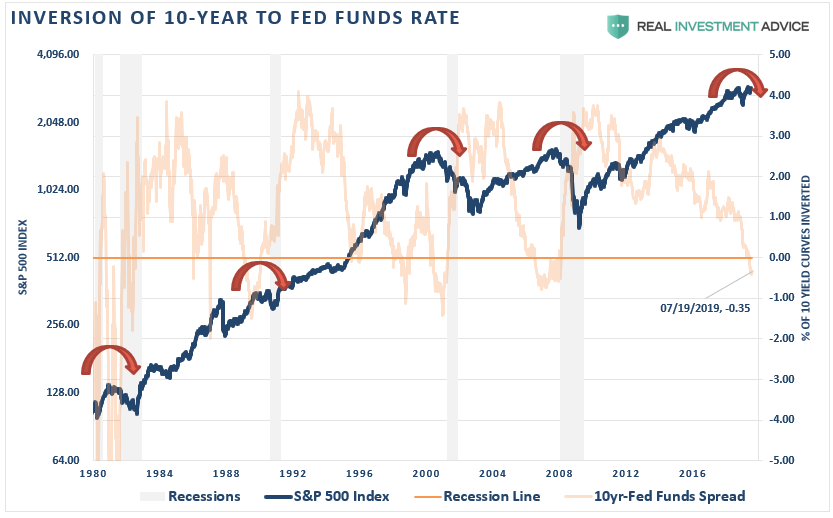

Currently, 50% of the 10-yield curves we track are inverted and have remained so for more than 3-months. Historically, when inversions last for one-quarter or more in duration, recessions have not been too far behind.

However, one of the biggest reasons the Fed is about to cut rates by up to one-half point is to un-invert the Fed Funds to the 10-year Treasury rate. The inversion between the ultra-short and long-end of the curve is impairing loan activity. The Fed clearly understands that if they don’t resolve this inversion, the probability of a recession grows rapidly.

Cass Freight Index

There is also substantial “hard data” evidence the economy in under severe pressure. While “sentiment-based” surveys, or “soft data,” has rebounded recently, data like the “Cass Freight Index” is ringing alarm bells.

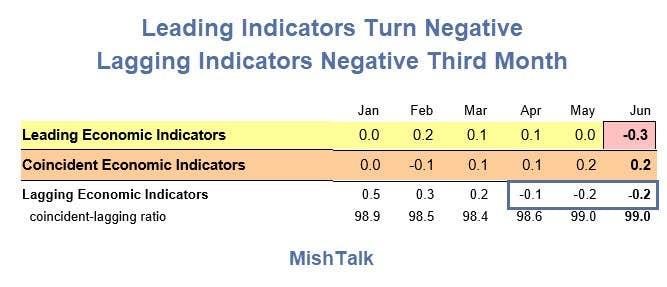

Leading Economic Indicators Drop

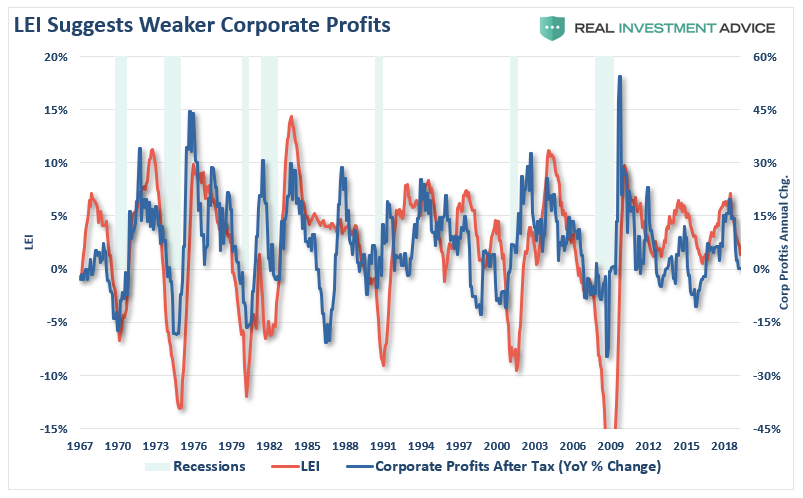

However, it is the Leading Economic Indicator (LEI) index, which has our attention currently.

“The Conference Board’s LEI index turned negative in June. The yield curve finally made a negative contribution. The conference board provides this press release on Leading Economic Indicators for June.

‘The US LEI fell in June, the first decline since last December, primarily driven by weaknesses in new orders for manufacturing, housing permits, and unemployment insurance claims. For the first time since late 2007, the yield spread made a small negative contribution.” – Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board

The consensus estimate was for LEI of +0.1, the read was a -0.3

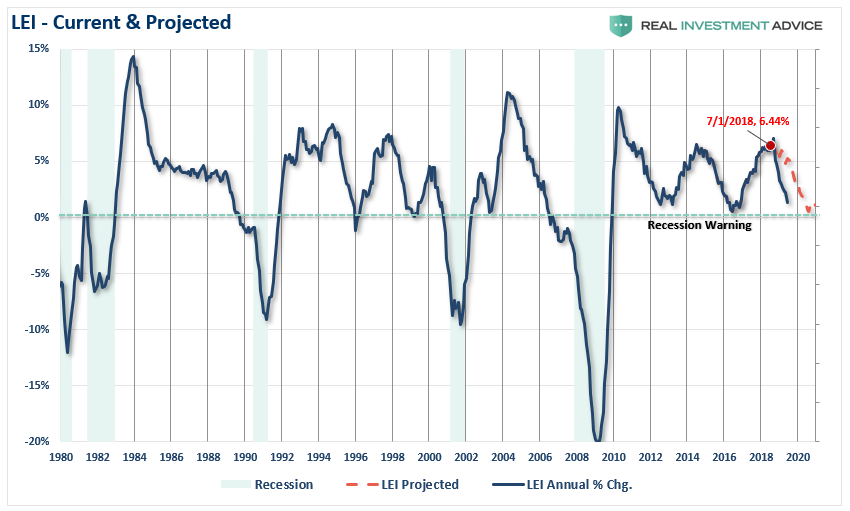

This decline is not surprising to us. In July of 2018, as noted in the chart below, we laid out a predicted path of reversion in the LEI index. As you can see, the reversion has been even sharper than we originally estimated.

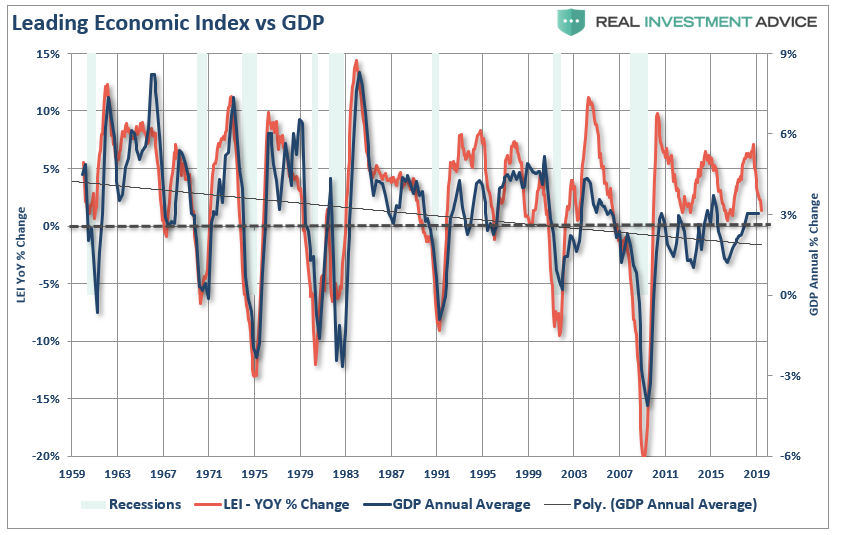

What is more concerning, and a reason the Fed is likely acting now, is there is a high correlation between the LEI and GDP, economic activity, and corporate profits. When compared to nominal GDP, the LEI index is suggesting a sharp slowdown is just ahead.

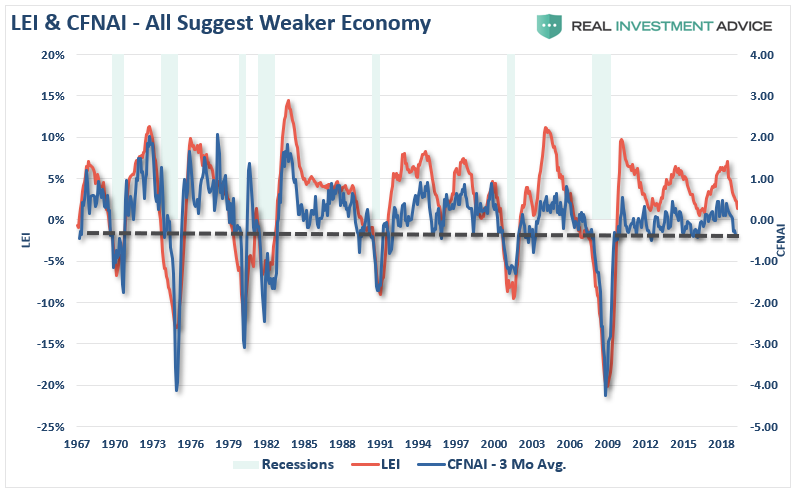

The Chicago Fed National Activity Index (CFNAI) is one of the broadest measures (80-sub components) of economic activity. The LEI and CFNAI, not surprisingly, also have a high correlation, which suggests further weakness is ahead.

Of course, if GDP, and underlying economic activity, is slowing down, it should not be surprising that corporate profits also decline.

The LEI is certainly not a perfect indicator for recessionary activity and has provided many false signals since the 2009 lows. However, the recessionary correlation is the highest when the LEI is signaling a recessionary warning at the same time the Fed Funds/10-Year yield inversion in place.

I think the Fed is beginning to panic as they were never able to get yields up to high enough levels to be effective in the next recession. Of course, this is exactly what we said would happen numerous times previously:

“The Fed surely understands that economic cycles do not last forever, and after eight years of a ‘pull forward expansion,’ it is highly likely we are closer to the next recession than not. While raising rates would likely accelerate a potential recession, and a significant market correction, from the Fed’s perspective, it might be the ‘lesser of two evils.’ Being caught at the ‘zero bound’ at the onset of a recession leaves few options for the Federal Reserve to stabilize an economic decline.”

Janet Yellen was smart enough to “exit” and stick Jerome Powell with the “tab.”

While the market rallied back from its 20% decline last year on “hopes” of an end to the “trade war” and “rate cuts,” the market is missing an important part of the picture.

“This used to be pretty simple. When the economy slowed, the Fed would cut rates. This encouraged borrowing and investment. People bought houses. Businesses expanded and hired people. The economy would recover.

Now, it doesn’t seem to work that way. Peter Boockvar succinctly explained why in one of his recent letters. The problem is that ‘easy money’ stops working when it becomes normal, as it now is.

Lower rates don’t encourage borrowing unless potential borrowers think it’s a limited-time opportunity. Which they don’t anymore, and shouldn’t, since the Fed shows no sign of ever going back to what was once normal.”

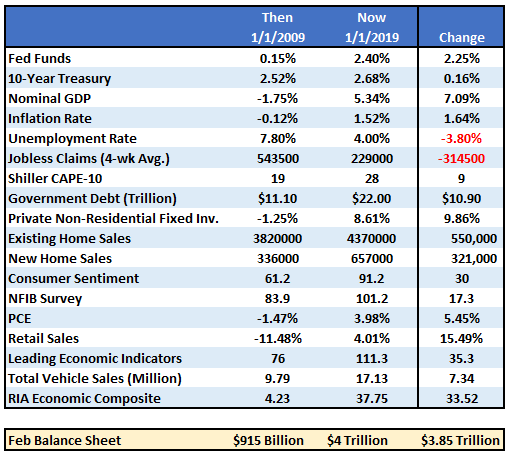

If the market fell into a recession tomorrow, the Fed would be starting with roughly a $4 Trillion balance sheet with interest rates 2% lower than they were in 2009. In other words, the ability of the Fed to ‘bailout’ the markets today, is much more limited than it was in 2008.

However, there is more to the story than just the Fed’s balance sheet and funds rate. The entire backdrop is completely reversed. The table below compares a variety of financial and economic factors from 2009 to the present.”

“The critical point here is that QE and rate reductions have the MOST effect when the economy, markets, and investors have been ‘blown out,’ deviations from the ‘norm’ are negatively extended, confidence is hugely negative.

In other words, there is nowhere to go but up.”

Let me be clear; it is certainly possible that asset prices could rise in the short-term given the “training”investors have received over the last decade to “Buy The F***ing Dip.” However, given the economic and fundamental backdrop, rate cuts will not change the onset, duration, or intensity of the coming recession.

Yes, participate with the “rate cut rally.”

We will be.

Just make sure you have a strategy to “leave the party before the cops arrive.”

via ZeroHedge News https://ift.tt/2Z7hL3O Notypist

About 12 investors made offers on a collection of rent stabilized Harlem apartment buildings that listed in April for $260 million, according to Bloomberg. But then, the NY legislature re-wrote the rules of stabilized rents, which capped property values and slashed the potential for increases in rent overnight.

The bids for the 28 building “Harlem Ensemble” apartments that were on the sale block instantly disappeared.

David Chase, partner at B6 Real Estate Advisors said: “They called us every day — and then we couldn’t reach them.”

The listing will expire at the end of the month.

Many other multifamily deals also collapsed due to investors fearing that the new legislation, which governs about 1 million apartments in the city, takes direct aim at landlords’ income and investment returns. It makes it nearly impossible to raise rents, remove units from state regulation or recoup the costs of capital improvements.

NYC apartment building sales fell 48% in the first half of 2019 from the year prior – the biggest decline for any 6 month period going back to 2009. In northern Manhattan, including Harlem, the drop led to a 61% fall in all commercial property transactions.

The total of all commercial deals citywide is on pace to fall below 2,000 for the first time since 2011.

Adrian Mercado, chief information officer at B6 said: “Right now, it’s a shot in the dark on the multifamily side. People are speculating as to what buildings should be trading at.”

via ZeroHedge News https://ift.tt/2JR3DFs Tyler Durden

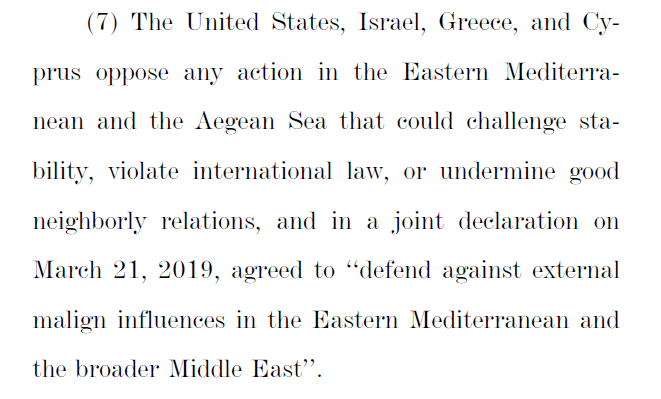

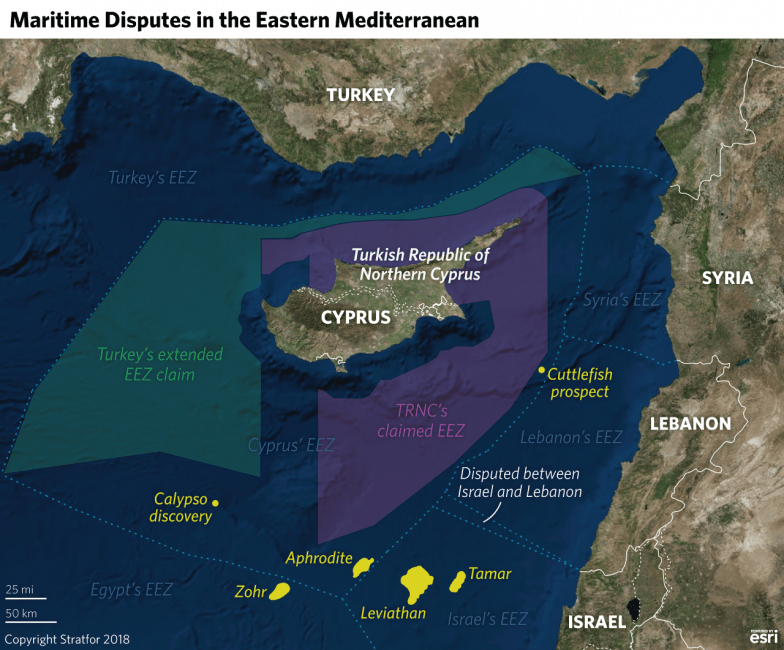

This week a group of US senators has proposed to leave Turkey in control of the northern part of Cyprus, and force the Greek Cypriots to choose between the US and Russia for the economic and political future of the south of the island.

The Senate Foreign Relations Committee agreed by a large bipartisan majority on June 25 to put into law a new Eastern Mediterranean strategy. If the bill is enacted, Cyprus will be required to decide that in exchange for American protection from Turkish military threats, including Russian-made S-400 missiles to be based in southwestern Turkey, the Cyprus Government must not allow Russian naval vessels to dock at Cypriot ports, and should block all Russian money and investments on the island. At the same time, Greece has been told the US military intends to expand its occupation of Crete around the Souda Bay base; at Larissa Air Force Base, midway between Athens and Thessaloniki; and at other Greek locations.

The proposed new law is the most comprehensive plan for American military occupation of Cyprus and Greece since the Greek civil war of the 1950s. The US plan also establishes State Department censorship of the Greek-language media in Cyprus and Greece, and threatens US sanctions against the Orthodox Church bishops of the two countries.

Senator Bob Menendez, Democrat of New Jersey, initiated the new policy as an amendment to Senate Bill No. 1102, “to promote security and energy partnerships in the Eastern Mediterranean, and for other purposes.” Menendez chaired the Foreign Relations Committee until the Republicans won control of the Senate last November. He has made a long record of legislating sanctions against Russia, while he himself has been under FBI investigation for corruption. Read the Menendez indictment here and the dismissal of the case a year ago, after a federal court jury could not agree on a verdict.

The text of S-1102, which now goes to the full Senate for a vote, can be read here. The new policy, as Menendez has agreed with the Republican majority of the Committee, can be read in full here.

In the preamble, Russia is identified as a “malign influence” in the Mediterranean:

US policy in the region should be aimed, the Bill declares, at backing the development of the Cyprus offshore gas deposits, as well as future regional pipelines and liquefaction plants, in order to compete against Russian gas supplies to southern Europe:

Without naming Turkey, which is currently threatening Cypriot gas exploration at sea with drilling vessels of its own, the Bill claims that Cypriot seabed exploration “must be safeguarded against threats posed by terrorist and extremist groups, including Hezbollah and any other actor in the region.”

The Bill promises to supply US weapons to Cyprus, ending the arms embargo introduced by Henry Kissinger after he backed the Turkish invasion of the island in mid-1974. But there is no parallel US promise in the Menendez bill to halt US arms from being deployed by the Turkish military command in northern Cyprus. Nor does the new US policy alter US acceptance of Turkey’s occupation of northern Cyprus.

There are two explicit pre-conditions for the supply of US arms to Cyprus; one is aimed at Russian investment in Cyprus – referred to in S-1102 as money-laundering — and the other at Russian Navy port calls in Cyprus.

The Senate is also promising US scholarships to “future leaders” of Cyprus, plus $1.5 million in US training for Cypriot military officers over the next three years.

With a requirement for a report by the State Department on “Russian Federation malign influence in the Republic of Cyprus, Greece, and Israel”, the Senate bill launches an attack on the Cypriot and Greek media and the Orthodox Church in both countries. The Greek-language media are to be targeted if the State Department report judges them to “promote pro-Kremlin views”.

Ranking churchmen in Cyprus and Greece are threatened with investigation and sanctions to deter them from siding with the Russian Orthodox Church against the breakaway Ukrainian church in the autocephaly controversy; for details of that, click to read.

During the Obama Administration, the US strategy for combating Russia’s relationships with Cyprus was to create a NATO base in the occupied Turkish zone, and to pressure the Cyprus President Nikos Anastasiades into accepting the Turkish partition as a NATO protectorate of the island. This was the plan of then Assistant Secretary of State Victoria Nuland (right); for that plan and its outcome, read the archive.

Nuland’s ambassador to the Ukraine at the time, Geoffrey Pyatt, is now US Ambassador to Greece. “Pyatt’s scheming in Athens,” comments a veteran Greek political observer, “may turn out to be longer lasting than his scheming in Kiev. Whether his new success will be as destructive as the old one remains to be seen.”

GREEK AND CYPRIOT BRANCH OF THE ANTI-RUSSIA LOBBY IN WASHINGTON

Left: Endy Zemenides, Executive Director of the Hellenic American Leadership Council (HALC). Right: Tasos Zambas, Chairman of the Justice for Cyprus Committee for the Federation of Cypriot-American Associations.

The new Senate plan is to isolate Russia and Turkey simultaneously, pushing them closer together and pressuring the Cypriots and Greeks to position themselves against both.

The Greek-American lobby in Washington has declared its support for the Menendez bill to make “the region more stable and prosperous and… advance both American interests and values.” The Federation of Cyprus-American Associations has added:

“the East Med Act is a huge leap forward in U.S. relations with both Greece and Cyprus. It places Greece in the centre of a new American strategy for the Eastern Mediterranean, and it stops the treatment of Cyprus as merely a problem but positions it as a solution. The Greek-American community thanks Senator Menendez for his decades of unparalleled leadership on these issues and to Senator Rubio for championing this new Eastern Mediterranean strategy.”

via ZeroHedge News https://ift.tt/2GmC7Pf Tyler Durden

In an epic example of hackers using their abilities to cause mischief, somebody hacked into the Twitter, email and website of the Metropolitan Police Department, and started posting a series of bizarre messages, some with anti-police themes or homophobic slurs, according to a series of reports in the UK press.

Some of the tweets sent from the Metropolitan Police’s official twitter account, which has more than 1 million followers, also called for the release of West London rap artist Digga D, who is reportedly in prison.

A stream of suspicious emails were sent from the force’s press bureau at around 11:30 pm BST (about 6:30 pm in New York). Scotland Yard soon confirmed to the press that the emails were the result of “unauthorized access” to the company’s servers. They elaborated that the department uses a program called MyNewsDesk to manage its public releases, and implied that the hack had been centered around this system. Scotland Yard said they’ve begun to make changes to this system.

The tweets, most of which have been deleted, contained offensive language and mentioned the names of several people, including a missing child.

In one strange tweet that also contained homophobic slurs, the hackers appeared to take aim at other individuals. It read: “We are the police… Cal and dylan are gay btw.”

Other messages included offensive anti-police slurs including messages like “F**k the police.”

Conservative commentators quickly blasted London Mayor Saddiq Khan, saying he had lost control of the city’s streets, as well as its internal infrastructure. One of the tweets was even shared by President Trump, who is apparently still sore about his treatment during his recent visit to London.

With the incompetent Mayor of London, you will never have safe streets! https://t.co/pJqL1NjyvA

Could it be possible that we are on the verge of the next “Lehman Brothers moment”?

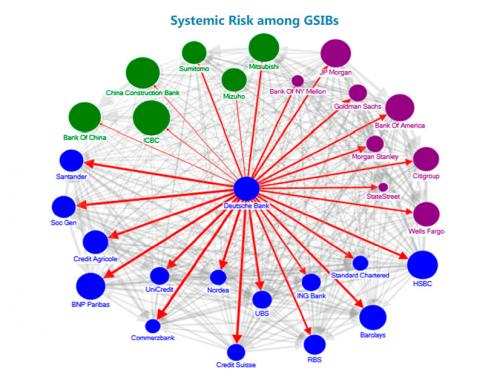

Deutsche Bank is the most important bank in all of Europe, it has 49 trillion dollars in exposure to derivatives, and most of the largest “too big to fail banks” in the United States have very deep financial connections to the bank. In other words, the global financial system simply cannot afford for Deutsche Bank to fail, and right now it is literally melting down right in front of our eyes. For years I have been warning that this day would come, and even though it has been hit by scandal after scandal, somehow Deutsche Bank was able to survive until now. But after what we have witnessed in recent days, many now believe that the end is near for Deutsche Bank. On July 7th, they really shook up investors all over the globe when they laid off 18,000 employees and announced that they would be completely exiting their global equities trading business…

It takes a lot to rattle Wall Street.

But Deutsche Bank managed to. The beleaguered German giant announced on July 7 that it is laying off 18,000 employees—roughly one-fifth of its global workforce—and pursuing a vast restructuring plan that most notably includes shutting down its global equities trading business.

Though Deutsche’s Bloody Sunday seemed to come out of the blue, it’s actually the culmination of a years-long—some would say decades-long—descent into unprofitability and scandal for the bank, which in the early 1990s set out to make itself into a universal banking powerhouse to rival the behemoths of Wall Street.

These moves may delay Deutsche Bank’s inexorable march into oblivion, but not by much.

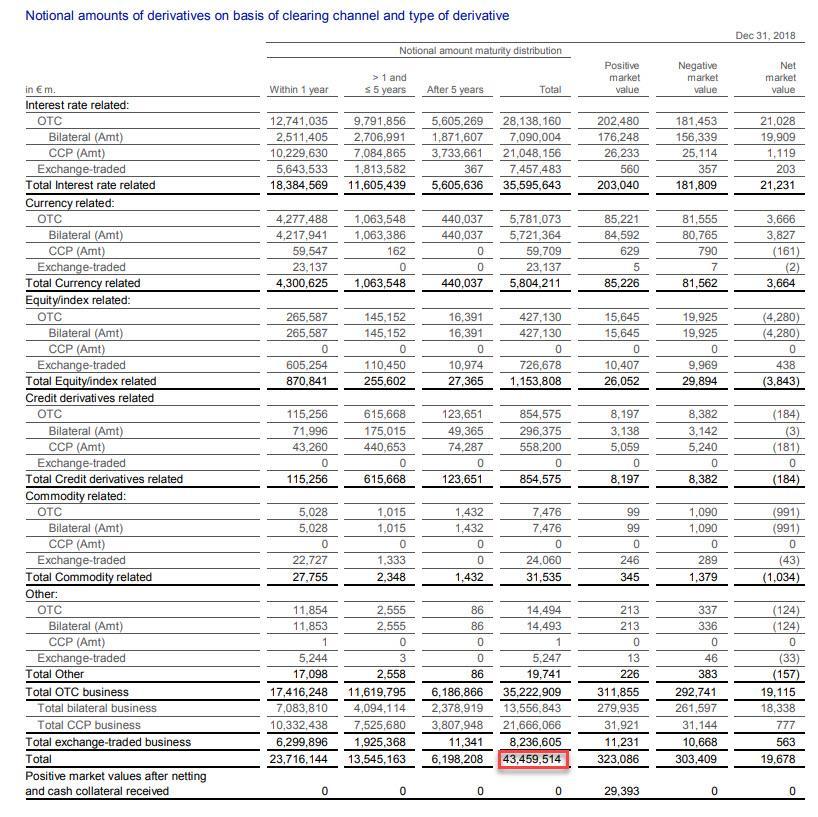

And as Deutsche Bank collapses, it could take a whole lot of others down with it at the same time. According to Wall Street On Parade, the bank had 49 trillion dollars in exposure to derivatives as of the end of last year…

During 2018, the serially troubled Deutsche Bank – which still has a vast derivatives footprint in the U.S. as counterparty to some of the largest banks on Wall Street – trimmed its exposure to derivatives from a notional €48.266 trillion to a notional €43.459 trillion (49 trillion U.S. dollars) according to its 2018 annual report. A derivatives book of $49 trillion notional puts Deutsche Bank in the same league as the bank holding companies of U.S. juggernauts JPMorgan Chase, Citigroup and Goldman Sachs, which logged in at $48 trillion, $47 trillion and $42 trillion, respectively, at the end of December 2018 according to the Office of the Comptroller of the Currency (OCC). (See Table 2 in the Appendix at this link.)

Yes, the actual credit risk to Deutsche Bank is much, much lower than the notional value of its derivatives contracts, but we are still talking about an obscene amount of exposure.

And this is especially true when we consider the state of Deutsche Bank’s balance sheet. According to Nasdaq.com, as of the end of last year the bank had total assets of 1.541 trillion dollars and total liabilities of 1.469 trillion dollars.

In other words, there wasn’t much equity there at the end of December, and things have deteriorated rapidly since that time. In fact, it is being reported that a billion dollars a day is being pulled out of the bank at this point.

I know that most Americans don’t really care if Deutsche Bank lives or dies, but as the New York Post has pointed out, the failure of Deutsche Bank could quickly become a major crisis for the entire global financial system…

But the important fact to remember is that Deutsche Bank traded these derivatives with other financial firms. So, is this going to be another Lehman Brothers situation whereby one bank’s problems becomes other banks’ problems?

Pay close attention to this.

If the situation gets out of hand, the Federal Reserve and other central banks will have no choice but to cut interest rates even if it’s not the best thing for the world economies.

In particular, some of the largest “too big to fail banks” in the United States are “heavily interconnected financially” to Deutsche Bank. The following comes from Wall Street On Parade…

We know that Deutsche Bank’s derivative tentacles extend into most of the major Wall Street banks. According to a 2016 reportfrom the International Monetary Fund (IMF), Deutsche Bank is heavily interconnected financially to JPMorgan Chase, Citigroup, Goldman Sachs, Morgan Stanley and Bank of America as well as other mega banks in Europe. The IMF concluded that Deutsche Bank posed a greater threat to global financial stability than any other bank as a result of these interconnections – and that was when its market capitalization was tens of billions of dollars larger than it is today.

Until these mega banks are broken up, until the Fed is replaced by a competent and serious regulator of bank holding companies, and until derivatives are restricted to those that trade on a transparent exchange, the next epic financial crash is just one counterparty blowup away.

As long as I have been doing this, I have been warning my readers to watch the global derivatives market. It played a starring role during the last financial crisis, and it will play a starring role in the next one too.

The fundamental structural problems that were exposed during 2008 and 2009 were never fixed. In fact, many would argue that the global financial system is even more vulnerable today than it was back during that time.

And now it appears that the next “Lehman Brothers moment” may be playing out right in front of our eyes.

Now more than ever, keep a close eye on Deutsche Bank, because it appears that they could be the first really big domino to fall.

via ZeroHedge News https://ift.tt/2YkEHze Tyler Durden

Turkey’s military is prepared to reinvade Cyprus “if needed for the lives and security of Turkish Cypriots,” Turkish President Recep Tayyip Erdogan said on Saturday.

“The entire world is watching our determination. No one should doubt that the heroic Turkish army, which sees [Northern] Cyprus as its homeland, will not hesitate to take the same step it took 45 years ago if needed for the lives and security of the Turkish Cypriots,” state-run Anadolu News Agency quoted Erdogan as saying.

Erdogan issued the statement as the nation marks the 45th anniversary of Turkey’s deeply controversial invasion of northern Cyprus in 1974, long condemned by the bulk of UN member countries.

But the provocative remarks come amidst what EU-member Cyprus has dubbed a “second invasion” involving illegal Turkish oil and gas drilling, accompanied by Turkish warships, F-16s, and drones to ensure “protection” of its drilling vessels.

The EU agreed on Monday to bring financial and political sanctions against Turkey after repeat warnings of the past weeks over Ankara deploying multiple offshore drilling vessels into international recognized Cypriot waters.

“Today, we will adopt a number of measures against Turkey — less money, fewer loans through the European Investment Bank, freeze of aviation agreement talks. Naturally, other sanctions are possible.”

The most serious measure will involve a cut of 145.8 million euros ($164 million) in European funds allocated to Turkey for 2020, according to a prior AFP report.

Erdogan appeared to directly address the crisis in his Saturday statement:

“Those who think the wealth of the island and the region only belongs to them will face the determination of Turkey and Turkish Cypriots.”

…Indicating an unwillingness to back down on Turkey’s oil and gas exploration claims inside Greek Cyprus’ exclusive economic zone.

“Those who dream of changing the fact that Turkish Cypriots are an integral part of the Turkish nation will soon realize that it is in vain,” Erdogan added.

Turkey has laid claim to a waters extending a whopping 200 miles from its coast, brazenly asserting ownership over a swathe of the Mediterranean that even cuts into Greece’s exclusive economic zone. So far Ankara has responded to EU sanctions by reaffirming its rights to waters of all parts of Cyprus’ coast.

Should the Turkish military attempt to enforce its drilling claims and run up against Cypriot and Greek vessels, it could spark a deadly encounter which would force the EU and NATO to finally weigh in more forcefully.

And just on the heels of the Russian S-400 standoff with Washington, the next major Turkish showdown with the West looks to be fast heating up in the eastern Mediterranean.

via ZeroHedge News https://ift.tt/2O9KSCH Tyler Durden

From observing the behaviour of ‘leavers‘ and ‘remainers‘ since the EU referendum in 2016, I have seen first hand how partisanship works as an effective tool to cloud judgement. Once a position of bias becomes ingrained, it has proved next to impossible to see beyond it or for the individual concerned to be convinced of an alternative perspective.

The psychological operation of ‘fake news‘ is now entrenched within society, with both sides of the divide claiming one another to be peddlers of false truths. By my reckoning this is all the more reason why positioning yourself as neither one thing or the other is the only logical way in which facts can be objectively scrutinised.

The role of the Bank of England in the Brexit process is an example of how bias is serving to insulate central banks from impartial and informed criticism. On one side are those who depict governor Mark Carney as an ‘enemy‘ of Brexit, whilst on the other are people who consider Carney as a safe pair of hands amidst a whirlwind of political turmoil. Non-partisan analysis of communications and policy decisions emanating from the BOE is rarely given space to evolve.

For instance, last week the bank published its latest Financial Stability Report in conjunction with a press conference delivered by Mark Carney. Whilst much of his interaction with the press on Brexit was of a similar theme to previous events, one aspect in particular stood out.

Asked by Joel Hills of ITV News about the level of preparation in the event of a no deal Brexit, Carney affirmed that the financial system in which the BOE presides over was ‘ready for whatever form Brexit takes.’ Carney’s conviction stems from a series of bank stress tests that the BOE conducted in 2018 in an attempt to gauge how the financial system would stand up to a crisis greater than 2008. The results as published by the BOE showed that the UK’s banking system was fully prepared.

Indeed, Carney’s confidence was such that he went on to say how the system would continue serving both households and businesses, ‘even if a worst case disorderly Brexit occurred at the same time as a global slowdown triggered by a trade war.’

Where it started to get more interesting is when Carney made an unequivocal distinction between financial stability and that of market and economic stability. The area where the BOE possess overarching control – the financial system – is, according to the bank, prepared for any adverse scenario. But this preparation does not extended to currency or equity markets, nor economic fundamentals such as inflation which would likely become volatile should supply chains into and out of the UK be compromised.

To quote Carney exactly, ‘market stability will adjust potentially quite substantially if there is a no deal Brexit. Even with a smooth adjustment this would still be a major economic adjustment and major economic shock – in not just a short period of time but virtually instantaneously.’

The expectation from the BOE is for immediate volatility if and when a no deal exit is confirmed. Not from within the financial system itself, but within the surrounding economic environment. The areas which the bank purport not to have direct jurisdiction over. Those who keep abreast of Brexit led developments will know that the pound would be most susceptible to a dysfunctional exit from the EU.

According to Carney, the preparedness of the UK system, which encompasses the country’s trade infrastructure, had seen ‘some progress‘, but ultimately it was for ‘the government to speak directly to that‘ and not the Bank of England.

Gradually over the last three years, the BOE have been carefully positioning themselves so as not to be held culpable for the economic ramifications of a ‘disorderly‘ Brexit. One mechanism for achieving this has been to re-elevate the importance of their 2% mandate for inflation, when in the years post 2008 it had no direct relevance for how the bank conducted monetary policy.

What we learn from Carney is that a no deal eventuality is a more pressing concern for markets and the economy than it is for the financial sector. Is this true? To a point perhaps, but not entirely as the Financial Stability Report alludes to.

An area of concern that has gestated since the referendum result is with uncleared OTC (Over the Counter) derivative contracts. Derivatives are essentially a contract between two or more parties that derive their value from the performance of an underlying asset, such as a commodity, currency or interest rate. Banks use a high degree of leverage to attain these positions in the market. Derivatives can also be used to speculate (bet) on the future value of assets, without the need to own the asset outright.

When it comes to uncleared contracts between the UK and EU, the Financial Policy Committee specifies these as a medium risk should Britain depart with no withdrawal agreement. As for the scale of contracts affected, the report is forthright. Note that the term ‘lifecycle events‘ includes actions such as settlement, modification and termination of derivative contracts.

Certain ‘lifecycle’ events will not be able to be performed on cross-border derivative contracts after Brexit. This could affect £23 trillion of uncleared derivatives contracts between the EU and UK, of which £16 trillion matures after October 2019. This could compromise the ability of derivatives users to manage risks, and could therefore amplify any stress around the UK’s exit from the EU.

This concern is what Mark Carney refers to as a potential ‘spillover‘. In their communications the Bank of England have routinely called for EU regulators to implement measures to mitigate the risks of a no deal exit. This is something that The European Banking Federation and The European Banking Authority have also been encouraging.

As well as this, the report states that for derivatives, the government has ‘legislated to ensure that EU banks can continue to perform lifecycle events on contracts they have with UK businesses.’

A possible spillover, however, stems from how The European Commission ‘does not intend to reciprocate for UK-based banks’ contracts with EU businesses.’ In particular, ‘uncertainty remains about the scope of current or proposed legislation in jurisdictions which account for approximately half of the notional value of outstanding contracts.’

A safe assumption is that potential economic fallout from derivatives would impact on financial stability. On the home front the Bank of England’s position is that markets and the economy would suffer from a volatile form of Brexit, but the financial system would remain fully functional and be able to withstand unprecedented stress. The validity of this claim could only be tested if a no deal exit comes to pass.

The caveat here is spillovers originating outside of the UK, which three months before the intended exit date of October 31st remain unresolved. Because the global economic system is interconnected, a banking crisis in one part of the world has the capacity to infect the system as a whole. This was evident over a decade ago when Lehman Brothers was sacrificed.

Derivatives, along with other financial instruments, are an inherent weakness built into the system. But instead of automatically interpreting such weaknesses as a threat to central bank autonomy, it is feasible that they present an opportunity for further far-reaching ‘reforms‘ to the financial system.

To globalists, crises open the gateway for establishing broad consensus for major economic change. Because out of chaos invariably comes consolidation of resources.

The question is, how could substantial financial instability be of benefit to the Bank of England? After the initial phase of the 2008 crisis had played out, the Bank for International Settlements put into motion new regulatory standards called ‘Basel III‘. Conceived on the global stage, the new regulations were designed to be implemented by national jurisdictions over a gradual period of time. Many of the standards are now in place, but the full roll out is not due to be completed until around 2021.

One of the aims of the FPC, as expressed in the Financial Stability Report, is to ‘ensure that systemically important payment systems support financial stability.’ This resonated with me because as I have touched on in previous articles, the Bank of England is targeting the year 2025 for the wholesale reform of the RTGS payments system in the UK. A reformed RTGS would have the capability of connecting to distributed ledger technology (DLT). As explained elsewhere, blockchain is a form of DLT, and works in conjunction with cryprocurrencies such as Bitcoin.

Changes on this scale would represent a major overhaul of the UK’s financial system, and would conveniently coincide with the BIS 2025 initiative. This initiative, as outlined by the BIS, will ‘foster international collaboration on innovative financial technology within the central banking community‘.

Based on the documentation I have read from the BIS, the IMF and the BOE, the introduction of central bank digital currencies (CBDC’s) is very much part of the drive for ‘innovative financial technology.’

The prospect of central banks issuing their own form of digital currencies in the future is, according to BIS general manager Agustin Carstens, something that might come sooner than people realise:

Many central banks are working on it; we are working on it, supporting them. And it might be that it is sooner than we think that there is a market and we need to be able to provide central bank digital currencies.

Whereas attention is directed to the short term actions of central banks, longer term plans provide a clearer perspective on the direction that global institutions want to take the financial system in the medium to longer term. It appears that globalists are targeting the period between 2025 and 2030 as the time when digital currencies would start to be implemented, resulting in the eventual abolition of physical money.

The concerted attention placed on CBDC’s comes as sterling remains highly sensitive to the Brexit process. I continue to think it is probable that a no deal exit will trigger a currency crisis. And given that currency markets have no borders, the danger is that a global trade conflict stemming from Brexit and the trade policies of the Trump administration would jeopardise the fiat currency system. This is a topic I discussed earlier this year when looking at the possibility of sterling no longer being considered a reserve currency post Brexit.

A crisis of this magnitude could quite easily be used by central banks as a rationale for a new approach to how currencies are disseminated and controlled.

Back in the present, the conventional theory pushed throughout alternative media is that protectionism is something that central banks and international institutions like the BIS and the IMF fear. On examination, I am doubtful of this claim. The FPC’s report makes it clear that even in the event of a ‘protectionist-driven slowdown‘ running in parallel to a no deal Brexit, the financial system would ‘absorb, rather than amplify, the resulting economic shocks.’ It remains to be seen whether this rhetoric bares any semblance to reality.

My concern is that rather than fear the breakdown of what globalists call the ‘rules based global order‘, it is in actuality an essential variable for orchestrating reforms of the system.

via ZeroHedge News https://ift.tt/2JHTNXx Tyler Durden