The Real “Helicopter Money”: Since 2009, China Has Created $21 Trillion Of New Money, More Then Double Than The US

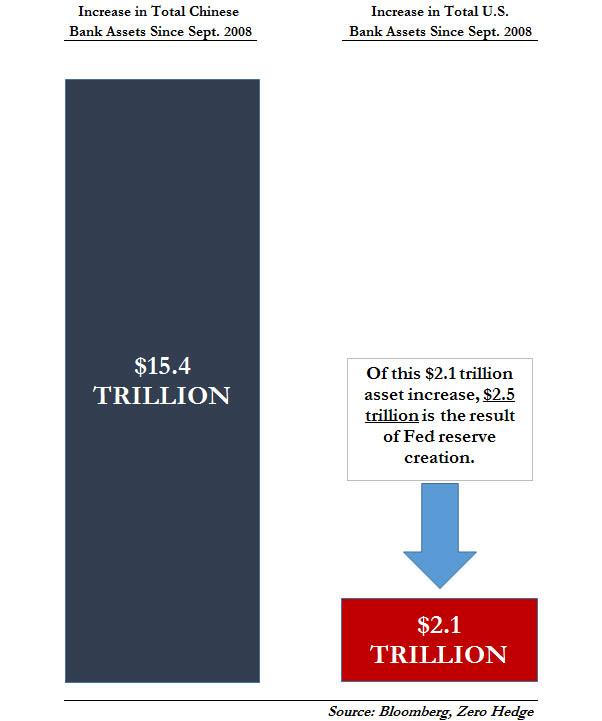

Back in the days of the Fed’s QE, much of thinking analyst world (the non-thinking segment would merely accept everything that the Fed did without question, after all their livelihood depended on it), was focused on how massive, and shocking, the Fed’s direct intervention in capital markets had become. And while that was certainly true, what we showed back in November 2013 in “Chart Of The Day: How China’s Stunning $15 Trillion In New Liquidity Blew Bernanke’s QE Out Of The Water” is that whereas the Fed had injected some $2.5 trillion in liquidity in the US banking system, China had blown the US central bank out of the water, with no less than $15 trillion in increases to Chinese bank assets, all at the behest of a juggernaut of new credit creation – be it new yuan loans, shadow debt, corporate bonds, or any other form of debt that makes up China’s broad Total Social Financing aggregate.

Now, almost six years later, others are starting to figure out what we meant, and in an Op-Ed in the FT, Arthur Budaghyan, chief EM strategist at BCA Research writes about this all important topic of China’s “helicopter” money – which far more than the Fed, ECB and BOJ – has kept the world from sliding into a depression, and yet is blowing the world’s biggest asset bubble.

Budaghyan picks up where we left off, and notes that over the past decade, Chinese banks have been on a credit and money creation binge, and have created RMB144Tn ($21Tn) of new money since 2009, more than twice the amount of money supply created in the US, the eurozone and Japan combined over the same period. In total, China’s money supply stands at Rmb192tn, equivalent to $28 TRILLION. Why does this matter? Because Chine money’s supply is the size of broad money supply in the US and the eurozone put together, yet China’s nominal GDP is only two-thirds that of the US.

This, as the BCA analyst explains, is a major problem.

Below we repost his latest FT Op-Ed, which explains why – as we said in the 2019 year ahead post – we remain confident that the spark for the next global financial crisis will be in China.

* * *

China’s ‘helicopter money’ is blowing up a bubble, authored by Arthur Budaghyan is chief emerging market strategist at BCA Research, and first published in the FT.

The escalation of the trade conflict between the US and China has raised the likelihood of greater stimulus by Beijing to prop up the economy. While China’s excessive debt isn’t news, investors must wake up to the reality of “helicopter money” — enormous money creation by Chinese banks “out of thin air”.

While this sugar rush may provide short and medium-term cover for investors, the long-term effects will exacerbate China’s credit bubble. China, like any nation, faces constraints on frequent and large stimulus, and its vast and still rapidly expanding money supply will produce growing devaluation pressures on the renminbi.

When a bubble emerges we are often told that this bubble is different. Many economists justify China’s credit and money bubble and continuing stimulus by pointing to the nation’s high savings rate. But this narrative is false. At its root is the idea that banks are channelling or intermediating deposits into loans. This is not how banks operate.

When a bank expands its balance sheet, it simultaneously creates an asset (say, a loan) and a liability (a deposit, or money supply). No one needs to save for this loan and money to be originated. The bank does not transfer someone else’s deposits to the borrower; it creates a new deposit when it lends.

In all economies, neither the amount of deposits nor the money supply hinge on national or household savings. When households and companies save, they do not alter the money supply.

Banks also create deposits/money out of thin air when they buy securities from non-banks. As banks in China buy more than 80 per cent of government bonds, fiscal stimulus also leads to substantial money creation. In short, when banks engage in too much credit origination — as they have done in China — they generate a money bubble.

Over the past 10 years, Chinese banks have been on a credit and money creation binge. They have created Rmb144tn ($21tn) of new money since 2009, more than twice the amount of money supply created in the US, the eurozone and Japan combined over the same period. In total, China’s money supply stands at Rmb192tn, equivalent to $28tn. It equals the size of broad money supply in the US and the eurozone put together, yet China’s nominal GDP is only two-thirds that of the US.

In a market-based economy constraints are in place, such as the scrutiny of bank shareholders and regulators, which prevent this sort of excess. In a socialist system, such constraints do not exist. Apparently, the Chinese banking system still operates in the latter.

There are clear downsides. Helicopter money discourages innovation and breeds capital misallocation, which reduces productivity growth. Slowing productivity and strong money growth ultimately lead to rising inflation — the dynamics inherent to socialist systems.

Air show in Tianjin, China shows off China’s helicopters. Getty Images.

In the long run, more stimulus in China will entail more money creation and will heighten devaluation pressures on the renminbi. As we all know, when the supply of something surges, its price typically drops. In this case, the drop will take the form of currency devaluation.

As it stands, China’s money bubble is like a sword of Damocles over the nation’s exchange rate. Chinese households and businesses have become reluctant to hold this ballooning amount of local currency. Continuous helicopter money will increase their desire to diversify their renminbi deposits into foreign currencies and assets. Yet, there is no sufficient supply of foreign currency to accommodate this conversion. China’s current account surplus has almost vanished.

As to the central bank’s foreign exchange reserves, at $3tn they are less than a ninth of the amount of renminbi deposits and cash in circulation. It is inconceivable that China can open its capital account in the foreseeable future.

If China chooses the path of unrelenting stimulus, investors should recognise the long-term negative outlook for the renminbi. Continuous stimulus will beef up investment returns in local currency terms, but currency depreciation will substantially erode returns in US dollars or euros in the long run.

The investment implications go beyond Chinese markets. Market volatility over the past few months as the talk of stimulus picked up has given us a peek into the future. As the renminbi has depreciated by 12 per cent since early 2018, the pain has reverberated across Asian and other emerging markets. The MSCI Asia and MSCI EM equities indices have each fallen 24 per cent in dollar terms since their peak in January 2018. Long-term pressures could play out even more dramatically.

Fortunately, Chinese authorities recognise these issues. Yet they face an immense task of stabilising growth while containing credit and money expansion. This will be hard to achieve in an economy that has become addicted to credit creation.

via ZeroHedge News https://ift.tt/32figtC Tyler Durden

{kind=link}