Key Events This Week: Plenty Of “Boom” Moments

As Deutsche Bank’s Jim Reid puts it, “If last week was back to school with a bang with Brexit and a bond market sell-off the highlights, this coming week has plenty more potential ‘boom’ moments.” The main highlight will be the ECB’s rate cut/QE restart on Thursday but today’s trip to Dublin from UK PM Johnson and the subsequent election vote later in Parliament (highly likely to be defeated) will be a “riveting” watch, especially with UK parliament set to be suspended later today; in data terms the highlights are US CPI (Thursday) and Friday’s US retail sales and UoM consumer confidence which last month fell to the lowest since October 2016.

With regards to what the ECB is expected to do, Reid reminds us that this will be President Draghi’s penultimate press conference before his term comes to an end. Deutsche economists expect the ECB to cut interest rates by 10bps at Thursday’s policy meeting, and they also anticipate a new system of reserve tiering, where some subset of reserves are exempted from the cost of negative interest rates, plus an enhanced version of forward guidance. While a shift to a symmetric inflation target or to a price level target would almost certainly be too radical for them to consider without a deeper policy review, they are likely to commit to some form of “lower for longer” rate guidance. There are also risks that they cut by more than 10bps, given the apparent lack of pushback by hawkish members of the Governing Council against a rate cut. There was more public pushback over the last few weeks against asset purchases, so that may be harder to agree on. DB’s economists nevertheless think a €30 billion per month purchase program is possible, though they could also see a more generous form of TLTROs if the ECB wants to focus on credit easing instead of measures that may flatten the curve.

Turning to Brexit, events are expected to continue to journey into the unknown this week. A vote in the House of Commons to hold an election will likely get defeated on Monday, with the opposition parties trying to force Johnson into asking the EU for an extension. The weekend papers were full of talk about the government working out whether they could sidestep the law with the Sunday Times reporting that the PM wants to even use the Supreme Court as an option. There was also talk of a PM resignation as one option being considered and even talk of the PM actively disobeying the law and perhaps facing a potential prison sentence if he does. As for the polls, after a torrid time in Westminster for the PM last week and over the weekend with another cabinet and party resignation, the Conservation Party have generally maintained their lead (between 3 and 14pts lead over 6 polls) but one poll suggested that if Brexit didn’t happen by October 31st then the lead would reverse and Labour would take a 2 point lead. This highlights why the opposition are gambling on denying an election this side of that date. The polls also show that hard tactics in Westminster are not necessarily damaging the governments support. However, the collateral damage to the party is significant so it’s high stakes for everyone.

Below is a daily breakdown of key global events, courtesy of Goldman Sachs:

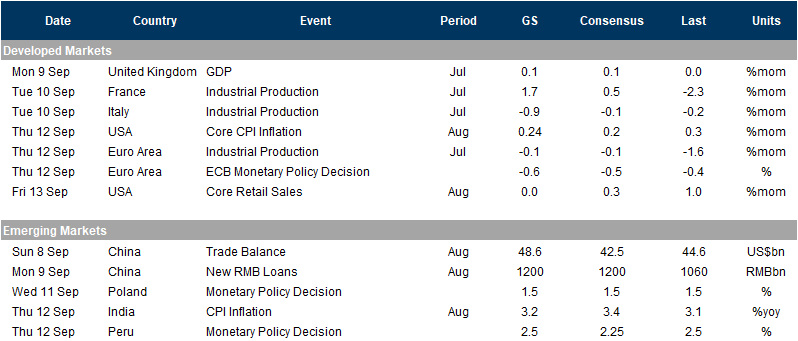

- Monday: United Kingdom, GDP (Jul). GS +0.1%, consensus +0.1%, last 0.0%, all %mom. We expect GDP growth of +0.1%mom in July, a touch above growth in June. We see this marginal pickup as largely driven by services. Construction may contribute positively sequentially, while manufacturing is expected to decline, given recent PMI reports.

- Tuesday: France, Industrial Production (Jul). GS +1.7%, consensus +0.5%, last -2.3%, all %mom. After a sharp decline of French industrial production in June, we expect a rebound in July in line with recent survey data pointing to an increase in sales and orders against decrease in inventories on the month; Italy, Industrial Production (Jul). GS -0.9%, consensus -0.1%, last -0.2%, all %mom. We expect Italian industrial production to contract further in July, given a sharp contraction in German industrial production and Italy’s trade links with Germany, notably in transport equipment. We expect the fall in Italian IP to reflect lower export orders in the auto industry, as noted by PMI reports last month.

- Thursday: USA, CPI Inflation (Aug). GS Core CPI Inflation +0.24%, consensus +0.2%, last +0.3%, all %mom-sa. We estimate a 0.24% increase in August core CPI (mom sa), which would boost the year-on-year rate by two tenths to 2.4% on a rounded basis. Our monthly core inflation forecast reflects a modest further boost from the tariffs implemented in May and June, which we expect to manifest in the household furnishings, auto parts, and personal care categories. We also expect a large rise in the apparel category related to methodological changes earlier this year. On the negative side, we expect a pullback in airfares reflecting lower oil prices, and we expect a further deceleration in monthly used car inflation, which we nonetheless expect to remain positive. We estimate a 0.11% increase in headline CPI (mom sa), reflecting lower gasoline prices;

- Euro Area, Industrial Production (Jul). GS -0.1%, consensus -0.1%, last -1.6%, all %mom. We expect Euro area industrial production (ex-construction) to show a small contraction on the month in July, in line with consensus. We expect the drop in German production as well as the expected contraction in Italian and Spanish production to weigh upon area wide IP;

- Euro Area, ECB Monetary Policy Decision. Deposit Facility Rate: GS -0.6%, consensus -0.5%, last -0.4%. We expect ECB officials to deliver a three-pronged easing package at this meeting. First, we look for a 20bp deposit rate cut, flanked by a tiered reserve system, which we expect to focus on excess reserves. Second, we expect a QE programme within the current constraints and a clear time limit. Third, the Governing Council is likely to enhance its forward guidance with a stronger link to inflation and an emphasis on the symmetry of the inflation aim.

- Friday: USA, Retail Sales (Aug). GS Core Retail Sales flat, consensus +0.3%, last +1.0%, all %mom. We estimate that core retail sales (ex-autos, gasoline, and building materials) were flat in August (mom sa), reflecting mean reversion in the non-store category following a record Amazon Prime Day in July. We also estimate a flat reading in the headline measure, and a 0.1% decline in the ex-auto measure, reflecting a rebound in auto sales but lower gas prices.

And visually:

Finally, focusing on the US, Goldman notes that the key economic data releases this week are the CPI report on Thursday and the retail sales report on Friday. There are no scheduled speaking engagements from Fed officials this week, reflecting the FOMC blackout period.

Monday, September 9

- There are no major economic data releases scheduled today.

Tuesday, September 10

- 06:00 AM NFIB small business optimism, August (consensus 103.5, last 104.7)

- 10:00 AM JOLTS Job Openings, July (consensus 7,311k, last 7,348k)

Wednesday, September 11

- 08:30 AM PPI final demand, August (GS flat, consensus flat, last +0.2%); PPI ex-food and energy, August (GS +0.1%, consensus +0.2%, last -0.1%); PPI ex-food, energy, and trade, August (GS +0.1%, consensus +0.2%, last -0.1%): We estimate a flat reading in headline PPI in August, reflecting relatively soft core prices as well as weaker energy prices. We expect a 0.1% increase in the core measure excluding food and energy, and also a 0.1% increase in the core measure excluding food, energy, and trade.

- 10:00 AM Wholesale inventories, July final (consensus +0.2%, last +0.2%)

Thursday, September 12

- 08:30 AM CPI (mom), August (GS +0.11%, consensus +0.1%, last +0.3%); Core CPI (mom), August (GS +0.24%, consensus +0.2%, last +0.3%); CPI (yoy), August (GS +1.81%, consensus +1.8%, last +1.8%); Core CPI (yoy), August (GS +2.37%, consensus +2.3%, last +2.2%): We estimate a 0.24% increase in August core CPI (mom sa), which would boost the year-on-year rate by two tenths to 2.4% on a rounded basis. Our monthly core inflation forecast reflects a modest further boost from the tariffs implemented in May and June, which we expect to manifest in the household furnishings, auto parts, and personal care categories. We also expect a large rise in the apparel category related to methodological changes earlier this year. On the negative side, we expect a pullback in airfares reflecting lower oil prices, and we expect a further deceleration in monthly used car inflation, which we nonetheless expect to remain positive. We estimate a 0.11% increase in headline CPI (mom sa), reflecting lower gasoline prices.

- 08:30 AM Initial jobless claims, week ended September 7 (GS 220k, consensus 215k, last 217k); Continuing jobless claims, week ended August 31 (consensus 1,678k, last 1,662k); We estimate jobless claims increased by 3k to 220k in the week ended September 7, after increasing by 1k in the prior week.

Friday, September 13

- 08:30 AM Retail sales, August (GS flat, consensus +0.2%, last +0.7%); Retail sales ex-auto, August (GS -0.1%, consensus +0.1%, last +1.0%); Retail sales ex-auto & gas, August (GS +0.1%, consensus +0.3%, last +0.9%); Core retail sales, August (GS flat, consensus +0.3%, last +1.0%): We estimate that core retail sales (ex-autos, gasoline, and building materials) were flat in August (mom sa), reflecting mean reversion in the non-store category following a record Amazon Prime Day in July. We also estimate a flat reading in the headline measure, and a 0.1% decline in the ex-auto measure, reflecting a rebound in auto sales but lower gas prices.

- 08:30 AM Import price index, August (consensus -0.5%, last +0.2%)

- 10:00 AM University of Michigan consumer sentiment, September preliminary (GS 89.5, consensus 90.4, last 89.8); We expect the University of Michigan consumer sentiment index declined by 0.3pt to 89.5 in the preliminary September reading, as recent economic misses could weigh on sentiment.

- 10:00 AM Business inventories, July (consensus +0.3%, last flat)

Source: DB, Goldman Sachs

Tyler Durden

Mon, 09/09/2019 – 08:32

via ZeroHedge News https://ift.tt/2N6dStE Tyler Durden