“A Looming Wall Of Dollar Debt:” 2020 Could Be A Disastrous Year For China’s Domestic Bond Market

New data compiled by Bloomberg, warns that 2020 could be the year of meltdowns in China’s domestic bond market.

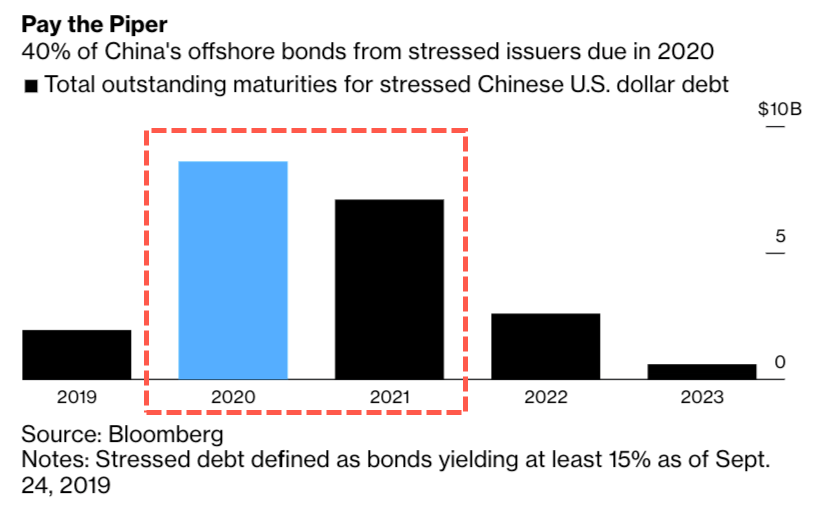

The report said, “a looming wall of dollar debt,” issued by borrowers who are experiencing rapid financial deterioration, might have extreme difficulty in repaying $8.6 billion of offshore bonds coming due next year that have 15% yields.

This equates to 40% of the total outstanding corporate dollar bonds from China’s most distressed companies comes to maturity right before the 2020 US presidential election, and also, at a time when the global economy could be in a trade recession.

“This is a market where you want to go for safer bets rather than be a hero,” said Michel Lowy, chief executive officer at Hong Kong-based SC Lowy, which specializes in fixed income. “We are on the verge of a massive snowball effect,” where defaults spur funds to take money out of high-yield debt, driving up yields and making it all the harder for firms to refinance, he said.

Wonnie Chu, managing director of fixed income at GaoTeng Global Asset Management Ltd., revealed to Bloomberg that many of these companies acquired cheap debt during 2017/18, the period of synchronized global expansion.

Chu said a lot of the debt was issued with a “low-interest-rate not comparable to the credit risk.” She added that a full-blown shock will likely be avoided but adds that stress will certainly be seen next year among borrowers.

Morgan Stanley, in anticipation of economic turbulence next year, has cut their holdings of riskier companies. MS said Asian high-yield credit funds experienced outflows in August.

Bloomberg notes below several issuers with bonds coming due next year that have stressed-level premiums:

- Yida China Holdings. Calls to the property developer in Shanghai seeking comment on its financing outlook went unanswered.

- Tewoo Group Co. Calls to the state-linked trading group based in Tianjin, southeast of Beijing, also went unanswered.

- Peking University Founder Group. A spokesperson for the technology services firm in Beijing said the group has an ample credit line with lenders, with 62.5 billion yuan ($8.8 billion) untapped as of June, and cash of 45.3 billion yuan.

- Oceanwide Holdings. The developer based in Beijing declined to comment when reached by phone.

Bloomberg also said half of the stressed companies are in property development.

MS research warned that China’s high-yield dollar-debt issuers have higher default risks than peers in other countries.

Kelvin Pang, head of the MS’ Asia credit strategy team in Hong Kong, told clients last month that default risks are higher with these companies “because of relatively short bond-maturity profiles — at close to 2.5 years.”

Pang said high-yield issuers’ loans maturities are very short in duration, at one to three years. It means that “China corporates are extremely sensitive to credit conditions,” and with a global trade recession expected to strike by the 2020s, all eyes are on China ahead of a “looming wall of dollar debt” due next year.

And 2020, according to the Chinese calendar, will be the year of the ‘rat’ — a 12-year cycle of animals that last appeared in 2008.

Tyler Durden

Thu, 09/26/2019 – 18:50

via ZeroHedge News https://ift.tt/2nwqCxY Tyler Durden