Futures Fall As Traders Brace For Dismal Payrolls Report

Global stocks faded a modest early session rebound, US equity futures drifted lower, and safe haven assets rose ahead of a key jobs report as investors hoped this week’s dismal data would trigger more U.S. interest rate cuts as “bad news is great news” again. Trading volumes were deplorable after a bruising week for risk after a slew of week economic data that revealed a slowdown in U.S. manufacturing and services.

“(The) market has very quickly reversed to the ‘bad news is good news’ model and rallied on increased rate cut expectation,” said Marija Veitmane, multi-asset senior strategist at State Street Global Markets.

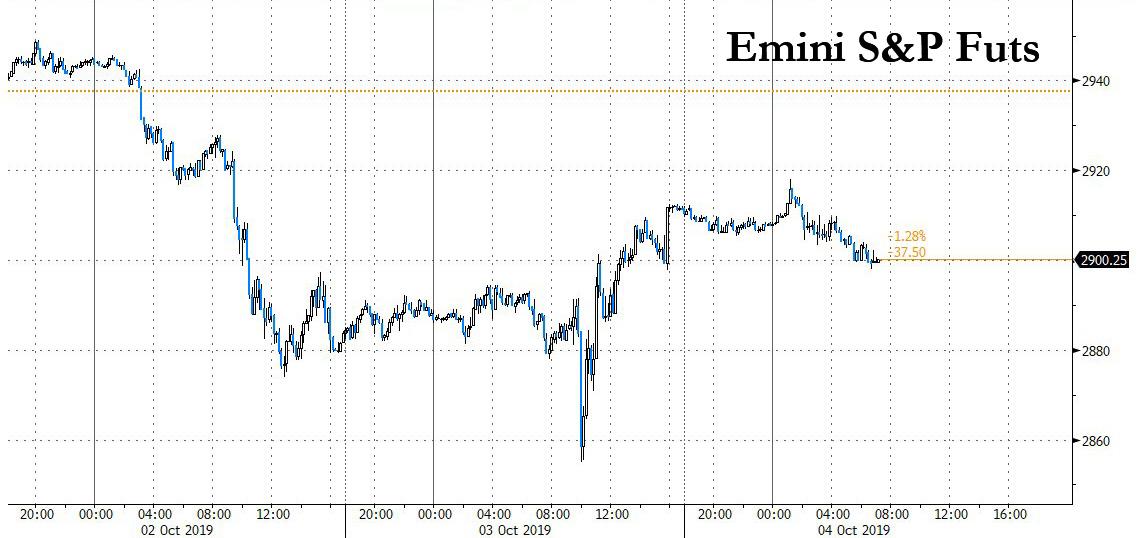

S&P futures were down 11 points at last check ahead of Friday’s September payrolls report (previewed here), reversing a pop higher triggered by a Nikkei report that Apple is raising iPhone 11 output by up to 10% and following a 0.80% increase in the S&P 500 on Wall Street overnight on hopes that future Fed rate cuts will support corporate profits.

For those pressed for time, here is a rundown of key events in the overnight session:

- European equities are indecisive and overall little changed ahead of US jobs report

- White House Trade Adviser Navarro reiterated that there will be no small deal with China

- Beijing is in no hurry to forge a deal, and cites the one secured between US and Japan as a reason for not rushing., SCMP

- Fed’s Clarida was optimistic on the economy, noted Fed is not on a pre-set course and a standing repo facility will be discussed in future meetings

- USD is marginally softer thus far, fixed is firmer; note, RBI cut by 25bp as expected

- Looking ahead highlights include US NFP and Trade, Baker Hughes, Canadian Trade, ECB’s de Guindos, Fed’s Powell, Rosengren, Bostic, Kashkari, Brainard, Quarles

European markets ground sideways ahead of today’s U.S. payrolls number. European equities pared back initial gains to trade flat, with autos, miners and energy names weighing; the Stoxx Europe 600 Index gave up its early advance as automakers and banks weighed down the gauge. The Stoxx 600 Technology Index topped the wider benchmark in Friday’s early trading with a gain of as much as 1%, following a report that Apple has told suppliers to increase production of its latest iPhone 11 range by as much as 10%. Semi names such as AMS +3.3%, Aixtron +3.2%, Dialog 2.6%, IQE +2.6%, STMicro +2.5%, Besi +2.3%, and ASML +0.9% were all higher in early trading. Oddo said the Nikkei Asian Review report confirmed that demand for the new iPhone 11 range exceeds expectations, which have been more cautious than last year. In the UK, the FTSE 100 outperformed. G-10 FX trades in a tight range.

Earlier in the session, Asian stocks fluctuated, heading for a weekly drop, as investors looked toward the U.S. non-farm payrolls report due Friday and Chinese Vice Premier Liu He’s Washington trip next week. Markets in the region were mixed, with Australia advancing and Hong Kong leading declines. China’s onshore market remains closed for National Day holidays. The Topix gained 0.3%, buoyed by Central Japan Railway and Sony. Bank of Japan Deputy Governor Masazumi Wakatabe said policy makers don’t want to continue low or negative interest rates for a long time. Hong Kong’s Hang Seng Index declined 1.1%, with real estate developer Sun Hung Kai Properties leading losses. The city invoked colonial-era emergency powers for the first time in more than half a century to ban face masks for protesters. Real estate stocks in the region underperformed as Hong Kong’s property market continues to bear the brunt of local riots, with reports stating that homeowners are slashing house prices by over 20% amid reluctant buyers and banks reducing property valuations due to the increasing violence. As a reminder, Mainland China remained closed due to its National Week holiday. Elsewhere, the Sensex dropped 0.7%, dragged by large lenders, after India’s central bank cut rates by 25 basis points and lowered its full-year growth forecast.

The MSCI World index, which was slightly lower on the session, was on track for a 1.8% drop on the week, its worst in two months, hurt by a surge in weak global data, political uncertainty in the United States and Hong Kong, geopolitical tensions in the Middle East and Brexit.

In other key news, a late Thursday report by CNN said that President Trump told Chinese President Xi that he will stay quiet on HK amid trade talks. At roughly the same time, White House Trade Adviser Navarro reiterated that there will be no small deal with China and added “we will get a great deal with China or no deal”. In response, the SCMP published an Op-Ed which stated, “Beijing is in no hurry to forge a deal and the one struck between the US and Japan on September 25 is good reason for not rushing”. The article noted that there was no agreement for the immediate removal of US penalties on Japanese vehicles and parts, but the accord referred to a levy elimination at a future date without specifying a time frame.

While talks between Beijing and Washington resume next week, aimed at agreeing a truce over the protracted trade spat between the world’s two largest economies, hopes of a definitive agreement are pretty low. Global equities could fall as much as 15-20% if negotiations break down and Trump follows through with his threat of car imports tariffs, UBS global chief investment officer Mark Haefele warned on Friday. The Swiss bank reckons there’s a 50% probability that additional duties will be announced by the year-end, potentially pushing global growth down to 3% next year, the slowest pace since the global financial crisis.

“Without a resolution to the U.S.-China trade dispute, we see limited upside for stocks in the near-term, and given the risks of further escalation we hold a modest tactical underweight on equities,” he said.

But first there is the main event of the day: nerves ahead of today’s jobs number – which may miss bigly based on ISM surveys…

… sent investors into safe haven asset such as government bonds and gold. The report is expected to show the world’s top economy added 145,000 new jobs in September, more than an increase of 130,000 in the previous month. If the soft U.S. ISM data is validated by Friday’s payrolls report, then the economic slowdown at a minimum will have “taken all of the sting out of the USD top side,” Deutsche Bank’s Alan Ruskin said. Others echoed this assessment: while it’s “too early” to call for the dollar to turn down on a broad basis, the yen remains the “main opportunity” among G-10 currencies, said Zach Pandl, co-head of global FX and emerging-market strategy at Goldman Sachs Group Inc.

In rates, Bunds and Treasury futures traded slightly higher around Thursday’s best levels with the long-end outperforming, flattening the curve mildly ahead of the payrolls report. Yields lower by ~1bp in 7- to 30-year sectors, 10-year by 0.7bp at 1.527%; 2s10s flatter by ~1bp, 5s30s by about 0.5bp, paring weekly steepening moves spurred by bigger-than-expected declines in ISM manufacturing and services gauges. Gilts outperformed after EU gave Boris Johnson one week to revise his proposed Brexit deal.

In FX, the dollar index dropped after hitting a 2-1/2-year high this week. It was down 0.3% on the week. Traders now see a 85.2% chance the Fed will cut rates by 25 basis points to 1.75%-2.00% in October, up from 39.6% on Monday, according to CME Group’s FedWatch tool. The Fed has already cut rates twice this year as policymakers try to limit the damage caused by the bruising Sino-U.S. trade war. The dollar edged down to 106.81 yen, close to a one-month low of 106.48 yen reached on Thursday. The euro was a shade higher at $1.0974, near a one-week high. NZD and AUD outperformed at the margin, while INR was slightly softer after the RBI matched market consensus for a 25bp rate cut.

In commodities, crude futures drift higher in choppy trade. Base metals are mixed with nickel +0.8% as inventories drop, copper down 0.5%, while spot gold was up 0.3%, on course for a 0.75% weekly gain.

Today’s calendar sees economic data including September payrolls and the US trade balance.

Market Snapshot

- S&P 500 futures down 0.2% to 2,907.00

- STOXX Europe 600 up 0.2% to 378.29

- MXAP up 0.08% to 155.56

- MXAPJ unchanged at 497.19

- Nikkei up 0.3% to 21,410.20

- Topix up 0.3% to 1,572.90

- Hang Seng Index down 1.1% to 25,821.03

- Shanghai Composite down 0.9% to 2,905.19

- Sensex down 0.7% to 37,824.66

- Australia S&P/ASX 200 up 0.4% to 6,517.08

- Kospi down 0.6% to 2,020.69

- German 10Y yield fell 0.7 bps to -0.597%

- Euro up 0.08% to $1.0974

- Brent Futures up 0.7% to $58.09/bbl

- Italian 10Y yield fell 7.3 bps to 0.488%

- Spanish 10Y yield fell 0.8 bps to 0.123%

- Brent Futures up 0.6% to $58.08/bbl

- Gold spot up 0.2% to $1,508.61

- U.S. Dollar Index down 0.01% to 98.86

Top Overnight News

- U.K. PM Johnson and the EU have given themselves a week to agree on a Brexit plan. Otherwise, Britain will be heading for either a no-deal exit or another postponement of its departure. While support is building for Johnson’s proposals at home, the EU’s chief negotiator Michel Barnier said the plans for the Irish border issue falls short of his conditions for a deal

- The world’s biggest government-debt markets are sending a clear signal that global economic growth is stalling and inflation expectations are fading fast. That sobering message is evident in tumbling yields on Treasuries and German bunds, in bond-market inflation metrics projecting further declines in price pressures and in a gauge that shows investors see no need for extra compensation to load up on long-term debt

- Two top American diplomats tried to strike a deal on behalf of President Trump for Ukraine’s leader to investigate discredited allegations of wrongdoing by Joe Biden and his son in return for improving relations with the U.S., according to documents released by House Democrats late Thursday

- Hong Kong invoked emergency rule for the first time in a half a century to ban face masks on protesters, Now TV reported, as authorities look to quell months of unrest

- WeWork’s leaders told staff that job cuts are coming as soon as this month. In a meeting with employees Thursday, company bosses said that cost- cutting efforts would include layoffs, according to attendees. The cuts will be handled as “humanely” as possible, one executive said, according to the people, who asked not to be identified

Asian equities traded with no firm direction as the region derived little impetus from the upbeat performance on Wall Street ahead of the US labour market report, where stocks rose amid increased expectations for further Fed stimulus after this week’s ISM metrics declined to multi-year lows. ASX 200 (+0.4%) treaded water for most of the session and was little swayed by reports that Commonwealth Bank of Australia’s life insurance arm has been charged with 87 counts of hawking life insurance products. Meanwhile, Nikkei 225 (Unch) remained within a tight range amid the cautiousness in the market and an uneventful domestic currency. Elsewhere, Hang Seng (-0.4%) was modestly softer ahead of an emergency meeting held by Chief Executive Lam which is anticipated to be on emergency regulation to ban protesters’ face masks, according to sources, although the enforcement of this law is still in question. Further, real estate stocks in the region underperformed as Hong Kong’s property market continues to bear the brunt of local riots, with reports stating that homeowners are slashing house prices by over 20% amid reluctant buyers and banks reducing property valuations due to the increasing violence. As a reminder, Mainland China remained closed due to its National Week holiday.

Top Asian News

- India Cuts Rates Fifth Time Amid Economic Slowdown, Banking Woes

- Fighting Against Bank of Japan May Not Be Crazy After All

- There’s a New Hedge Fund for Badly Governed Companies in Japan

- How Far Hong Kong’s Emergency Law Can Go (Online Too): QuickTake

Major European Bourses (Euro Stoxx 50 -0.1%) are mixed and little changed overall, in relatively rangebound trade ahead of pivotal US employment data. However, Indices are off of yesterday’s post weak US ISM Non-manufacturing data lows, managing to track the bounce back seen on Wall Street. JPM argue that the rise off lows seen in US indices was fairly unimpressive due to its low volume, and suggest the move was likely an oversold bounce, since prior to the data the SPX was already 4.5% lower on the week. Nonetheless, the bank acknowledges a number of other factors could have been lending support: Firstly, the bank suggested that investors may have returned to the mentality of “bad data is good data” again in the US, since it increases the likelihood of more aggressive Fed easing. Indeed, the odds of a Fed rate cut this month has now increased to near 100% (up from 50/50 at the start of the week). Secondly, the base case for most investors is for some kind of trade truce between the US and China this month, with such trade hopes helping the market rebound from similar levels in the month of September. Thirdly, poor manufacturing PMI data earlier in the week had already set the bar very low, and the non-manufacturing data was not a disaster in that it is still above the expansionary/contractionary 50 mark. Finally, JPM say that new WTO permitted US tariffs on EU imports weren’t as bad as feared, and any EU response is unlikely before the beginning of 2020 (although the US decision on EU auto tariffs looms in November). Sector are mostly in the green; Health Care (+0.6%) is the outperformer while Materials (-0.4%), Consumer Discretionary (-0.4%) and Financials (-0.6%) (on lower yields) lag. Notable individual movers include; STMelectronics (+2.0%) and other Apple suppliers were buoyed by the news that the iPhone maker is to increase production of its iPhone 11 by 10%. London Stock Exchange (+2.1%) caught a bid on premarket reports that investors in the Co. will push for the Hong Kong Stock exchange to up its takeover offer by 20%, including more cash. UK Insurance names, including Admiral Group (+0.8%) and Direct Line (-2.6%), are under pressure on the news that the FCA may ban some pricing practices used by insurers, having determined that competition is not working effectively in the market. BP (+0.8%) outperformed other energy names on the news that its CEO Dudley had resigned. Finally, Deutsche Lufthansa (-3.6%) shares were weighed by news that the German Government reportedly intents to increase taxes on flight tickets.

Top European News

- U.K. MP Rory Stewart Resigns From the Conservative Party

- Italy 2Q Year-to-Date Budget Deficit at 4.0% of GDP

- Europe Airlines Winter Capacity Outlook ‘Constructive,’ RBC Says

- Swedish Nationalists Now Even With Social Democrats in Poll

In FX, the Dollar is treading gingerly into the final big US release of the week having been wrong-footed by both ISM surveys and buffeted by a dire Chicago PMI along the way. Indeed, having kicked off the new month/quarter with a fresh ytd high (99.667) the DXY is struggling to contain losses below the 99.000 level and only just off a circa 98.630 base amidst further bull re-flattening across the US Treasury yield curve and lofty October FOMC easing expectations (80%+ probability for another 25 bp cut). In terms of the key BLS metrics, consensus for headline payrolls is 145k, with the jobless rate seen at 3.7% and average earnings forecast to hold at 3.2% y/y, but after an ADP miss and other soft employment proxies the NFP skew seems to be on the downside. Hence, nearest technical supports for the index could be vulnerable and for reference 98.730 represents a Fib retracement ahead of the 30 DMA at 98.616.

- NZD/AUD – The Kiwi is back at the head of the G10 pack having relinquished pole position to the Pound late yesterday, with Nzd/Usd climbing further above 0.6300 and Aud/Nzd nudging further below 1.0700 even though the Aussie is also benefiting from its US counterpart’s demise and consolidating around 0.6750.

- CHF – The Franc has pared some of its recent heavy losses on a multiple of well known/documented bearish factors, and reports that the EU may be set to remove Switzerland from its tax haven grey list could well be aiding the recovery. Usd/Chf is back below parity and Eur/Chf has shied away from 1.1000, but this may just be consolidation and short covering given the scale of depreciation of late.

- EUR/JPY/CAD/GBP – All firmer against the Buck, but relatively rangebound and off Thursday’s post-US ISM highs awaiting the aforementioned key US labour report. The single currency is confined between 1.0984-64 and decent option expiries from 1.1000-20 to 1.0925 (just over 1 bn either side), the Yen is meandering in an equally tight band through 107.00, Loonie within 1.3340-20 parameters ahead of Canadian trade data and Sterling trades tentatively on the 1.2300 handle eyeing Brexit-related news in the pre-NFP amble.

- EM – The Rupee is just about on an even keel with the Greenback in wake of the latest RBI rate cut that was in line with median expectations, at -25 bp, but not as big as some were anticipating or hoping for. Hence, Usd/Inr is off lows and skirting 71.1000.

- Riksbank’s Jansson says they have seen a relatively rapid decline in the economic situation. Recent developments have underscored his view that it would not be a good idea to lift rates at the end of 2019 or start of 2020. (Newswires)

- RBI cut rates by 25bp as expected to 5.15% (Prev. 5.40%). Decision was unanimous, retained accomodatie stance, note the conituned slowdown ‘warrants intensified efforts’ to restor India’s growth momentum; negative output gap has widened further.

The crude complex is edging higher, seemingly tracking the bounce in US/European equities, amid a lack of fresh fundamental drivers. WTI and Brent Nov’ 19 futures have built on overnight gains, the former now probing resistance at the USD 52.90/bbl region (yesterday’s high) ahead of the USD 53.00/bbl mark, while the latter has already cruised past USD 58.00/bbl and eyes resistance at USD 58.40/bbl (Tuesday’s low). Brent seemed unresponsive to news of a halt in production in the Buzzard Oil field in the North Sea (capacity of 180k BPD), but analysts note such news has been market moving in the past. The pace of new Middle Eastern geopolitical developments, particularly on the US/Saudi/Iran front, appears to have slowed for the time being, although the head of the UN’s Nuclear Watchdog, the IAEA, said that Iran has improved their cooperation with the organisation, but issues are not completely addressed. Elsewhere, the desk is monitoring ongoing violent protests in Iraq (locals are protesting against government corruption, poor public services etc.); for now, protests don’t seem to present any risk to the country’s oil industry/exports. Meanwhile, the news that US Energy Secretary Perry is expected to resign in November, and be replaced by Deputy Energy Secretary Brouillette, has done little to move the dial. Gold is marginally higher but appears rangebound ahead of today’s NFP print, in cautious trade following yesterday’s choppy post ISM data action which saw the precious metal spike from the low USD 1500s/oz to the mid USD 1520s/oz before retracing. Technicians will be eyeing resistance at yesterday’s USD 1525.50/oz high and support at the USD 1511/oz (yesterday’s post data low and Wednesday’s high) and USD 1502/oz marks (yesterday’s low). Copper prices are lower, as growth concerns linger in wake of this week’s slate of poor US and European PMI readings, albeit copper prices are off monthly lows. Potentially lending to underperformance in the red metal are reports noting that Antofagasta is seeking negotiations with workers at its Chilean Antucoya mine in an attempt to stave off a strike, albeit union leaders said there had been little progress

US Event Calendar

- 8:30am: Average Hourly Earnings MoM, est. 0.2%, prior 0.4%

- 8:30am: Change in Nonfarm Payrolls, est. 145,000, prior 130,000

- 8:30am: Change in Private Payrolls, est. 130,000, prior 96,000

- 8:30am: Change in Manufact. Payrolls, est. 3,000, prior 3,000

- 8:30am: Unemployment Rate, est. 3.7%, prior 3.7%

- 8:30am: Two-Month Payroll Net Revision

- 8:30am: Average Hourly Earnings YoY, est. 3.2%, prior 3.2%

- 8:30am: Average Weekly Hours All Employees, est. 34.4, prior 34.4

- 8:30am: Labor Force Participation Rate, est. 63.2%, prior 63.2%

- 8:30am: Underemployment Rate, prior 7.2%

- 8:30am: Trade Balance, est. $54.5b deficit, prior $54.0b deficit

Central Bank Speakers

- 8:30am: Fed’s Rosengren Speaks at Boston Fed Conference

- 10:25am: Fed’s Bostic Speaks at Tulane University

- 2pm: Powell Makes Opening Remarks at Fed Listens Event

DB’s Jim Reid concludes the overnight wrap

After a testing week, how am I going to relax this weekend? Now my daughter is in the school system I’m forced to go to my first big school event – a family fun run. For avoidance of doubt I won’t be running or having fun. Here’s hoping the twins run in the same direction.

It hasn’t been much of a fun run for markets this week and today we welcome in another payrolls Friday. After the two big ISM misses this week including yesterday’s services miss – which we’ll come to shortly – arguably this has become one of the most anticipated employment reports for a long time.The market has swiftly repriced to 22bps of cuts for October’s Fed meeting versus 10bps this time last week. So we haven’t quite got a full cut priced in but clearly we’ve seen a big step change in expectations this week given the data and even an in-line payrolls reading today shouldn’t do much to change the narrative. The consensus for today is for a 145k payrolls print which follows 130k in August with the range amongst the survey participants on Bloomberg anywhere from 85k to 185k.

Our economists are below market at 125k however they note that this could again be boosted by Census workers, which is why it will be critical for market participants to focus on private payrolls (100k forecast vs. 130k consensus and 96k previously). A payroll print in line with our colleagues’ forecast should have the effect of raising the unemployment rate a tenth to 3.8%. Note that similar to August, the consensus forecast for private payrolls has missed the initial print in four out of the last five Septembers by an average of 44k. The median miss during this period has been an even larger 64k. Indeed, if our team’s below consensus forecast is realised, the Fed’s characterisation of the labour market as “strong” could be questioned. As far as the rest of the report is concerned, earnings are expected to rise +0.3% mom and participation rate to hold steady at 63.2%.

So the tee up for today’s data came in the form of a much weaker than expected ISM non-manufacturing (52.6 vs. 55.0 expected). That’s the lowest level and biggest miss since August 2016. Apart from this one low reading in 2016, you’d have to go back to 2012 to get a lower number. However it was the employment component that most were focusing on and like the equivalent sub component of the manufacturing data earlier this week, it didn’t make for great reading after dropping 2.7pts to 50.4 and the lowest since February 2014. This has historically been a leading indicator for private payrolls so points at some real downside risk to payrolls over the coming months even if it doesn’t show up today.

The immediate reaction in markets to the data was a big rally across rates. Indeed 2y and 10y yields rallied the best part of 10bps and 7bps immediately and eventually closed last night near the lows at -9.0bps and -6.5bps respectively. The rally at the short end did mean the 2s10s curve steepened however and at 14.4bps is now at the steepest since early August. It was a similar story across other bond markets where in Europe 10y Bunds traded down to -0.590% (-4.3bps). Similarly Gold (+0.43%) turned in a third consecutive positive session.

In contrast to bonds, equities experienced more intraday volatility. Most markets promptly sold off as soon as the data was released, with S&P 500 down as much as -1.11% at the lows, however it clawed back to end up an impressive +0.81%.There were two, now-familiar catalysts driving the rebound: positive trade rhetoric and dovish Fed expectations. On the trade front, President Trump spoke optimistically about next week’s planned meeting between his team and Chinese Vice Premier Liu He. The NASDAQ and Philly semiconductor indexes were down a similar amount as the S&P 500 at the lows (-1.09% and -1.12% respectively), but they rebounded even more strongly to end +1.12% and +1.71%, consistent with their outsized trade exposure. Meanwhile, financials (+0.16%) lagged significantly as bond yields dropped and expectations for a near-term Fed rate cut solidified. The VIX traded at an intraday high of 21.44 but ultimately settled down to close back at 19.1, while in Europe the STOXX 600 closed only -0.02% lower. Meanwhile US HY credit spreads were +12bps wider and Oil fell -0.61%. That means oil is now down for 8 sessions in a row – the longest run since last November – and amazingly is trading $11 lower than the post drone strike intraday highs last month and -4.61% below where we were just before the attack.

This morning in Asia markets are largely trading flattish to down with the Nikkei (+0.03%) and Kospi (+0.02%) broadly unchanged while the Hang Seng (-0.54%) is lower. Chinese markets remain closed for their week long holiday. Elsewhere, futures on the S&P 500 are down -0.11% and yields on 10yr JGBs are down -1.3bps to -0.215%.

In other overnight news, the White House trade adviser Peter Navarro, a China hawk, reiterated in an interview with the Fox Business Network overnight that the US will get a great deal with China on trade or there will be no deal. Earlier in the week, Navarro had also said that the unrest in Hong Kong provides context for trade talks. If Hong Kong is brought up as part of trade discussions though then this is likely to limit the possibility of reaching a deal. Elsewhere, Hong Kong is expected to ban face masks for protesters today in a bid to quell months of violent unrest, invoking emergency rule for the first time since the city came under Chinese control in 1997. The move to invoke colonial-era emergency powers — last used more than 50 years ago — is likely to trigger intense clashes this weekend, with protesters already calling for mass demonstrations to oppose the law (per Bloomberg).

Before we get to the weekend, Fed Chair Powell is due to speak at 7pm BST tonight at a Fed Listens Event where he is scheduled to make opening remarks. Given the data this week expect there to be plenty of focus on his remarks. Ahead of that Vice Chair Clarida spoke last night and the most important comments from him came on the balance sheet as he said that “We indicated in July that at some point after a time that we’d begin to grow our balance sheet again and Chair Powell indicated that is a topic we will be discussing in our October meeting, So we’ll have something for you after our October meeting on that.” On the economy his comments were a bit hawkish as he said that “The economy is in a good place. The consumer is in good shape, inflation is stable.” So non-committal towards a rate cut at the October meeting despite the recent barrage of weak economic data.

Back to yesterday and whilst not as market-moving as the ISM report, it’s worth noting that the final European PMIs were also weak, with the euro area services index revised down -0.4pts to 51.6, taking the composite index to 50.1. That’s the lowest reading since June 2013. On a country level, Italy was the only outperformer, with the services PMI at 51.4 compared to consensus for 50.5. Other than that, it was uniformly negative, with Spain’s reading at 53.3 compared to expectations for 53.9, and with France and Germany’s services indexes revised down -0.5pts and -1.1pts to 51.1 and 51.4. That takes Germany’s composite PMI to 48.5, the first time that Europe’s largest economy has had the lowest composite print among the big-four European countries since the early 2000s. That fairly dire data has again focused attention on the outlook for fiscal support. Mark Wall published a new note yesterday examining the scope for fiscal easing (link here ). He thinks the data would need to deteriorate further before we get meaningful easing, but if and when we do get fiscal support, it could equal around one percent of euro area GDP.

On the Brexit front, the only noteworthy news yesterday was a series of comments from the Irish Deputy Prime Minister Simon Coveney, who said that “if that (the UK’s latest plan) is the final proposal, there will be no deal.” However, he did leave the door open to further negotiations, rather than rejecting the process completely, so that was a positive and it does keep the path open towards a deal. From the UK side, the current plan does now command support from the pro-Brexit ERG, Northern Ireland’s DUP, and some labour MPs, raising the odds that it could survive a parliamentary vote if that ends up occurring. The pound ultimately gained +0.30%.

Finally to the day ahead where the obvious focal point will be this afternoon’s US September employment report. Away from that it’s very quiet for other data with only the September construction PMI due in Germany and September new car registrations due in the UK. Next in line at the Fed are Rosengren and Bostic before we get the aforementioned Powell opening remarks at an event this evening. The ECB’s Guindos is also due to speak today.

Tyler Durden

Fri, 10/04/2019 – 08:01

via ZeroHedge News https://ift.tt/352jEC9 Tyler Durden