Here’s The Simple Reason Why A Global Economic Recovery Is Not Coming

One of the recurring themes that emerged since the start of September, is that not only will an economic recession be avoided (thanks to the Fed’s three recent rate cuts and $60 billion in monthly QE) but the global economy is now on an upswing.

To see Wall Street’s recent bullish reversal in thinking on this critical issue look no further than the latest piece from Goldman’s David Kostin who starts his latest Weekly Kickstart piece by saying that “The performance of the US equity market during the past three months suggests the pace of US economic growth will improve in the near future” adding that “recent data releases have supported the market’s expectation for a rebound in the US economy.” Additionally, as we reported over the weekend, perennial market bear Morgan Stanley finally threw in the towel and after downgrading global stocks to a Sell in July, turned Neutral (after what we assume were countless complaints by its clients who accused the bank of missing the recent rally).

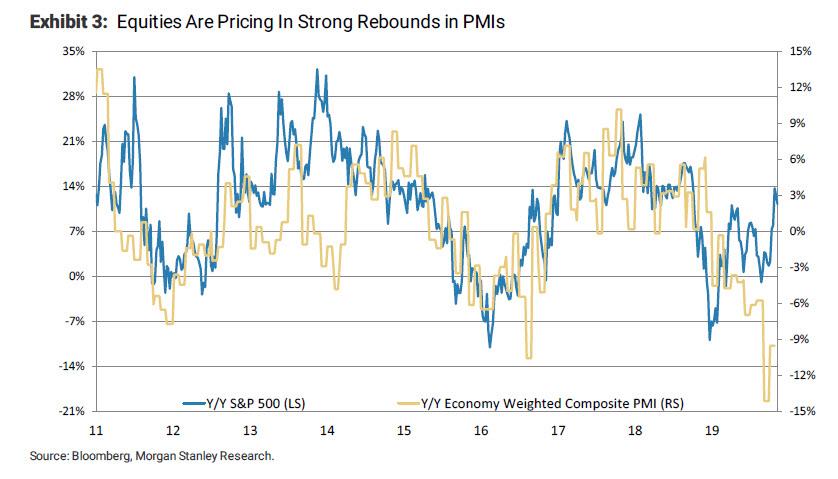

One look at the market, and it’s clear: stocks have now fully priced in a global recovery, and are expecting a dramatic surge in global PMIs in the coming months.

But has the global economy indeed troughed, and is a period of smooth sailing ahead? The answer will depend, as it traditionally has in the past decade, on whether China will stimulate both its own, and the global economy to the point where it successfully triggers a global inflationary shockwave around the globe.

Unfortunately, the answer for now appears to be a resounding no, and not just as a result of the latest leading economic indicators out of China which missed across the board, confirming that Beijing is bracing for the first ever sub-6% GDP print.

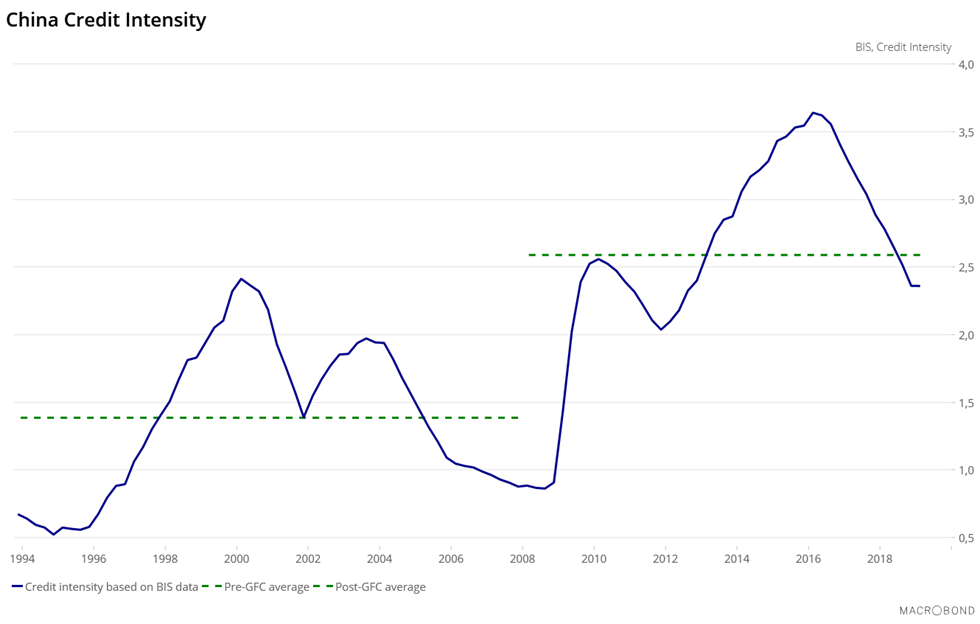

As Saxo Bank’s Christopher Dembik writes, there is another reason ahy China will not open massively the credit tap anytime soon. But before we get into his argument, as a reminder, the latest Chinese credit data was a disaster, with the revised Aggregate Financing data series printing at its lowest level on record as we discussed in “China’s Credit Creation Unexpectedly Collapses At The Worst Possible Time.”

Using BIS credit data, Saxo Bank calculated China credit intensity since 1994. Before the Global Financial Crisis, China needed on average one unit of credit to create one unit of GDP. Since 2008, 2½ units of credit are required to create one unit of GDP. In other words, it means that China needs much more credit than 10 years ago to have the exact same amount of GDP. Injecting more credit in the economy is not the miracle solution it used to be, and the disadvantages of credit push tend to surpass the advantages.

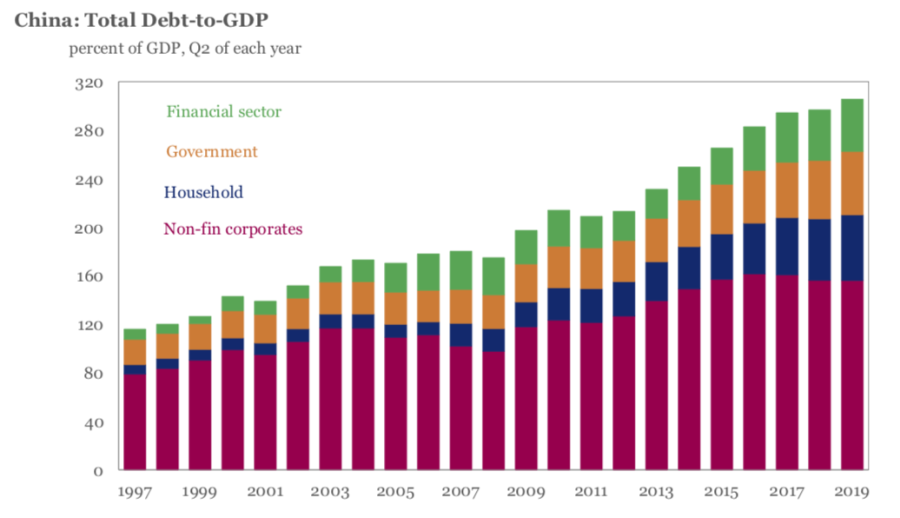

As Christopher notes, higher credit intensity over the past years has directly fueled the debt engine, the same debt engine that single-handedly pulled the world out of a global depression in 2008/2009. Alas, this will not happen again: China’s public and household debts are at their highest historical levels, respectively at 51% of GDP and 53% of GDP, and the private sector debt service ratio is becoming a burden for many companies, reaching on average 19.7% This records an increase from 13% before the crisis. Overall, China’s debt to GDP is fast approaching an unprecedented 320%!

Here is a more vivid representation of the above, one in which China’s record debt bubble gives the world the finger:

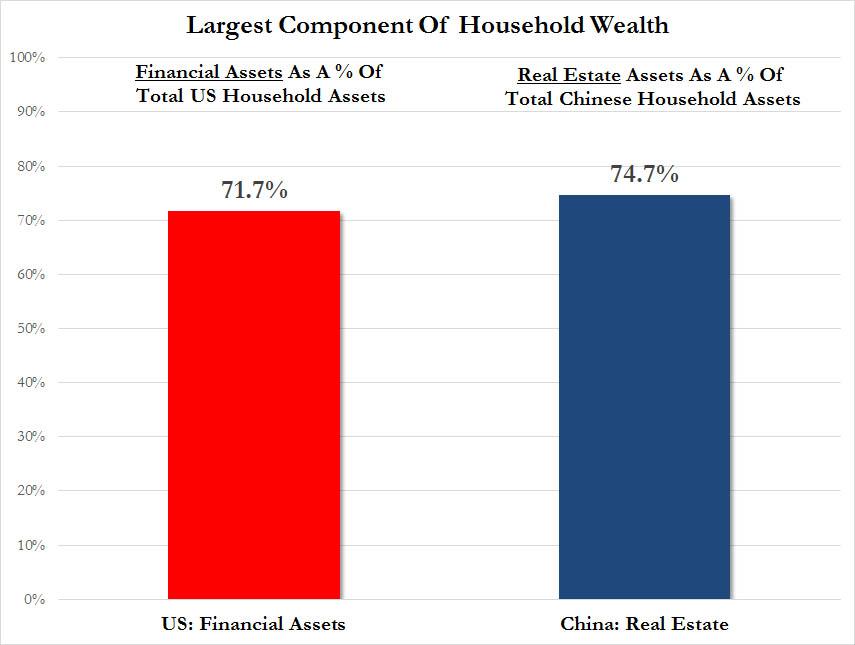

On the top of that, the PBoC will probably refrain from massive easing as long as the real estate sector remains well-oriented. As we have discussed here extensively in the past, Chinese housing is the key economic sector for China’s growth as it represents around 75% of Chinese people’s wealth (in the US, it is financial assets that are the primary source of household net worth).

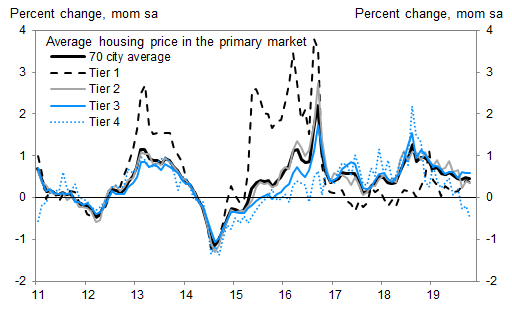

And while completed investment growth in real estate has decelerated since last spring, and some housing tiers are starting to sputter, especially the lowest, Tier 4, China’s real estate sector is still at high level compared with previous years, running slightly above 10% YoY in last September.

As Saxo concludes, “that high credit intensity combined with resilience in the real estate sector will push the PBoC to be in wait-and-see position until the end of the year and to adopt a fine-tuning policy in 2020 if needed.”

It’s not just Saxo: according to One River’s Eric Peters, China is actually deliberately slowing the economy in hopes of buying more time to enjoy economic stability, well aware that one wrong move with 320% debt/GDP could lead to catastrophe. Below we excerpt from Peters’ latest note:

“Beijing smoothed previous cycles, now they’re truncating the tails,” said Alpha. They’ll accept more slowing than in the past, to avoid a boom and bust. “You see it in the data, their reaction function changed.”

Beijing is pursuing policies to moderate leverage. They could slash interest rates, or announce massive infrastructure spending, but haven’t. “Incremental global growth is no longer driven by the Fed, the ECB or BOJ. It is driven by China. They’re deliberately slowing. And only a contraction in the real estate sector will get them to stimulate.”

“Beijing sees HK’s problems as driven by property prices that priced people out forever,” said Alpha. “2016 stimulus went into property. Recent attempts to maintain growth have focused on local infrastructure, but the IRRs are low, so money finds its way into property which is not what they want.” Beijing can’t afford housing prices to run away, but construction is the source of credit creation – which must be maintained – it’s a daunting problem. “Xi consolidated power – he’s not going to now trade cyclical growth for longer-term instability.”

Bingo. Which brings us to Saxo’s dour conclusion for all those who believe that the global economy is about to enjoy another period of sustainable growth (and has confused the Fed’s QE for economic resilience and fundamentals):

Contrary to previous periods of slowdown, notably in 2008-2010, 2012-2014 and in 2016, China is unlikely to save the global economy once again.

Needless to say, without China – which has created 60% of all new global debt over the past decade – there can be no global recovery.

In other words, enjoy the current growth delusion while it lasts… some time into Q2 2020 when the Fed’s NOT QE will fade to nothing.

Tyler Durden

Mon, 11/18/2019 – 15:15

via ZeroHedge News https://ift.tt/2CRl7P3 Tyler Durden