FOMC Minutes Preview: Just What Is A “Material Reassessment” In The Outlook

At 2pm today the Fed will release the FOMC minutes from the October meeting, which will signal that policy is on hold for now, barring a material reassessment in the outlook, per Chair Powell’s recent rhetoric. As DB’s Jim Reid notes, it’ll be interesting to see if the minutes shed any light on what exactly would qualify as a “material reassessment,” as well as details on how deep the internal disagreement over the rate cut was. Also any updates on the policy review, and any new thoughts on dealing with funding market disruptions will be looked for.

As a reminder, in the October 31 meeting, the Fed concluded its “mid-cycle adjustment”, re-adopting a data-dependent approach. There is as always a risk the minutes will be stale – especially if they reveal a position the market is not expecting – revealing little new information, given the heavy slate of recent Fedspeak. Traders will also eye updates on the balance sheet, and potentially discussion of details regarding a Standing Repo Facility (SRF).

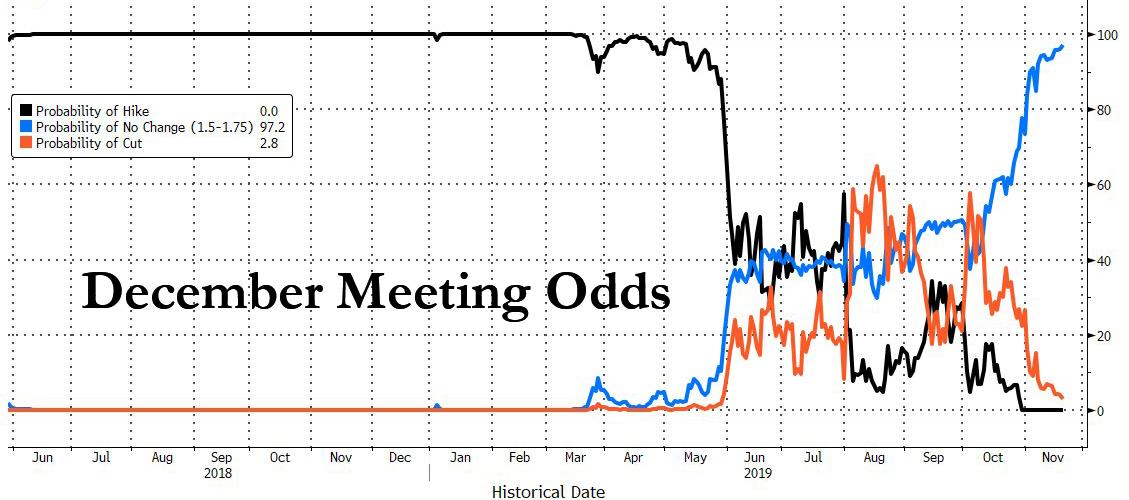

Meanwhile, with less than three weeks to go until the December 10 FOMC meeting, the odds of another rate cut have plunged from nearly 60% at the start of October to just 2.8% currently.

More details on what to expect in today’s Minutes release, courtesy of RanSquawk:

MEETING REVIEW:

The Fed cut rates by 25bps, as was anticipated. Hawkish dissent came from George and Rosengren again, although Bullard did not repeat his call for a deeper rate cut. The statement saw the Fed tweak its language on future rate moves, now stating it will “continue to monitor the implications of incoming information for the economic outlook as it assesses the appropriate path of the target range for the federal funds rate,” (from “will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion” – a line that the market had taken to meet that the door to further cuts was open); the tweak was subtle, which analysts said gives the Fed optionality on future moves. Additionally, much of the language on the economy was left unchanged: labor markets still remain “strong”; growth was rising at a “moderate rate”; business fixed investment and exports “remain weak”; job gains have been “solid”; household spending was rising at a “strong pace”; inflation still running below 2%. Analysts took the statement as a signal that the so-called mid-cycle adjustment was over, with the Fed now re-entering data dependency. Powell’s Press conference gave further credence to that view.

FEDSPEAK FROM POWELL, CLARIDA, WILLIAMS:

There has been a heavy slate of Fedspeak post the October FOMC, which could render the minutes somewhat stale. The influential trio of Powell, Clarida and Williams all continued to sound upbeat on the outlook, repeating key messages from the statement, though Powell’s testimonies also noted the moderate level of vulnerabilities in the financial system, while investor appetite for risk was elevated in some asset classes, though the core of the financial sector appeared resilient. He also warned that the high level of US government debt might restrain the ability of fiscal policymakers to support the US economy in the event of a downturn, and that noteworthy risks to the US outlook still remain, with sluggish global growth and trade developments. Vice Chair Clarida has mentioned that immediate Fed policy was unlikely to change, unless the outlook did (Powell and Clarida both think the outlook is currently favourable). Clarida also does not see cracks in the US consumer, stating it has never been in better shape. NY Fed’s Williams has also been positive on the economy; he did, however, note monetary policy should not get involved with the volatility of trade wars and Brexit, and to instead take a longer view.

FEDSPEAK FROM HAWKS AND DOVES:

The dovish contingent – 2019 voter Bullard and 2020 voter Kashkari – also seem to believe rates are appropriate where they are, with the latter seeing conditions as modestly accommodative. Bullard was pleased with the normalisation of the yield curve, saying it could be a bullish sign for 2020. Bullard also spoke about the Fed being able to take back the insurance rate cuts if the economy improved (and only when businesses adjust to the new trade landscape). The hawks (Rosengren, Mester) were mixed; Rosengren opted to keep rates unchanged at the last meeting as he felt monetary policy was already accommodative, and has expressed concerns of running out of policy room in the event of a negative economic shock. Mester (2020 voter), however, believes current monetary policy is “well calibrated”, and although she would not have opted for a cut, she was sympathetic on the reasoning for one.

CURRENT MARKET PRICING:

Money markets currently price 31bps of FOMC easing through the end of next year (i.e. one further cut from current levels). For the December 2019 meeting, markets do not foresee any adjustment to rates. With the Fed now in data dependency, traders will be looking to the minutes for any clues on the conditions that the Fed would need to see to tweak its data-dependent bias, though it seems there is more risk of a dovish rather than a hawkish pivot, if anything. At the post-meeting press conference, Powell himself said that for the Fed to consider hikes, inflation would have to “runaway” from their target (which he does not foresee). UBS believes the minutes will not hold a discussion on the requirements to resume hiking, stating Powell suggested the bar for a hike would be quite high. Others have noted given the lack of upside risks mentioned by Powell, suggests he appears he is leaning more on the dovish side, suggesting a higher barrier for any hikes than for cuts. UBS believes his words would imply there would not be a hike until 2020 at the earliest (current pricing looks for one 25bp cut by the end of 2020). The bank also observes that Powell continues to focus on risks to the economy, though caveats this with commentary about how risks have subsided recently.

STANDING REPO FACILITY/REPO OPERATIONS:

NY Fed President Williams has said that reserves are now at an ample level, noting that the previous levels did affect market liquidity and sensitivity of interest rates. (NOTE: The NY Fed administers the Fed’s money market operations, and as such, Williams is the authority). In order to maintain ample reserves, the Fed has been conducting overnight and term repo operations. The central bank is also discussing the design and implementation of a Standing Repo Facility, though details are slim, and the instrument is yet to be finalised; any details will be welcomed.

Tyler Durden

Wed, 11/20/2019 – 12:45

via ZeroHedge News https://ift.tt/344rlXz Tyler Durden