Ticking Time Bomb: Is This Powell’s “Subprime Is Contained” Moment?

Authored by Sven Henrich via NorthmanTrader.com,

I’m of the long standing view that Fed chairs have one prime responsibility above all others: Keeping confidence up, and if it requires to sweet talk problems then that’s what it takes.

The often classic quote by Ben Bernanke of “subprime is contained” right before it blew up in everybody’s face being a prime example.

Is the Fed that blind to reality or just on an elaborate marketing mission to ensure that nobody panics and sells stocks? I leave that judgment to the reader.

But I can see differing messaging coming out the Fed when people are in office and when not.

Take corporate debt for example.

Here’s Jay Powell in May of this year sweeting talking and dismissing any concerns:

“Business debt does not present the kind of elevated risks to the stability of the financial system that would lead to broad harm to households and businesses should conditions deteriorate. Moreover, banks and other financial institutions have sizable loss-absorbing buffers,” he said. “The growth in business debt does not rely on short-term funding, and overall funding risk in the financial system is moderate.”

Sweet, no worries then. Odd then that Janet Yellen, no longer in office, feels free to say in essence the exact opposite:

“I have expressed concerns about leveraged lending,” Yellen said during a keynote discussion that was closed to the press. “I do think non-financial corporations have run up, really, quite a lot of debt.”

“What I would worry about is if the economy encounters a downturn, we could see a good deal of corporate distress. If corporations are in distress, they fire workers and cut back on investment spending. And I think that’s something that could make the next recession a deeper recession,” “I have concerns about the deterioration in lending standards that we have seen,” Yellen said. “A large share of it is covenant-lite and some of the explicit ways in which covenants have weakened are a concern to me.”

No worries from Powell, worries from Yellen.

What’s reality?

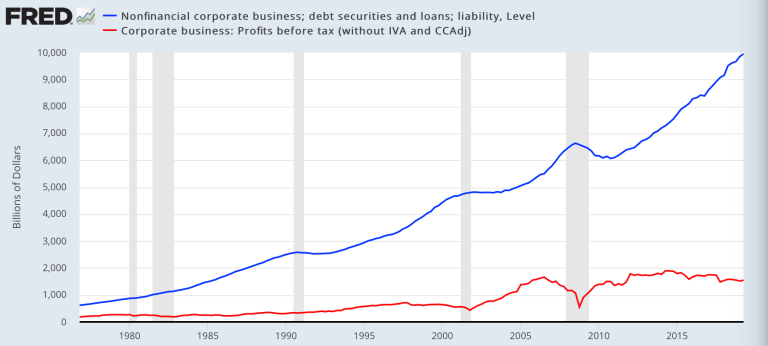

Well, for one corporate debt has increased by 64% in the last 9 years now reaching $10 trillion:

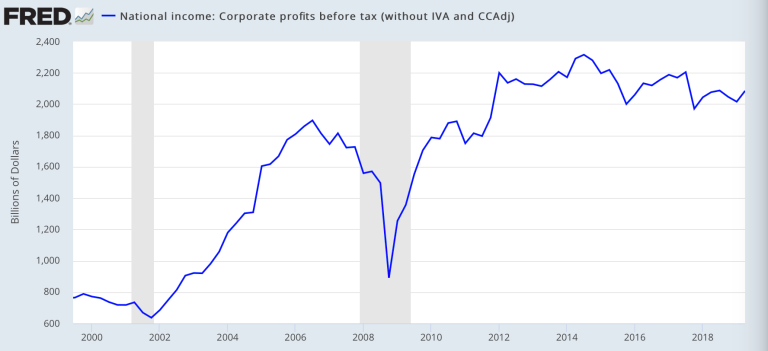

Good thing profits have vastly increased in that time:

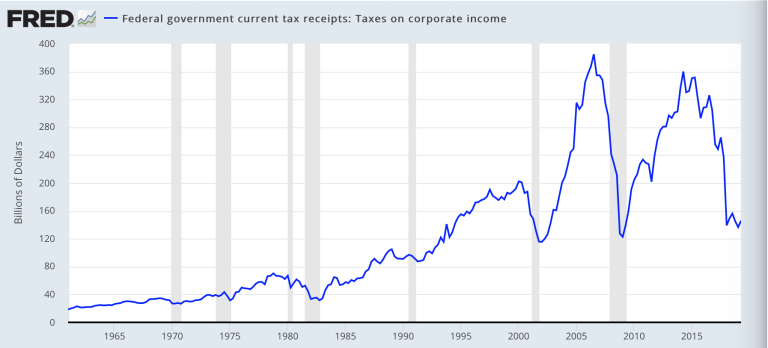

Oh wait, corporate profits have actually peaked in 2014. Well that’s odd, as markets keep racing higher from high to high you’d think there’d be this massive expansion in profits. Well of course not, profit growth peaked last year on the heels of the corporate tax cuts resulting in corporate tax payments collapsing to levels only seen during big recessions:

Ponder this: Corporations now pay roughly the same about of taxes as they did in the mid 90’s when the economy and aggregate profits were much smaller.

Quite the historic deal.

No, we know why stock markets kept rising in 2019: Thanks to Fed intervention:

Goldman admits reality: “With S&P 500 earnings on track for roughly 0 growth from this time last year, solid returns likely would not have been possible without central bank support. Central bank easing accounts for almost all of the price return since the start of the year” https://t.co/Akv3Zll7HL

— Sven Henrich (@NorthmanTrader) November 22, 2019

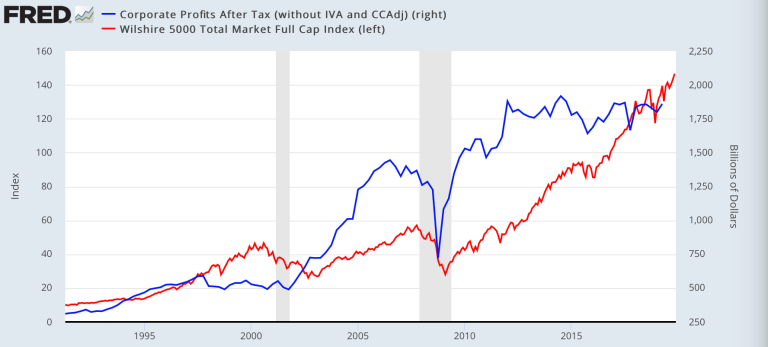

Indeed if you take a look at corporate profits versus the market’s ascent we can observe a large deviation from the actually profit picture:

The above mentioned tax cuts did help the bottom line of course and one can argue the picture looks slightly better when viewed on an after tax basis:

Thanks tax cuts, but the deviation remains. And it remains if you view it through the lens of EPS:

Have #equities got ahead of themselves? S&P 500 Index vs. #earnings per share. pic.twitter.com/sQGfmGtuIS

— jeroen blokland (@jsblokland) November 24, 2019

The aggregate picture is stunning:

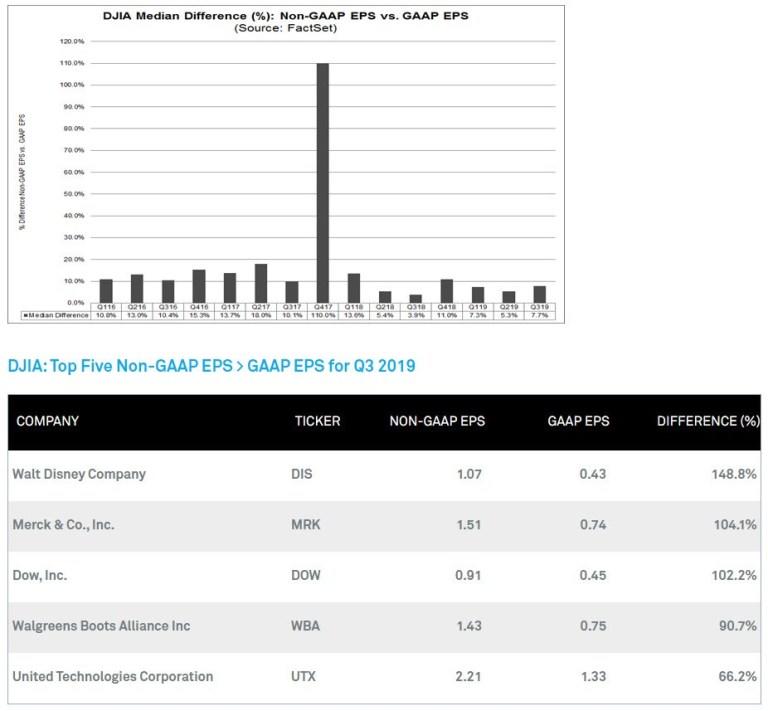

And of course EPS growth is in the eye of the beholder as earnings are regularly overstated via non GAAP versus GAAP accounting:

Not to mention the insidiously deceiving growth illusion created by buybacks.

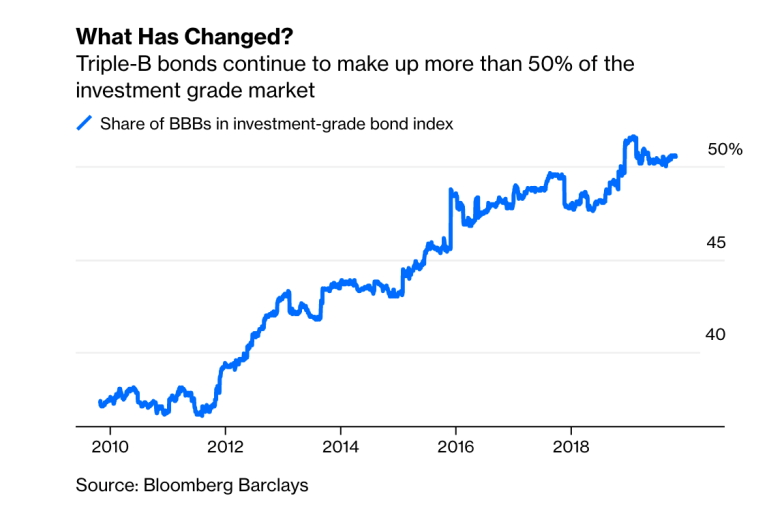

So what you have is a market disconnecting ever farther from the underlying already weakening and overstated earnings growth picture, earnings that require an exorbitant amount of debt expansion to produce with much of the tax cut benefits going toward buybacks while half of the debt expansion is running on BBB fumes:

“The growing universe of triple-B rated US corporate debt — the lowest rung of the higher-quality bond market — has garnered the most attention. At $2.5tn, it is now twice as big as the entire junk bond market beneath it. The hunger for yield has “paved the way for unprecedented erosion in capital structures and credit quality”, Moody’s noted in a recent report.”

Do worry says Janet Yellen, but don’t worry says Jay Powell. The economy is in a good place he says apparently instructing all the Fed speakers to read off the same script:

Sweet. How do they all get on the same page when determining their market communication strategy? Sadly the Fed minutes are void of any such discussions. Must be a different meeting.

Yea, the economy is in a good place:

https://t.co/epTdz8ceiM pic.twitter.com/rRKwgeiWLb

— Sven Henrich (@NorthmanTrader) November 24, 2019

And subprime is contained and corporate debt is not a problem as long as you are Fed chair. It only becomes a problem when you’re no longer Fed chair.

No, corporate debt is a massive problem, it’s a ticking time bomb that millions of workers get to pay for during the next recession. That’s not my hyperbole, no Sir, or have you already forgotten what Janet Yellen already told you?

“if the economy encounters a downturn, we could see a good deal of corporate distress. If corporations are in distress, they fire workers and cut back on investment spending. And I think that’s something that could make the next recession a deeper recession”.

No financial crisis in our lifetime when Fed chair, the next recession could be deeper thanks to extended corporate debt when not Fed chair. Funny that.

She knows and so does Jay Powell, he’s just busy keeping confidence up by telling you everything is fine and dandy. After all that’s precisely why he cut rates 3 times and expanded the Fed’s balance sheet by over $280B in 2.5 months. Cause that’s exactly what you do when the economy is in a good place.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

Tyler Durden

Sun, 11/24/2019 – 14:55

via ZeroHedge News https://ift.tt/37wUNrr Tyler Durden