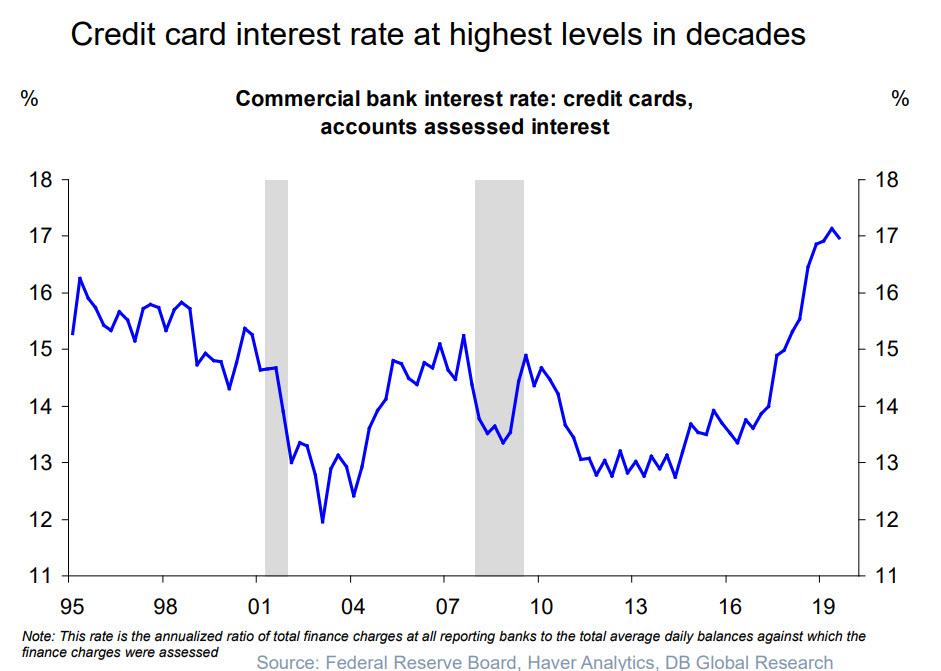

A Funny Thing Happened As The Fed Cut Rates: Credit Card Rates Hit All Time Highs

Something “odd” happened as the Fed prematurely ended its rate hike cycle and cut rates 3 times starting this summer: while banks were quick to trim the interest they pay on deposits to match the Fed’s cuts (and in the case of some “retail banks” like Goldman, even cut ahead of the Fed) they pushed the rates they charge on credit cards to all time highs.

And while we are confident such stalwart defenders of Fed policy as supportive of US consumers (instead of, say, US banks) as Neel Kashkari will be quick to explain how it is that rate cuts have resulted in higher credit card interest rates, and why the Fed is doing nothing to reverse this latest handout from consumers to banks, here are some more charts from Deutsche Bank showing that after carrying the US economy for the past year (as we reported on Friday, consumption account for more than 100% of the GDP growth in Q3), this may soon be ending.

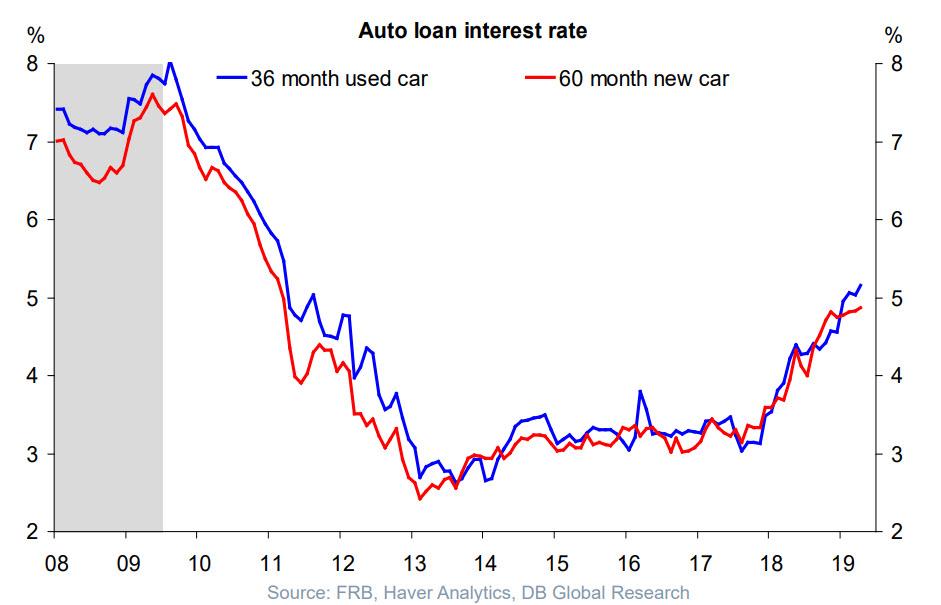

First, it’s not just credit card rates that are surging – so are auto loan interest rates, and while they have yet to hit all time highs, they have risen by a material 2% in 2018 and also are showing no signs of reversing.

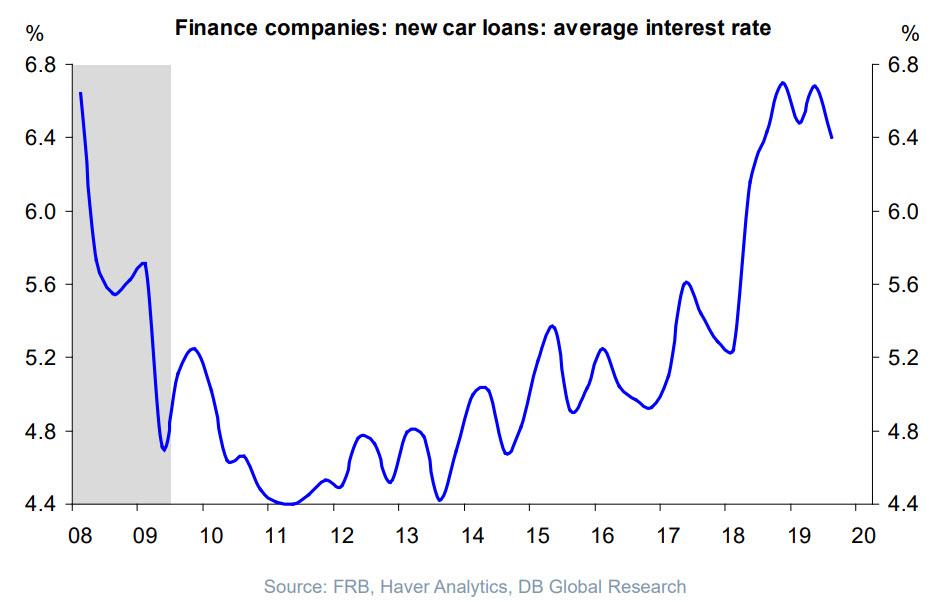

Worse, while bank auto loan rates have yet to hit cycle highs, when it comes to rates charged by finance companies, they are back to levels seen when the Fed Funds rates was about 3% higher.

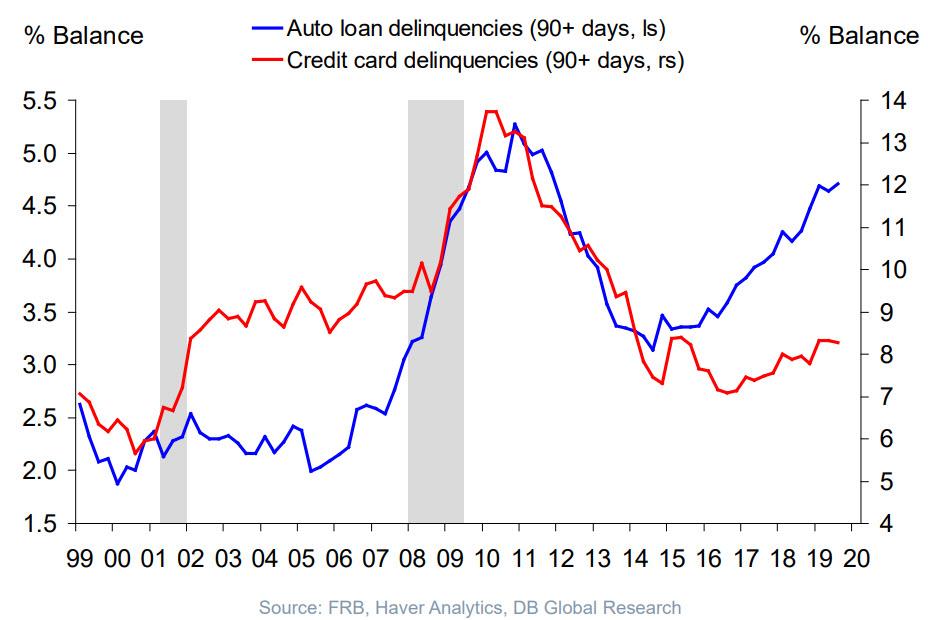

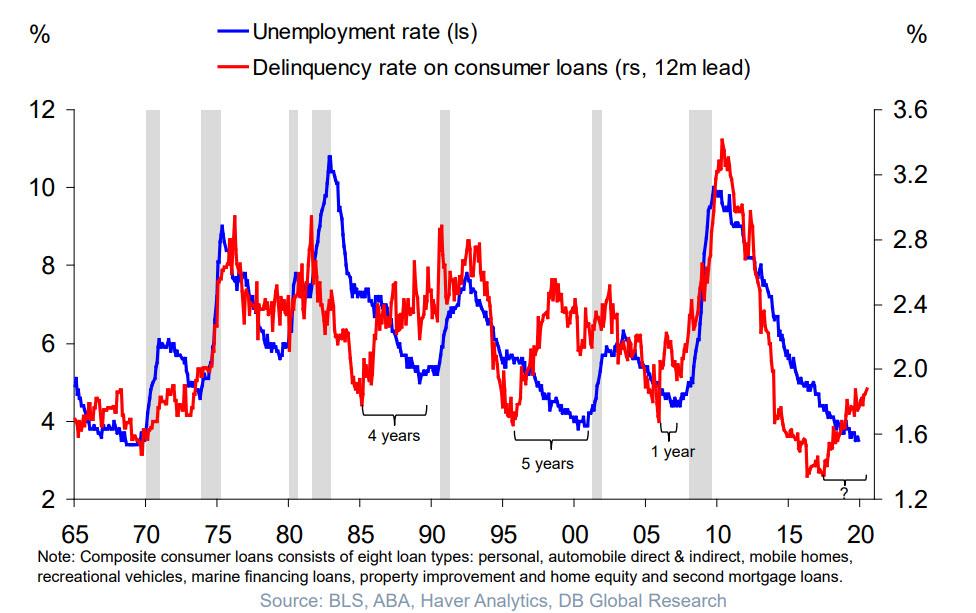

One explanation for the relentless creep higher in rates banks charge consumers is that delinquency rates are also rising, and sure enough, that’s exactly what’s going on, although one would think that the 75bps cut this year would find at least some pass through to end markets. Alas, that is not the case.

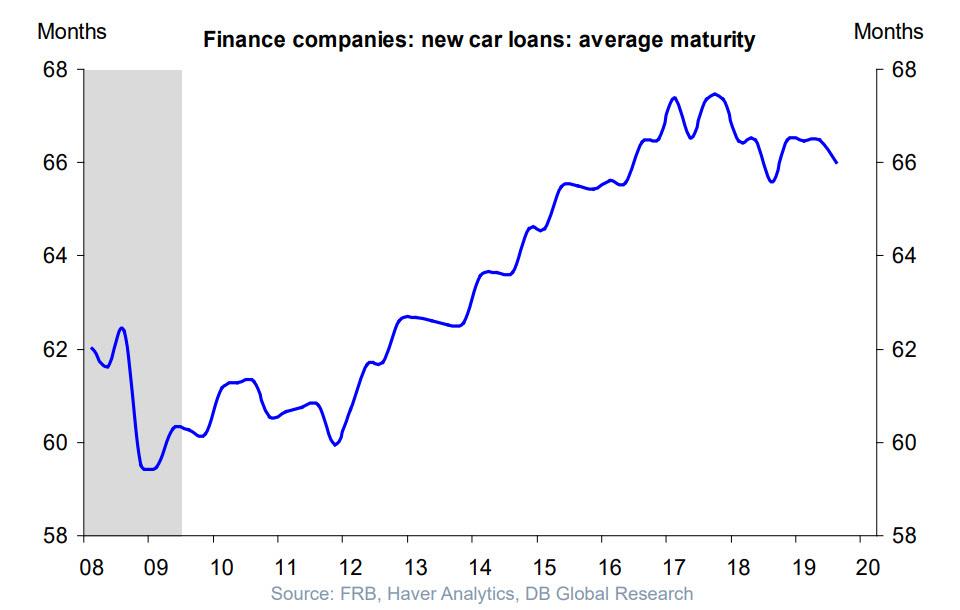

Meanwhile, despite the recent surge in car loan delinquencies which is also fast approaching record levels, finance companies are allowing increasingly broke US consumers to take out ever longer loans and leases in order to make the monthly payments smaller while tacking on mandatory payments to the tail end, which has risen to as much as five and a half years.

And as maturities get ever longer, so total loan sizes rise to new all time highs, allowing OEMs to keep hiking average prices to new records. After all, why comparison shop and look for deals when one can just charge it and worry about the price the next billing cycle, and the next, and the next… with compounding interest.

Shifting away from cars, and looking at the broader consumer loan category, something ominous is taking place here too: after hitting an all time low 3 years ago, the number of defaults has spike, even as the increasingly unreliable and seasonally adjusted unemployment rate remains near all time lows.

Finally, while the big banks – which carefully season and select their portfolios have barely seen their credit card delinquency rates increase, the same can not be said for most US commercial banks that are not among the 100 largest: it is here that the next American delinquency crisis will hit first, because as noted here previously, delinquency rates among America’s small and medium banks are effectively at all time highs.

Tyler Durden

Sun, 12/22/2019 – 19:11

via ZeroHedge News https://ift.tt/2SdEBGq Tyler Durden