S&P Futures Soar Back To All Time High On Viral Cure Optimism

As Bloomberg’s Richard Breslow writes this morning in a note lamenting that there is “little obvious” about this market, “some days it’s best just to let things play out for a little while. Economic numbers that came out overnight haven’t hurt. Very dovish comments by a senior Bank of Japan official. Upbeat comments by the governor of the Reserve Bank of Australia. And then the big one, hopeful comments concerning potential progress in dealing with the virus outbreak. And the market has taken off.“

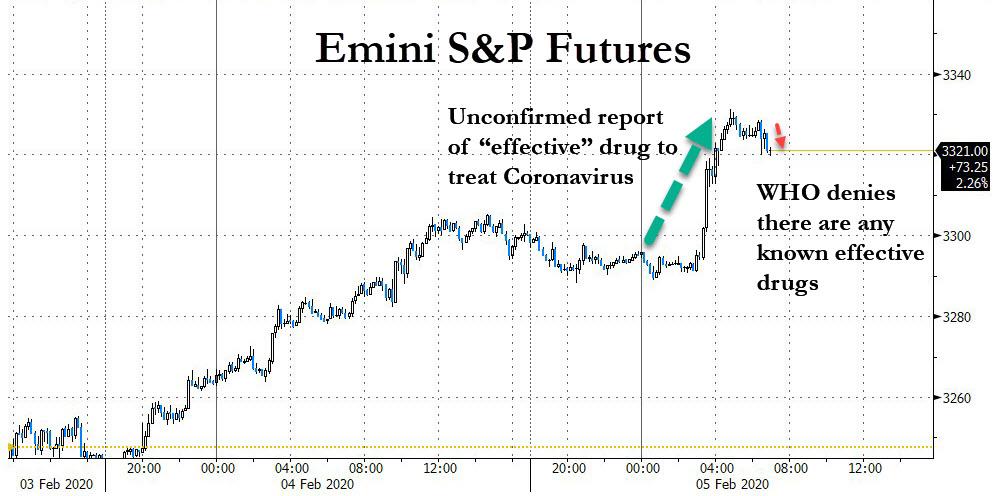

Indeed, at roughly 3:40am ET, futures surged as much as 30 points, rising to 3,335 and surging just shy of the Jan 22 all time high of 3,337.50, after the following Reuters headline hit:

- CHINESE TV: RESEARCH TEAM AT ZHEJIANG UNIVERSITY HAS FOUND AN EFFECTIVE DRUG TO TREAT PEOPLE WITH THE NEW CORONA VIRUS

Even though Reuters itself said it has not confirmed the veracity of the report, it was enough to unleash a case of viral (or is that virus) optimism, with futures filling the gap back to all time highs, as algos bought first and asked questions, well never. And in typical broken market fashion, two hours later, when a WHO spokesperson, asked about a coronavirus treatment breakthrough, said there are no known effective therapeutics against the virus, futures barely dipped, or to summarize Dow futs up 300 point on unconfirmed optimism, and down 50 on reality.

What is notable is that Chinese state media first covered this yesterday but was largely ignored by mainstream media; the report got a second wind this morning today however after traders focused on the fact that over 900 people have recovered from the coronavirus, which some took for evidence the treatment is becoming more effective, while ignoring that the 500 or so deaths reported so far is likely are greatly underrepresented number by China which has been burning the vast majority of casualties to literally eliminate the evidence.

Optimism was also boosted by a separate Sky News report which said U.K. scientists made significant progress for a vaccine by reducing a part of the normal development time from “two to three years to just 14 days”; the scientist added that it will be in animal models by the beginning of next week, and the next phase will be to move from early animal testing into the first human studies, which could happen in “months”, with the report adding that the vaccine will be too late for this current outbreak but it will be crucial if there is another one.though human trials wouldn’t begin for a few months; at roughly the same time news hit that Chinese researchers have applied for a local patent on an experimental Gilead drug that they believe might fight the coronavirus.

“Traders have taken the view that the situation is now more likely to be under control and hopefully the spread of the health crisis will be stemmed,” said David Madden, market analysts at CMC Markets.

But what is the reality on any vaccine? Stated simply, it would take months of trials before anything legitimate got off the ground. In short, nothing that hit overnight provides any indication the world is remotely closer to having an effective means to slowing the current pandemic, but all algos cared about was the optimism that was unleashed by the reports, and lo and behold, we are back to all time highs.

Meanwhile, stocks also rallied on bad news, as expectations of more central bank stimulus lifted world stocks to their highest in more than a week on Wednesday with the MSCI global benchmark rising 0.3%, helping investors look past a mounting coronavirus death toll and policymakers’ concerns for the disease’s economic impact.

The unconfirmed report and the stimulus expectations offset at least partly the news that the virus’s death toll had killed 500 and sickened 25,000.

So as a result of both good and bad news, futures on all US indexes turned sharply higher and Europe’s Stoxx 600 Index rebounded after a string of reports on possible vaccines or treatments for the deadly pathogen. Contracts on the S&P 500 Index climbed as Tuesday’s the surge in tech stocks continued in premarket trading for Apple and Nvidia. Gilead Sciences edged lower after jumping this week on speculation over its antiviral drug.

Data also showed euro zone and UK business activity accelerated last month, though the figures are now meaningless as the surveys were collected before the coronavirus spread much beyond China. The concerns for economic growth were reflected in signals from the Bank of Japan and the Monetary Authority of Singapore that they were ready to ease policy. BOJ Deputy Governor Masazumi Wakatabe pledged not to rule out any option, including lowering already-negative interest rates; meanwhile in Thailand, the central bank unexpectedly cut rates to a record low 1.0% as the economy has been hard hit by the Coronavirus.

“Clearly… all the central banks are ready to act if necessary,” said Justin Onuekwusi, a portfolio manager at Legal & General Investment Management.

Earlier in Asia, stocks notched their first back-to-back daily gain in two weeks and headed for their best two-day gain in almost two months as investors assessed earnings releases in the region and the latest status of the coronavirus outbreak, even as quarantines were set up in the Chinese base of iPhone maker Foxconn, at land borders with Hong Kong, on a cruise ship off Japan and U.S. military bases. The region’s benchmark MSCI Asia Pacific Index jumped as much as 0.8%, with most markets trading in the green. China’s Shanghai Composite Index had its best two-day advance since June, while the ChiNext Index rose another 3% in a continued rebound after the post-holiday slump. Japan’s Topix index advanced as Mitsubishi Corp. and Itochu Corp. climbed after reporting quarterly earnings that beat estimates. China (PBOC) is also likely to lower its key rate on Feb. 20, sources told Reuters. while Thailand unexpectedly cut interest rates.

In rates, 10-year Treasury yields rose three basis points to 1.637% while German yields rose 4 bps to a one-week high. Sovereign bond curves across Europe bear steepened, though Treasuries were harder hit by the sell-off.

In FX, the dollar was roughly unchanged even as 10Y yields rose, while the Australian dollar led gains in G-10; the franc led declines against the greenback with the yen holding little changed after erasing an earlier gain. The pound extended gains after better- than-forecast services U.K. PMI, which also led money markets to price out expectations for BOE rate cuts to less than 25bps

In commodities, crude oil headed for its first gain in six sessions in New York trading: Brent crude also bounced 2.5%, after losing 16% since Jan. 21. It was supported too by expectations OPEC and its allies would cut output to offset lower demand.

Economic data include mortgage applications, trade balance and Markit services PMI. Qualcomm, Boston Scientific and General Motors are due to report earnings.

Market Snapshot

- S&P 500 futures up 0.8% to 3,324.50

- MXAP up 0.8% to 168.04

- MXAPJ up 0.8% to 544.32

- Nikkei up 1% to 23,319.56

- Topix up 1% to 1,701.83

- Hang Seng Index up 0.4% to 26,786.74

- Shanghai Composite up 1.3% to 2,818.09

- Sensex up 0.9% to 41,169.64

- Australia S&P/ASX 200 up 0.4% to 6,976.05

- Kospi up 0.4% to 2,165.63

- STOXX Europe 600 up 1% to 422.48

- German 10Y yield rose 2.6 bps to -0.373%

- Euro down 0.05% to $1.1038

- Brent Futures up 3% to $55.57/bbl

- Italian 10Y yield unchanged at 0.785%

- Spanish 10Y yield rose 2.6 bps to 0.295%

- Brent Futures up 3% to $55.57/bbl

- Gold spot down 0.01% to $1,552.78

- U.S. Dollar Index unchanged at 97.96

Top Overnight News from Bloomberg:

- The death toll from the coronavirus outbreak climbed toward 500 as confirmed cases worldwide almost 25,000. Hong Kong announced plans to quarantine travelers coming from the mainland, while thousands remained stuck on cruise ships

- Chinese researchers have applied for a local patent on an experimental Gilead Sciences Inc. drug that they believe might fight the novel coronavirus outbreak

- The euro area’s private sector expanded at a faster- than-anticipated pace in January, providing a foundation for economic growth to accelerate in the course of the year, with a composite Purchasing Managers’ Index rising to the highest since August

- The Bank of Thailand cut its benchmark interest rate to a record low as the coronavirus outbreak, a stalled government budget and bad drought imperil economic growth, while most other monetary policy makers have stuck to expressing concern and signaling a willingness to act on risks from the virus. Australian central bank Governor Philip Lowe reinforced expectations that policy makers will refrain from more interest- rate cuts

- Poland became the first emerging-market sovereign to get paid for borrowing in euros via a syndicated bond deal

- OPEC+ officials gathered in Vienna for a second day of debate on the impact of the coronavirus, a process that could result in an emergency ministerial meeting where Saudi Arabia would push for an oil-production cut

Asian equity markets were positive across the board as the global rebound filtered through to the region after having underpinned the major indices on Wall St and pushed the Nasdaq to a fresh record high. ASX 200 (+0.4%) and Nikkei 225 (+1.0%) were both higher after taking impetus from stateside peers with tech and commodity-related sectors the outperformers in Australia but with gains limited by resistance at the 7000 level and with gold miners suffering as investors shunned safe-havens, while gains in Tokyo were exacerbated by a weaker currency. Elsewhere, Hang Seng (+0.4%) and Shanghai Comp. (+1.3%) notched respectable gains as the bargain hunting resumed in the mainland, unfazed by softer Caixin Services and Composite PMIs, continued increases in the number of coronavirus cases and the PBoC skipping open market operations in which it noted that current liquidity is ample and can fully meet market demand. Finally, 10yr JGBs extended on this week’s pullback from the 153.00 level and following the bear-steepening in USTs in which T-notes retreated below 131.00 as the gains across stocks sapped safe-haven demand.

Top Asian News

- Singapore Dollar Tumbles After MAS Flags Scope for Decline

- Hong Kong Will Quarantine Travelers Coming From Mainland China

- China Virus Shuts Airbus Plant, Hitting Narrow-Body Jet Output

- Thailand Cuts Interest Rate as Virus Outbreak Hurts Economy

European equities are firmer across the board [Eurostoxx 50 +1.0%] following a tame open, as risk sentiment was bolstered by unconfirmed reports that a research team at a Chinese university has found an “effective” drug to treat people with Coronavirus. Moreover, reports via Sky News suggested that a team of UK scientists reduced the normal development timeframe for a vaccine to 14 days from 2-3 years, but crucially, the report noted that the “vaccine will be too late for this current outbreak, but it will be crucial if there is another one.” Nonetheless, bourses have held onto gains with sectors staging a complete turnaround from the open. European sectors now largely reflect risk appetite with defensives lagging cyclicals (ex-healthcare). Movers this morning are mostly orientated around earnings – with DAX heavyweight Siemens (+0.5%) initially opening with earnings-induced losses in excess of 1.5% before conforming to the overall gains in the German bourse. On the flip side, Imperial Brands (-7.8%) rests at the foot of the pan-European index following a profit warning in which it now forecasts a circa 10% drop in H1 profits. Other earnings-led movers include Smurfit Kappa (+7.8%), Barratt Developments (+3.3%), Danske Bank (-0.7%), Novo Nordisk (+1.5%) and Infineon (+9.0%). Elsewhere, Adidas (+1.0%) and Puma (+0.2%) shares opened lower to the tune of around 2% after US peer Nike noted that the coronavirus outbreak is expected to have a “material impact” on its Chinese operations. Adidas’ CEO also echoes some comments from Nike in which it sees a negative impact on its Chinese business, but stopped short of giving details or extent of impacts.

Top European News

- Vodafone Warns of 5G Delays if Huawei’s Share Capped Beyond U.K.

- U.K. Services Rebound More Than Expected in Post-Election Bounce

- ABB Says Coronavirus Threatens China’s Already Fragile Recovery

- Romania’s Orban Faces Confidence Vote He Doesn’t Mind Losing

In FX, the Dollar is holding up firm in the face of a marked pick-up in sentiment surrounding China’s coronavirus based on media headlines suggesting that scientists and researchers may be closer to finding a vaccine than previously anticipated. The reports have boosted the YUAN for obvious reasons, with Usd/Cnh retreating from around 7.0100 to sub-6.9750 and below the 200 DMA (6.9905) not to mention the PBoC’s 6.9823 overnight Usd/Cny mid-point fix. However, the Greenback is forging gains at the expense of safer havens, like the YEN, EURO, SWISS FRANC and GOLD, with the DXY clinging to 98.000 and on course to keep its head above a key Fib retracement level (98.011), barring any bad miss via ADP, final Markit PMIs and/or the non-manufacturing ISM.

- JPY/CHF/EUR/XAU – As noted above, all weaker vs the Buck and overall on a broad unwind of FTQ premium/positioning, as Usd/Jpy climbs further above 109.50, Usd/Chf reclaims 0.9700+ status, Eur/Usd retreats from near 1.1050 to just under 1.1025 and Usd/Xau retests support circa Usd 1550/oz after briefly tripping stops on a break of Tuesday’s low (Usd 1549) to trade a whisker below Usd 1548.

- AUD/GBP/NOK/SEK/NZD/CAD – The Aussie has extended post-RBA gains with the aid of commentary from Governor Lowe reinforcing a wait-and-see stance on top of the more encouraging Chinese outbreak news. Aud/Usd has now climbed firmly back above 0.6750 to revisit late January peaks (0.6777), while Aud/Nzd has rebounded over 1.0400 to the detriment of Nzd/Usd that has not been able to regain a sure grip on the 0.6500 handle in wake of somewhat mixed NZ jobs data. Conversely, another handsome UK PMI beat vs consensus has boosted Sterling across board, as Cable hovers close to best levels of the wtd (1.3070) and Eur/Gbp sub-0.8450 following rather contrasting Eurozone services PMIs. Elsewhere, the Scandi Crowns have rebounded alongside risk appetite and the Norwegian Krona especially fuelled by a strong recovery in crude prices whereas its Swedish counterpart is being partially hampered by poor hard data offsetting an upbeat services PMI. Similarly, the Loonie is not deriving that much from the aforementioned bounce in oil ahead of Canadian trade data and a speech from BoC’s Wilkins, albeit with Usd/Cad nearer the base of a 1.3299-62 band.

- EM – Most regional currencies have tracked Yuan and high-beta peer appreciation, but the SGD and THB have both been subject to dovish MAS and Thai CB vibes in the form of guidance and an unexpected 25 bp ease respectively, while the Try is still on the defensive due to geopolitical factors. Conversely, SA Government backing for COSATU proposals to cut Eskom debt have given the Zar and extra fillip.

In commodities, WTI and Brent futures have extended on overnight gains amid the aforementioned reports of seemingly constructive coronavirus headlines. WTI and Brent front-month futures hit fresh 2020 lows (of ~49.30/bbl and 53.70/bbl respectively) in light of a larger than expected headline API inventory build (+4.18mln vs. Exp. +2.8mln). Thereafter, prices clambered off worst levels before piggybacking on the virus headlines which, if true, could significantly improve the demand outlook for the complex. Elsewhere, OPEC’s JTC will convene for the second day of discussions later today after the technical committee reportedly did not discuss production cuts yesterday but will revisit the topic, according to delegates who noted it studied between 200-400k BPD impact on oil demand from the coronavirus. Reports also note that OPEC numbers suggest a circa 400k BPD demand impact for around six months from the coronavirus, although these forecasts are highly contingent on how long the epidemic lasts alongside any prolonged effects. Analysts at ING note that a 500k BPD of additional OPEC cuts in Q1 and a rollover of current cuts in Q2 (through to end-June) should be almost enough to balance the oil market, assuming the OPEC figures are correct and factoring in supply disruptions in Libya. Next up, traders will be eyeing the weekly DoEs with headline crude forecast to print a build of 2.831mln barrels, according to Reuters Estimates. Elsewhere, spot gold conformed to the overall risk appetite as prices briefly dipped below 1550/oz before encountering stops just below the figure. Copper continues yesterday’s sentiment-led rebound as the red metal almost wipes out a bulk of last week’s losses.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 7.2%

- 8:15am: ADP Employment Change, est. 158,000, prior 202,000

- 8:30am: Trade Balance, est. $48.2b deficit, prior $43.1b deficit

- 9:45am: Markit US Services PMI, est. 53.2, prior 53.2; Markit US Composite PMI, prior 53.1

- 10am: ISM Non-Manufacturing Index, est. 55.1, prior 55

DB’s Jim Reid concludes the overnight wrap

With coronavirus fears continuing to ease, the last 24 hours have been kind to risk assets once again. The latest numbers show 24,324 cases and 490 deaths as of this morning versus 20,438 and 425 this time yesterday but the fact that there appears to be a slowing in independent incidents in countries outside of China and a slowing in the rate of transmission in cases outside of Wuhan province appear to be making investors more comfortable for now. While this could change, our conclusion was that these were the conditions that needed to be satisfied for markets to feel more at ease following DB’s client call with a virus expert on Monday. For those that missed it the replay details can be found here (link here).

As for markets, coming off the back of 8 sessions where by the S&P 500 flipped between gains and losses, yesterday’s +1.50% return means the index is up +2.23% in the last two sessions. The NASDAQ also rallied +2.10% yesterday – a new record high and the biggest gain since August – and the DOW +1.44% which means all three indices are back in positive territory YTD again. Also worth noting was the +4.11% surge for the NYSE FANG index meaning the index is up an impressive +9.10% in the last two sessions. Even copper – which had been on a 13-session losing run – finally joined the party, rising +1.40%.

At a micro level it was the incredible +13.73% surge for Tesla which really grabbed the spotlight yesterday though. That means the stock is up +36.35% over the last two sessions and 112% this year already. More impressive still is the 435% rally from the 2019 lows. With a market cap of nearly $160bn that also puts the company in between the nominal GDPs of Ukraine and Kazakhstan. For what it’s worth Tesla isn’t in the S&P 500 but a quick look at the index would mean it would be around the 50th largest and would have added roughly 13pts to the index this year. Incidentally, the electric car maker may soon be eligible to join the index now that it is close to posting four straight quarters of profits – the only requirement the company was short.

The more macro focus yesterday was the results of the Iowa caucus and following “inconsistencies in the reporting” we’ve finally had an update overnight. At the time of writing, 71% of the vote has been made official. Currently South Bend Mayor Peter Buttigieg is leading among delegates with 26.8%, followed closely by Senator Sanders with 25.2%, then Senator Warren with 18.4%, and Vice President Biden at 15.4%. This would be a very disappointing result for Biden, who came into the night polling in second place. Mayor Pete became the winning Moderate and while the results are not final, they stand to show the current break in the Democratic primary between the Left (Sanders + Warren = 43%) and the Moderate (Biden + Buttigieg + Klobuchar = 56) wings. Markets are not likely to react strongly to the democratic primary until you see the more Left candidates’ numbers climb higher.

Prior to this President Trump addressed the nation in his 2020 State of the Union, however there wasn’t a huge amount to report. Trump previewed his 2020 general election pitches; touting a strong economy on the back of deregulation, renewed trade deals, and lower corporate taxes, promising continued focus on immigration reforms, and pushing plans on health care changes. Staying with Trump, yesterday Gallup’s latest approval rating put the President at 49%, which is the most since he took office.

Back to markets and a quick glance at our screens this morning shows the positive momentum has continued into Asian markets with Chinese bourses leading the advance – the CSI (+1.13%), Shanghai Comp (+1.25%) and Shenzhen Comp (+2.63%). The Nikkei (+1.42%), Hang Seng (+0.47%) and Kospi (+0.58%) are also making gains. In FX, the Singaporean dollar is down -0.75% this morning as the country’s central bank said that it sees room for more easing. Elsewhere, futures on the S&P 500 are down -0.12% and Brent crude oil prices are up +1.30% overnight even as Saudi Arabia’s push for deeper output reductions to combat the drop in consumption received resistance by Russia. As for overnight data releases, China’s January Caixin services PMI came in at 51.8 (vs. 52.0 expected) bringing the composite to 51.9 (vs. 52.6 expected).

Looking ahead to today, whether the positive risk momentum continues may depend on the data. Of particular note are the ISM non-manufacturing and ADP employment change prints. The consensus expectation is for the headline in the former to tick up slightly to 55.1 however it’s the employment component which will also be watched closely given payrolls is due at the end of the week. Our economists have highlighted that this series was up a little over three points in December from its September low of 51.7. Thus, further improvement would be a positive sign given that the services sector accounts for nearly 84% of private payrolls. With respect to the ADP employment survey, it has missed the initial BLS prints over the past couple of months by fairly wide margins. Market participants may therefore want to discount somewhat its signal.

Back to yesterday where, in other markets, there was also a decent bounce back for European equities where the STOXX 600 rallied +1.64%. More interesting were some of the comments at a corporate level regarding the impact of the coronavirus. Oil giant BP suggested that one-third of global oil demand is under threat while Carlsberg mentioned that it’s breweries in China remain closed. Pandora also flagged the risk to its lucrative Asia business. Adding to these comments, one of the key Apple suppliers in China, Hon Hai, slashed its sales growth forecast range overnight to 1% – 3% (from 3% – 5% earlier). Walt Disney also said overnight that it expects the Shanghai park closure alone to reduce profits in the current quarter by $135m, assuming it is shuttered for two months, while the loss from closing of the Hong Kong park would likely add another $40m. In bond markets yesterday the risk-on sentiment saw yields move sharply higher. Indeed 10y Treasury yields backed up +7.2bps while 10y Bunds were +4.3bps higher. Brent and WTI oil retraced over 2% intraday gains to finish down -0.90% and -1.10% respectively as demand concerns mount while Gold edged down -1.31%. In credit, US HY spreads finished 11bps tighter.

In other news, yesterday’s data was mostly an afterthought in the US. The final core capex orders reading was revised up one-tenth to -0.8% mom while durable goods ex transport were unrevised at -0.1%. Meanwhile, factory orders were reported as rising +1.8% mom.

Finally, to the day ahead, where this morning the focus will be on the remaining PMIs in Europe with final January services and composite prints due. Away from that we’re due to get December retail sales for the Euro Area while in the US the PMIs are due along with the January ISM non-manufacturing, January ADP report and December trade balance. Elsewhere, the ECB’s Guindos, Perrazzelli, Lane and Lagarde are all due to speak – the latter in Paris at 12.15pm GMT, while the Fed’s Brainard speaks this evening albeit on payment innovation. As for earnings, Merck, Glaxo, Siemens and General Motors are among the highlights.

Tyler Durden

Wed, 02/05/2020 – 07:49

via ZeroHedge News https://ift.tt/2ukFovD Tyler Durden