BMO: The Biggest Risk Is Not The Crash, But How Long Asset Prices Remain At Current Levels

Less than a week after Powell panicked, and cut rates by 50bps, sparking an even broader market panic as traders freaked out over what Powell may (or may not) know, stocks suffered their biggest crash since the financial crisis, on a double whammy of crashing crude prices and growing coronavirus concerns. Only this time, Powell did nothing.

According to BMO, the Fed chair has apparently learned a few lessons from his first emergency rate cut:

- One-and-done is hard to do,

- Risk assets don’t respond positively to every dovish impulse, and

- capitulating early isn’t necessarily the safest strategy.

Or, as BMO’s Ian Lyngen puts it, “the time-tested monetary policy wisdom goes: gotta know when to hold’rates, know when to ease’em, know when to walk’em back, and know when you’re done. They’ll be time enough for splainin’ when the cycle’s done.”

Unfortunately, the cycle’s countdown is almost up.

But going back to Powell’s market reaction function, this time the Chair has taken a markedly different tact this week versus last. Ironically, by doing nothing and not giving into calls for another 50 bp ease in response to the leg lower in domestic equities and the downdraft in the global energy complex, the Fed Chair may have boosted market confidence as “investors took some solace in the implied confidence in the current monetary policy stance communicated by the FOMC’s inaction.”

Which is not to say the market didn’t crash, it did… but it could have been even worse.

To be sure, triggering the circuit breakers in the S&P 500 was a milestone for the coronavirus – although as BMO admits, “certainly not a positive one in the broader context of how the market might have otherwise interpreted the Fed’s efforts to ease financial contagion fears.” Which is why the next few trading sessions will be particularly informative as to investors’ willingness to wait until next Wednesday for another installment of policy accommodation.

It would be folly to attempt to assign causation over correlation between the stabilization in risk assets and the passage of the morning without any official FOMC unscheduled announcement; nonetheless, the respite from declining risk assets after the earlier extreme surely offered solace to the Committee.

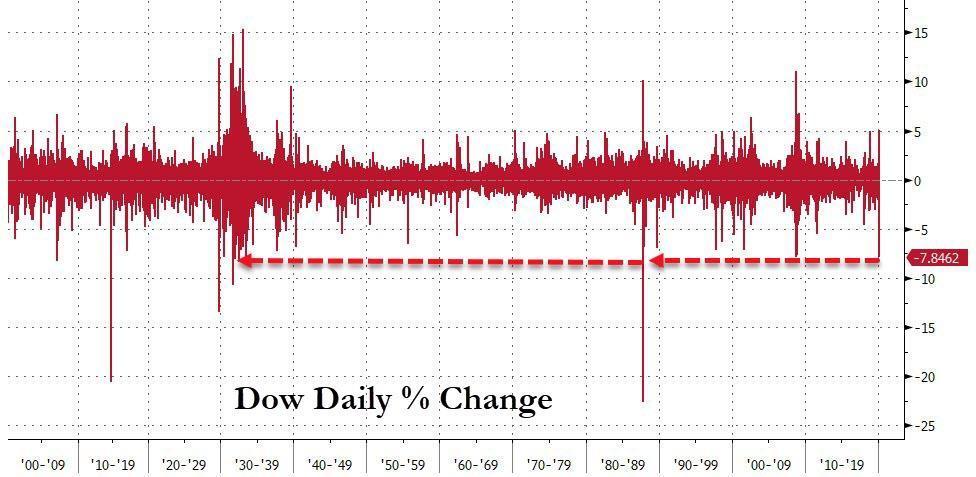

That’s one way of putting it. Another is that we just had a record point drop in the Dow, and S&P future that was halted for hours, and just barely skirted the biggest percentage change in the market in history.

And then there’s rates.

With 2-year yields at 38 bp, 10s at just 50 bp, and 30s below, gulp, 90 bp (after touching 70 bp overnight) the best phrase to characterize the tone in the market is ‘sticker shock’, and as BMO puts it, “the first 50 bp leg of this year’s drop in 10-year rates was eye-opening, but the last 100 bp was jaw-dropping.” The initial move took many by surprise, even if it conformed to a more bond bullish narrative, but “the repricing of 30-year yields below 1.0% was paradigm shifting, to put it mildly.”

Conversations have shifted from postulating whether or not the move has been overdone, to considering which sectors will be hardest hit by the new economic reality. Suffice it to say, uncertainty doesn’t bode well for any willingness to catch the proverbial falling knife.

Unfortunately, as Lyngen notes, between concerns about the credit implications for the high yield market from the energy sector and the broader reaching emerging market implication from sub-$35 crude, there are few bright spots save the spinning-up of the refi-machine (that’s the whirring sound in the background). That said, even the most direct transfer of lower rates to consumer spending will likely take months given capacity concerns on the origination side, to say nothing of an understandable reluctance on the part of lenders to rebase borrowing costs lower if 50 bp 10s could be an anomaly.

So putting today’s historic move in a bigger context, BMO cautions that the biggest risk (and the one undoubtedly troubling the FOMC) isn’t that the price action is overdone, but instead how long rates and asset prices can remain at current levels. Indeed, if prices are too depressed for too long, BMO’s dire conclusion is that “it will become self-fulfilling by running highly leveraged energy producers into insolvency, undermine other related sectors, and eventually flow through to the labor market shaking consumer confidence.“

And as the Canadian banks points out further, it’s once sentiment is hit that attention quickly turns toward the pace of consumption – this will ultimately be the origin of any recession in the US. Of course, long before this, other global central banks will have an opportunity to follow the Fed’s lead in providing additional accommodation. The first such opportunity will be on Thursday, when ECB holds its meeting, and it will be critical to see how aggressive Lagarde is willing to be in the face of so many unknowns.

Tyler Durden

Mon, 03/09/2020 – 18:25

via ZeroHedge News https://ift.tt/2TSno4A Tyler Durden