Can Europe’s Fragile Economy Withstand Another Shock?

Submitted by Caroline Grady of MacroHive

The European economy is grinding to a halt. Fourth quarter GDP growth slowed to the lowest for almost seven years, and supply-side disruption from the coronavirus and new regulations in the auto sector will compound the weakness.

We expect activity to slow further before any sustained rebound sets in. Meaningful fiscal stimulus appears unforthcoming, and further support from monetary policy will be limited given policy is already close to extremes. Consumer spending, the mainstay of the economy, can only do so much to fend off a difficult external environment and the disruptive structural change in autos.

Euro Area Economy Already Close to Stalling in Q4

Thawing US-China trade tensions appears so far to have had no discernible impact on Europe’s trade-orientated economy. The German manufacturing recession deepened in the fourth quarter, and any renewed optimism on trade has been firmly outweighed by worries over the impact of the coronavirus. Moreover, while US-China tensions may have eased, trade policy uncertainties remain – from the lingering threat of auto tariffs to the more recent announcement of increased tariffs on European aircraft, effective as of March.

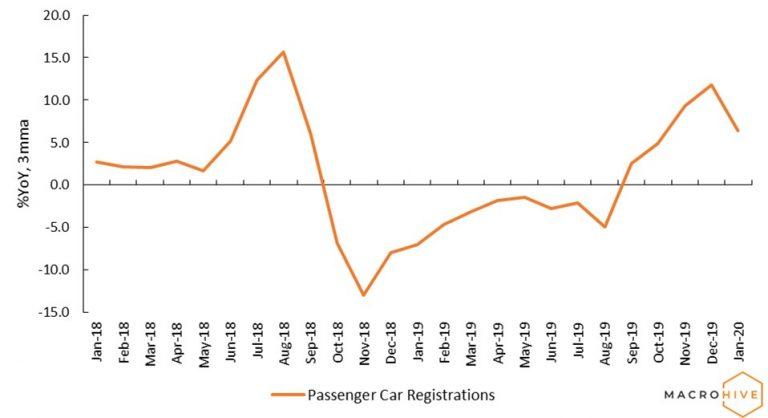

At just 0.1% QoQ in the fourth quarter, Euro area GDP growth was the slowest since Q1 2013. The German economy stalled due to trade and manufacturing weakness, and both France (-0.1%) and Italy (-0.3%) contracted with strikes, inventory run-down, and bad weather all playing a role. Euro area IP is contracting sharply, down -4.1% YoY in December and -2.8% for Q4, marking 14 consecutive months of shrinking output. The earlier improvement in the auto sector has also reversed, with new emissions-based taxes in place as of January triggering a 7.5% YoY decline in new passenger car registrations. Some of this reflects a payback from the very strong December readings as consumers bought cars ahead of the tax change. But German passenger car production is now at its lowest level in more than 20 years and unlikely to improve anytime soon.

Last year’s manufacturing weakness could finally be spilling over into the service sector with Euro area retail sales showing the largest MoM drop in December since 2011. Given consumer spending has been the main driver of Euro area growth in recent quarters, continued weakness in retail sales could trigger a significant shift in growth projections. It would raise questions on the continued resilience in the labour market. On the surface this looks robust, with the unemployment rate remaining the lowest for more than a decade at 7.4%, and employment almost 4% above the pre-crisis peak. Any repeat of December’s higher-than-expected increase in German unemployment claims would bode poorly for any pickup in growth in the coming quarters.

Initial Survey Data Points to a Pronounced Impact From Coronavirus

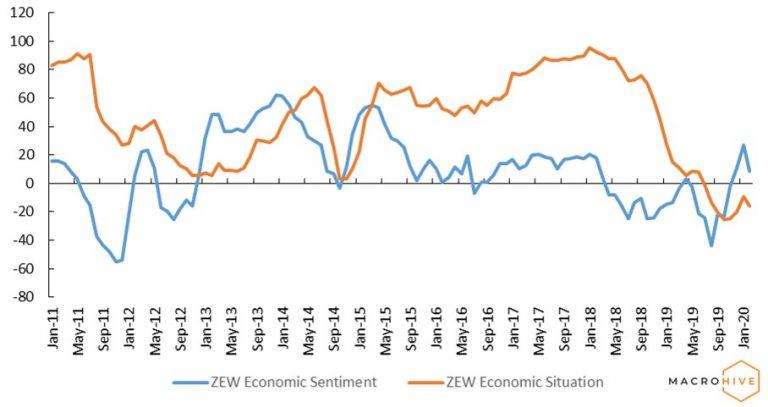

With the Euro area expansion teetering on the brink, a pronounced hit from the coronavirus could well tip the economy into something close to recession. However, the real economy impact will take some time to play out (both in China and globally), leaving survey data as the best gauge of the likely impact. This week’s Zew survey in Germany suggests the hit could be significant. Sentiment dropped sharply and expectations for export industries were badly hit, particularly given the earlier reported decline in manufacturing orders. The flash PMI releases due at the end of the week are also expected to bring an end to the earlier modest improvement in the manufacturing malaise seen through late 2019.

The combination of weaker Chinese demand for German goods, possible disruptions to German supply chains due to Chinese production shutdowns, and weaker demand in other export markets hit by the coronavirus disruption could well provide the fatal blow to the meagre growth in the Euro area economy. At a minimum it suggests that the economic environment is set to deteriorate before improving, particularly as this comes on top of the structural headwinds from the shift in the auto sector and the already precarious state of the manufacturing sector more broadly.

Forecast revisions are concentrated on China for now with a baseline that the impact of the virus will be contained in Q1 and the economy plays catch-up in Q2. Without concrete evidence of the impact in China or the global supply chains, it is impossible to quantify the effect on Germany or the Euro area more broadly. And for now, the assumption of a recovery in global trade volumes and a modest acceleration in global growth remains in place from the IMF and others.

Policymakers Must Stand Ready to Act

Despite still-sanguine forecasts, Europe’s policymakers will be vigilant. Monetary policy cannot offset the impact of a supply shock, but it can provide some boost to growth and inflation should the economy be on the verge of recession. The ECB will likely consider another rate cut and larger monthly QE purchases in the coming months if the data continue to deteriorate. On the fiscal side, it might take a recession for Europe to finally enact some meaningful budget expansion.

Tyler Durden

Mon, 03/09/2020 – 03:30

via ZeroHedge News https://ift.tt/2wJ9t8N Tyler Durden