S&P Futures Rebound As Oil Buyers Emerge

&P futures rebounded alongside European and Asian stocks on Wednesday as oil pared its recent historic losses and upbeat quarterly earnings reports lifted investor sentiment following a two-day selloff due to a record crash in oil prices, even as companies warned of more pain in the coming months. Treasurys and the dollar dropped while gold gained, rising above $1700.

Emini futures climbed after the cash index dropped more than 3% a day earlier, when investors shrugged off the progress of a fresh relief package to counter the economic hit from the coronavirus. The Stoxx Europe 600 Index rose broadly in the wake of Tuesday’s slump.

Earlier in the session, Asian stocks gained, led by energy and communications, after falling in the last session. Markets in the region were mixed, with India’s S&P BSE Sensex Index and Jakarta Composite rising, and Japan’s Topix Index and Australia’s S&P/ASX 200 falling. The Topix declined 0.6%, with Istyle and Financial Products Group falling the most. The Shanghai Composite Index rose 0.6%, with Junzheng Energy and Ningbo Construction posting the biggest advances

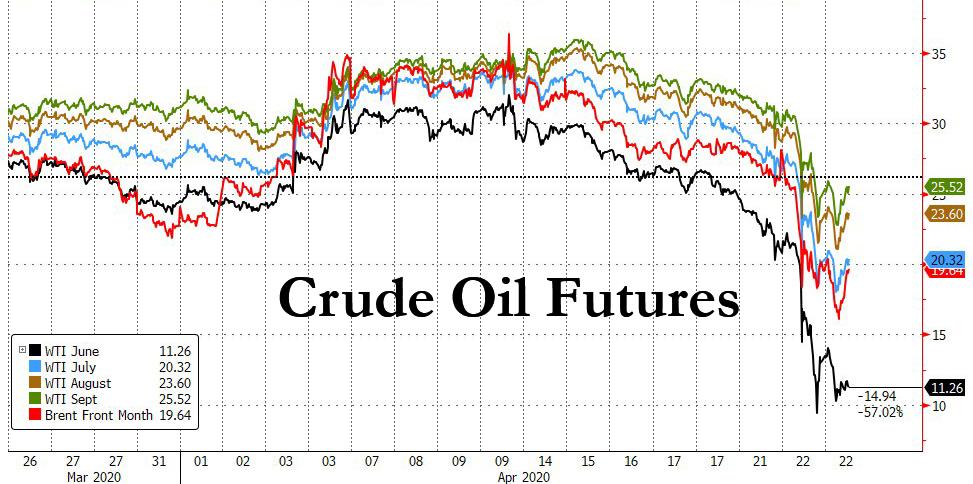

The S&P 500 index fell nearly 5% in the first two days of the week as May WTI contracts plunged below zero for the first time ever, and the benchmark Brent hovered near 1999-lows, triggering alarm about the hit to the global economy from a near halt in business activity.

Texas Instruments headed higher in thin premarket trading as it reported better-than-expected first-quarter results and said a strong inventory allowed it to be prepared for the disruptions caused by the pandemic. Netflix deemed a “stay-at-home” stock as the wide restrictions boost demand for online streaming services, more than doubled its own projections for new customers in the first quarter. However, its shares fell 2% as the company failed to translate the subscriber surge into additional revenues, while forecasting a weaker second half if the lockdown measures were to be lifted. Chipotle reported soaring digital and home delivery sales and said it had enough cash and liquidity to get through the next year.

Trader attention remains glued to oil, with Brent crude erasing a tumble that reached as much as 17% overnight, while West Texas oil also pared most of its slide, even though the June contract was trading just above single digits.

Yesterday, OPEC Delegates discussed the oil market crisis within a conference call; although the call was reportedly not designed to make a new oil decision and they were said to consider a May 10th meeting for further production cuts. Furthermore, Saudi, UAE, and Kuwait did not take part in the call and a delegate noted that OPEC+ members will be unable to start production cuts earlier because April’s oil production is already committed for export contracts. Meanwhile, the Iraq Energy Minister said OPEC+ could take additional steps to absorb the oil surplus but added that taking further measures by producer countries depends on global market development and compliance by other OPEC+ and other non-member producers with the oil cut deal. Russia again downplayed the gravitas of the oil market situation. Elsewhere, the fallout from the Texas Railroad Commission meeting saw two out of three Texas Oil and Gas regulators stated they are not ready to vote on oil output cuts today and they are to revisit the issue on May 5th. Sticking with North America, sources stated that producers in Alberta, Canada have reportedly already voluntarily cut 400k-700k BPD, according to Energy Intel. The contracts saw further downside as EU trade got underway, with WTI June resided under USD 11/bbl whilst Brent held onto losses of over 10% and eyed USD 17/bbl to the downside; however, since then we have recovered somewhat in what has been choppy trade for the complex but, ultimately, are in proximity to the lows – particularly for WTI, which ekes mild gains at the time of writing

The one thing that can definitively send oil sharply higher is a reopening in the global economy, and to this end, governments are devising ways to return people to work even as they discover infections are more extensive than they insisted only weeks ago. The coronavirus killed two people in California in early and mid-February, suggesting the pathogen was circulating in the U.S. weeks earlier than health officials thought. While Germany and a few other countries are moving to relax lockdown measures to contain outbreaks, Singapore – a global standard bearer for taming the deadly illness early on – has now become home to Southeast Asia’s largest recorded outbreak and is racing to regain control.

Meanwhile, corporate earnings have been mixed. Consumer-goods companies from brewers to paint-makers sounded notes of caution on spending. Heineken NV canceled its interim dividend, while Kering said it doesn’t see a recovery in the U.S. or Europe before at least June or July after sales at its flagship brand Gucci tumbled.

“There’s no way you can predict earnings right now,” Michael Cuggino, portfolio manager at Pacific Heights Asset Management LLC, said on Bloomberg TV. “It’s virtually impossible until we have more visibility with respect to how to world comes out of the coronavirus on the other side.”

Treasuries edged lower along with the dollar and European bonds fell. As Bloomberg reported yesterday, European policymakers plan to hold a call on Wednesday evening where they may discuss whether to accept junk-rated debt as collateral from lenders. Related to that, Italian bond yields and the risk premium the sovereign pays on its debt rose on Wednesday as the funding of the already heavily indebted country’s coronavirus stimulus plans remained uncertain. It may take European Union countries until the summer or even longer to agree on how to finance an economic recovery from the coronavirus pandemic as major disagreements still persist, an official with the bloc said on Wednesday.

“What we’re generally seeing is that there is less possibility that we are going to get some sort of conclusion on Thursday and even beyond that,” said Peter McCallum, rates strategist at Mizuho, referring to an EU summit on Thursday where measures to support coronavirus-hit economies will be discussed.

Yields across Italy’s curve rose, with the 10-year yield up as much as 10 basis points to 2.27%, a new peak since March 18, when the ECB announced its emergency purchase programme after trading hours. The gap between its 10-year bond yield and Germany’s – effectively the risk premium Italy pays – rose as high as 271 basis points, just five basis points away from touching their highest since the announcement of the emergency measures.

Spanish bonds extended declines and underperformed euro-area debt after the nation’s Treasury launched a massive 10-year syndicated debt sale.

In FX, a dollar gauge snapped two days of gains as European stock markets and U.S. equity futures rebounded. The dollar slipped versus all G10 peers; The Australian dollar advanced against its Group-of-10 peers after leveraged funds covered short positions exposed by better-than- expected retail sales data. Japan’s government bonds rose as the slump in oil prices raised concern about the global economic outlook, prompting demand for haven assets; the yen advanced for the first time in three days. Economic data include mortgage applications. AT&T, Thermo Fisher and Biogen are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 1.2% to 2,764.25

- STOXX Europe 600 up 1.1% to 327.88

- MXAP up 0.2% to 141.41

- MXAPJ up 0.7% to 457.74

- Nikkei down 0.7% to 19,137.95

- Topix down 0.6% to 1,406.90

- Hang Seng Index up 0.4% to 23,893.36

- Shanghai Composite up 0.6% to 2,843.98

- Sensex up 1.9% to 31,216.92

- Australia S&P/ASX 200 unchanged at 5,221.25

- Kospi up 0.9% to 1,896.15

- Brent Futures down 9.2% to $17.56/bbl

- Gold spot up 0.6% to $1,695.43

- U.S. Dollar Index down 0.1% to 100.16

- German 10Y yield rose 2.0 bps to -0.457%

- Euro down 0.02% to $1.0856

- Brent Futures down 9.2% to $17.56/bbl

- Italian 10Y yield rose 21.4 bps to 1.978%

- Spanish 10Y yield rose 10.4 bps to 1.108%

Top Overnight News

- Singapore reported more than 1,000 new cases for the third straight day. New coronavirus cases in Germany stayed close to a three-week low as the country begins gradually lifting lockdown measures

- The U.K. bond market looks set to face a flood of bond sales that dwarfs the current record for government borrowing set during the global financial crisis

- ECB policy makers will hold a call on Wednesday evening where they may discuss whether to accept junk-rated debt as collateral from lenders

- The euro area’s run of record-breaking government bond sales has continued in Spain, highlighting that demand for the region’s higher-yielding securities remains robust, when the price is right

- Global funding markets are beginning to diverge — easing in the U.S. while still showing signs of stress in Europe

- Oil’s plunge below zero for the first time in history has broken the models that many traders rely on to calculate risk. For Wall Street’s biggest banks, that has meant a franticscramble over the past 24 hours to recalculate the value and riskiness of their trading books

Asian equity markets initially extended on losses as the subdued tone rolled over once again from Wall St where sentiment was pressured by the continued oil market rout, but initially finished relatively mixed. Price action included the WTI June contract prices briefly slipping to single digits and with underperformance in tech amid President Trump’s plans for an immigration ban given the sector’s reliance on foreign talent. ASX 200 (U/C) and Nikkei 225 (-0.7%) were weaker with Australia dragged lower by the mining related sectors and as corporate updates trickled in with Beach Energy also suffering from softer quarterly production, while the Japanese benchmark briefly fell below 19k as the recent detrimental currency flows reverberated across exporter names. Hang Seng (+0.4%) and Shanghai Comp. (+0.6%) conformed to the subdued global risk tone but with losses in the mainland limited by anticipation of further support after Chinese President Xi pledged stronger macro policy tools to soften the epidemic fallout and the State Council noted that China will boost targeted assistance to those in need, as well as small businesses. Finally, 10yr JGBs advanced as the took advantage of the weakness in stocks and amid the BoJ’s presence in the market today for JPY 710bln of JGBs heavily concentrated in 3yr-10yr maturities.

Top Asian News

- China’s Banks Hit by Increase in Bad Loans in First Quarter

- India Eases Up on Currency Intervention, Protecting Reserves

- Bank Indonesia Says IDR Exchange Rate Stability Maintained

- Bank Indonesia Makes First Direct Purchase of Government Bonds

European equity futures see tailwinds from the turnaround in sentiment at the end of the APAC session (Euro Stoxx 50 +1.1%), with US equity futures also posting gains in excess of 1% in early trade. Sectors see broad-based gains, albeit energy lags as the complex remains under pressure from storage scarcity. In term of the breakdown, Tech names lead the gains following earnings from STMicroelectronics (+6.2%), whilst the sector also sees tailwinds from Texas Instruments (+3.0% pre-mkt), with the former, despite misses on its metrics, noted that Q1 was exited with stable net financial position, over USD 2.5bln in liquidity and available credit facilities above USD 1bln. Looking at other movers, Roche (+1.7%) is supported post earnings in which it topped estimates and pharma sales rose 7% YY. The Co. also stated that Clinical Phase III study to evaluate the safety and efficacy of Actemra/Roactemra in severe COVID-19 pneumonia is ongoing in several countries, with results expected in early summer, adding there is capacity for a rapid increase of production. On the flip side, Credit Suisse (+0.4%) is hampered vs. the region after it stated it is to take an additional EUR 900mln loan loss provisions in Q1. Finally, other earnings-related movers include Akzo Nobel (+7.9%), Ericsson (+6.4%) and Kering (-5.42), the latter reported a decline in Gucci sales of 23.2% YY.

Top European News

- Spain Follows Italy With Record-Setting Bond Demand at Sale

- EU Braces for Tense Call as Leaders Given No Plan to Work On

- Heineken Pulls Payout, Kering’s Gucci Sales Slump: Earnings Wrap

In FX, another swing in broad risk sentiment amidst less pronounced pressure on oil and other commodities has aided the latest Aussie, Kiwi and Loonie recovery, but with the former also benefiting from a short squeeze in wake of a record rise in retail sales per preliminary data for March. Aud/Usd took some time to digest the release and acknowledge the fact that stock-piling for COVID-19 boosted consumption, but subsequently breached 0.6300 on the way to circa 0.6350 with stops tripped above 0.6325 and macro fund offers over 0.6340 absorbed along the way. Meanwhile, Nzd/Usd retested 0.6000, albeit with a lag as Aud/Nzd rebounded from sub-1.0550 to around 1.0580, and Usd/Cad has retreated between 1.4237-1.4139 parameters on the aforementioned relative stability in crude prices ahead of Canadian CPI.

- GBP/SEK/NOK – Sterling has unwound some of its recent underperformance on technical rather than fundamental grounds given Cable remaining above the 30 DMA (1.2257) and revisiting 1.2300+ levels, while Eur/Gbp has reversed towards 0.8800 as the DXY meanders within a tight band on the 100.000 handle and single currency continues to straddle 1.0850. Similarly, the Scandis are seeing some reprieve from oil and pandemic risk aversion, with Eur/Nok and Eur/Sek both off highs near 11.5950 and 10.9700 respectively and the Swedish Krona weighing up more unconventional Riksbank easing in the form of municipal QE in the run up to next week’s official policy meeting.

- JPY/EUR/CHF – All sticking to pretty narrow and well trodden recent confines vs the Dollar, as the Yen flits from 107.86 to 107.52, Euro hovers below 1.0900 and above 1.0800 amidst decent option expiry interest at the former (1.5 bn) and 1.0825 (1 bn), and Franc pivots 0.9700.

- EM – Softer than expected SA CPI has not hindered the Rand amidst the overall upturn in risk appetite, but the Lira is treading more cautiously into the CBRT even though the Central Bank has already lifted FX swap limit transactions to 30% from 20% in what may be an effort to keep Usd/Try under 7.0000 in the event that rates are cut again, as widely expected, but perhaps more than the -50 bp consensus. On that note, the Mexican Peso seems to have taken Banxico’s emergency ½ point ease in stride or at least lubricated by the less fractious state of trade in crude markets.

- Australian Retail Sales (Mar P) 8.2% (Prev. 0.5%); largest increase on record. ABS said the March sales data indicated unprecedented demand for food retailing industry. (Newswires)

In commodities, WTI and Brent front month futures remain choppy, but ultimately mixed this morning, with WTI swinging between gains and losses whilst Brent remained in the red for the entirety of the session thus far. Yesterday, OPEC Delegates discussed the oil market crisis within a conference call; although the call was reportedly not designed to make a new oil decision and they were said to consider a May 10th meeting for further production cuts. Furthermore, Saudi, UAE, and Kuwait did not take part in the call and a delegate noted that OPEC+ members will be unable to start production cuts earlier because April’s oil production is already committed for export contracts. Meanwhile, the Iraq Energy Minister said OPEC+ could take additional steps to absorb the oil surplus but added that taking further measures by producer countries depends on global market development and compliance by other OPEC+ and other non-member producers with the oil cut deal. Russia again downplayed the gravitas of the oil market situation. Elsewhere, the fallout from the Texas Railroad Commission meeting saw two out of three Texas Oil and Gas regulators stated they are not ready to vote on oil output cuts today and they are to revisit the issue on May 5th. Sticking with North America, sources stated that producers in Alberta, Canada have reportedly already voluntarily cut 400k-700k BPD, according to Energy Intel. The contracts saw further downside as EU trade got underway, with WTI June resided under USD 11/bbl whilst Brent held onto losses of over 10% and eyed USD 17/bbl to the downside; however, since then we have recovered somewhat in what has been choppy trade for the complex but, ultimately, are in proximity to the lows – particularly for WTI, which ekes mild gains at the time of writing. Looking at the metals market, spot gold benefits from the Dollar pullback and reclaimed its USD 1700/oz handle. While copper trades subdued around USD 2.25/bbl, with miner Antofagasta stating that Q1 copper production rose almost 5% YY.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 7.3%

- 9am: FHFA House Price Index MoM, est. 0.3%, prior 0.3%

DB’s Jim Reid concludes the overnight wrap

Markets stuck to the risk-off theme once again yesterday, as a negative cocktail of oil market turmoil, weak corporate earnings and concerns about Europe conspired to make this a more difficult week so far for equities. Indeed, with the S&P 500 down a further -3.07% yesterday, that means the index has had its worst start to a week for 5 weeks, back when markets were at their most tumultuous. And in another warning sign, the VIX index has also had its largest 2-day increase since it hit its peak back in mid-March.

All eyes were on oil once again yesterday, where governments tried unsuccessfully to contain the rout. Brent Crude fell below $20/barrel for the first time since 2002 and down -24.40% on the day. Things haven’t gotten any better overnight where it’s down another -12.62% to $16.89/bbl. May WTI settled yesterday at $10.01 but the previous day’s shenanigans (lows of -$37.63) extended into the June contract which was down -43.37% to $11.57 and is trading at $10.90 this morning. As our oil analyst Michael Hsueh pointed out the previous evening, negative pricing could extend into the June contract so the sharp move wasn’t a surprise.

OPEC ministers did not decide on any new policy measures on an unscheduled call last night, which followed reports earlier in the day that they’d start their planned output cuts immediately rather than waiting until the start of May. In a joint closing statement the ministers said that they should “continue holding such consultations”, but it remains unclear if any country has the ability or the inclination to cut further than what is expected to come on May 1. Meanwhile President Trump tweeted that “We will never let the great U.S. Oil & Gas Industry Down”, and that he’d instructed the Energy and Treasury Secretaries “to formulate a plan which will make funds available so that these very important companies and jobs will be secured long into the future!” Unsurprisingly, oil-producing currencies took a hit once again, with the Russian Ruble (-2.00%) and the Norwegian Krone (-1.85%) both suffering against the US dollar.

Other global equity markets joined the S&P lower, with the NASDAQ (-3.48%), the STOXX 600 (-3.39%) and the DAX (-3.99%) all seeing major declines. One sector that had a bad day were European banks, with the STOXX Banks index down -4.60% at its lowest ever level since the index began in the late 1980s, having now lost almost half its value since the start of this year. The overall risk-off came against the backdrop of some weak corporate earnings. Netflix surged +12% right after the closing bell, but within 2 hours had given the entire post-market rally to be back near unchanged. The online streaming company announced nearly 16 million subscribers (nearly double consensus estimates of 8.47 million), but the company’s guidance did not deliver as the company is forecasting a number of subscriptions will be cancelled when confinement ends. Going through the other highlights, Coca Cola (-2.24%) said that they’d experienced a global volume decline of around 25% since the start of April with sales outside the home suffering thanks to the pandemic. Lockheed Martin (-2.32%) lowered their sales outlook, while HCA Healthcare (-4.50%) withdrew their 2020 guidance and suspended their quarterly dividend programme. In Europe, PSA (+0.26%) said that they expected the European vehicle market to shrink by 25% this year, as they announced a 15.6% decline in their Q1 sales.

The overnight session has seen markets in Asia follow Wall Street’s lead however the good news is that the declines are more modest. Indeed the Nikkei (-1.06%), Hang Seng (-0.50%), Shanghai Comp (-0.16%), ASX (-0.14%) and Kospi (-0.81%) are all posting small declines. Elsewhere, futures on the S&P 500 are up +0.30% while yields on 10y USTs are down -1.8bps to 0.553%.

In other news, the US senate passed $484bn in new pandemic relief funds yesterday. President Trump said soon after that he would sign the legislation and then turn to the next round of stimulus which is said to include aid to state and local governments and coronavirus caregivers, amongst others. The bill is likely to be voted on in the House today before it moves to President Trump’s desk. Trump also said in an overnight press conference that he’ll ask larger companies to return money they accessed from the federal stimulus package because it was intended to help small businesses while at the same conference Treasury Secretary Mnuchin threatened “severe consequences” for such companies. Trump also gave clarity on his decision on stopping immigration, saying the pause will be in effect for 60 days and will apply only to individuals seeking permanent residency with some exceptions and he will likely sign the order today.

Ahead of tomorrow afternoon’s European Council videoconference, there was a Reuters story yesterday which said that EU member states were moving closer to an agreement that would see the next long-term budget used for a stimulus package, rather than being done through coronabonds or some other form of joint debt issuance. However, the report also said that leaders continue to disagree on the implementation and “seem virtually certain to defer any final decision”. This was later backed up by Italian Prime Minister Conte, who said he didn’t think that leaders would manage to reach a “definitive solution” tomorrow. However he did say he was ready to work with the EU on a new ESM line which was seen as conciliatory.

The spread of 10yr Italian yields over bunds was up by +24.6bps to 263bps, its highest level since 18 March, though still below the intraday highs of 320bps reached that day. A large €16bn syndicated deal was successfully launched but likely led to indigestions across other parts of the curve. A reminder that S&P will likely opine on their review of Italy’s BBB rating by Friday. Late in the session Bloomberg reported that the ECB will hold a call tonight to discuss whether to allow junk rated debt as collateral. They’ve already done this for Greece and they might be preparing the way for Italian debt if the need arises over the coming weeks or months.

Meanwhile Spanish (+14.2bps), Greek (+31.3bps) and Portuguese (+13.9bps) spreads all saw sizeable moves wider as well, with the Spanish spread over bunds actually closing at its highest level since April 2017. Outside of southern Europe, sovereign debt actually performed much stronger, with US 10yr Treasury yields closing just above their lowest ever level, at 0.569%. 10yr bund yields also saw a fall of -2.9bps, while gilt yields were down -4.0bps.

Wrapping up with the data releases, there wasn’t a great deal out yesterday, though the ZEW survey from Germany saw the current situation reading fall to -91.5 in April (vs. -77.5 expected), which was its lowest level since May 2009. Nevertheless, the expectations reading actually surprised, coming in at (28.2 vs. -42.0 expected), its highest level since July 2015. We are going to get some choppy diffusion indices over the next couple of months as they measure activity relative to the previous month so it’s easy to have bigger swings in both directions than even the likely volatile nature of the data would suggest. Over in the US, existing home sales in March fell by -8.5% month-on-month, which was their largest monthly decline since November 2015. Finally in the UK, before the pandemic hit in the December-February period, the employment rate hit a record high of 76.6%.

To the day ahead, and data releases include March CPI readings from both the UK and Canada, the European Commission’s advance Euro Area consumer confidence reading for April, Italian industrial sales and industrial orders for February, along with weekly MBA mortgage applications and the FHFA house price index for February from the US. From central banks, Turkey will be deciding on rates and we’ll also hear from the ECB’s Rehn. Finally, earnings out today include AT&T and Thermo Fisher Scientific.

Tyler Durden

Wed, 04/22/2020 – 08:35

via ZeroHedge News https://ift.tt/2RWrNmX Tyler Durden