“Unprecedented Damage To The Euro Zone” – European PMIs Hammered By Record Collapse

Economic activity across the eurozone ground to a halt this month as the new coronavirus sweeping across the world forced governments to impose lockdowns and firms to down tools and shut their businesses.

The latest monthly PMI manufacturing and service surveys illustrated the severity of the crash in economic activity across Europe and the UK, as lockdowns stifle businesses from Paris to Frankfurt. Overall, the eurozone composite purchasing manager’s index – which monitors manufacturing and services activity – fell to 13.5 in April, from 29.7 in the previous month, a record low in more than 22 years of the history of the survey, and blow even the lowest estimate of 18.0. The manufacturing component tumbled from 44.5 in March to 33.6 in April, below the 39.2 expected, but it was the collapse in Services that was shocking, collapsing more than 50% from 26.4 to 11.7.

According to Markit, demand all but dried up this month, headcount was reduced at a record pace and firms cut prices at one of the steepest rates since the survey began.

“April saw unprecedented damage to the euro zone economy amid virus lockdown measures coupled with slumping global demand and shortages of both staff and inputs,” said Chris Williamson, chief business economist at IHS Markit.

“The ferocity of the slump has also surpassed that thought imaginable by most economists.”

Williamson said the PMI was consistent with the European GDP contracting 7.5% this quarter. A Reuters poll published on Wednesday had a 9.6% contraction pencilled in. Unsurprisingly therefore, optimism was also at a survey low. The future output sub-index, which almost halved last month, was 34.5.

With restaurants, bars and other leisure activities shuttered, holidays cancelled and travel restricted the situation in the bloc’s dominant services industry was dire. The flash services PMI sank to a new record low of 11.7 from 26.4.

A new business index dropped to a record low of 11.6 from 24.0, and firms completed outstanding demand at the fastest rate in the survey’s history. April is also proving to be a grim month for the bloc’s factories.

The preliminary manufacturing PMI dropped to a survey low of 33.6 from March’s 44.5. An index measuring output, which feeds into the composite PMI, more than halved to 18.4 from 38.5. Demand was barely existent and with many of their factories closed, manufacturers cut staffing levels sharply. The employment sub-index fell to 35.7 from 44.3, its lowest since April 2009, around the start of the euro zone debt crisis.

“In the face of such a prolonged slump in demand, job losses could intensify from the current record pace and new fears will be raised as to the economic cost of containing the virus,” Williamson said.

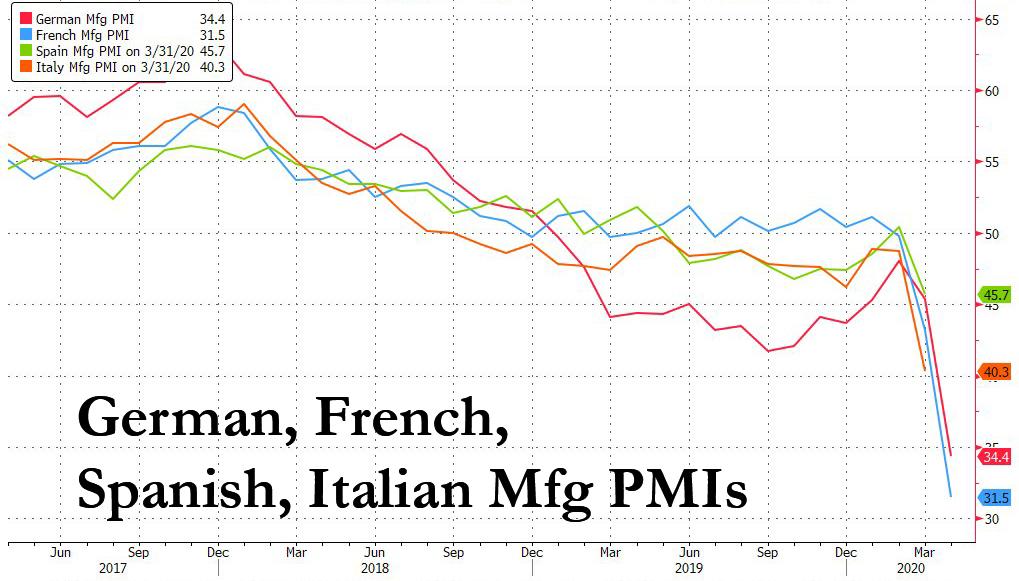

Earlier, French and German business activity also fell to record lows, in readings that suggest the region faces a major economic downturn, with manufacturing hit hard …

… but once again it was Services that were crushed as virtually all of the continent was put on lockdown.

As can be seen above, business in Germany – the eurozone’s economic powerhouse – crashed this month, following France in recording its lowest readings of services and manufacturing activity on record. The IHS Markit flash purchasing managers’ index for services fell to 15.9 in April from 31.9 in March, the lowest since record began more than 22 years ago as about three-quarters of companies reported a fall in activity.

The index for manufacturing output also dropped to a record low at 19.4 in April, from 41 in the previous month. The IHS composite index, an average of services and manufacturing fell to 17.1 in April, also a record low. April’s PMI surveys show “business activity across manufacturing and services falling at a rate unlike anything that has come before,” said Phil Smith, principal economist at IHS Markit.

Summarizing the catastrophic data, economist Daniel Lacalle said that “the collapse is much larger than expected and the largest ever seen. With most of the stimuli aimed at the wrong areas of the economy (mostly zombie states and enterprises) while keeping high taxes and regulatory burdens, the recovery will be long and painful.”

Tyler Durden

Thu, 04/23/2020 – 07:53

via ZeroHedge News https://ift.tt/3cDVMb2 Tyler Durden