The S&P Is Caught In A Gamma Trap, Preventing Turmoil From Record High Valuations

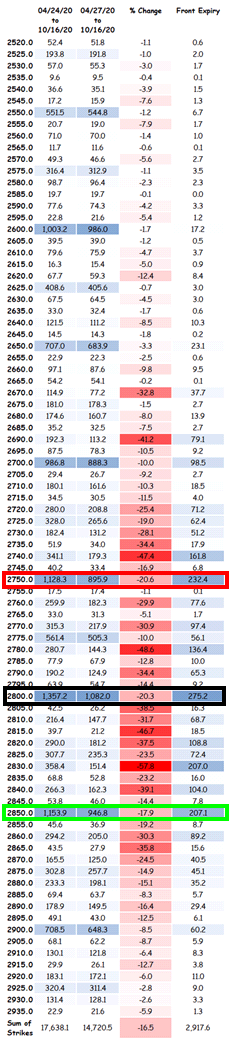

Over the past three days, despite a barrage of negative news about the global economy and crushed hopes about Gilead’s Remdesivir treatment which according to the FT was a “flop”, stocks have been stuck in a tight range around the 2,800 S&P level, and there is a specific reason for that. As Nomura’s Charlie McElligott notes, the S&P 2,800 has emerged as the “Neutral Gamma” zone for the market “and again, is likely to remain that way, as the 3 largest aggregated Gamma strikes on the board have the S&P surrounded” as follows: $1.128B at 2750, $1.357 at 2800 and $1.154B at 2850:

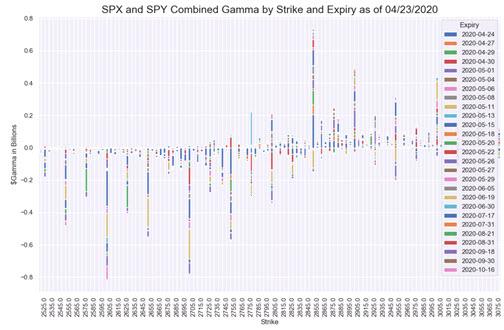

Here is the data above shown in combine gamma format:

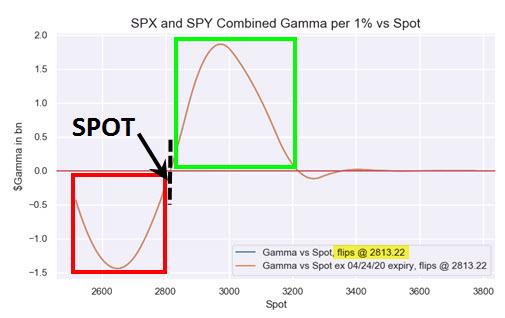

To be sure, with the S&P caught in this “gamma trap” on both sides, bulls will be gunning to close the S&P above the “flip” level 2813 coming out of today’s expiration, which would push dealer gamma in the green, creating a feedback loop whereby higher prices result in even higher prices as dealers are forced to chase the market higher.

Further adding to this market “brake” effect are normalizing Vol Control strategy flows, where the recent violent repositioning in the form of US stock selling over the past 3 month (~$305B estimated) was followed by the pivot towards buying seen more locally (+$13.5B bot the past 2w), which however has slowed to a trickle, reducing “second order” systematic flows which as Nomura explains, typically act as an accelerant following a “Gamma Impulse” which occurs after a macro shock, such as the double-whammy of the COVID pandemic alongside the oil price crash.

That about covers the technicals. Where things get interesting is the fundamentals (assuming those still matter in a world where only the Fed’s liquidity injections have an impact on stock prices), and here -as we first noted two weeks ago – the euphoria is once again unmatched.

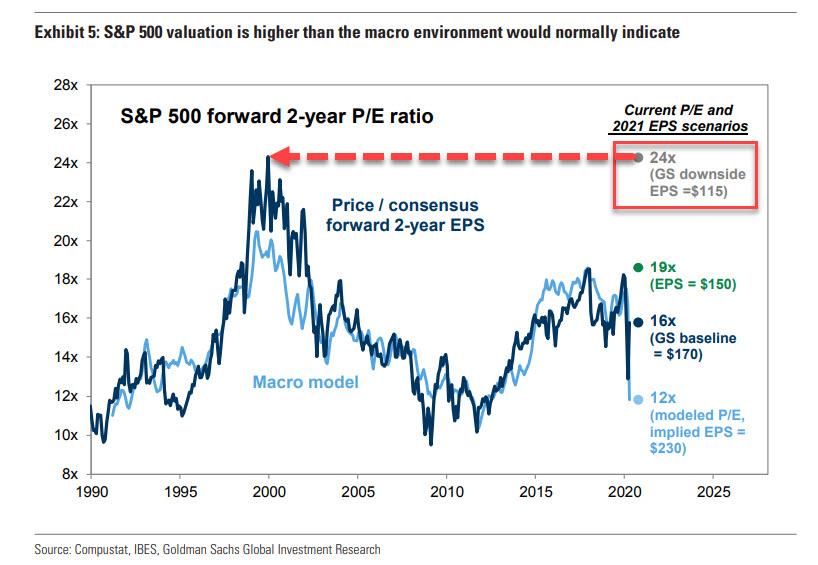

Picking up on what we wrote two weeks ago, namely that “As The US Enters A Depression, Stocks Are Now The Most Overvalued Ever“, today the Financial Times writes that “US equity valuations reach near two-decade high after rally“, and points out what our readers have long known, namely that

“the rally has pushed the forward price-to-earnings ratio for the S&P 500 above 21 to its highest level since December 2001 — during the final stages of the dotcom bubble. The ratio reflects the price put by investors on future profits and is one of the most popular tools for investors to value stocks.”

Worse, the estimates shown above are based on highly optimsitic consensus forecasts which have yet to come down sharply. More from the FT:

Some portfolio managers warn that this expansion in the earnings multiple has left investors at greater risk from stale forecasts. Wall Street analysts have faced extra difficulty in gauging earnings given many US blue-chips have withdrawn full-year profit guidance, citing the uncertainty posed by the pandemic.

“A lot of companies are not giving guidance and it’s harder for analysts to revise their numbers,” said James Wong, a portfolio manager who runs the equity group of Payden & Rygel, a fund manager based in Los Angeles. “They’re looking for guidance and without it their numbers are a shot in the dark.”

Here is the truth: if one uses a downside case for forward EPS 2021, which Goldman believes is as low as 115, it means that the current forward PE is not 21 but actually24, the highest on record.

Alas, companies won’t be of any help in sharing hints on what earnings to expect as they themselves don’t know: In the past few weeks of first-quarter earnings, companies including Wells Fargo, IBM and Uber have scrapped the full-year profit guidance they typically share with analysts.

“I would have to close my eyes and throw a dart at a dartboard to guess what earnings will be this year,” said Terri Spath, chief investment officer of Sierra Investment Management also in Los Angeles. “It’s too challenging to put a number to it — this complete contraction of the economy is very painful.”

And while the Fed is doing everything in its power to tear the last links between stocks and fundamentals by injecting gargantuan amounts of credit into the system, some old-school traders remains skeptical and actually focus on near-term valuations. “I’m concerned that earnings haven’t been revised down enough,” said Wong. “If the markets don’t come off here, the price-to-earnings ratio is going to get even higher.”

* * *

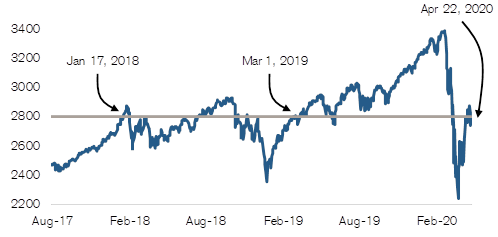

One final observation on the S&P getting stuck at 2,800 is that as Credit Suisse chief equity strategist puts it, we’ve been here before on many occasions. Here are his observations:

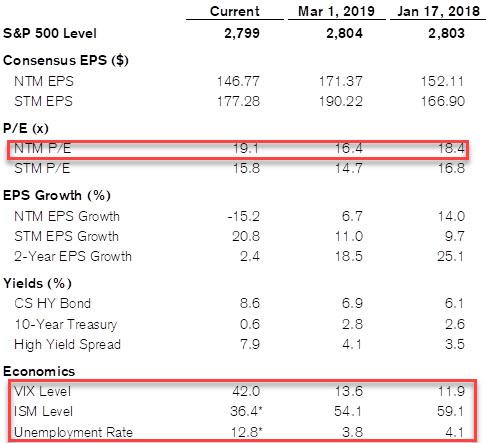

One of the greatest challenges for investors in the current environment is a lack of comparisons. The cause of the current crisis and the economic damage are unlike anything we’ve experienced. However, we have been at 2800 on the S&P 500 before, in Jan 2018 and again in March 2019.

The table below highlights just how different conditions are today, with the goal of addressing one simple question: are investors being compensated for the risk being taken?

Key takeaways and observations:

- While treasury yields are lower today, credit spreads are wider. As a result, the cost of capital is higher, implying lower valuations.

- Volatility (as a measure of uncertainty) is 3-4x higher today.

- Consensus Forward P/Es (next 12 months) are higher today. We believe this will be stretched even more as estimates continue to fall.

- Consensus Forward P/Es (second 12 months) are relatively comparable to other periods. These multiples assume a sharp V in corporate profits.

- EPS growth is expected to be weaker over the next 12 and 24 months than in comparable periods.

Finally, here is what the macro backdrop looked like in the last two times when the S&P was “stuck” at 2,800: long story short, it has never been as ugly as it is right now.

Which begs the question: How much longer can technicals and the Fed defy the fundamentals?

Tyler Durden

Fri, 04/24/2020 – 10:50

via ZeroHedge News https://ift.tt/3cQdhVT Tyler Durden