Freight Trucking Demand Plunges To All Time Lows; Rates Crash And Industry Grapples With Lockdown

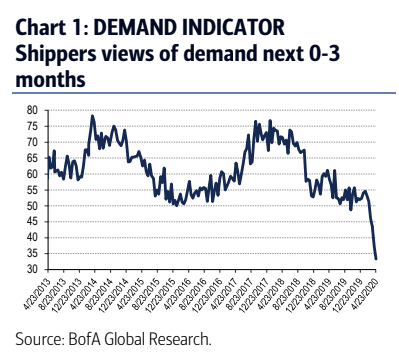

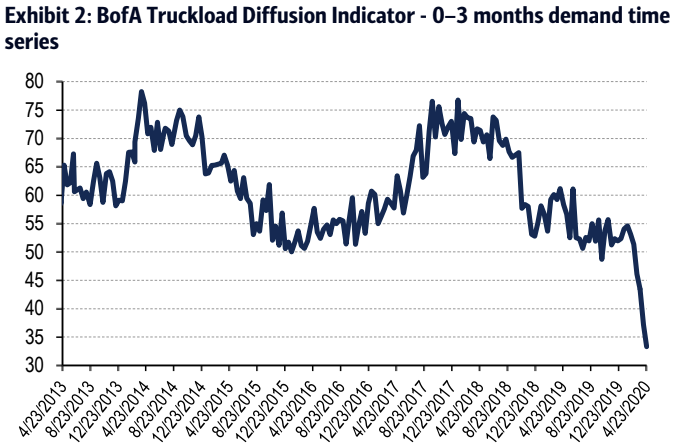

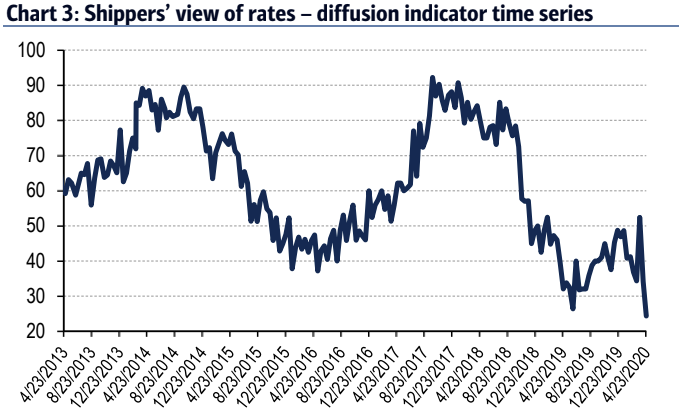

Bank of America’s Truckload Diffusion Indicator for shippers continues to paint a grim picture not only of freight, but of the overall economy. Put simply, the pandemic has led to record lows and some of the ugliest survey numbers since the bank started conducting it back in 2012.

Heavy duty trucking was already in the midst of trying to shake off the results of a bloated Class 8 order backlog that started in 2018, as we document on a month-by-month basis here on Zero Hedge. Not unlike the auto industry, it was a terrible time for the industry to be hit with demand interruption and the coronavirus has forced the sector from “bad” to “worse”.

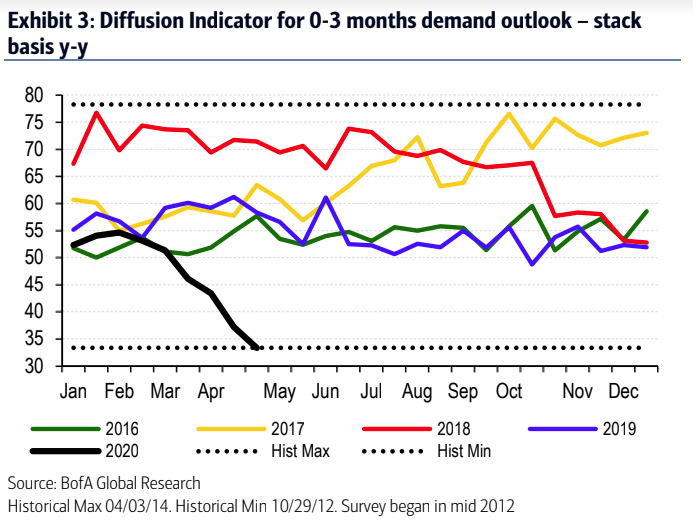

Bank of America’s Truckload Diffusion Indicator for shippers’ 0- to 3-month freight demand outlook dropped to 33.3 from 37.2 last issue, a -10% sequential decline. It’s the fourth survey in a row that sets an all time low.

The bank wrote in a note on Friday of last week: “The Demand Indicator is down -39% after hitting a temporary peak of 54.6 on January 30. The survey is down 43% year-over-year, its 43rd consecutive decline (its longest stretch), and posting the largest ever year-year decline, accelerating from last survey’s -39% decline.”

The note continued: “Shippers’ short-term positive outlooks was stable at 21% from last survey, neutral outlooks fell to 15% from 22%, while negative outlooks increased to 64% from 56% (the highest level in our survey history). For the week of April 23, we surveyed 39 shippers across the US to get current views on freight demand and supply.”

Meanwhile, freight supply has ballooned: “The Truck Capacity Indicator rose to 80.8, up 12% from 72.0 last issue, matching the all-time survey high, highlighting the over-supply of trucking capacity that emerged in May.”

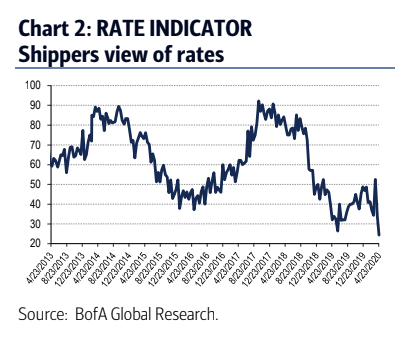

Inventory has also risen while capacity frees up and prices fall: “The Inventory Indicator is at 53.8, up 13% from 47.6 last issue, indicating shipper’s inventory levels are building rapidly. With respect to rates, 44% of shippers expect rates to be flat, mirroring last issue, 54% expect rates to fall, rising from 44%, and only 3% expect rates to rise, down from 12%. On capacity, 67% of shippers expect capacity to increase, up from 56% last survey, 28% expect the fleet to remain flat, down from 32% and only 5% expect capacity to be lower, down from 12%.”

The bank is also getting pessimistic feedback from the corporations that utilize freight as an integral part of their business. For instance, a shipper from the consumer staples industry noted “there remains heightened uncertainty around the timing of resumption of non-essential businesses, and how the remaining truckload carriers will be able to manage that influx.”

Finally, there doesn’t seem to be any help coming from Class 8 producers, who produced 18,123 heavy duty trucks in March versus just 7,610 orders. The nearly 11,000 truck spread was the largest since September 2019 and will likely continue to weigh on rates.

Tyler Durden

Mon, 04/27/2020 – 10:30

via ZeroHedge News https://ift.tt/2KAbbNJ Tyler Durden