ECB Preview: Don’t Expect Much

Just like the Fed yesterday, don’t expect much from today’s ECB meeting. According to Saxobank’s Christopher Dembik, President Lagarde’s main goal today will be to explain what her strategy is and how she sees the shape of the recovery. There is no urgent need to beef up asset purchases yet.

Summary:

- ECB policy announcement due Thursday 30th April; rate decision at 1245BST/745ET, press conference 1330BST/ 0830ET

- Rates set to be left unchanged, tweaks to the PEPP could be on the cards

- President Lagarde likely to stress the Governing Council’s willingness to “do whatever it takes” in the absence of any other policy adjustments

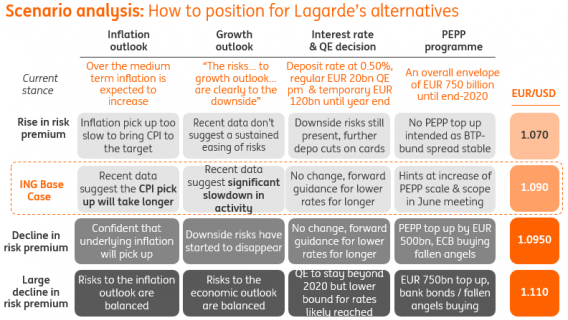

ECB Cheat Sheet courtesy of ING economics:

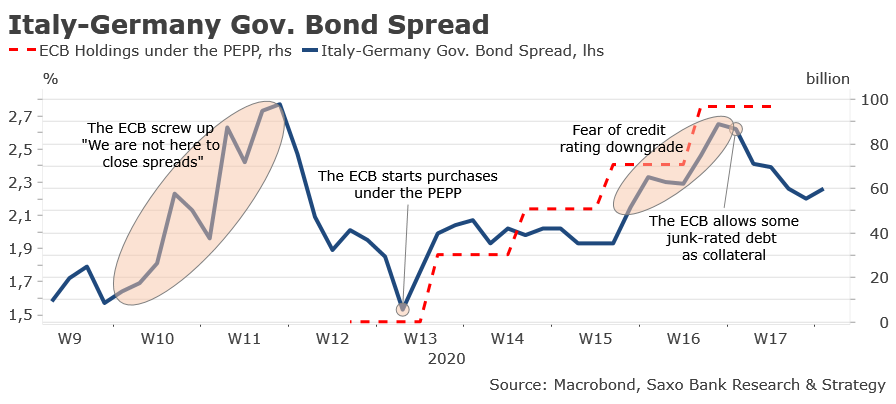

Context: If we omit Lagarde’s mistake on the ECB’s willingness to close spreads, the central bank has done a good job to address the financial and economic issues related to the COVID-19 outbreak. Since the first week of March, the ECB has implemented more favorable terms for the already planned TLTRO III with a rate up to -0.75% and it has considerably expanded asset purchases. Including the new PEPP of about €750bn, previous measures and the relaunch of QE by Lagarde’s predecessor in 2019, the total asset purchases are expected to reach around €1tr in 2020. The ECB also showed high degree of flexibility in the design and the implementation of its several virus-fighting packages. The 33% limit does not apply under the PEPP and the ECB can purchase debt across all the yield curve, including Greek debt under waiver. In its most recent move, the ECB also acted to shield Italy from rating downgrade by accepting some junk-rated debt as collateral for loans to banks.

* * *

Today’s meeting is not expected to yield much in the way of policy action. Basically, Lagarde’s challenge is to explain in the most simple manner the ECB’s strategy and how she sees the shape of the recovery – especially following the release of France’s horrific Q1 GDP figure at minus 5.8%. Like Fed Chairman Powell yesterday, Lagarde is likely to make it clear that she is not in the V-shape recovery camp. She should also repeat over and over her readiness to act appropriately to tackle any market tensions, so much so she may feel like a broken record.

Expectations are very high that Lagarde stresses the door is open to new measures, likely announced in June. The ECB can afford to wait as the emergency work has been masterfully done. However, it seems inevitable that it will have to increase in the near term the scale and the scope of the PEPP in order to deal with the increase in gross issuance in 2020, notably in the periphery. Based on our calculations, eurozone government need to roll over almost €2tr in debt and finance new net issuance of about €1.5tr this year. The ECB’s commitment to buy only around €1tr is understandably insufficient. We expect that it will need to increase total asset purchases by at least 500bn this year to absorb coronavirus debts.

If new market tensions should materialize, the ECB is not running out of ammunition. Other innovations are possible, including a further loosening of lending benchmark which currently stands at minus 0.75%, a shift into junk bonds with the extension of the Greek waiver to other eurozone countries or even the inclusion of mortgage loans in the pool.

Courtesy of RanSquawk, here are the key expectations from today’s meeting:

OVERVIEW: The ECB is expected to stand pat on rates this week with focus instead likely to fall on the Bank’s balance sheet and how it views monetary and fiscal actions taken thus far. On the balance sheet, consensus leans in favor of the GC needing to expand the current scope of its Pandemic Emergency Purchase Programme (PEPP). Views are mixed on whether such an adjustment will be made this week or Lagarde will invoke strong rhetoric on the Bank’s preparedness to do more and defer the decision until June when lockdown measures have been eased across the Eurozone. As has been a common theme throughout Lagarde’s tenure, the President will likely use the press conference as a forum to call for further support from fiscal authorities.

PRIOR MEETING: In March, the ECB refrained from succumbing to market pricing and maintained the deposit rate at -0.5%. Instead, it tweaked existing measures, making the terms of the current TLTRO-III programme more favourable, with the rate on these operations (which run until June 2021) to be 25bps below the main refi rate, and in some cases, 25bps below the deposit rate. Further, it also unveiled a new series of LTROs which will ‘bridge the gap’ until the TLTRO-III operations resume in June. Additionally, the Governing Council also opted to expand the size of its Asset Purchase Programme by EUR 120bln until the end of the year. Note, the ECB maintained its forward guidance on rates and reinvestments.

FOLLOW UP MEASURES: On March 18th, the Bank unveiled a EUR 750bln PEPP in which purchases will be conducted until the end of 2020, whilst more recently, the Governing Council unveiled a package of temporary collateral easing measures and accepted the use of Greek government bonds (Apr 7th). Furthermore, on April 22nd, the ECB took steps to mitigate the impact of potential debt rating downgrades on collateral availability.

FISCAL EFFORTS: Monetary authorities have not been alone in their efforts to support the Eurozone economy with many national governments manufacturing domestic fiscal packages and Eurozone Finance Ministers agreeing to increase availability of the ESM’s Credit Line, create a short-time work scheme and provide further support via the European Investment Bank. However, EU27 leaders are yet to sign off on plans for a bloc-wide long-term recovery plan and the debate about joint debt mutualisation continues to lay bare the divisions across the continent. The ECB’s view on fiscal efforts will likely be a key line of enquiry during the Q&A, on which, RBC believes that with details still pending, it is likely to be too early to draw any firm conclusions on progress. However, despite work still needing to be done, the Canadian bank takes a relatively optimistic view on proceedings and expects Lagarde to have a positive interpretation of efforts thus far.

RECENT DATA: The traditional backward-looking data points have largely been dismissed as “stale” by the market with participants instead favoring more timelier indicators. Last week saw the latest batch of PMI readings which saw the EZ-wide composite metric slip to an eye-watering reading of 13.5 (prev. 29.7); manufacturing 33.6 (prev. 44.5) and services 11.7 (prev. 26.4). Following the release, IHS Markit noted that the reading would be indicative of the Eurozone economy contracting at a quarterly rate of around 7.5%. ABN AMRO provided a scenario analysis framework in which they estimate that 1) if existing lockdowns continue until the end of April (base case) 2020 GDP would contract by 4.5%. 2) if existing lockdowns continue until the end of May (negative case) 2020 GDP would contract by 8%. 3) if existing lockdowns continue until the end of April but consumer behavior normalizes at a quicker pace (positive case), the real economy could recover sharply but would benefit less in 2021 as stimulus efforts will be less aggressive. On the inflation front, given the fallout from COVID-19 on consumer spending and the nosedive in oil prices, the outlook for price pressures in the Eurozone is relatively bleak with the 5y5y inflation expectations gauge sub-1%. ABN AMRO notes that “HICP inflation will drop in the coming months and will probably register a couple of negative numbers on a year-over-year basis during Q2 of this year”. However, assuming a recovery in oil prices later in 2020, “headline inflation should bounce back sharply towards 2% by mid-2021”.

RECENT COMMUNICATIONS: Since the prior meeting, asides from policymakers trying to airbrush President Lagarde’s comment about it not being the ECB’s job “to close spreads”, rhetoric from the Bank has largely centered around trying to reassure markets in the face of the ongoing crisis. In recent remarks, governor Lagarde (Apr 16th) stated that the ECB is “fully prepared to increase the size of its asset purchase programmes and adjust their composition, by as much as necessary and for as long as needed. It will explore all options and all contingencies to support the economy”. Even some of the more traditionally hawkish members appear to be on board with such a stance with Dutch central banker Knot noting that adjustments to the PEPP cannot be excluded and the Bank will not allow spreads to widen too much. Germany’s Schnabel also echoed this sentiment and made the point that the Bank “‘needs to avoid fragmentation that may hamper the smooth transmission of our monetary policy’, again, a potential hat-tip to the perils of widening spreads. However, looking beyond the crisis, her domestic colleague Weidmann has cautioned that at some stage, focus must return to lowering debt.

RATES: From a rates perspective, consensus overwhelmingly looks for the deposit rate to be held at -0.5%, with the decision not to lower rates in March symbolic of scepticism over the efficacy of delving further into negative territory. UBS expects the ECB to stand pat on rates until the end of their forecast horizon (end-2021). The Swiss bank also suggests that as liquidity in the Eurozone rises, policymakers could opt to tweak the specifics of its tiered system (adjust the multiplier); such a move could be made this week or the June 4th meeting.

BALANCE SHEET: Instead, focus could fall on the ECB’s balance sheet with the current EUR 750bln size of its Pandemic Emergency Purchase Programme (PEPP) not deemed as sufficient to weather the course of the crisis given the surge in issuance by member states. Capital Economics suggests that at the current pace of purchases, PEPP would run out by October, however, since the ECB intends to run purchases until the end of the year, a reduction in the pace of buying would be required, something which could prove detrimental to the Eurozone economy and hinder the Bank’s ability to prevent spreads from widening further (despite the communication mishap from Lagarde in March). As such, Capital Economics suggests the Governing Council could opt to increase the size of its PEPP with an eventual size of over EUR 2trl. Alternatively, rather than setting a specific size for its PEPP, it could engage in purchasing bonds to cap yields at a desired level. Note, 1/4 economists in a recent newswire survey suggested that an announcement could be made this week, with expectations mounting over a potential EUR 500bln addition. Conversely, analysts at ING believe, that “If old patterns hold, the June meeting with a fresh round of economic projections, would be the right moment to announce such an increase”

ECONOMIC ASSESSMENT: Given the slightly dated nature of some of the economic indicators available, participants will likely take guidance from the GC’s current qualitative assessment of the Eurozone economy; note, no staff economic projections will be presented at this meeting. Ultimately, the Bank’s assessment of the Eurozone economy is likely to be particularly downbeat with March’s press conference already noting that “risks surrounding the euro area growth outlook are clearly on the downside” (this was during the early stages of the crisis), whilst last week it was reported that President Lagarde believes that Eurozone GDP could fall by as much as 15% this year. However, Lagarde will need to be careful in conveying the extent of the crisis, as too damming an assessment in the face of a lack of action this time around could stoke fears that policymakers are running out of ammo. Concerns that could also be exacerbated by any pessimistic language surrounding the Bank’s ability to hit its inflation goal; a target that has become even more opaque given the delays to the upcoming strategic review. As a guide, the ECB currently classifies measures of underlying inflation as “generally muted”.

Tyler Durden

Thu, 04/30/2020 – 07:31

via ZeroHedge News https://ift.tt/35gYEYW Tyler Durden