Here Is JPMorgan’s Latest Trade Idea: Buy Bond ETFs Before The Fed Does

It’s strange how capital markets work under central planning.

Late last Friday bond king Jeff Gundlach tweeted something which we had observed just one day earlier, namely that “the Fed has not actually bought any Corporate Bonds via the shell company set up to circumvent the restrictions of the Federal Reserve Act of 1913” adding that this “must be the most effective jawboning success in Fed history if that is true”…

I am told the Fed has not actually bought any Corporate Bonds via the shell company set up to circumvent the restrictions of the Federal Reserve Act of 1913. Must be the most effective jawboning success in Fed history if that is true.

— Jeffrey Gundlach (@TruthGundlach) May 1, 2020

This followed our own musings on the latest Fed balance sheet (currently at $6.66 trillion) in which we pointed out that “what is most interesting is that so far the Fed has not yet purchased a single corporate bond, whether investment grade of fallen angel junk. In other words, without lifting a finger, the Fed’s “whatever it takes” jawboning managed to inject trillions “in value” in countless debt and credit products.”

Bank of America also chimed one day later, which published a “A Note To Fed” which was meant to precipitate the Fed’s decision to get off the fence and to start waving bonds in, as “a lot of investors (including non-credit ones) have bought IG corporate bonds the past two months on the expectation they can sell to you. So would be helpful if you soon began buying broadly and in size.”

So in response to Gundlach’s query and BofA’s lament, and concerned there may be some selling by trapped LQD and JNK bagholders who suddenly are worried the Fed isn’t buying corporate bonds as it had promised, today the NY Fed unveiled that it expects to begin purchasing eligible ETFs under its Secondary Market Corporate Credit Facility “in early May.”

The SMCCF is expected to begin purchasing eligible ETFs in early May. The PMCCF is expected to become operational and the SMCCF is expected to begin purchasing eligible corporate bonds soon thereafter. Additional details on timing will be made available as those dates approach.

And so, just a few hours later, perhaps inspired by Blackrock’s Rick Rieder, head of the firm’s global allocation team, who in April wrote a blog post explaininghow the world’s largest asset manager will invest going forward, namely “follow the Fed and other DM central banks by purchasing what they’re purchasing, and assets that rhyme with those“, none other than JPMorgan had a brilliant trade idea for its clients, which basically boils down to this: buy corporate bond ETFs before the Fed does.

As JPM’s Shawn Quigg explains, “with the CCFs officially entering the market this month, it may further solidify the market’s perception of the Fed’s perceived put, and tighten credit spreads further.“

Of course, since such a simple trade reco would be frankly humiliating for such a “sophisticated” group of people as JPM’s derivatives team led by the rocket scientist Marko Kolanovic who every week or so writes a report on how stocks are undervalued when – it appears – all he means is one should simply frontrun the Fed…

… not to mention not generate any commission revenues for the bank, JPM had to make its trade reco sexier and more complex, and instead of simply buying the LQD, JPM recommended buying an LQD July 125p/ 130c/ 135c call spread collar – i.e., selling the put to fund the purchase of the call spread – for a zero cost, indicatively and a $128.66 reference price.

Also, since a stated rationale of simply “frontrun the Fed” would make a mockery out of JPM – and every other sellside strategist whose job is to divine the future of risk prices based on such obsolete anachronisms as fundamentals not how much money a central bank is going to print – the bank felt compelled to embellish just a bit, and that’s precisely what the Kolanovic-led team did:

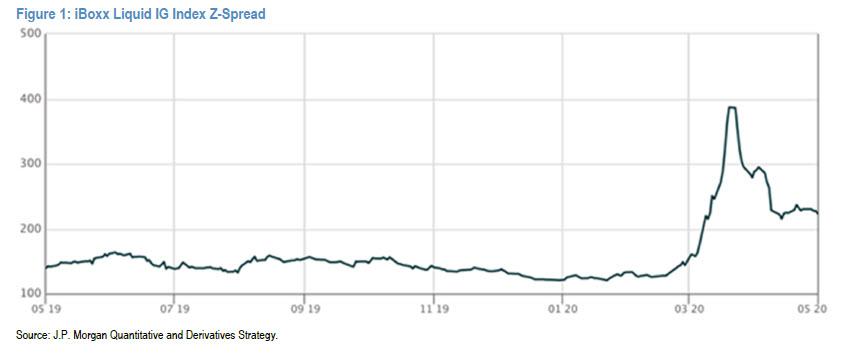

Rationale & Considerations: The combined size of the CCFs will be up to $750 billion. The PMCCF and SMCCF will leverage the Treasury’s equity at 10 to 1 when acquiring corporate bonds of issuers that are investment grade and for ETFs whose primary investment objective is exposure to U.S. investment grade corporate bonds. The CCFs will cease purchasing eligible corporate bonds and ETFs no later than September 30, 2020, unless extended by the Board of Governors of the Federal Reserve and the Department of the Treasury. If at expiration shares close at/below the put strike, investors will purchase shares at $125, representing spread levels in early April (and below its 50/100/200d technical moving averages). Conversely, the LQD spreads still trade substantially above the pre-COVID-19 levels, leaving much room for potential compression.

Current 3M volatility skew (95%-105%) ranks in its 85th %-ile over the last year, but with the execution of the CCFs we believe there is an argument to be made that volatility skew should cheapen further moving forward.

An even simpler argument to be made, yet one which won’t be, is that in this day and age of what Deutsche Bank accurately calls “administered markets” where “market outcomes will be dictated by the policy goals of the Fed and Treasury, and the tools they select to implement policy”…

…all that matters is what the Fed will or won’t be buying, and since by endorsing this trade JPM effectively agrees that frontrunning central banks is the only thing that matters, we wonder if JPM realizes the irony in that it has effectively “reco-ed” itself right out of all relevance, because it doesn’t take a rocket scientist to read a Fed press release and figure out what asset class the central bank will buy next (spoiler alert: after the next crash, it will be equities. At that point Wall Street becomes meaningless).

Incidentally, another side effect of Wall Street analysts admitting they are now irrelevant in this time of centrally-planned markets, is that as Jeff Gundlach tweeted in a follow up to his original Friday observation, closing the loop on a process that he himself started with a tweet just three days earlier, once Main Street realizes that the Fed is buying ETFs “broadly and in size” to not “let down” the buyers who front ran the Fed, it will “not be well received on Main Street.”

If the Fed does start buying ETFs “broadly and in size” in response to recent requests they do so as to not “let down” the buyers who front ran the Fed April 9th will not and should not be well received on Main Street.

— Jeffrey Gundlach (@TruthGundlach) May 4, 2020

We doubt JPM is too worried about condemning its clients to a fate of angry Main Street pitchforks, because unlike Gundlach, we are confident that the vast majority of Americans neither care, nor have any idea about the vast wealth transfer that is taking place below the surface of what was one a market courtesy of the Fed’s helicopter money, which is now openly destroying future generations of Americans by burying them under simply laughable amounts of debt just to keep a handful of millionaires and billionaires filthy rich here and now.

Tyler Durden

Mon, 05/04/2020 – 21:26

via ZeroHedge News https://ift.tt/3aZ5Qu0 Tyler Durden