Platts: 4 Commodity Charts To Watch This Week

Tyler Durden

Mon, 06/15/2020 – 11:20

via S&P Global Platts Insight blog,

Global recovery from the coronavirus pandemic is proving patchy, and demands a close look at oil demand signals – the first stop in this week’s roundup of energy and raw material trends. S&P Global Platts editors also look at prospects for US crude exports to Asia, Ukraine’s importance to the European gas market this summer, and the impact of reduced French nuclear availability on power markets.

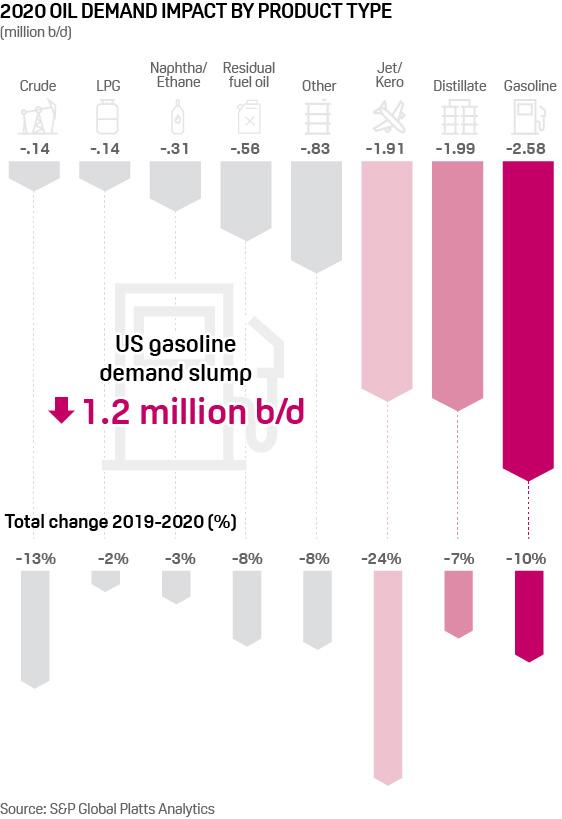

1. Global oil demand set for uneven recovery as coronavirus battle continues

What’s happening? Global oil demand is recovering from a record, 20 million b/d slump in April but not all fuels have suffered equally from sweeping lockdowns to combat the spread of coronavirus. Road and air transport fuels are on the frontline of the demand impact, suffering massive year-on-year contractions due to the curbs on travel and social movements. Estimates from S&P Global Platts Analytics show US gasoline demand is by far the biggest casualty accounting for almost half of the 2.6 million b/d global impact for the key driving fuel. It is the grounding of thousands of flights globally, however, that will see jet fuel take the largest hit by market share with almost a quarter of jet demand disappearing this year.

What’s next? Oil market watchers are closely tracking so-called high-frequency data sources, such as road congestion, to gauge the pace – and potential stalling – of the global oil demand recovery this year. Central to the focus has become the potential for a second-wave of COVID-19 infections which could severely delay the expected return of oil demand to its pre-crisis trajectory. Demand sensitivities from efforts to restrict and track passenger movements as international air travel slowly resumes are also a key pointer to when the tail end of the pandemic’s shadow over energy markets may fully lift.

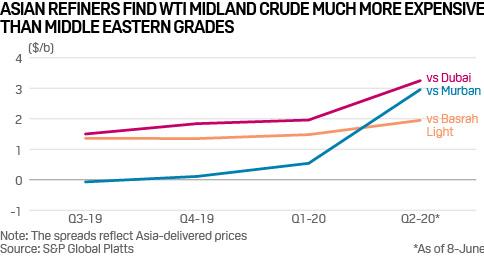

2. US crude exports to Asia soared early 2020, but face stiff price competition in Q2

What’s happening? Asia’s biggest US crude customer, South Korea, imported 53.76 million barrels from the US over January-April, up 34% year on year, latest data from state-run Korea National Oil Corp. showed. Thailand boosted its US crude imports over January-April by 75%, while Taiwan raised US imports by 2% year on year in Q1. However, Asia’s ample US crude intake does not reflect attractive US-Asia arbitrage economics or a full recovery in Asian oil demand. Spot trades for the US cargoes received so far happened before the pandemic, and were mainly due to Asian refiners’ rush to secure low-sulfur refinery feedstock late 2019, to produce IMO-compliant marine fuels.

What’s next? Asian refiners’ US crude imports could recede from Q3 as they no longer find WTI, Bakken and Eagle Ford grades attractive. This could help Middle Eastern producers lift sales to Asia when OPEC+ members roll back their output cut to 7.7 million b/d after July. S&P Global Platts data showed the spread between WTI Midland CFR North Asia basis and Abu Dhabi’s Murban Asia delivered basis has averaged $2.96/b to date in Q2, from 54 cents/b in Q1 and 11 cents/b in Q4 2019. The spread between WTI Midland and Iraq’s flagship Basrah Light on an Asia-delivered basis has averaged $1.95/b to date in Q2, widening from $1.48/b in Q1 and $1.35/b in Q4 2019. Despite the latest hike in Saudi OSP differentials for July-loading cargoes bound for Asia, many refiners would continue to favor Persian Gulf cargoes over US export grades, including WTI Midland and Eagle Ford, due to prevailing high long-haul freight rates.

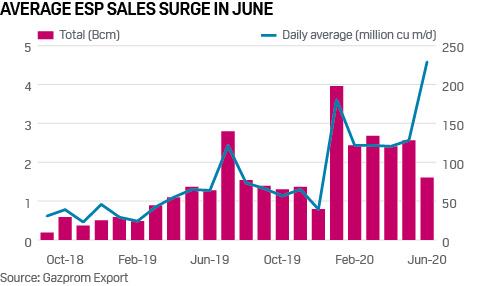

3. EU gas traders snap up Gazprom auction volumes for Ukraine storage play

What’s happening? Russia’s Gazprom Export has been making record high sales on its Electronic Sales Platform (ESP) so far in June, with average sales reaching almost 230 million cu m/d. While sales to its long-term contract holders in Europe are expected to fall this year, the ESP is offering the option to the market to buy alternative Russian gas during the daily auctions.

What’s next? A large amount of gas sold in recent weeks is for delivery in Q3 to Slovakia. This suggests market players are securing Russian gas volumes for delivery to the Slovakian virtual trading point with a view to then send to Ukraine for storage. Ukraine has around 13 Bcm of spare storage capacity and has made it easier and cheaper for European traders to store gas there — against the background of quickly filling storage sites elsewhere in Europe. The country is now seen as an “overflow” for European gas storage, helping to absorb some of the oversupply on the region’s gas market and possibly helping to prevent a further price collapse in the coming months.

4. French nuclear flexes amid weak demand; availability cuts boost forward price

![]()

What’s happening? French nuclear output peaks fell to 32 GW June 8 with two more reactors taken offline for extended maintenance. France’s nuclear generation plunged 22% on year in May to a record-low 33 GW for the month. French nuclear availability is not forecast to average above 30 GW before November, and only needs to average 29 GW for the remainder of 2020 to meet EDF’s reduced 300 TWh 2020 target, calculations by S&P Global Platts show. The fleet is demonstrating impressive price-responsive flexibility, meanwhile, ramping down to 23.2 GW June 6, as strong winds and low demand pushed west European spot power prices below zero.

What’s next? At least three more French reactors are scheduled to start maintenance this month, while final closure of the veteran Fessenheim 2 this month will reduce installed French nuclear capacity to 61 GW. The availability cuts have lifted French forward power prices, with Q4-20 now trading above Eur59/MWh on EEX, up 9% month on month. For the summer, price upside should be limited by cheap gas and healthy French hydro stocks, while system operator RTE has reassured consumers that winter supply is secure. This could potentially be at some cost, however, as the system operator turns to imports and up to 5 GW of demand side contracts with industrials if it turns chilly and electric heaters ramp up.

via ZeroHedge News https://ift.tt/3e6CegB Tyler Durden