Futures At All Time High As Target Reports Record Quarter

Tyler Durden

Wed, 08/19/2020 – 07:58

S&P futures edged higher, alongside European stocks, flirting with record highs and just shy of 3,400 following blockbuster earnings from retailers Target and Lowe’s, a day after the S&P 500 completed its fastest recovery from a bear market in history. The dollar headed for a sixth daily drop while Treasuries rose again, the 10Y yield sliding to 0.6477%.

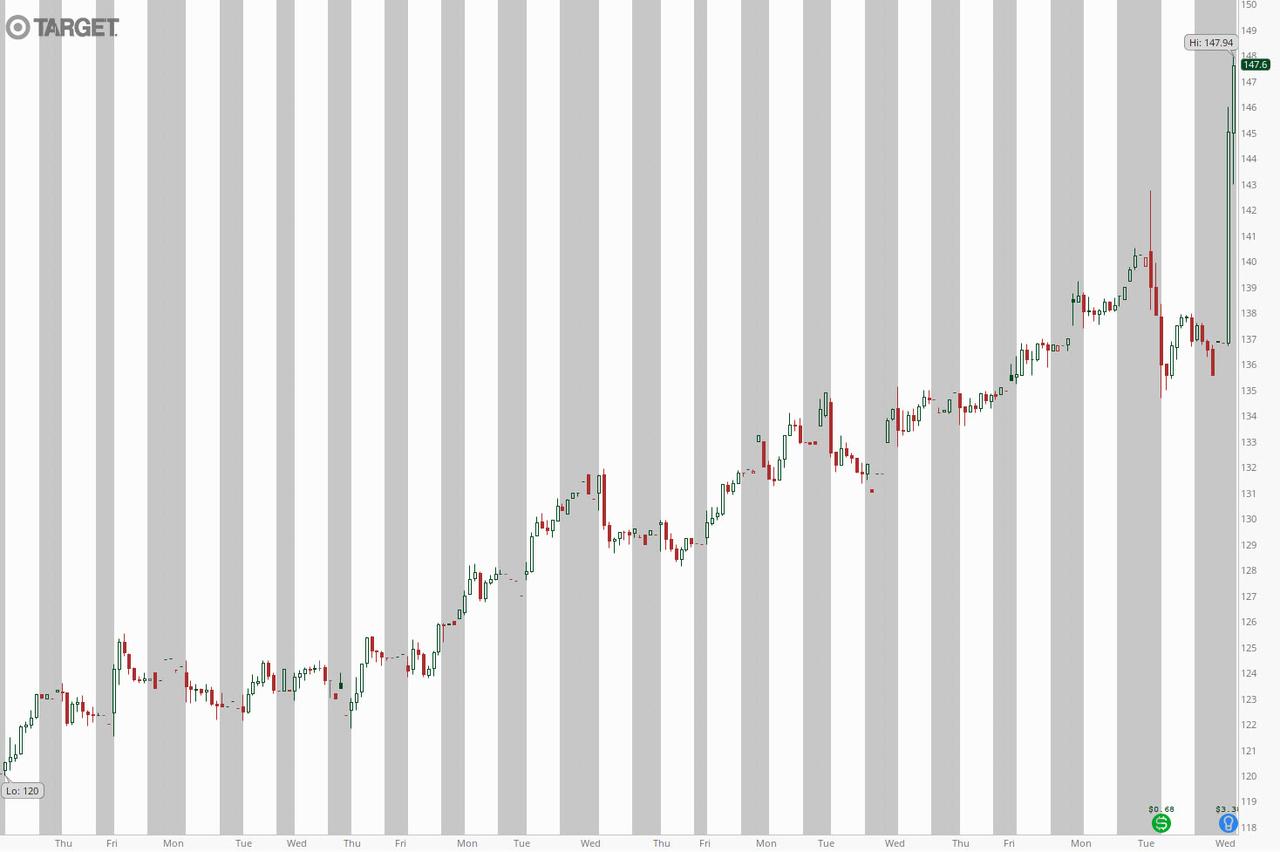

Target Corp soared in premarket trade to a record high of $150 after posting its best quarterly comparable sales growth on record and online revenues that nearly tripled. The supermarket operator reported second-quarter sales that smashed analysts’ expectations, brushing off concerns that demand would ebb after consumers spent their relief checks. Comparable sales rose a record 24% in the three months through Aug. 1, Target said Wednesday – the fastest pace in the retailer’s 58-year history, and almost three times higher than the average estimate of 8.6%. Adjusted earnings per share also touched an all-time high at $3,38, more than double the 1.58 expected, while revenue hit $22.98 billion, beating estimates of $19.82 billion. Additionally, the average Q2 transaction amount rose +18.8% vs. +0.90% y/y, while digital sales as share of total sales rose 17.2% in Q2 vs. 7.30% y/y.

Target CEO Brian Cornell said the retailer attracted consumers’ dollars because they couldn’t go on vacation or spend money on typical summer activities during the pandemic. “We’re not on planes. We’re not spending dollars on lodging, so many of those dollars have been redirected into retail,” he said in an interview with CNBC.

Home improvement chain Lowe’s Companies also jumped 2.7% after beating estimates for quarterly same-store sales as it benefited from a surge in demand for its products from consumers stuck indoors. Its larger rival Home Depot and retail behemoth Walmart reported similar results on Tuesday, although they reversed gains after warning that the Q2 selling frenzy was fading as stimulus payments were cut.

On Tuesday, the S&P 500 closed at a new record high, completing a stunning 50% recovery from a dramatic pandemic-led sell-off. The Nasdaq, the first of the three main indexes to confirm a bull market in June, also closed at an all-time high. Only the Dow remains some 6% below February’s record closing high. Yet while trillions of dollars in fiscal and monetary support and a preference for tech-related stocks have helped the benchmark surge about 55% from its March lows, the battered economy is still far from the pre-pandemic levels.

“We have a Federal Reserve that is all in, keeping rates low probably across the curve for as far as the eye can see,” Katie Nixon, chief investment officer at Northern Trust Wealth Management, said on Bloomberg TV. “That is supportive of higher valuations.”

In a positive signal for equities, Nancy Pelosi suggested that Democrats might be willing to make more cuts to their stimulus proposal to seal a deal with Republicans and speed Covid-19 relief. “The lack of fiscal progress has been a big driver of late and has taken the baton from what was initially a more virus-led story,” strategists including Craig Nicol at Deutsche Bank AG wrote in a note.

In Europe, the Stoxx 600 reversed early losses, gaining as health-care firms including AstraZeneca and Roche Holding led the index higher.

Earlier in the session, Asia stocks were mixed: sentiment was dampened after President Donald Trump said he called off last weekend’s trade talks. The State Department is also asking colleges and universities to divest from Chinese holdings in their endowments. Australia’s S&P/ASX 200 and South Korea’s Kospi Index rose; Japan’s Topix also gained 0.2% with Softbrain and TEMONA rising the most. Meanwhile, the Shanghai Composite Index retreated 1.2% pausing after recent gains, with Haiqi Transportation and Yijiahe Tech posting the biggest slides.

In FX, the Bloomberg Dollar index fell for a sixth consecutive day, but failed to breach its lowest level in over two years reached Tuesday as profit taking on short exposure was quickly offset by momentum and hedge funds looking to sell even the shortest of rallies. The pound edged higher amid firmer-than-expected U.K. inflation in July and managed to erase this year’s drop versus the greenback. U.S. corporate names and institutional accounts were among the main sellers of the euro around $1.1950 and the pound at $1.3260 on a take-profit basis.

The Aussie climbed, supported by higher iron ore prices, though rising tensions between Australia and China likely limited gains; the Kiwi led gains among Group-of-10 peers as short positions versus the Aussie were unwound. Japan’s yen halted a three-day gain to trade little changed after earlier strengthening toward 105 per dollar as offshore banks earlier sent the Japanese yen to day highs around 105.10, according to three traders in Europe.

The Yuan enjoyed a firm session as the recent Dollar weakness prompted the PBoC to set the CNY mid-point at a 7-month high, with today’s USD/CNY setting at 6.9168 vs. yesterday’s 6.9325. USD/CNH was driven lower during the APAC session and briefly traded sub-6.9000 for the first time since January.

In rates, Treasuries are higher across the curve led by the long end, while bunds gained amid record demand for 30-year German bond sale. Yields are lower by as much as 2.8bp at long end, 10-year by 2.1bp at 0.648%, with front-end yields little changed, flattening 2s10s and 5s30s by ~1.5bp; S&P 500 futures are little changed after cash index closed at a record high Tuesday. 10-year and 30-year yields, which climbed into last week’s record-size auctions of those tenors, are lower for a third straight day, both at lower yields (higher prices) than buyers in the auction obtained. On deck today, bond market prepares to digest a $25BN 20-year bond auction at 1pm ET.

An hour later, at 2pm the Fed is slated to release minutes of July 29 FOMC meeting, which will offer clues into the policymaker’s view of the economy and its actions in September, where Average Inflation Targeting is expected to be unveiled. The market’s focus will also shift to U.S. presidential elections, which is about 11 weeks away. Democrats on Tuesday formally nominated Joe Biden for president. The Republican National Convention is slated for next week.

Also on today’s calendar, Analog Devices, TJX and Nvidia are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.1% to 3,391.25

- STOXX Europe 600 up 0.1% to 367.64

- MXAP down 0.04% to 172.34

- MXAPJ down 0.2% to 568.35

- Nikkei up 0.3% to 23,110.61

- Topix up 0.2% to 1,613.73

- Hang Seng Index down 0.7% to 25,178.91

- Shanghai Composite down 1.2% to 3,408.13

- Sensex up 0.6% to 38,759.63

- Australia S&P/ASX 200 up 0.7% to 6,167.64

- Kospi up 0.5% to 2,360.54

- Brent futures down 1% to $45.01/bbl

- Gold spot down 0.6% to $1,989.88

- U.S. Dollar Index down 0.1% to 92.18

- German 10Y yield fell 1.9 bps to -0.482%

- Euro up 0.1% to $1.1943

- Italian 10Y yield fell 0.4 bps to 0.801%

- Spanish 10Y yield fell 0.6 bps to 0.304%

Top Overnight News from Bloomberg

- U.K. inflation accelerated to the fastest in four months in July, an unexpected jump that’s unlikely to last or persuade the Bank of England to ease off the stimulus pedal

- An auction of 30- year German debt saw the highest demand in the record books, which date back to 1997

- The Trump administration sees a possibility for Republicans and Democrats to agree on a smaller round of pandemic relief totaling $500 billion that would omit the biggest areas of disagreement, according to a senior U.S. official

- The $20 trillion U.S. Treasury market is giving the Federal Reserve a thumbs-up for its efforts to revive inflation after the coronavirus pandemic threatened to inflict a damaging bout of deflation on the U.S. economy

- Japanese exports continued to drop steeply in July even as a recovery in shipments to China helped cushion declines to Europe and other key markets where the coronavirus is spreading rapidly

A quick rundown of global markets courtesy of NewsSquawk.

Asian equity markets sustained the mixed lead from their counterparts on Wall St where the S&P 500 and Nasdaq notched fresh record intraday highs shortly after the open, although the tone briefly soured before picking back up again with participants somewhat tentative and volumes thinner due to the lack of data and risk events ahead. Nonetheless, ASX 200 (+0.7%) was positive with the best performing stocks in the index driven by earnings, while Nikkei 225 (+0.3%) was rangebound as participants digested mixed releases including disappointing Machinery Orders and although trade data printed better than expected, there were still substantial contractions to both Exports and Imports. Elsewhere, Shanghai Comp. (-1.2%) weakened alongside the closure of morning trade in Hong Kong due to a typhoon signal, ultimately, Hang Seng (-0.7%); as well as the continued antagonism between US-China as President Trump noted that he postponed talks with China and does not want to talk with China right now, while he responded “we’ll see“ when questioned if he will pull out of the trade agreement. Finally, 10yr JGBs were choppy with mild pressure seen as Japanese stocks just about remained afloat, but with downside also stemmed amid the BoJ presence in the market for JPY 770bln of JGBs with 3yr-10yr maturities.

Top Asian News

- Japan Exports Drop Steeply Again as Virus Continues Spread

- Bank Indonesia Holds Rates Steady to Safeguard Weak Currency

- China Stocks Post Biggest Loss in Three Weeks on U.S. Tensions

European equities trade with little in the way of firm direction (Eurostoxx 50 +0.3%) with ongoing pessimism surrounding US-China relations and stimulus talks in Washington unable to impose any meaningful sway on summer-thinned European markets. Price action thus far has been more of a case of treading water ahead of the US entrance to market, although Europe has seen a modest pick-up in recent trade as indices across the Atlantic continue to eye record highs. From a sectoral standpoint in Europe, energy names are a laggard in-fitting with price action in with some of the modest losses seen in the complex, albeit downside is relatively small in terms of magnitude. Elsewhere, some of the travel & leisure names such as IAG (+2.9%), easyJet (+0.5%) and Ryanair (+0.9%) began the session on a slightly firmer footing amid reports in UK press that Heathrow could expand its testing capabilities in an attempt to replace the imposition of blanket quarantines. Utility names are seen lower in Europe amid losses in RWE (-4.0%) with the DAX-constituent having completed a USD 2bln share issue to support its expansion into renewable energy. Of note for the DAX, investors are awaiting the release of the updated composition of the index at 21:00BST today with reports suggesting that Wirecard could be replaced by Delivery Hero (+0.8%). Maersk (+4.7%) have been a standout outperformer thus far following its Q2 earnings release, in which the Co. beat on estimates for profits and subsequently reinstated guidance at a higher level than indicated previously.

Top European News

- Billionaire Greensill’s German Bank Draws Regulatory Scrutiny

- Galapagos Suffers Biggest Fall Ever as FDA Fails to Approve Drug

- The Best Days May Be Over for Europe’s Stock Rally This Year

- U.K. Is Working on Covid Tests at Airports to Ease Quarantine

In FX, The broader Dollar and index are losing steam as the APAC consolidatory strength, which reverberated into early European hours, fades ahead of the FOMC Minutes (Full preview available in the Research Suite). DXY found an overnight base at 92.150 ahead of the YTD low at 92.124, with the index now residing closer to the middle of the current 92.150-92.388 intraday band.

- NZD, AUD, CAD – The non-US Dollars posted various degrees of resilience vs. the Buck in overnight trade and have since extended on gains as the Dollar wanes. NZD/USD outperforms in the G10 FX space after finding support at the 0.6600 mark before topping its 21 DMA at 0.6621. AUD/USD gains in tandem after breaching mild resistance around 0.7237-43, but market participants eye a sustained break above the 200 WMA at 0.7255 ahead of the Feb 2019 weekly high at 0.7295. Meanwhile, the Loonie ekes mild gains despite losses in the crude complex with potential technical factors at play – USD/CAD drifted below its 200 DMA (1.3169) overnight before dipping under 1.3150 as it eyes the release of Canadian CPI later today.

- GBP, EUR – Both marginally firmer against the USD, although the former saw some fleeting strength on the back of UK CPI metrics notably topping forecasts across the board, mainly due to a less significant decline in clothing prices alongside the easing of lockdown restrictions. Cable meanders around mid-range after printing a post-CPI high of 1.3267 (low 1.3230) ahead of the Dec 31st 2019 high of 1.3283. EUR/USD meanwhile remains within recent ranges and moves in tandem with the USD, having had shrugged off Final CPI figures heading into the European summit on Belarusian sanctions, albeit EU diplomats noted that these are unlikely to be agreed on until the end of this week at the earliest. Note: EUR/USD sees a hefty EUR 1.7bln in options expiring at strike 1.1900 at the NY cut.

- CHF, JPY – Mixed trade between the CHF and the JPY, with the former compliant to USD-action and the latter flat after a choppy APAC session amid mixed data and an absence of clear sentiment. USD/CHF inched closer towards 0.9000 to the downside, with yesterday’s low residing at 0.9008. USD/JPY remains sub-105.50 after rebounding from an overnight base at 105.11, with the pair seeing USD 762mln in options rolling off at 105.00 and USD 800mln scattered between 105.25-30. For the technicians, if 105.00 fails to hold then focus will turn on 104.86 which marks the 76.4% Fib of the Jul-Aug rise.

- Yuan – A firm session for the Yuan as the recent Dollar weakness prompted the PBoC to set the CNY mid-point at a 7-month high, with today’s USD/CNY setting at 6.9168 vs. yesterday’s 6.9325. USD/CNH was driven lower during the APAC session and briefly traded sub-6.9000 for the first time since January.

In commodities, WTI and Brent October futures have been edging lower in early European trade as participants eye the fallout of the JMMC meeting poised to commence from 15:00BST. Although no fireworks are expected from the meeting, market chatter yesterday noted of a possible recommendation of an early taper of the output cut deal, speculations that were dismissed by Russian Energy Minister Novak last week. Focus will likely fall on the laggards’ compliance levels amid pledges to over-comply to make up for their earlier shortfalls, whilst commentary on the JMMC’s outlook will also garner attention given resurging COVID-19 cases. Alongside the meeting, the weekly EIA inventories will be released, with headline crude forecast to have fallen 2.670mln barrels in the past week after private inventories printed a larger than expected draw of 4mln barrels vs. Exp. -2.7mln – with prices shrugging off the release. Elsewhere, Eastern Libyan authorities are to allow limited and temporary exports from the blockaded oil ports in a bid to free up storage to allow fuel production for fire stations. The blockades have resulted in a build-up in condensates and the reduction of gas production used for power stations. In terms of precious metals, spot gold and silver largely move in tandem with the Dollar amidst a lack of fresh catalysts, with the former meandering just under USD 2,000/oz and the latter just north of USD 27.50/oz. UBS remains constructive on gold over the next 6-month, with its base case is at USD 2,000/oz and an upside case of USD 2,200-2,300/oz, whilst UBS’ silver upside case resides around USD 30-40/oz. Over to base metals, Dalian iron ore continued to rise amid firm demand from China as steel mill outputs remain near record levels. However, analysts at ING note that as uncertainties over Brazilian supply subsides, the bank expects prices to ease. Meanwhile, copper prices gain as mining giant Rio Tinto lowered its copper guidance to 135k-175k tons from 165k-205k tons.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 6.8%

- 2pm: FOMC Meeting Minutes

DB’s Craig Nicol concludes the overnight wrap

Much of the focus in markets over the last 24 hours has been on yet another leg lower for the dollar. Indeed the dollar index fell -0.62% yesterday – good for a fifth consecutive daily decline – and to the lowest level since April 2018 with the move fairly broad across most major currency pairs with the euro in particular above $1.19 for the first time since May 2018. The lack of fiscal progress has been a big driver of late and has taken the baton from what was initially a more virus-led story. Mnuchin’s comment yesterday about not knowing why a deal seems so far off didn’t do much to help, as did comments from Walmart’s CFO about potential earnings pressure ahead with the end of stimulus checks.

There was one glimmer of good news on the fiscal front late in the US session though, when House Speaker Pelosi indicated that Democrats could pullback their stimulus demands to cut a deal with Republicans now before introducing additional bills after the November elections. With all that in mind it’ll be interesting to see if the FOMC minutes today change the narrative at all with monetary policymakers recently reiterating the need for further fiscal support.

A reminder that at the meeting, Powell noted that the Committee aims to wrap up the policy review in the “near future”, which would be consistent with our economists’ expectation that the results of this review will be released at the September meeting. The minutes should give a sense as to what kind of issues were discussed at the July meeting and how close the Committee is to announcing any changes to how they conduct monetary policy. So, worth keeping an eye on.

Ahead of that the S&P 500 finally closed at an all-time high last night, finishing up +0.23%. The NASDAQ also hit a fresh record high of its own, following a further +0.73% advance. While the weaker dollar certainly helped, the US housing data for July also played a part. Indeed the number of housing starts rose to an annualised 1.496m (vs. 1.245m expected), while building permits also rose to 1.495m (vs. 1.326m expected), in a move that puts them basically back at their pre-Covid levels. It was a somewhat tentative rally again though, with roughly 67% of the S&P down on the day and the majority of the move was driven by retail and communications stocks.

Of course it wouldn’t be a recap without another round of US-China trade headlines. Late last night, President Trump said that he cancelled last weekend’s talks with China, saying “I don’t want to talk to China right now”. He also said “we’ll see what happens” when addressing whether the US would pull out of the phase one trade deal. Prior to this the US administration said that it wants university endowments to divest Chinese holdings, saying it would be “prudent” to get ahead of potentially more onerous measures on holding the shares including a wholesale de-listing of PRC firms from U.S. exchanges. The State Department letter also warned universities of China’s growing influence on campuses and said the US is accelerating investigations of what it called “illicit PRC funding of research, intellectual property theft and the recruitment of talent”.

The Shanghai Comp -0.30%, Shenzhen Comp -0.86% and CSI -0.54% are all lower in response overnight. In contrast, the Nikkei (+0.37%), Kospi (+0.89%) and ASX (+1.10%) are up while the Hang Seng is yet to reopen as we go to print after scrapping the morning session following a typhoon alert. Futures on the S&P 500 are also up with +0.17% gain while spot gold is back below $2000/oz, and bond markets are a touch stronger.

Back to yesterday, where along with the weaker dollar, treasuries continue to unwind some of last week’s selloff. Indeed 10y yields fell by -2.0bps and measures of the curve including 2s10s and 5s30s have now retraced -3.9bps and -3.4bps of the +12.9bps and +15.0bps respective steepening last week. It was a stronger day for bonds in Europe too where 10y bunds closed -1.2bps lower however equity markets closed at their lows for the session – the STOXX 600 down -0.56% – not helped by the stronger euro and also deteriorating virus news including German Chancellor Merkel warning that the recent increase in cases meant that it wouldn’t be possible to ease restrictions further. German cases doubled in the last 3 weeks and are now seeing the highest daily increases in infections in nearly four months. Elsewhere, Amsterdam has increased scrutiny of bars and restaurants to ensure they adhere to guidelines as the number of new cases is on the rise. In Asia, South Korea reported 297 additional cases in the past 24 hours, marking the biggest daily increase since March.

In other virus news, trackthrecovery.com’s updated small business stats in the US showed a continued downward trend through August 7. Small businesses open are now roughly 20% below pre-virus levels and are near the lowest since mid-May. Job postings, while very volatile, fell to near a low for the recession period being down -36%. These stats lines up well with the NY Fed survey that came out yesterday, which could point to lower ISM service index numbers this month. Cases overall in the US rose 0.8% yesterday, in-line with the 0.9% 7-day average.

To the day ahead now, and the data highlights include the UK’s CPI reading for July, the Euro Area’s current account for June, along with Canada’s CPI for July. From central banks, the Fed will be releasing the minutes from their latest meeting and we’ll hear from Richmond Fed President Barkin. Finally, the Democratic vice presidential nominee Kamala Harris will be speaking at the party’s convention.

via ZeroHedge News https://ift.tt/3h6mRX3 Tyler Durden