“Smart Beta” Is Actually Still Just Dumb Money: New Study Reveals The Quant Strategy To Be A “Mirage”

Tyler Durden

Fri, 09/04/2020 – 12:35

Color us not surprised that that dumb money, even if it invests in “smart beta”, is still really just…dumb.

A new study called “The Smart Beta Mirage”, released this summer by collaborators at the University of Washington, Michael G. Foster School of Business and The University of Hong Kong, Faculty of Business and Economics, has all but debunked the idea of “smart beta”.

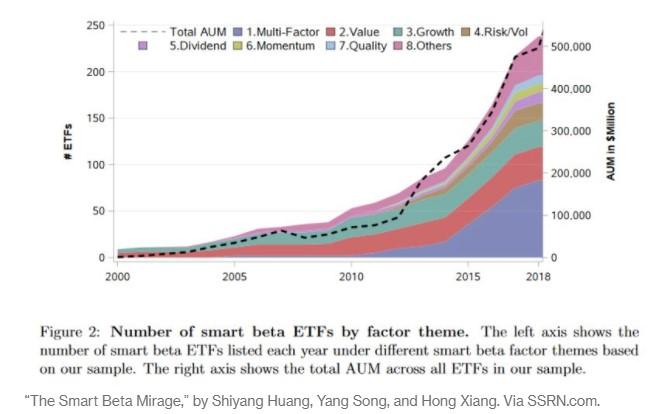

Fueled by the notion that historical quantitative data can somehow give you an edge to passive investing, smart beta strategies “seek to passively follow indices, while also considering alternative weighting schemes such as volatility, liquidity, quality, value, size and momentum,” according to Investopedia. Long story short, it is a fancy term that allows ETF owners to charge higher fees by claiming they are doing something technologically brilliant that most of their semi-conscious customers wouldn’t understand if they lived to be 150.

But that gravy train appears it is ending. Ever see those disclaimers on Wall Street that say “past performance is not indicative of future results”? Those pushing “smart beta” products would do well to give these types of disclaimers a read on the daily.

Why? Because the study found that strategies that worked great according to their historical data simply don’t work going forward.

The abstract reads: “We document sharp performance deterioration of smart beta indexes after the corresponding smart beta ETFs are listed for investments. Adjusted by aggregate market return, the average return of smart beta indexes drops from 2.77% per year ‘on paper’ before ETF listing to −0.44% per year after ETF listing.”

It continues: “We find evidence of data mining in constructing smart beta indexes as the post-ETF-listing performance decline is much sharper for indexes that are more susceptible to data mining in backtests. Our results caution the risk of data mining in the proliferation of ETF offerings as investors respond strongly to the stellar performance in backtests.”

Similarly, Vanguard published a white paper in 2012 that found similar results, according to Bloomberg: “…indexes created for fund launches using backfilled performance data, in which most fared well before inception…generated weaker returns once turned into ETFs.”

But this hasn’t stopped “smart beta” from becoming more than 20% of the U.S.’s $4.8 trillion dumb money ETF market.

Because if there’s one thing this Fed-rigged market has shown us, it’s that facts, evidence, numbers and data have all but become completely meaningless.

via ZeroHedge News https://ift.tt/331f5bd Tyler Durden