Futures Rebound As Tech Gains; Powell, Mnuchin To Speak In Congress

Tyler Durden

Tue, 09/22/2020 – 08:01

US equity futures bounced on Tuesday alongside European shares, with beaten-down shares of technology-related companies leading early gains, while Dow futures were subdued on uncertainty over more U.S. fiscal stimulus; Treasurys were flat and the dollar dropped before Fed Chair Powell and Treasury Secretary Steven Mnuchin speak later in the day at a Congressional panel.

Early premarket gainers on Tuesday included Microsoft, Apple, Amazon.com, Alphabet and Facebook all of which have dominated Wall Street’s rally since a coronavirus-driven crash in March. Amazon was upgraded to Outperform by Bernstein with a $3,670 price target, after analyst Mark Shmulik wrote that the pandemic “has pulled forward secular trends, from e-commerce to digital advertising and Cloud, with Amazon as a primary beneficiary across all three revenue pools” adding that e-commerce “has permanently inflected,” and that investments made by the company had positioned it well for the long term. AMZN shares are up 1.7% premarket.

Tesla fell 3.4% after Elon Musk warned about the difficulties of speeding up production as an expert cautioned the carmaker’s increased reliance on large-scale aluminum parts could bring new manufacturing challenges. Oracle shed 1.2% on report that Beijing was unlikely to approve a proposed deal by the software maker and Walmart for ByteDance’s TikTok. Carnival Corp lost 1% after the cruise operator announced sale of its two Princess Cruises ships – Sun Princess and Sea Princess – to undisclosed buyers.

“The market may be taking a breather but I would be surprised if that was it,” said Rabobank’s Head of Macro Strategy Elwin de Groot, referring to Monday’s rout that came as countries had been forced to reintroduce some of the COVID-19 restrictions they removed over the summer. “The market won’t like it. The base case was that the second wave wouldn’t be as bad as the first… but the fourth quarter will be now another quarter with stringent restrictions and there are going to be an increasing number of economic victims,” he said.

All three main Wall Street indexes started the week on the back foot amid a stalemate in Congress over the size and shape of another coronavirus-response bill, rising Covid-19 cases in a number of nations and predictions of market volatility around the presidential election dented hopes of a swift economic recovery.

“Some money is being taken off the table pre-election, and as we approach elections in the next six weeks I think there will be more of this happening,” Saed Abukarsh, senior executive officer at Ark Capital Management Dubai Ltd., told Bloomberg Television. “We’re now consolidating into a lower range in the S&P.”

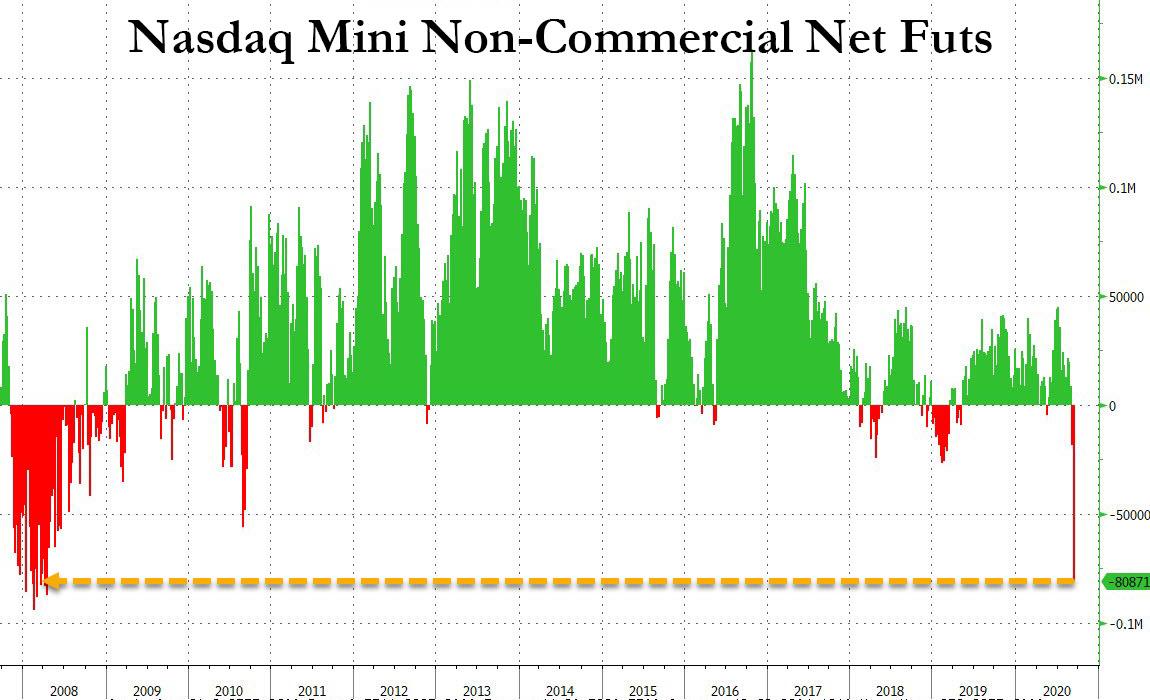

U.S. stocks have tumbled over the past three weeks as investors dumped heavyweight technology-related shares following a stunning rally that lifted the S&P 500 and the Nasdaq to new highs. On Monday, the S&P 500 closed down 9% from its Sept 2 record high, just above correction territory. JPMorgan and Bank of New York Mellon fell 3.1% and 4.0% respectively on Monday too. Meanwhile, a furious bearish reversal in Nasdaq sentiment as measured by Nasdaq 100 mini futures, leaves the door open for another dramatic short squeeze.

Indeed, the squeeze may have started late on Monday when the growth-linked technology sector was the only one to post gains in the previous session following a dramatic surge in the last hour of trading led by Apple (buybacks), while value-oriented sectors such as industrials, energy and financials tumbled about 3%.

European markets clawed back some ground on Tuesday, a day after rising second waves of the coronavirus epidemic caused the region’s biggest wipeout since June and drover investors back to government bonds. Europe’s STOXX 600 index made back 0.6% of the 3.2% it lost on Monday, its biggest drop in three months, helped by respective 1.5% and 0.6% gains for the tech and healthcare sectors. Travel and leisure stocks saw 0.3% falls to add to Monday’s 5.2% plunge, however, and as investors stayed close to safety, yields on Germany’s government bonds held near six-week lows and the dollar rose.

In the UK, the FTSE 250 index fell 0.3%, contrasting with the bounce back for other European indexes, with the domestically-focused U.K. benchmark pulled down by insurers and travel stocks amid increasing Covid-19 restrictions. The decline is in contract to Stoxx 600 +0.5% and FTSE 100 +0.3%. Insurers were among the biggest fallers in FTSE 250, hit by both a poorly-received update from Lloyd’s insurer Beazley and by a regulatory crackdown on motor and home policy pricing.

UK Prime Minister Boris Johnson spoke in Parliament where he encouraged Britons on Tuesday to go back to working from home, along with announcing a 10pm curb on pubs, bars and restaurants. This came as France saw its seven-day daily rolling case count rise above 10,000 for the first time over the weekend, Italy introduced more mandatory testing and Germany describe the situation as “worrying”.

Earlier in the session Asian stocks also dropped, with South Korea and China bourses pulling Asia down for a second day after the tech-heavy Nasdaq fell out of its recent stellar range. Australia’s S&P/ASX 200 had dropped 0.7%, pressured by miners and energy stocks and the Aussie dollar fell to a one-month low while Hong Kong’s Hang Seng index had closed down nearly 1%. Japanese markets were closed for a public holiday but early trading indicated a subdued day in store for Wall Street, with S&P 500 futures down 0.18% and Nasdaq 100 futures flat%.

Beyond the impact of the virus, Hong Kong shares of HSBC and Standard Chartered weakened a further 2%, after leaked reports showed they were among global lenders that have transferred more than $2 trillion in suspect funds over nearly two decades.

“Markets globally have run hard on the weight of huge liquidity, so it’s not surprising to see a pullback in some valuations,” said James Rosenberg, an EL&C Baillieu advisor in Sydney. “Add in uncertainty with U.S. elections and another COVID wave in Europe … it unsettles investors.”

Fed Chair Jerome Powell said the U.S. economy is improving but has a long way to go before fully recovering. Powell will face lawmakers Tuesday along with Treasury Secretary Steven Mnuchin to discuss the need for more stimulus

In FX, the dollar pared an early advance against G-10 peers, and Treasuries were little changed. The greenback was modestly lower against most G-10 peers while the Bloomberg Dollar Spot Index consolidated near the higher end of the range it’s been trading in over the past month. The pound pulled back from a two-month low after the delayed prospect of negative interest rates replaced concerns about new U.K. restrictions to contain the coronavirus. The Norwegian krone fell a fourth day against both the dollar and the euro, despite improved sentiment and stabilizing oil prices; the currency neared 11 per euro, a level unseen since in more than three months.

Overnight, the Swedish central bank kept the repo rate at 0% and left its rate path unchanged in a decision that was widely expected and there were no real surprises, suggesting that Sweden will have a zero rate at least through the third quarter of 2023. The central bank stayed the course and continues to view its historic asset purchase program as the main tool to support the economy during the current crisis. The bank still left the door open for a rate cut, and highlighted eroding confidence in its 2% inflation target as something that could force it to take the rate below zero again, according to Bloomberg. The Riksbank cut its inflation forecast slightly for the next couple of years but it still believes CPIF inflation will rise to 1.8% in 2023.

In rates, treasuries held steady before Federal Reserve Chair Jerome Powell and U.S. Treasury Secretary Steven Mnuchin speak later in the day at a Congressional panel. Bunds were steady, in line with Treasuries, and European peripheral spreads tightened, in another sign of steadying market sentiment. Italian bonds rallied after the country’s governing coalition saw off right-wing parties in regional elections, sending borrowing rates to the lowest level since February.

In credit, investment-grade credit was resilient in the selloff while high- yield bond spreads widened the most since June, and leveraged loan prices fell the most since then. HYG, the largest high-yield ETF, suffered its largest one-day outflow since February.

In commodities, gold fell against the rising dollar, and traded at $1,908.76 per ounce, while in oil markets, Brent gained 0.4% to $41.65 and U.S. crude rose 0.5% to $39.5 per barrel.

Expected data include existing home sales. AutoZone, Aurora Cannabis and Nike are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.1% to 3,277.75

- Stoxx Europe 600 up 0.6% to 359.11

- MXAP down 0.7% to 171.19

- MXAPJ down 1% to 556.65

- Nikkei up 0.2% to 23,360.30

- Topix up 0.5% to 1,646.42

- Hang Seng Index down 1% to 23,716.85

- Shanghai Composite down 1.3% to 3,274.30

- Sensex down 0.6% to 37,817.78

- Australia S&P/ASX 200 down 0.7% to 5,784.07

- Kospi down 2.4% to 2,332.59

- Brent futures up 1.3% to $41.99/bbl

- Gold spot down 0.3% to $1,906.83

- U.S. Dollar Index little changed at 93.69

- German 10Y yield rose 0.9 bps to -0.521%

- Euro down 0.2% to $1.1744

- Italian 10Y yield fell 4.3 bps to 0.713%

- Spanish 10Y yield fell 1.3 bps to 0.24%

Top Overnight News from Bloomberg

- The U.K. government is telling the public to work from home again if possible, as Prime Minister Boris Johnson prepares to announce new restrictions on bars and restaurants in a bid to halt a surge in coronavirus cases

- The Bank of England isn’t close to negative interest rates despite the resurgence of the coronavirus reinforcing economic risks, according to Governor Andrew Bailey. While the bank has “looked hard” at rate cuts and negative rates are in the toolbox, planned technical work on the policy is to examine whether it can be implemented rather than a signal it is coming, he said.

- Sweden’s Riksbank stuck with a forecast of years of zero interest rates, and pledged to continue its historic asset purchase program as it navigates its way through the Covid crisis

- Hotels, pipelines, convenience stores and automaker bonds are among the assets being bought by some of the world’s biggest asset managers as they look for value in a world thrown into turmoil by the coronavirus pandemic

A quick look at global markets courtesy of NewsSquawk

Asian equity markets were lower across the board with weakness stemming from the uninspiring performance in global peers after risk appetite in Europe was dragged by pandemic-related concerns and with spillover selling on Wall St where the DJIA briefly slumped below the 27,000 level and registered losses of over 500 points, although a late resurgence in tech helped the Nasdaq 100 finish in the green. ASX 200 (-0.7%) was pressured by underperformance in mining names and losses in the largest weighted financials sector as some of the Big 4 banks could reportedly face increased scrutiny in light of the recent FinCEN revelations, but with downside limited by resilience in tech and defensives. Japanese markets remained closed for Autumnal Equinox holiday and KOSPI (-2.4%) suffered amid the broad risk aversion, but with some bright specks seen including Samsung Biologics which was awarded a USD 331mln supply agreement with AstraZeneca. Hang Seng (-1.0%) and Shanghai Comp. (-1.3%) were negative with HSBC and Standard Chartered extending on the losses related to the recent money laundering allegations and with dark clouds looming over the TikTok deal after US President Trump warned the US will not approve the deal if Walmart and Oracle do not control the company and China’s Global Times editor Hu Xijin suggested that Beijing won’t approve the current agreement as it would endanger China’s national security, interests and dignity. Tensions regarding Taiwan also continues to polarize ties between the world 2 largest economies with China’s Foreign Ministry announcing to take countermeasures against high ranking US officials due to their visits to Taiwan, and China’s military released a video which showed a simulated attack on an island which resembled Guam. Nonetheless, the losses in Chinese markets were only moderate amid PBoC liquidity efforts in which it conducted a total net injection of CNY 350bln.

Top Asian News

- Indonesia Sees Economy Contracting for First Time Since 1998

- Reliance Is Said to Plan Big Smartphone Push After Google Deal

- ZTO Express Said to Raise $1.27 Billion in Hong Kong Listing

Overall a firmer picture in Europe (Euro Stoxx 50 +0.8%), but with the gains seen in early hours somewhat stalled, and waning for some bourses, whilst US equity futures also see a mixed performance, with the ES and YM flat, and NQ outperforming. Individual indices in Europe seem to be more influenced by sectoral performance, with Germany’s DAX (+1.0%) outperforming peers as the tech sector outpaces on tailwinds from the yesterday’s State-side tech rally into the close. This sees tech behemoth SAP (+2.0%) as a top performer in the German index, with the Co. also accounting for ~5.8% of the Euro Stoxx 50, whilst ASML (+2.9%) represents almost 6% of the European index. Meanwhile, Spain’s IBEX (-0.2%) resides in negative territory as Travel & Leisure underperforms on continuing woes over the implications of renewed lockdown measures for the sector. CAC 40 (+0.3%) is weighed on by Airbus (-3.5%) and Accor (-2.5%), with the former on the back of CEO comments who could not guarantee that there will not be any compulsory layoffs, whilst the latter is pressured by the aforementioned COVID-19 updates. In terms of individual movers, Austrian listed ASM (+4.3%) outperforms the tech sector amid source reports that its Hong Kong listed ASM Pacific Tech is in discussions with potential investors to help take the group private. Meanwhile, tobacco names Imperial Brands (+2.7%) and British American Tobacco (+3%) are underpinned by positive broker moves by RBC.

Top European News

- Deutsche Bank CFO Signals Preference for Cross-Border Mergers

- BOE’s Bailey Plays Down Chance of Negative Rates on Virus Risks

- Europe Finds Mass Testing Is No Panacea for the Coronavirus

- Riksbank Affirms QE as Preferred Tool to Fight Covid Crisis

In FX, although broad risk sentiment has stabilised somewhat after Monday’s meltdown, the Dollar remains in firm recovery mode as major and EM currency rivals continue to flounder alongside precious metals. Indeed, following a short-lived and shallow bout of consolidation, the DXY rebounded to 93.893, and perhaps tellingly from a technical or momentum perspective, after the index found a base and underlying bids just ahead of the 93.500 level having spent so long anchored around 93.000.

- GBP/SEK/AUD – Sterling looked all set and resigned to losing 1.2700+ status vs the Buck and extend declines through 0.9200 against the Euro after BoE Governor Bailey said the MPC has looked very hard at the scope of reducing the Bank rate further, and including lowering the benchmark below zero, but caveated that the BoE needs to know more about the technicalities and application of NIRP, as other countries that have adopted negative rates have seen mixed ramifications. However, the real kicker for Sterling bears and shorts came with his warning to markets about not reading too much into last Thursday’s statement when it was revealed that structured research about the operational aspects of implementing NIRP would begin with the PRA. Cable has now turned full circle and more having ‘breached’ a series of MA levels on the way down to around 1.2715 and tripped a few stops at 1.2825 before fading just ahead of 1.2840, while Eur/Gbp has retested yesterday’s sub-0.9150 low compared to a circa 0.9220 peak. Conversely, the Swedish Crown is sitting tight within a 10.4290-10.3845 range vs the single currency after another rock steady message from the Riksbank that the repo rate is projected to be held at the current 0% mark for the forecast horizon (out to the 3rd quarter of 2023), albeit with the option to cut if required. Elsewhere, the Aussie has been undermined and briefly under 0.7200/at 1.0800 against its US and NZ peers in wake of remarks from RBA Deputy Governor Debelle effectively covering all potential policy stimulus measures if needed, including longer-dated QE, easing the cash rate from 0.25% towards zero or through parity and direct FX intervention to weaken the Aud, though the latter may not be an effective instrument as it is aligned with fundamentals.

- EUR/CHF – Both succumbing to the ongoing Greenback revival, with the Euro now propping up the major ranks following a deeper retreat through 1.1800 and Monday’s trough to circa 1.1720. Note, decent option expiry interest is also capping Eur/Usd as 1 bn rolls off between 1.1770-80 and another 1.4 bn sits from 1.1815-20. Similarly, the has pulled back further from recent highs within a 0.9142-73 band as the clock ticks down to Thursday’s SNB confab.

- JPY/CAD/NZD – The Yen continues to ‘outperform’ or at least hold up better than other G10s without the normal depth of volume due to Japanese markets observing another holiday today. Nevertheless, Usd/Jpy has settled into a higher range either side of 104.60 after the severe test of 104.00 yesterday was defended staunchly. Meanwhile, the Loonie appears to have found underlying buying interest into 1.3350 vs its US counterpart alongside steadier crude prices and the Kiwi is straddling 0.6650 in advance of the RBNZ on Wednesday.

- NOK/EM – In keeping with other oil fired or dependent currencies, the Nok has derived some traction alongside the commodity, but not before sliding towards 11.0000 vs the Eur, while the Try has fallen irrespective of a marked improvement in Turkish consumer confidence.

In commodities, WTI and Brent front month futures have nursed overnight losses and currently eke mild gains in price action that coincides with upside in the stock markets, despite the DXY holding onto yesterday’s gains. News flow for the complex has remained light in early European hours, although overnight newsflow from Libya’s NOC noted that total output is expected to reach 260k BPD next week from Thursday’s touted output of 220k BPD. In terms of ramifications for OPEC, sources yesterday noted that OPEC needs time to observe whether the output in Libya is sustained before assigning a quota to the exempt country under the OPEC+ deal. Furthermore, OPEC delegates via FT voice concern about the local lockdowns in Europe and rising cases in India, whilst also warning that crude and petroleum product stockpiles are not depleting as fast as initially thought. One delegate said, “we might have to [act] soon”. Elsewhere over in the Gulf of Mexico, Beta remains a Tropical Storm – with no current hints of it evolving into a hurricane, but the NHC notes that there is the danger of life-threatening storm surge near time of high tides today along portions of the Texas and Louisiana coasts. WTI Nov resides around USD 40/bbl (vs. low USD 39.36/bbl), while its Brent counterpart meanders just under 42/bbl (vs. low 41.26/bbl). Elsewhere, spot gold and silver see modest losses as precious metals succumb to the Dollar, with the yellow metal oscillating on either side of USD 1900/oz whilst spot silver lost its USD 25/oz status and trades closer to USD 24/oz. In terms of base metals, LME copper recouped some of yesterday’s losses as the red metal tracks the gains in stocks, with some also attributing gains to firm demands from China. Finally, Dalian iron ore futures added to yesterday’s losses amid a continuation of the theme of lower than expected demand for the steel-making material.

US Event Calendar

- 10am: Existing Home Sales, est. 6m, prior 5.86m

- 10am: Existing Home Sales MoM, est. 2.39%, prior 24.7%

- 10am: Richmond Fed Manufact. Index, est. 12, prior 18

DB’s Jim Reid concludes the overnight wrap

Regular readers may be mildly amused to learn that I tweaked my upper back yesterday. To understand how we have to go back to when new US Golf Open Champion Bryson DeChambeau came back from lockdown around 20lbs heavier (45lbs in a year) and hitting the golf ball an absurd amount further. At that point in June I decided I needed to strengthen my body to get to the next level with the beautiful but utterly soul destroying game of golf. I’d been having regular lower back and hip problems. So I’ve been doing core training for three months and now have the first signs of 1-pack developing and have massively improved my glutes and hamstrings. Now that was I more stable I decided it was time to move onto the upper body after consultation with a physio. However within one set of a “Prone Mid-Trapezius Dumbbell Raise” I felt something tweak between my shoulders and I think I’ll need to rest for a few days now. So my bulking up and ripping it further with the driver strategy will have a wait a few more days. Sigh.

Markets also broke down yesterday as renewed fears over the coronavirus, a sharp global bank equity slump and numerous other headwinds led to a sharp sell-off in global risk assets, with travel and leisure stocks among the worst performers as investors grappled with the prospects of further restrictions being imposed. The US rallied back a bit into the close but Europe saw large declines, with the STOXX 600 down -3.24% in its worst daily performance since June 11. The travel and leisure sector fell by an even larger -5.20%. Every sector in the index moved lower on the day however, and no country was immune either, with the DAX (-4.37%), the CAC 40 (-3.74%) and the FTSE MIB (-3.75%) all losing major ground. European banks lost -6.30% and led the decliners as the weekend leaks around past suspicious activity reports heavily weighed.

US banks were down -3.35% and also among the worst performers there. The S&P 500 finished -1.16% while the NASDAQ was down just -0.13%. A substantial late rally in the US hid the extent of the midday losses which were more similar to the European bourses. The S&P was down as much as -2.72% – with the NASDAQ down -2.54% – in the first hour of trading and remained under pressure for most of the session until tech led the way into the close. The technology hardware industry (+1.90%), specifically Apple (+3.03%) led the rebound along with other Megacap tech stocks such as Microsoft (+2.71%) and Nvidia (+2.69%). Even within tech breadth is becoming an issue with 83% of stocks in the NASDAQ lower yesterday even as the index only fell -0.13%. Maybe there was a hint of a WFH trade reigniting as restrictions build again.

Staying with the US, tomorrow our US economics team will be hosting a call with Biden campaign adviser Jared Bernstein, on economic policy and the election. To participate in this conference call, please click here for the note with the registration details. Mr Biden is currently leading Mr Trump +6.5pts in the RealClearPolitics polling average, which is roughly where the race has been since early August. However, the new open Supreme Court seat may add a wrinkle to the election now just six weeks away. Senators in vulnerable seats will be particularly interesting, because the Senate composition will be important for whichever candidate wins the Presidency.

Overnight, Bloomberg has reported that President Trump is moving towards nominating Amy Coney Barrettto to replace the late Justice RBG on the Supreme Court. She is a favourite of anti-abortion rights advocates and is preferred by Senate Majority Leader Mitch McConnell, the report added. Barrett may help the president secure votes for his re-election in vital Rust Belt and Great Lakes states where he currently trails Democratic candidate Joe Biden. Further, Trump’s second choice is believed to be Appeals Court Judge Barbara Lagoa, a Cuban-American from Florida, which might help Trump in that must-win state.

In terms of the coronavirus itself, yesterday saw further concerning developments, particularly in Western Europe once again. Here in the UK this morning, Prime Minister Johnson will be chairing a Cobra emergency committee meeting, following which he’ll be speaking in the House of Commons on the matter of Covid and will then make a broadcast to the nation at 8 pm. It’s widely expected that further restrictions are going to be announced, including hospitality venues, like bars and restaurants, ordered to close at 10pm from Thursday and will be limited to table service only. In terms of other restrictions, The Times has reported overnight that attendance at weddings may be cut to 15 guests from 30 while the Telegraph has reported that office goers will be asked to work from home where possible, this reversing a move to get people back to the office. During a press briefing yesterday, the country’s Chief Scientific Adviser and Chief Medical Officer said that if cases kept doubling every 7 days, then the UK could be seeing around 50,000 cases a day by mid-October. Later the UK alert level was raised from a 3 to a 4. In fact, yesterday saw another 4,368 confirmed cases here, making it the 3rd time in the last 4 days that over 4,000 cases had been reported. Data released yesterday also highlighted that 1,261 people in England were hospitalised with Covid-19 (vs. 782 a week ago), with 154 of them on ventilators (vs. 88 a week ago). Areminder that we have the latest cases and fatality tables in the pdf of this note which you can see under “View Report”. We have revamped them today so take a look. Hopefully it’ll provide a better way of showing the latest trends.

Elsewhere on the coronavirus, Italy announced plans to test travelers from certain regions of France after having implemented mandatory tests on travelers arriving from Spain, Croatia, Malta and Greece. This came as France saw its 7 day rolling case count rise above 10,000 for the first time over the weekend. In Germany, Health Minister Spahn noted the country’s health system can cope with the current level of infections, though the rise there and in neighboring countries are “worrying” especially given its central location and the level of mobility currently seen. While in the US, the weekly average has risen to 41,100 but without clear hot spots. Former FDA Commissioner Scott Gottlieb said yesterday that he is expecting the US to go through “at least one more cycle” of infections in the coming cold-weather months.

Asian markets have followed Wall Street’s lead this morning with the Hang Seng (-0.26%), Shanghai Comp (-0.12%), Kospi (-1.98%) and Asx (-0.70%) all trading lower. However, outside of the Kospi, the declines are relatively muted in nature while futures on the S&P 500 are also down a relatively modest -0.12%. Japan is closed for a holiday.

In other overnight news, we have seen text of the Fed Chair Powell’s testimony that he is scheduled to deliver before the House Financial Services Committee today. There was nothing particularly new in the released remarks as he is likely to reiterate that more is required from both fiscal and monetary policy to prevent the pandemic from causing long-term damage to the economy. He will also say that, “The path forward will depend on keeping the virus under control, and on policy actions taken at all levels of government.”

Looking back to yesterday, the selloff in risk assets saw investors pour into sovereign bonds, which rallied on both sides of the Atlantic. Yields on 10yr Treasuries fell -2.8bps to 0.666%, though most of that seemed to be driven by a decline in inflation expectations, with 10yr breakevens falling -4.3bps to 1.631%, their lowest level in the last month. Europe saw a similar advance, with yields on 10yr bunds down -4.5bps, while Italian BTPs – having initially sold off in the risk-off – rallied sharply after the news came through that the centre-left Democrats were ahead in elections in the key region of Tuscany, reducing concerns about a possible government breakup. By the end of the session, Italian 10yr yields had traded in a 9bp range before finishing -4.4bps lower. Meanwhile in FX, the US dollar surged +0.79% in its best day since March yesterday as part of a similar move into havens, while the traditionally safe Japanese Yen was the 2ndstrongest performer among the G10 currencies.

Over in commodity markets, oil prices suffered as part of the rotation out of risk assets, with both Brent crude (-3.96%) and WTI (-4.38%) losing significant ground, while the industrial bellwether of copper also moved -2.70% lower in its worst day for over a month. Precious metals were something of an exception though to the broader strength in safe havens, and by the close, gold had fallen -1.97% and traded below the $1900/oz mark for the first time since in six weeks before finishing at $1913/oz. While both silver (-7.72%) and platinum (-4.82%) suffered significant losses too.

To the day ahead now, and the highlight will likely be Fed Chair Powell and Treasury Secretary Mnuchin’s appearance before the House Financial Services Committee. Otherwise, we’ll also hear from Bank of England Governor Bailey, the ECB’s Lane, Villeroy and Panetta, along with the Fed’s Evans and Barkin, and the Riksbank will be announcing their latest decision on interest rates. Data releases include US existing home sales for August, the Richmond Fed’s manufacturing index for September, and the Euro Area’s advance consumer confidence reading for September.

via ZeroHedge News https://ift.tt/35XHCl6 Tyler Durden