Desperate Illinois To Borrow From Fed’s “Lender Of Last Resort” Facility A Second Time

Tyler Durden

Tue, 10/13/2020 – 11:20

Authored by Ted Dabrowski via Wirepoints.org,

Illinois is set to borrow several billion from the Federal Reserve’s Municipal Liquidity Fund (MLF) for a second time if a new U.S. stimulus package and a progressive tax hike scheme for Illinois don’t come through, according to comments from Illinois Gov. J.B. Pritzker. Illinois already borrowed $1.2 billion from the MLF earlier this year in an attempt to close some of the state’s 2020 budget shortfall.

The borrowing is significant since Illinois is the only state in the country to tap the MLF. The Fed created the MLF in April to be a “lender of last resort,” where cities, states and other government entities can go if they can’t raise money as a result of COVID-19. The governor’s comments are an admission that the normal financial markets aren’t willing to lend money to Illinois at competitive terms.

Normally, billions are raised by cities and states in the municipal bond market, where banks, insurance companies and all types of financial entities lend money directly to governments. But COVID put all that at risk, leading the Fed to step in to make sure governments had somewhere to go if the markets weren’t working.

Fortunately, despite some initial hiccups early on in the pandemic, the financial markets have worked just fine. Billions have been raised by cities and states across the country without having to tap the Fed.

The only exception so far, when it comes to city and state governments, is Illinois. The state borrowed from the MLF in June after the state failed to successfully raise $1.2 billion from the markets one month earlier. New York’s Metropolitan Transportation Authority is the only other borrower in the country to tap the MLF.

COVID-19 has brought to full view all of Illinois’ pre-pandemic problems. The increased stress is highlighting Illinois’ extreme outlier position nationally when it comes to finances, notably pension debts and the state’s unwillingness to reform. Gov. Pritzker continues to count on a federal bailout and more tax hikes to keep the state afloat, but neither will reverse the problems of overwhelming pension costs, the “nation’s least-tax-friendly-state” status and the increasing outmigration of Illinois residents. Wirepoints laid out the state’s outlier status in its recent special report linked here.

Fiscal reality kicks in

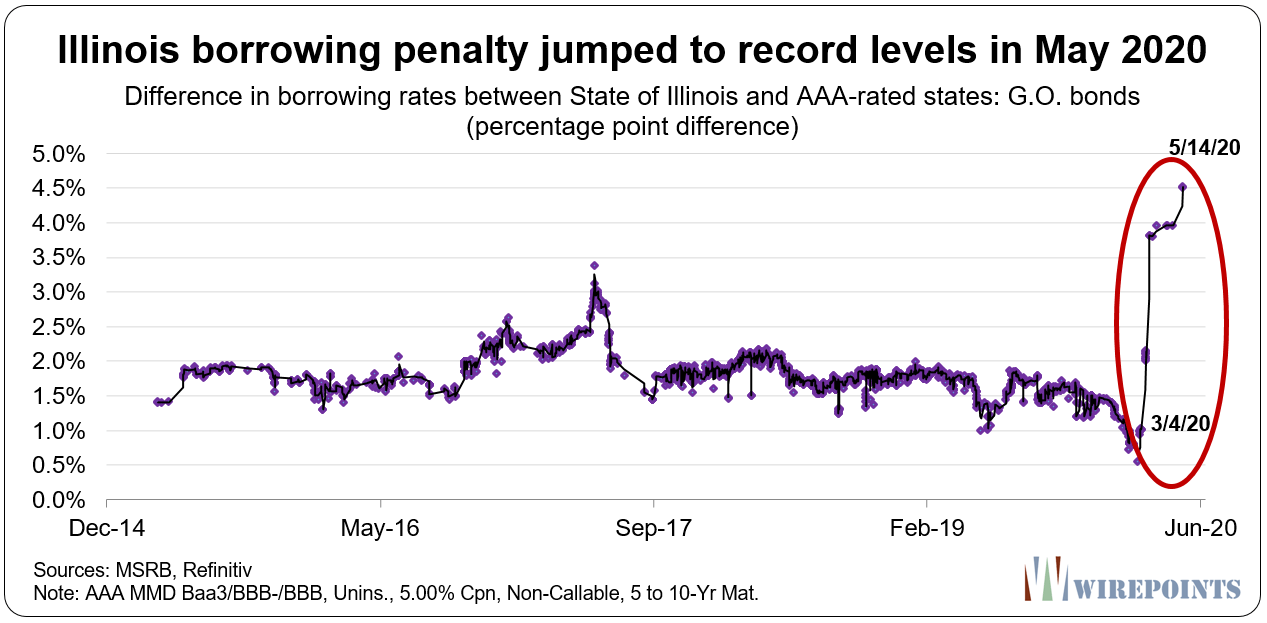

Fiscal reality began setting in for Illinois after the state was forced to pay punitive rates when it borrowed $800 million from the markets in May. Illinois’ borrowing rate then was 5.65 percent, five times higher than what well-run, AAA-rated states were paying to borrow money – around 1.1 percent.

It’s a massive penalty that ordinary Illinoisans are being forced to pay through higher taxes or cuts in core government services. The penalty reflects the continued collapse in the state’s finances. Unpaid bills of more than $8 billion, $261 billion in state pension debts, and the legislature’s unwillingness to pass any reforms has destroyed confidence in Illinois’ ability to manage its finances. Gov. Pritzker refuses to pursue pension reform, calling any attempts a “fantasy.”

As the below graphic shows, Illinois’ borrowing “penalty” – what the state pays over and above what well-run states pay to borrow – spiked to 4.50 percentage points at the time of the $800 million borrowing in May. That means Illinois’ debt was effectively trading like junk bonds, even though the state was still rated one notch better than junk by all three rating agencies.

Gov. Pritzker has increased Illinois’ dependence on the federal government since the first $1.2 billion MLF borrowing. The governor “balanced” the state’s 2021 budget by including a planned $5 billion borrowing from the Fed, with a further hope to repay that debt via another federal stimulus package.

The governor’s refusal to pursue structural reforms has not gone unnoticed by the rating agencies. Neither has the governor’s failure to pursue budget savings since the pandemic started, though the governor has finally begun talking about cuts. He recently asked his agencies to submit proposals for 5 percent cuts in 2021 and 10 percent in 2022.

That hasn’t impressed the S&P, which noted in a recent report:

“The magnitude of the current budget gap and reliance on one-time measures make us question Illinois’ ability to achieve structural balance in a reasonable time. Even if Illinois receives federal aid in fiscal 2021, we expect that it will face challenging budget gaps beyond the current fiscal year.”

The rating agency’s analysis reads like it is setting the stage for downgrading Illinois to junk:

“With the need for additional borrowing, an elevated bill backlog, and lingering substantial structural imbalance, Illinois could exhibit further characteristics of a non-investment-grade issuer.”

Illinois is like the financial basket case down the street whose credit score is so poor he has to borrow at crazy rates from payday lenders. The solution isn’t to keep doing the same things over and over. Instead, it’s to cut up the credit cards, change the bad spending habits and restructure the massive debts.

Read more about Illinois’ fiscal mismanagement:

-

Moody’s new estimate of Illinois pension shortfall increases to $261 billion

-

Pritzker’s Upside-Down Message On Budget Cuts And Federal Help

-

Solving Illinois’ Pension Problem | Part 1: Illinois is the Nation’s Extreme Outlier

-

Solving Illinois’ Pension Problem | Part 2: Pensions – Overpromised & Overgenerous

via ZeroHedge News https://ift.tt/2SNT5vN Tyler Durden