Rabobank: “A Dangerous Moment”

Tyler Durden

Mon, 10/26/2020 – 10:15

By Michael Every of Rabobank

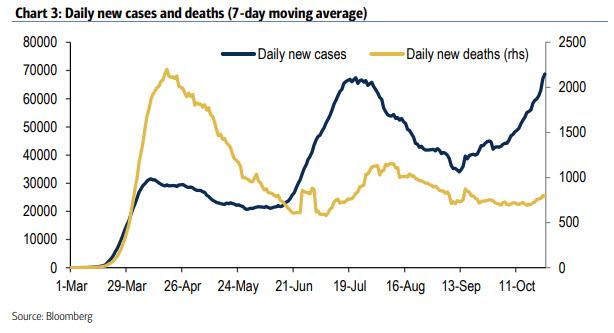

The markets have started a new week of trading in risk off mode (when this note was heading to press) amid fading expectations that the US Congress will pass another fiscal package. With just 8 days left until the presidential election, both sides may not have a sufficient incentive to reach an agreement. Even if there is no deal in the coming days, a fiscal stimulus is still likely to be agreed after the election to support businesses and households as the US is struggling to contain the coronavirus pandemic. In fact, President Trump’s chief of staff openly admitted that the US is “not going to control” the pandemic and instead will focus on “proper mitigation factors”, such as vaccines and treatments. Former Vice President Biden strongly criticized the Trump administration saying that “they’ve given up on their basic duty to protect the American people.” The US recorded a record daily number of new cases of 85,000.

Meanwhile, the WHO has warned that some countries in the northern hemisphere are facing a “dangerous moment.” This assessment applies to a number of EU countries, where political leaders are trying to protect their citizens by using various restrictions to flatten the coronavirus curve. Spain declared a state of emergency and imposed a curfew. Italy has tightened restrictions as well after new infections rose to a record high of 21,273 on Sunday. France reported record new infections for the fourth consecutive day. Last week the French government announced an extension of the curfew to 54 départements, covering some 2/3 of the country.

While these restrictions are not yet as tight as in spring, the latest set of data has already revealed that the pace of economic recovery in services has started to lose momentum. The Eurozone services PMI plunged to 46.2 from 48 on the back of various social distancing restrictions imposed across the continent to regain control over the coronavirus pandemic. Meanwhile, the manufacturing PMI edged higher from 53.7 to 54.4 in October driven by demand from abroad, particularly Asia, where countries seem to have adapted to the virus and have learnt to live with it. Looking at specific countries in the Eurozone, France’s manufacturing PMI slipped 0.2 points to 51, whilst the services PMI fell further below the boom-bust mark, to 46.5 from 47.5 in September. Commenting on the data Elwin de Groot said that this development is not a surprise of course now that France and many other countries are once again installing measures to contain/slow down the spread of the virus.

In Germany a similar picture is playing out with manufacturing activity actually recovering further in October. This appears to be related to stronger overseas demand – such as from China – and the recovering auto sector. However, the services PMI fell below the 50-mark (to 48.9 from 50.6). Elwin argues that this is only ‘the beginning’ and weakness in activity is likely to extend into the final months of this year. Despite the ‘technical rebound’ since May (which should show up as a strong growth number for Q3), a negative growth number for Q4 (and as such a double dip) is becoming increasingly likely. The key risk now is that the negative demand-shock (which was effectively attenuated by the government support measures in the first wave) will now gain momentum, in the form of a rising number of defaults among smaller businesses and rising unemployment, according to Elwin. This is the constellation in which the ECB meeting will take place on Thursday.

In the UK (still technically part of the EU) the pace of growth slowed to the weakest since the post-lockdown recovery started. The recovery in domestic demand is stalling as the labour market deteriorates and sentiment sours, Stefan Koopman commented. It is also worth noting that GfK consumer sentiment fell by the most since the start of March’s lockdown. On a more positive note, the Brexit rumour mill has slowed markedly over the past couple of days. This typically means that, behind closed doors, there’s some rational thinking and talking going on. At the same time, there’s good reason for prime minister Johnson to await the outcome of the US elections, so we wouldn’t get our hopes up about a deal already being announced this week.

Elsewhere in the EU, the Czech government has imposed a partial lockdown of the economy to regain control over the raging coronavirus. Speaking this morning PM Babis said that more virus curbs could be announced today. In Poland, the government may allegedly opt for a full-lockdown if the pace of infections does not slow down by the end of this week. While the hospitality sector will be among the worst impacted due to severe restrictions across the CEE region, rising concerns about health may weigh on private consumption and spill over to other sectors. A bleak winter is ahead of the CEE countries. Instead of a V-shaped recovery from the sharp contraction in Q2, the CEEs are moving into a W-shaped or even a U-shaped recovery depending on the damage the second wave of the pandemic will cause to confidence among households and corporates. We prefer to focus on higher levels in EUR/CEEs in the coming weeks as outlined most recently here.

The Turkish lira remains the worst performing EM currency so far this month. USD/TRY has reached another milestone breaching the 8.00 level this morning. Over the weekend President Erdogan reportedly dared the US to impose economic sanctions on Turkey. “Whatever your sanctions are, don’t hesitate to apply them”, the Turkish president reportedly said. “You told us to send back the S-400s. We are not a tribal state, we are Turkey.” The market is seriously concerned that if former VP Biden wins on November 3, the US will penalise Turkey for purchasing the Russian S-400 air defense system. It is also worth recalling that the CBRT left the market deeply disappointed by keeping the 1-week repo rate unchanged last week. We discussed this in details here, but in short the CBRT may have miscalculated market’s tolerance for conducting an unorthodox policy based on using an interest corridor to manage liquidity. The CBRT may seriously consider an emergency rate hike to stem the lira’s rout, especially if on this occasion opinion polls prove to be correct and Biden wins.

via ZeroHedge News https://ift.tt/35D8AfM Tyler Durden