Futures Rebound From Overnight Tech Wreck

Tyler Durden

Fri, 10/30/2020 – 08:06

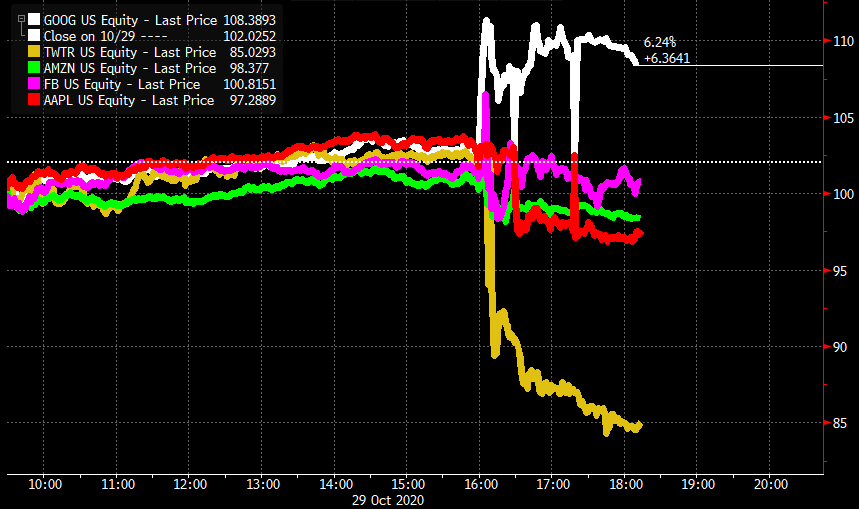

On Monday we presented readers with the latest observations from BofA quants who pointed out that Q3 earnings “smacked of the tech bubble” because despite impressive beats, in many cases stocks dropped (or outright tumbled) in kneejerk response as virtually everything has now been priced to (and beyond) perfection with little chance of upside surprise. Nowhere was this more obvious than Thursday afternoon when the world’s 4 biggest tech companies all reported blockbuster earnings and yet all but Google sank subsequently with the exception of Alphabet which popped after hours (while Twitter plunged as countless conservatives bailed on the ultra-partisan and liberal social network).

Nasdaq futures fell about 1%, erasing more than half of what was a 2.7% slide earlier after Apple’s iPhone sales and Twitter’s user growth both missed estimates. The two stocks sank in pre-market trading. Amazon.com fell 1.4% after it forecast a jump in costs related to COVID-19, while Facebook shed 2% as it warned of a tougher 2021. Google parent Alphabet was the only bright star among the FAAMGs with its shares jumping 7% after it beat estimates for quarterly sales as businesses resumed advertising.

Ahead of the overnight tech rout, global stock were already on course for the worst weekly decline since March as lockdown measures and the collapse of stimulus talks (which “nobody” could have predicted) crippled trader optimism. Treasuries, the dollar, oil and gold were little changed.

Third-quarter earnings season is past its halfway mark and about 84.8% of S&P 500 companies have beaten estimates for earnings, according to Refinitiv data. Overall, profit is expected to tumble 13.4% from a year ago.

The broad-based weakness in the market-leading giga-tech stocks added to trader concerns about a surge in coronavirus cases, and hammered stock futures on Friday, although futures are now off their worst levels of the day.

S&P e-minis fell 25.00 points or 0.9% and Nasdaq 100 E-minis were down 121 points, or 1.1%. A longer-term chart shows the precarious positioning for the S&P, with any further declines set to take out the Sept 24 lows and open up a trapdoor to much lower levels.

Shares of tech heavyweights had jumped ahead of tech results on Thursday, helping the S&P 500 close higher. Still, the benchmark index is set to wrap up its worst week since mid-June, while Wall Street’s fear gauge held at a 20-week high, also on fears of a contested election next week. Ahead of the final weekend before Election Day on Tuesday, President Donald Trump and Democratic challenger Joe Biden will barnstorm across battleground states in the Midwest where the coronavirus pandemic has exploded anew.

“Our short-term risk-appetite indicator is firmly in negative territory,” said Credit Agricole CIB head of global markets research Jean-Francois Paren. “The adjustment of risky asset prices to the weaker epidemic and economic outlook could continue, which is not encouraging for risk asset prices in the coming days, especially given the uncertainty regarding the U.S. elections.”

European shares fluctuated amid a string of mixed earnings reports. Europe’s Stoxx 600 Index erased declines of as much as 0.9%, climbing 0.3%, led by energy and banks, with E&P giants Total and Shell among biggest gainers; Total posted 3Q profit that exceeded the highest analyst estimate; Barclays raised Shell to equalweight, saying newly presented financial framework addresses main concerns. Tech stocks faltered as did Danish drug giant Novo Nordisk A/S, whose earnings underwhelmed analysts. Bank stocks advanced after Spain’s BBVA SA and the U.K.’s NatWest Group Plc reported improved pictures for soured loans.

Earlier in the session, Asian stocks fell, led by the health care and IT sectors. Trading volume for MSCI Asia Pacific Index members was 28% above the monthly average for this time of the day. The Topix lost 2%, with Takeda and Hoya contributing the most to the move. The Shanghai Composite Index retreated 1.5%, driven by China Life and Yili Industrial.

As Bloomberg notes, weakness in technology shares has added to volatility that’s likely to remain elevated heading into next week’s U.S. election. Global equities are on course for the worst weekly decline since March as lockdown measures in some countries and the lack of an agreement on U.S. stimulus dent sentiment. New U.S. coronavirus cases topped 89,000, setting a daily record.

In FX, the Bloomberg Dollar Spot Index steadied after swinging between gains and losses; the euro steadied but was set for its biggest weekly drop against the dollar since September. Sweden’s krona led gains among Group-of-10 peers, though the Japanese yen remained supported on haven demand. The Australian dollar advanced on month-end flows, with a stronger yuan also spurring appetite for the commodity-linked currency.

In rates, Treasuries were unchanged with long-end supported ahead of month-end. Yields are off richest levels of the day as e-minis recouped some early losses. Treasury yields are within a basis point of Thursday’s close, slightly lower across the curve; 10-year yields around 0.82%, remain toward cheaper end of 0.74% to 0.84% weekly range and outperforming bunds, gilts by almost a basis point each. Treasuries rallied in early Asia session as Apple stock fell over 4% in after-market trading on Thursday; into early U.S. session Nasdaq e-minis remain lower by 1.2%, S&P e-minis are off 0.9%.

In commodities, oil was flat after suffering a recent rout, while spot gold headed for its third consecutive monthly decline. Crude oil was little changed in New York.

On today’s calendar AbbVie, Exxon and Charter Communications are among Friday’s scheduled earnings. Personal spending, U. of Michigan sentiment are due.

Market Snapshot

- S&P 500 futures down 1.4% to 3,257.75

- STOXX Europe 600 up 0.1% to 342.16

- MXAP down 1.3% to 172.21

- MXAPJ down 1.2% to 572.11

- Nikkei down 1.5% to 22,977.13

- Topix down 2% to 1,579.33

- Hang Seng Index down 2% to 24,107.42

- Shanghai Composite down 1.5% to 3,224.53

- Sensex down 0.6% to 39,523.90

- Australia S&P/ASX 200 down 0.6% to 5,927.58

- Kospi down 2.6% to 2,267.15

- Brent Futures down 0.03% to $37.64/bbl

- Gold spot up 0.2% to $1,871.30

- U.S. Dollar Index down 0.04% to 93.92

- German 10Y yield rose 1.4 bps to -0.622%

- Euro down 0.05% to $1.1668

- Brent Futures down 0.03% to $37.64/bbl

- Italian 10Y yield fell 7.3 bps to 0.489%

- Spanish 10Y yield rose 1.7 bps to 0.15%

Top Overnight News from Bloomberg

- Germany and the rest of the euro area’s biggest economies surged in the third quarter, in a rebound that’s now being derailed by an intensifying pandemic and new government restrictions on businesses

- European Central Bank policy maker Robert Holzmann said it is right to assume that President Christine Lagarde signaled more monetary stimulus is coming, though not until December

- U.K. house prices posted their biggest annual gain since 2015 this month as a revival in the housing market defied a wider economic malaise

- Jeremy Corbyn’s suspension from the U.K. Labour Party he led until April threatened to re-open divisions in the party after six months of relative calm under new leader Keir Starmer

- Treasury Secretary Steven Mnuchin accused House Speaker Nancy Pelosi of pulling a “political stunt” and holding up a new stimulus bill by refusing to offer compromises, in an escalation of acrimonious finger-pointing over stalled virus-relief negotiations

- U.S. new virus cases topped 89,000, setting a new daily record, as the outbreak intensifies ahead of next week’s presidential election. The U.S. is seeing a jump in cases in New York and New Jersey again, and a record outbreak across the Midwest states

- France is aiming to limit the drop in economic activity to 15% during the country’s second coronavirus lockdown starting on Friday, Finance Minister Bruno Le Maire said in a government briefing on Thursday

- German Chancellor Angela Merkel delivered a wake-up call to fellow leaders in the 27-nation European Union, saying they all failed to step in quickly enough to control the pandemic as the cost of a second lockdown begins to come into focus

- Oil is poised for the biggest monthly decline since March as a resurgent coronavirus across the U.S. and Europe raised concerns the fragile demand recovery will be derailed.

Here’s a quick look at global markets courtesy of NewsSquawk

Asian equity markets weakened heading into month-end and after US stock index futures faded the recovery seen on Wall Street amid disappointment from the big tech earnings despite Apple, Alphabet, Amazon, Facebook and Twitter all beating on top and bottom lines. Apple shares declined over 4% in extended trade with investors discouraged by the miss on iPhone sales and lack of guidance, as well as a 29% Y/Y drop in its Chinese revenue which pressured its supply Chain in Asia and Twitter slumped nearly 18% after hours on slower user growth. ASX 200 (-0.6%) and Nikkei 225 (-1.5%) were weaker with industrials and tech frontrunning the declines in Australia although losses in the index were briefly pared by financials as AMP shares surged over 20% following a takeover approach by Ares Management, while the mood in Tokyo was clouded by currency effects and soft inflation data but with Panasonic shares a notable gainer on reports it is working with Tesla to build a new battery cell production line at the Gigafactory. Elsewhere, the Hang Seng (-2.0%) and Shanghai Comp. (-1.5%) remained cautious amid a plethora of large-cap earnings and with participants mulling over the initial details of the 5-year plan which seeks to build the nation into a technological powerhouse and emphasized quality growth over speed but refrained from specifying a targeted pace of growth. Finally, 10yr JGBs were lower and fell below support near 152.00 on spillover selling from T-notes as Wall Street initially nursed losses and following an uninspiring 7yr auction stateside, although the downside for JGBs was cushioned with the BoJ in the market for nearly JPY 1.3tln of JGBs with up to 10yr maturities.

Top Asian News

- Hong Kong Economy Shows Early Signs of Revival as Exports Jump

- Singapore Overtakes Thailand to Become Asia’s Worst Stock Market

- BOJ Widens Buying Ranges While Cutting Frequency for Short Bonds

European equities (Eurostoxx 50 -0.1%) have trimmed opening losses throughout the session despite underpeformance of Stateside peers. After a mixed close yesterday, equities in the region initially succumbed to some of the heavy selling pressure seen after the Wall St. close in the wake of earnings from US tech mega-caps. Despite the likes of Apple, Alphabet, Amazon, Facebook and Twitter recording beats on top and bottom lines, earnings (ex-Alphabet; up 5.6% pre-market) were received poorly with Apple shares currently lower by 4.5% in pre-market trade following a miss on iPhone sales and lack of guidance, as well as a 29% Y/Y drop in its Chinese revenue. Social media names Facebook (-2.4%) and Twitter (-17.5%) are seen lower ahead of the cash open, whilst e-commerce giant Amazon (-2.1%) are also lagging with some citing soft operating income guidance for December. In Europe, given the gravitational pull of the aforementioned large-caps, stocks across the continent commenced the session on the backfoot before staging a mild recovery with little in the way of clear fundamentals behind the move; as context the Eurostoxx 50 is lower by 6.4% on the week. Sectoral performance is somewhat mixed with oil & gas names the clear outperformer in the wake of earnings from Total (+2.3%) who reported a heavy beat on Q3 net income and maintained its dividend despite the likes of BP, Shell and Eni trimming theirs in 2020. Elsewhere, banking names are also performing well this morning following Q3 results from Natwest Group (+5.6%) which saw the Co. beat expectations for quarterly pre-tax profits and suggest that FY impairments are seen at the lower end of the range. IAG (+2.6%) have lent some support to the travel & leisure sector despite reporting a wider than expected loss for Q3 operating income with the CEO noting that his top priority will be reducing the Co.’s cost base. To the downside, underperformance has been observed in personal & household goods and food & beverage names. Health care names are also softer on the session following earnings from Novo Nordisk (-1.5%) with the insulin producer missing on expectations for EBIT and net profits.

Top European News

- Spanish Banks Join EU Peers in Painting Rosier Bad Loans Picture

- Continental CEO Degenhart to Resign, Citing Health Reasons

- Italy in Talks With Paschi on $1.75 Billion Capital Increase

- U.K. House Prices Jump Most in Five Years as Boom Gathers Pace

In FX, the Dollar remains relatively firm and resilient given a loss of safe-haven status or less demand amidst a fragile recovery in risk sentiment, month end portfolio rebalancing and positioning ahead of next week’s US Presidential Election. However, the index is back below 94.000 and Thursday’s 94.105 high within a 93.983-762 range as several major counterparts claw back some lost ground before another raft of data, the Chicago PMI and final Michigan sentiment.

- JPY/AUD – Leading the aforementioned G10 recovery in spite of somewhat mixed Japanese CPI, unemployment and ip updates, the Yen is back above 104.50 and a key Fib at the half round number alongside hefty option expiry interest (2.2 bn). On the flip-side, 1.4 bn expiries at the 104.00 strike will act as a barrier and support for Usd/Jpy after the pair got to within 2-3 pips of the level yesterday, and conversely the Aussie appears to be drawing comfort from the fact that it survived an equally close shave with 0.7000 to probe 0.7050 with assistance from ANZ’s CEO arguing against an RBA ease next week on the grounds it would flood the financial system with more liquidity, impair bank profitability and only boost the economy and jobs marginally.

- GBP – Also firmer vs the Buck after losing 1.2900+ status on Wednesday and maintaining momentum against the Euro close to 0.9000 in wake of the ECB, though wary of ongoing Brexit uncertainty and end of month Eur/Gbp cross flows that can deviate from RHS to LHS quite sporadically.

- NZD/EUR/CAD/CHF – All narrowly mixed vs the Greenback, as the Kiwi regains hold of the 0.6600 handle in wake of another upbeat sentiment survey (ANZ consumer confidence up to 108.7 in October from 100.0 previously), and the Euro pares some post-ECB losses after basing at 1.1650. Note, this coincided with the 100 DMA, which is now 5 pips firmer and the 2 chart points also align with 1.5 bn option expiries for today’s NY cut. Perhaps predictably, market contacts tout stops on a break of 1.1650 that would expose a virtual double bottom from late September (1.1615-12). Elsewhere, the Loonie is deriving a degree of comfort from stability in oil prices and the generally less risk averse tone to retest 1.3300 from 1.3390 or so, but the Franc is still lagging below 0.9150 and hovering near 1.0700 against the Euro.

In commodities, WTI and brent are modestly firmer this morning in a pull-back from some of the overnight losses after sentiment took a hit on the earnings-spurred downside in US equities last night. Following this, the crude complex has continued to lift off lows throughout the session alongside sentiment in general; WTI and Brent are currently firmer by around USD 0.30/bbl. Turning to OPEC where the Iraq oil minister pushed back on reports that the country and others are considering a rollover of existing OPEC+ output cuts into 2021 given developments on both the demand & supply side. While the remark is interesting there is still over a month until the next OPEC+ gathering and as such a pushback on such commentary at this stage is perhaps not too surprising. Elsewhere, the BSEE report of 43-companies had just shy of 85% of oil shut-in for the Gulf given Storm Zeta; its worth noting the storm is continuing to dissipate and as such production should be restored to the Gulf over the next few days – assuming no damage occurred. Moving to metals, spot gold is modestly firmer this morning as the USD has dipped as sentiment sees a moderate pick up from a European perspective. Separately, mining updates saw Glencore confirm their FY production guidance with the exception of coal given strike action at the Cerrjeon site; additionally, their YTD copper production is -8% vs. the prior period.

US Event Calendar

- 8:30am: Personal Income, est. 0.4%, prior -2.7%

- 8:30am: Personal Spending, est. 1.0%, prior 1.0%

- 8:30am: Employment Cost Index, est. 0.5%, prior 0.5%

- 8:30am: PCE Core Deflator YoY, est. 1.7%, prior 1.6%

- 9:45am: MNI Chicago PMI, est. 58, prior 62.4

- 10am: U. of Mich. Sentiment, est. 81.2, prior 81.2; Current Conditions, est. 84.9, prior 84.9; Expectations, est. 78.8, prior 78.8

DB’s Jim Reid concludes the overnight wrap

For the first 40-odd years of my life Halloween was a minor curiosity. My Dad’s dislike of trick or treaters didn’t help cement it in my social calendar as a kid. However since we’ve had kids my wife has slowly ensured it’s become a bigger and bigger event. Last night I learnt that she has gone into overdrive and bought what I thought were pretty expensive costumes ahead of us going to a pumpkin picking Halloween themed afternoon tomorrow at a local farm. Apparently I have an extravagant ghost costume and the twins have matching baby ghost costumes. My wife and Maisie have mother and daughter witch costumes and broomsticks. I’m not sure what the Halloween version of bah humbug is (maybe boooo humbug), but I’m slowly having it drummed out of me.

Over the last 24 hours we’ve gone from treat to trick as the prospect of big tech earnings first lured investors back in and then disappointed when they arrived after the bell. The S&P 500 was up over +2% late in the actual session last night prior to a sharp 70bp pullback in the last half hour of trading. It still closed +1.19%, with the NASDAQ rising a greater +1.64%.

After the close, Apple (+4.53% daily gain) fell over -4% even as its quarterly results beat estimates with record sales of Macs and services. However the largest US company also revealed that iPhone revenues fell -21% with revenue in Greater China, one of the company’s most important regions, falling by -29% to the lowest level since 2014. Amazon (+2.33% earlier) was down nearly -2% after giving up an immediate postmarket gain as revenue and earnings both solidly beat analyst estimates. The dip came after the CFO indicated that covid-related expenses will go up to $4 billion. Facebook’s (+5.75% earlier) shares were down over -2.5% in the after-market, even as revenues and user growth both beat estimates. On a more positive note, Google’s (+4.16% earlier) parent company, Alphabet, gained over +6% in after-market trading with news that the company’s digital advertising profits bounced back strongly from the previous quarter.

As a result, S&P 500 and Nasdaq futures are down -1.39% and -1.90% respectively as we type. Asian markets have also taken another leg lower with the Nikkei (-0.84%), Hang Seng ( -0.50%), Asx (-0.55%) and Kospi (-1.43%) all down. Chinese markets are more mixed with the Shanghai Comp up +0.08% while the CSI is down -0.09%. In FX, cable is down -0.18% to $1.2907 as more and more areas in England are moving to the topmost tier of restrictions. Meanwhile, yields on 10yr USTs are down -1.8bps this morning

Overnight, we also got a look into some details of China’s new five-year economic plan, which had tech in focus. The new plan elevated China’s self-reliance in technology into a national strategic pillar. Senior party officials of the Communist Party said that the nation would accelerate development of the kind of technology needed to spur the next stage of economic development with focus on bold measures to cut reliance on foreign know-how.

Back to yesterday and European stocks tried to turn positive after three straight days of declines to start the week as ECB President Lagarde outlined steps the central bank could take in December to recalibrate monetary policy in light of the worsening pandemic (more below). Her comments saw the STOXX 600 rise +1.76% off the lows of the day, however part of those gains were given back in the last half hour of trading with the index ending down -0.12% on the day. While the DAX (+0.32%) gained, other bourses such as the CAC (-0.03%) and FTSE (-0.02%) were not able to stay above water. European futures are down around -1.2% this morning.

As our economists point out (see their note here) this was a unique ECB meeting as for the first time we saw a unanimous post-dated decision to act at the next meeting (December in this case). The composition of that action remains to be determined however, and will be a function of events, both pandemic and economic, over the next six weeks. Our economists suggest that the emphasis on “all instruments” being under consideration is a message to think beyond just PEPP. The sensitivity to weak private credit implies changes to the TLTRO framework. For the time being, they hold onto their view of a composite easing strategy in December: a package of measures, including tweaks to the TLTRO framework, to complement more PEPP in one form or another to address the pandemic risk and more APP to address the persistent low inflation problem.

As they also point out, six weeks can be a long time in a non-linear pandemic. However, post-dated action is not to be confused for ECB inactivity for the next six weeks. ECB President Lagarde emphasised the flexibility of existing programmes like PEPP to respond to any downside surprises. There is still more than half the PEPP available and it is flexible enough to be deployed on an “anytime, anyplace, anywhere” basis. The pace of purchases can re-accelerate if necessary.

The euro fell -0.61% by the end of the day to one month lows but that was as much due to dollar strength as half the move occurred before the ECB meeting. 10yr bund yields fell -1.1bps to -0.64%. With the signal of added ECB support peripheral bond yields fell, with Italian (-6.2bps), Spanish (-3.4bps), Greek (-10.7bps) and Portuguese (-3.5bps) 10yr bonds all tightening to 10yr bunds. US Treasuries fell with the risk on sentiment, as yields rose +5.2bps to 0.823%, the largest one day rise in over three weeks.

In terms of data, the US economy expanded at a record 33.1% (annualised) pace off the lows of the pandemic, with business reopening and consumer spending powered by stimulus injections. The rise in GDP, which on a quarterly basis is 7.4%, slightly beat market expectations of 32.0%, and comes after Q2’s also record decline of -31.4%. Overall, GDP is now -3.5% below pre-virus (Q4 2019) levels. In terms of components, consumer services spending was -7.7% below pre-virus levels, but consumer goods spending +6.7% above. There was also initial jobless claims out of the US, where claims in regular state programs totaled 751k in the week ended Oct. 24, down 40k from the prior week. Continuing claims decreased 709k to 7.76mn in the week ended Oct. 1, having now fallen for five straight weeks. Overall these were positive data points, but the virus’s progression may impact the winter readings going forward.

With less than five full days before polls close in the US elections, former Vice President Joe Biden is currently in a strong position with the fivethirtyeight.com model giving him an 89% chance of winning, the highest so far, and a national polling average lead of +8.8. Biden holds strong polling leads in the key Midwest swing states of Pennsylvania (+5.2pts), Wisconsin (+8.4pts), and Michigan (+8.1pts), and is also leading to a smaller degree in the Sunbelt swing states of Florida (+2.1pts), North Carolina (+2.2pts) and Arizona (+2.7pts). Biden can win by just carrying the Midwest but, as has been highlighted before, we are likely to know results from the latter group of states earlier because they process mail-in ballots ahead of the election and both Florida and North Carolina will also be allowed to count votes ahead of time. A quick win there for Biden and the “Blue Wave” could materialise rapidly, but a Trump win in that part of the map and we could be waiting until the end of the week at least. The Secretary of State in Pennsylvania has said that the “overwhelming majority” of votes should be counted by next Friday, but that is still at least 3 days of uncertainty and that is before we get to any implications of Supreme Court rulings.

Staying on politics EU Commission President Ursula von der Leyen stated that Brexit talks are ‘making good progress’ and are now ‘boiling down to the two topics that are the most important – Level Playing Field and fisheries’. These two issues as well as a mechanism in the final treaty for resolving future disputes are among the most important outstanding points. European Council President Michel, expressed the expectation that the state of the negotiations would probably be assessed next week with his hope being to start the ratification process in mid-November.

On the coronavirus, hospitalisation rates in some countries are approaching peak levels seen during the first wave. Belgium reported 5,924 patients currently hospitalised, surpassing its previous peak from back in April. While in Portugal, the number of ICU patients is now 269, just short of its previous peak of 271. Similarly in Italy, there are now 17,615 patients in hospitals, though capacity still remains there compared to the nearly 29,000 back in April. This is why countries throughout Europe have been enacting new restrictions to try to flatten the curve again. Yesterday Sweden, whose actions have been among the most scrutinised, announced that residents in Stockholm are to avoid shops, gyms and any other indoor venues that don’t provide essential services. This comes as the country has seen around 3,000 new cases, a record daily rise. In the US, weekly cases have hit record highs as the virus continues to spread through the Southern and Midwestern regions. However yesterday there was troubling news out of the northeast, which had been resistant to a second wave, as New Jersey’s and New York’s positivity rates of covid-19 tests hit their highest levels since May. Lastly Dr Fauci predicted yesterday that normality may not return until late 2021 even with an effective vaccine broadly distributed.

Looking ahead to today there will be readings of France, German, Italian and Euro Area Q3 GDP. As well as CPI data for France and Italy and unemployment data for Italy and the Euro Area. In the US, we will get personal spending and income data along with PCE core deflator. There is also the MNI Chicago PMI and final University of Michigan sentiment reading for October. In terms of Central Banks, the ECB’s Weidmann is expected to speak. About halfway through earnings, we will see results today from Novo Nordisk, AbbVie, ExxonMobil, Charter Communications, Chevron, Total and NatWest Group.

via ZeroHedge News https://ift.tt/3mOiUJd Tyler Durden