Quant Carnage Hammers Iconic Hedge Funds Renaissance, Two Sigma

Tyler Durden

Tue, 11/17/2020 – 15:17

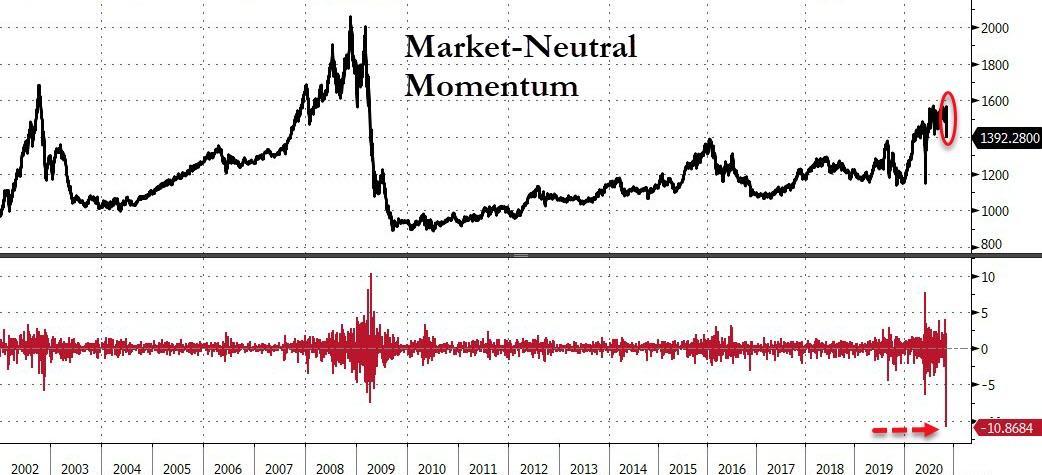

Last Monday, when momentum stocks suffered a spectacular collapse as the Dow Jones Market Neutral Momentum index plunged the most on record…

… a move which Nomura’s Charlie McElligott quantified as a 15 sigma drawdown, or one which normally would take place every several billions years…

… we said that “what was already a dismal year for quant funds is about to get absolutely catastrophic.”

We were right, because as Bloomberg reports today the carnage spread as far as some of the most iconic quant powerhouses: Jim Simons’ Renaissance Technologies and its peer, Two Sigma Advisors.

According to Bloomberg, the two quant investing giants, both of which rely heavily on factor investing, have seen losses across several of their funds in 2020, “a sign of how unprecedented market volatility caused by the Covid-19 pandemic hurt even the most sophisticated traders.”

The reason: not only did momentum stocks, which virtually all quants had been riding since the March lows as a result of the chronic underperformance of the value factor, tumbled…

… but the VIX exploded higher, and has averaged 33 since the end of February, 14 points higher than the average over the prior 30 years. That has upended performance from firms that in recent years have been among the best on Wall Street, and normally thrive during periods of heightened volatility.

But the real reason for the quant carnage is that backtests and historical trade relationships which quants rely on to formulate investment strategist, have failed miserable in 2020: “Quants rely on data from time periods that have no reflection of today’s environment,” said Adam Taback, CIO at Wells Fargo Private Wealth Management. “When you have volatility in markets, it makes it extremely difficult for them to catch anything because they get whipsawed back and forth.”

As a result, Renaissance saw a decline of about 20% through October in its long-biased fund, with the $75 billion firm’s market-neutral fund tumbling 27% and its global-equities fund losing about 25%. Amusingly, the firm “explained” its dismal performance to investors claiming that its losses are due to being under-hedged during March’s collapse and then over-hedged in the rebound from April through June. That happened because models that had “overcompensated” for the original trouble.

One would think such excuses are moot when one’s fund has a “hedge” adjective behind it, but apparently not.

“It is not surprising that our funds, which depend on models that are trained on historical data, should perform abnormally (either for the better or for the worse) in a year that is anything but normal by historical standards,” Renaissance told clients in a September letter. According to Bloomberg, the firm said it has redirected additional personnel to work on the funds, and that its leadership “made it clear to the research staff that understanding and addressing the situation with these funds is our company’s highest priority.”

Yeah, well, in a world in which central bankers have no idea what they are doing, we wish the “research staff” all the best as they go back to the drawing board with their investing models.

Another legendary quant firm, the $58 billion Two Sigma, saw its risk-premia strategy lose 11.5% this year through last month, Bloomberg reported. The firm’s absolute-return fund declined 2.7%, while its absolute-return macro fund slumped 23%.

While we have yet to hear of more pronounced casualties, it’s only a matter of time before far greater losses are unearthed. The reason is that for quant funds which specialize in factor-investing – picking securities based on traits such as recent performance or volatility – November may have added to the bruising, according to Neuberger Berman Group’s Ian Haas who oversees quantitative and directional strategy research.

“This could be a very bad month” for firms that had been betting on so-called momentum stocks, said Haas based on preliminary performance data from some of those hedge funds on Nov. 9. That’s when Pfizer Inc. announced the results of its vaccine trial, which spurred an unprecedented rotation out of growth, tech and momentum companies that had been benefiting from the pandemic and the lowflation environment into value stocks.

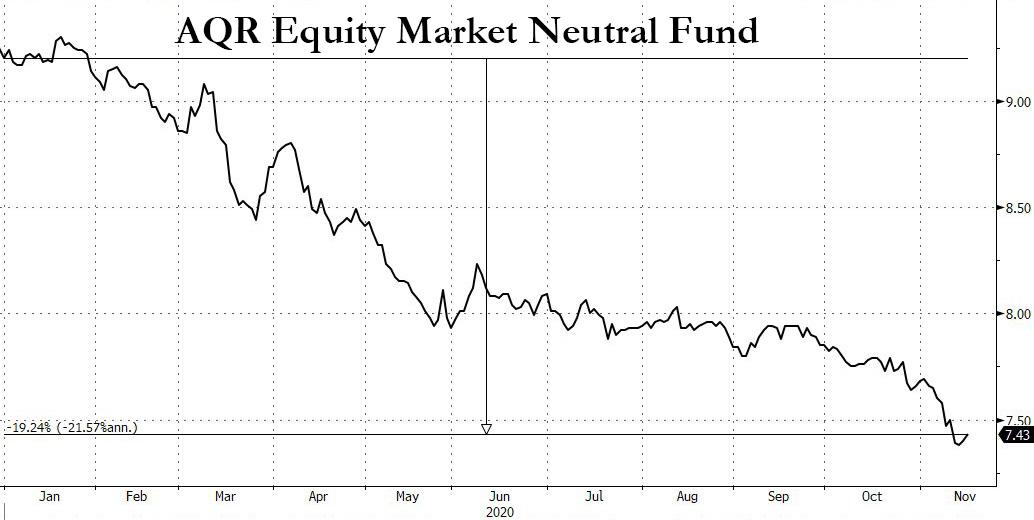

Ironically, even quants such as Cliff Asness’ AQR Capital Management, which have a pro-value tilt in many of its portfolios, the pullback from momentum exposure was simply too big. In fact, the overall hit was so big that the AQR Equity Market Neutral Fund added to its losses without barely a rebound, and is down 19% this year through Monday, just off the worst levels of the year.

To be sure, not every quant has had a miserable year: D.E. Shaw’s main hedge fund, The Composite Fund, made 0.4% in October, bringing gains for the first 10 months to about 15%, Bloomberg reported, adding that its macro-oriented Oculus Fund jumped 2% in October, extending 2020 gains to 23%.

via ZeroHedge News https://ift.tt/36KWOkb Tyler Durden