Apocalypse Now And The Rise Of The Extremes

Tyler Durden

Tue, 11/17/2020 – 21:20

The Western Minority Report

A few days ago, we learnt that Joe Biden and his team were considering Janet Yellen as a serious candidate for the next Secretary of the Treasury position. According to betting markets, Lael Brainard may be also well-positioned for the job.

Such potential links between the future administration and the Federal Reserve should not come as a surprise. First, the independence of the Fed is a myth. Second, since the late 1990’s, there have been two certainties in America (and not only in America): monetary policy and economic policy.

The fierce debates between Democrats and Republicans are just part of the political show, but they have no serious consequence on the underlying economic policy. In fact, all administrations have done basically the same thing, i.e. postponing the question of the debt and supporting asset wealth.

The fact that Biden’s team is considering Janet Yellen as a serious option is meaningful, as the former chair of the Fed claimed at the end of October 2016 that “Fed purchases of stocks could help in a downturn”.

Beyond the Treasury Secretary position, we have also heard radical voices among the Democratic Party calling for the forgiveness of student debt. You can be sure that people who already paid their loan back will appreciate that.

Once again,the next four years are likely be dominated by money printing and money spending. In fact, MMT has quietly become the golden rule of the United States. And also of Europe and Japan.

Would Keynes endorse post-Keynesian economics?

Almost all public decision makers in the West, whether they are central bankers or politicians, are heavily influenced by the old Keynesian way of thinking.

Every person who has studied a bit economics may be familiar with the following equation: Y = C + I + G + (X – M), where Y is the GDP, C is consumption spending, I is investment spending, G is government spending, and (X – M) is the trade surplus/deficit.

No need to be a rock star scientist to understand that increasing public spending mathematically leads to an increase of the GDP. Besides, as the national income grows with Y, consumption spending may continue to rise afterwards (all things being equal), and so on. This theoretical virtuous circle is known as “the Keynesian multiplier”.

However, this model has serious scientific limits.

First, it is based on several unrealistic assumptions, like the fact that economic agents are said to be rational, and also the fact that the economy is supposed to reach an equilibrium which does not make any sense for living systems.

The second objection is the fact that this model is an approximation of very short-lived dynamics. Said differently, it may be true on a few months period, but the previous equation becomes highly unstable on the long run.

More specifically, the model does not explain the organic economic trajectory of a country, and it does not enable to understand what happens when debt and money supply become out-of-control. John Maynard Keynes did criticize the lack of public intervention during the Great Depression. However, I am not sure that he would have agreed on current policies based on infinite public deficit and permanent monetary expansion.

Infinite Bailouts

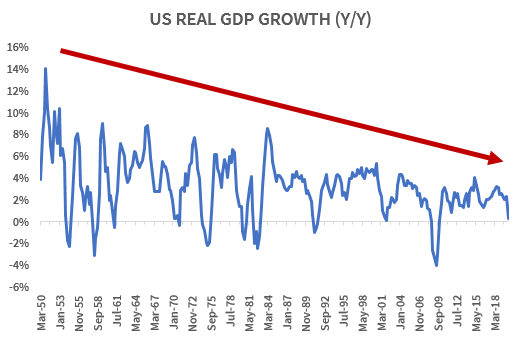

From Japan to America, all Western countries face a similar problem: their economies are ending a multi-decades Kondratiev wave, meaning that they are facing a structural crisis risk that may be necessary to start a new long period of sustainable economic growth. There are two big reasons for that: ageing population and debt spiral.

The organic economic demand in those countries structurally diminishes, leading to more solvency issues. While governments and central bankers always intervene to refinance agents, the problem is that such accommodative policies do not affect this organic demand trend. Worse, they create a bigger debt problem, with more zombie agents in the economy and more revenues dedicated to repayment, increasing the likelihood of more bailouts in the future (see There Ain’t No Such Thing as a Free Lunch – Part 2).

Infinite QE

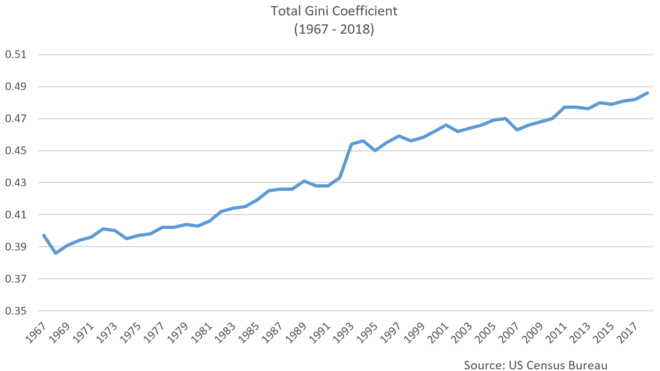

Beyond indebted agents, the biggest fear of our decision makers is to let markets crash. Probably, because it would lead to a severe confidence shock. At least for “the Haves” (i.e. upper classes, Baby-boomers). Thus, another priority of the past two decades has been to maintain the upward dynamic of assets like stocks, bonds, and real estate, whatever the cost for the economy.

Of course, this focus on markets has created severe distortions in the economy, as asset inflation is killing housing affordability and reducing savings capacities, resulting in a durable squeeze of working and middle classes (see There Ain’t No Such Thing as a Free Lunch – Part 1).

While the so-called Keynesian multiplier effect has become extremely limited, one could argue that today the theoretical virtuous circle has been replaced by a vicious one, as more intervention is likely to lead to more zombification and more financial squeeze, leading to even more intervention afterwards.

One could this mechanism the negative Brrrr multiplier.

Supermassive Black Hole

To summarize, it is impossible for Western countries to create real and durable growth based on nothing, as there is no such thing as a free lunch. It is true that without all the interventions of the past 20 years, the economy might already be in depression.

But, the Kondratiev wave is a powerful natural force. Despite huge levels of money printing and deficits, such measures have not managed to recreate the growth dynamics of the aftermath of World War II. While Raoul Pal recently described bitcoin as a “supermassive black hole”, I believe that the real supermassive black hole is the end of the long-term cycle.

In other words, instead of an economic collapse, all we get is the spaghettification of the economic activity. But this is not good news. Indeed, Western economies are becoming immobile as the possibility of new Kondratiev wave is being postponed.

The Immobile Republics

In 1989, French diplomat and politician Alain Peyreffite wrote:

“Kids are playing on an escalator, walking up in the wrong direction. If they stop to walk, they go downstairs. If they keep on walking, they remain in a stationary position. If they climb faster, they go upstairs.”

According to him, this tricky game is the fundamental dynamic of all human societies. In the long run, immobile countries will gradually decline, leaving space for those making significant progress (see The Immobile Empire).

While the US, Europe, and Japan are immobile, willing to do “whatever it takes” to stimulate a dying system, other countries like China have started to restructure their economy, eliminating inefficient agents, creating new opportunities for the coming decades (see Reverse Black Swan?).

Western governments are not magicians, and there will be no revival without a major economic and financial reset.

Corruption and Democracy

Why does it seem impossible for politicians and decision makers to make such a diagnostic? Why are the questions of the debt and money supply never debated in the West? Why all the parties are pursing the same kind of economic policies, whether they are Democrats, Republicans, Socialists, or Nationalists? Why do all central banks seem to reach a perfect consensus at each meeting?

And more importantly, why have capital and property markets become so important for our decision makers?

I do not say that there is an easy answer to those questions. Nevertheless, it looks like political power has been more and more monopolized by a cast of people sharing common interests. For instance, the fact that most of them belong to “the Haves” and will be negatively impacted by asset deflation.

Indeed, Jerome Powell and his S&P 500 ETF holdings is not an isolated case. You can be sure that the next Biden administration will be staffed by persons with quite significant financial and/or real estate wealth.

While politicians are good at being vocal about wealth inequalities, especially when they come from the left wing, all them will do whatever it takes to keep stimulating asset prices, leading to even bigger inequalities.

Why are more and more individuals willing participate to this speculative frenzy? Perhaps, because many among “the Haves not” have become desperately looking for more purchasing power in a world of low wage inflation. Thus, all that remain is the hope of huge capital gains on the stock market, the crypto market or the property market

We all know that markets have detached themselves from reality. But officials, and especially central bankers, refuse to admit that their policies are fueling bubbles. Probably because their intention is to keep this absurd ponzi scheme alive, as their actions since 2000 have clearly managed to feed a powerful “assets only go up” narrative.

Where is the glory in that?

The Rise of the Extremes

However, more and more people are getting angry as they do realize that such policies benefit to a minority.

Whatever your opinion on Donald Trump, the 2016 election should not be treated as a “political accident”. Same thing for the Brexit, Catalonia independence movement, recent success of Italian Lega Nord party or the Five Star movement, and the French “yellow vests” protest.

More and more people are getting fed up with the so-called “elites”. They feel that Western democracies are being controlled by mafia-style administrations which are corrupted and only work in their own interest.

Of course, the Trump administration did exactly the same thing as their predecessors in terms of federal deficit and money printing. However, the 2016 election and the record number of people who still voted for him recently despite all the media calling “to defend democracy by voting for Biden”, shows us how deep the political fracture in the West is.

Apocalypse Now?

2020 will end soon, and the current picture is unbelievable. Every week, the world most powerful central bank, the Federal Reserve, is multiplying media interventions to make sure that the fragile “assets only go up” narrative does not break. So, what’s next for America and Europe?

In my opinion, there are three possible scenarios for the future of the West, and each one is a dystopian perspective:

#1 – The narrative is finally broken and markets crash. This is the most likely scenario, as History shows us that it almost always ends like this. Central banks lose control and the West enters depression.

#2 – Political chaos spreads up with systemic dislocation in Europe and/or in America.

#3 – More and more trade exchanges are paid in non-dollar currencies (e.g. Chinese renminbi), meaning that Western fiat currencies quietly collapse, forcing central bankers to desperate moves that could break their financial system.

In fact, you should probably expect a mix of those three scenarios.

For those who do not believe that Western democracies can fail, I recommend they read more about the Mississippi Company bubble, the impact of the crash, and all the political events in France at the end of the eighteenth century.

via ZeroHedge News https://ift.tt/35FQKtV Tyler Durden