Chinese 10Y Yield Premium Over US Treasurys Hits Record High

Tyler Durden

Thu, 11/19/2020 – 09:50

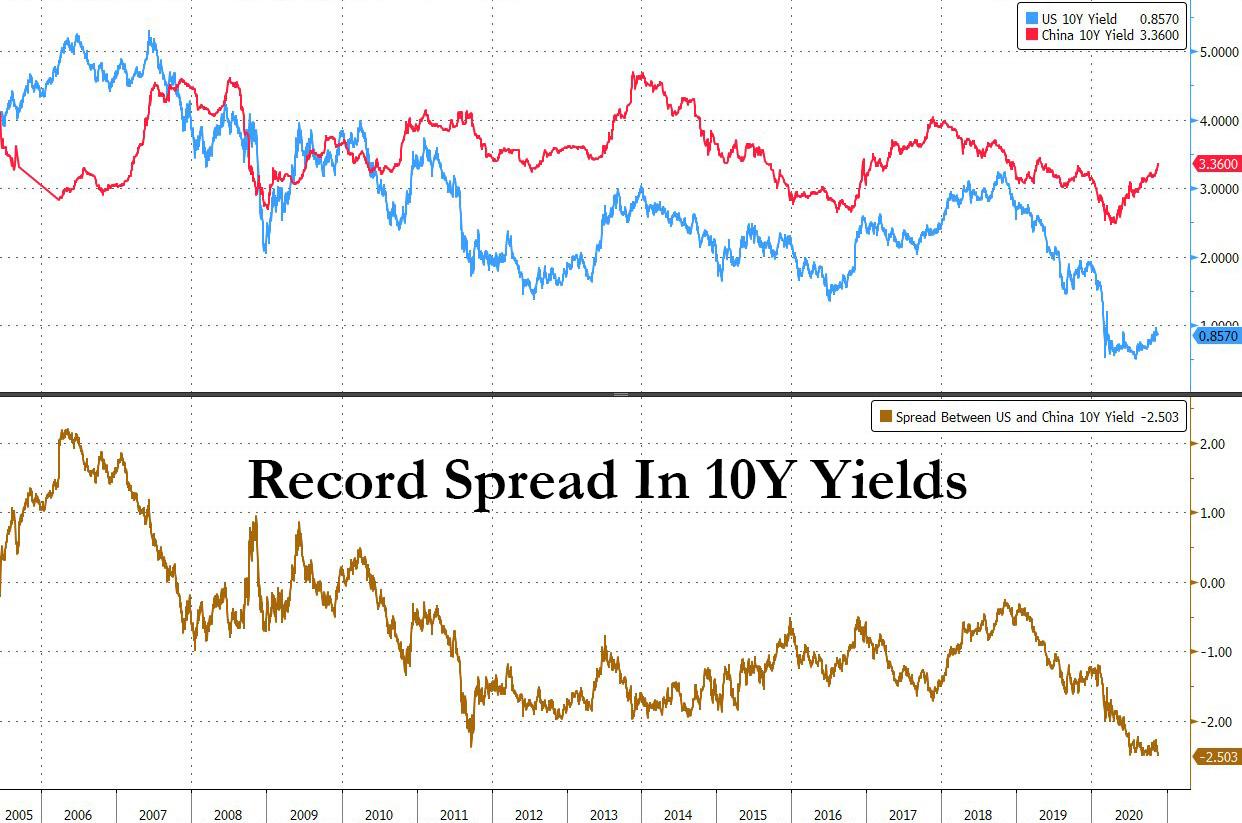

With US Treasury yields capped around 0.90% amid concerns that in the absence of fiscal stimulus the Fed will need to step in with more easing (either in the form of extending QE maturities, or an outright expansion in QE), China is facing a different set of challenges and following the recent rout in the bond market following several unprecedented SOE defaults, overnight the Chinese 10Y yield rose another 2bps to 3.36%, and almost 90bps from the all time low of 2.48% hit in April.

As a result, the premium for China’s 10-year government bonds over U.S. Treasuries of same duration has climbed to 250 basis points, the highest on record.

A big part for the continued push higher in Chinese yields is the PBoC’s “limited approach” to dealing with recent SoE defaults, which we profiled on Monday in “China’s Bond Market Turmoil Worsens As More State-Owned Companies Default.”

Still, as Caixin reported overnight, the series of bond defaults by Chinese state-owned enterprises is now on the radar screen of the country’s top economic planner. At a routine press conference Tuesday, National Development and Reform Commission (NDRC) spokesperson Meng Wei called for local governments to step up supervision through project screening to prevent default risk for enterprise bonds.

{kind=link}

Overall, risk prevention for enterprise bonds has been relatively good and there has been no default this year, Meng said. The cumulative default rate of enterprise bonds is at the lowest level among corporate debts, she said.

As discussed previously, the number of defaults by China’s SOEs is expected to rise marginally next year as the central bank shifts toward a more neutral policy stance amid an economic recovery, according to a Fitch report released Monday. Also on Monday, China’s central bank pumped 800 billion yuan of liquidity into the money market Monday through its medium-term lending facility helping to relieve some of the anxiety that’s gripped institutions and investors after the recent bond defaults, although judging by the continued drift higher in yields, tensions remain.

Investor appetite for debt from weaker SOEs is likely to ebb as market liquidity tightens, a trend that Yongcheng’s surprise default may accelerate, Fitch said. Before the Yongcheng default, five SOEs failed to repay debt from January through October, close to levels seen in the previous two years, according to Fitch.

Amid the investor strike following the SOE defaults, at least 20 Chinese companies have suspended planned bond sales worth 15.5Bn yuan ($2.4bn) over the past week, as the high-profile defaults of three state-owned enterprises and questions about the solvency of a fourth unnerved investors in the world’s second-largest bond market, the FT reported.

via ZeroHedge News https://ift.tt/3lNFjG7 Tyler Durden