Here Is The Little-Known Provision In The CARES Act That Could Trigger A Year-End “Selling Deluge”

Tyler Durden

Sun, 12/13/2020 – 18:30

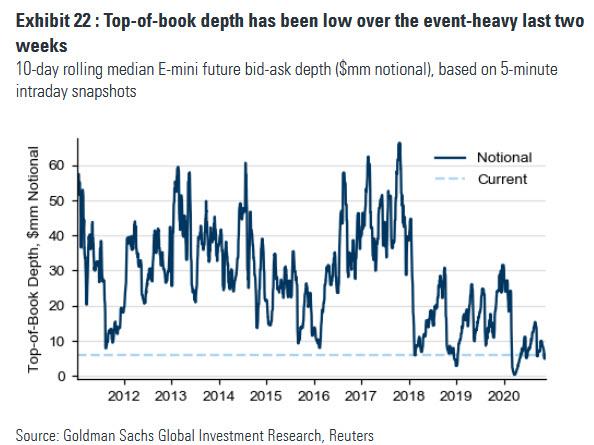

One week before the end of November, JPMorgan issued a startling warning: according to calculations by the bank’s quant, Nick Panigirtzoglou, some $160 billion in negative equity rebalancing (read selling) was on deck by various pension and balanced mutual funds, and – should the rally continued into December – an additional $150 billion in forced selling could emerge from funds who have to keep their 60/40 stock/bond asset allocation. While many on Wall Street braced for a late November drawdown following this note, expecting a deluge of selling into an extremely illiquid market, with Emini top-of-book depth near the lowest levels on record…

… aside from a modest dip on Nov 30, stocks continued their upward ascent with the S&P hitting an all time high last week, just above 3,700.

That said, it may be too early to give the “all clear”, for two reason: first, it is possible that the rebalancing fund “forced selling” has merely been pushed back to December, and year-end, and if JPM’s calculation that we could be facing over a $100 billion in forced selling in the coming, even more illiquid days is correct, it is unlikely there will be enough buying interest to offset the coming pension rebalancing. The second reason why we may experience market turbulence in the last days of the year, is over a little noticed piece of legislation which according to Larry McDonald’s Bear Traps Report, could open the floodgates to 401K selling, leading to a “selling deluge.”

As McDonald writes, buried deep in the CARES Act (the Corona Aid, Relief and Economic Security Act) which was enacted on March 27, 2020, and provided $2.2 Trillion of fiscal stimulus to offset the impact of the coronavirus on the U.S. economy, “is a clause that gives temporary flexibility on early withdrawals from retirement accounts. These temporary changes to the rules give more leeway to make emergency withdrawals from tax-deferred retirement accounts without incurring a penalty.”

Specifically, Section 2022 of the CARES Act eliminates the 10 percent early withdrawal penalty if you are under the age of 59 ½ and withdraw up to $100,000. It also allows for the spread out of your income tax liability over three years rather than the same year you withdraw the money. And since the window to make these penalty-free early withdrawals closes by the end of 2020, millions of cash-strapped households may have no choice but to sell tens, if not hundreds of billions in passively-managed funds to take advantage of this one-time offer to avoid a 10% early withdrawal charge.

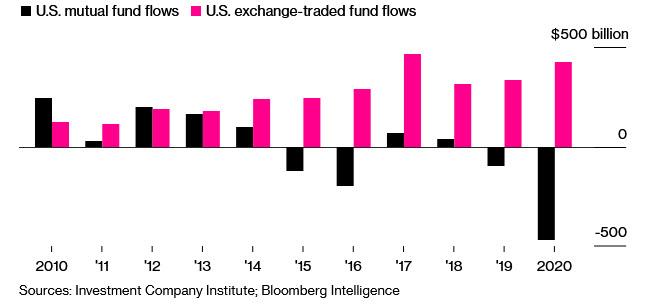

McDonald then goes on to highlight the importance of passive investing which over the past decade has emerged as the dominant price setter in a world where actively managed funds have been fading. As the Bear Traps author writes, “the explosive impact of passive investing is significant. In recent years, passive equity funds have enjoyed inflows of more than $2T, even as traditional, active ones have suffered outflows of over $1.5T, according to data provider EPFR.” Indeed, the main story on Bloomberg this morning picks up on this, writing that “roughly $427 billion has poured into U.S. exchange-traded funds this year, divided almost evenly between equity and fixed-income funds, according to Bloomberg Intelligence data. Meanwhile, mutual funds have bled roughly $469 billion of assets in 2020, on track for the worst year on record in Investment Company Institute data going back to 1990.“

While we have for years covered the staggering divergence between active outflows and passive inflows – which threaten to make conventional stock pickers obsolete and make market prices meaningless – and thus the topic is familiar to regular readers, Bloomberg writes that “this stark divergence in fortunes is part of a tectonic shift that’s seen investors favor ETFs over mutual funds for nine consecutive years, lured by the industry’s ultra-low fees and tax advantages. That trend was accelerated further in 2020, thanks to a well-timed rule from the Securities and Exchange Commission and the Federal Reserve’s first foray into the $5.3 trillion U.S. ETF market. Combined with another rocky performance from active managers, it’s clear why ETFs are winning out, according to State Street Global Advisors.”

In any case, as McDonald summarizes, “there is now over $12T in index funds globally —either passive mutual funds or the increasingly popular ETFs.”

And while the 401(k) provision is intended for those hardest hits by the pandemic, such as people who lost their jobs, the rules are applied rather loosely. For example, a qualified person includes those that “experience adverse financial consequences from being quarantined, being furloughed or laid off or having their work hours reduced.” Also qualified are those who “experienced adverse financial consequences as a result of being unable to work due to lack of childcare [or] closing or reducing hours from a business that you own or operate due to SARS Cov-2 or Covid-19”. Since virtually anyone can argue that they are qualified under these criteria, the language is open to interpretation and the IRS is unlikely to enforce the limits of this provision to the letter of the law according to McDonald, especially since banks and retirement management companies – who have themselves benefited greatly from the CARES act – are giving considerable leeway to allow their customers to use the CARES Act early withdrawal exemption.

McDonald then makes one final point – the same one we noted three weeks ago – namely the lack of market depth or liquidity, to wit:

This potential selling deluge comes as positioning in U.S. equities is becoming stretched and implied volatility for the Georgia runoffs is above average. Year-end rebalancing by pension funds is still expected to create supply in equities as funds rebalance their (now) overweight in equities. Overall, for 2021 we should expect volatility to grind lower as the removal of trade war risk, the declining corona risk with the advent of the vaccines, the removal of the uncertainty of the elections, and rebounding GDP growth with 0% Fed funds rates provide a supportive backdrop for risk assets. Notwithstanding that, we first need to pass the year-end hurdle of retirement withdrawals, pension rebalancing, and Georgia runoffs.

Ultimately, The Bear Trap report’s conclusion is identical to that of Morgan Stanley’s Michael Wilson, who has recently cautioned that a near-term “drawdown” is coming, but that would be followed by a brisk episode of BTFD and new highs in 2021, or as McDonald puts it, while the coming selling deluge “could take an overstretched market by surprise…. we would then use a meaningful pullback to prudently add to the risk.”

via ZeroHedge News https://ift.tt/3oSwvQn Tyler Durden