FX Strategist Explains Why This Time Bitcoinmania “May Be Different”

Tyler Durden

Thu, 12/17/2020 – 18:20

Now that bitcoin is once again all the rage among investors, both retail and institutional, opinions on its future prices follow a bimodal distribution with a concentration at either extreme and few moderate view inbetween. Which is why this morning’s note from SocGen FX strategist Kit Juckes with interest as it presents one of the more nuanced takes on what may happen next, and if nothing else, we believe he hammers the point with the following observation on how “bitmania” is different from tulipmania:

“Bitcoin is different because even now, most activity is ‘buy to hold’; by people who believe it is the natural competitor to gold as a store of value in a time when central banks are playing footloose and fancy free with fiat money.”

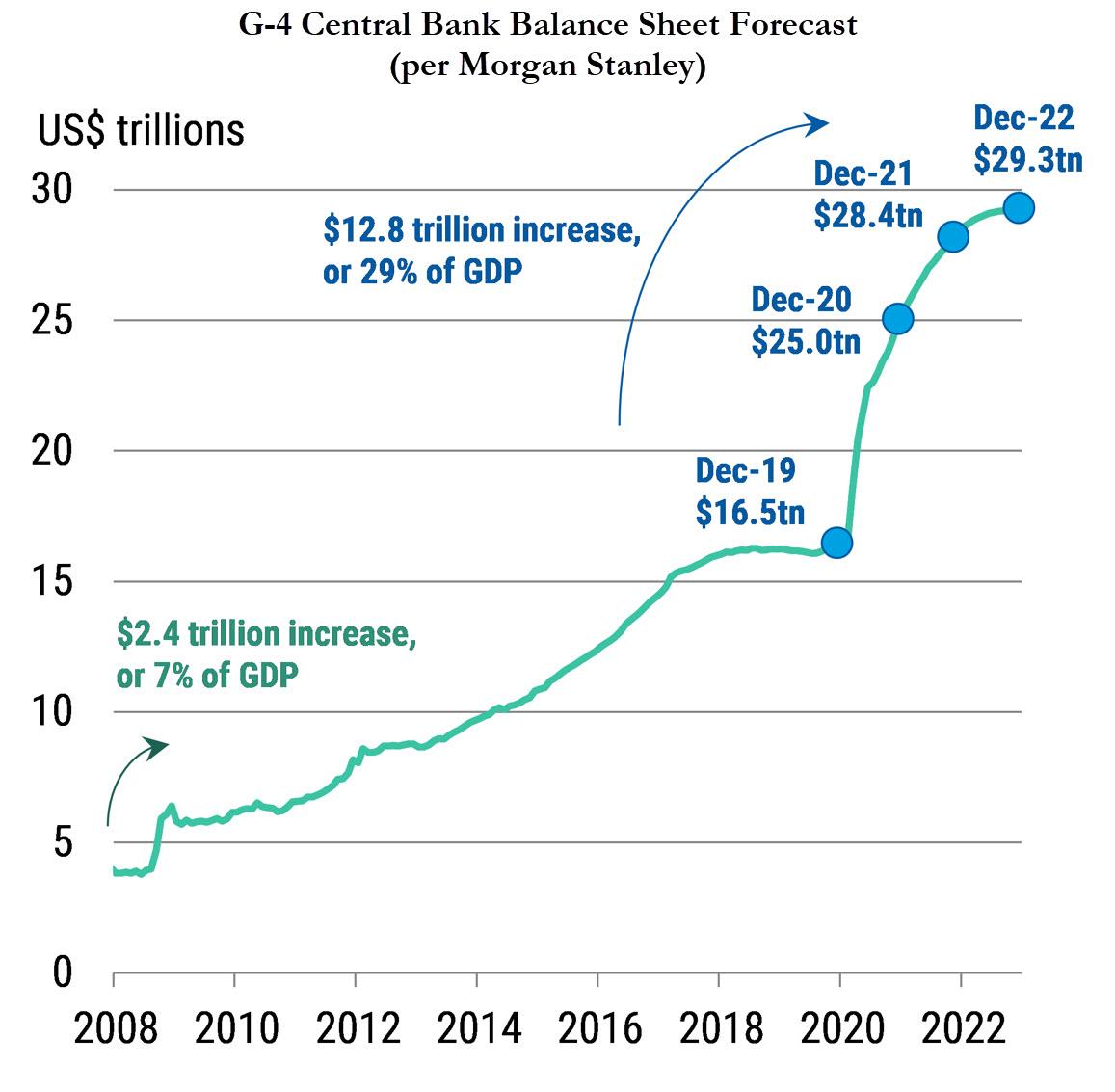

Of course, the real reason behind bitmania – and why it may persist – is simple: it’s all in response to brrrr (which is why we find all the Fed fanboys bashing bitcoin so hilariously absurd).

As to why bitmania will likely have staying power, well, as Juckes concludes, “aAficionados believe that central banks who have turned the monetary tap wide open at the back end of a historic era when a surge in the global labor force, and huge technological change have kept inflation at bay, will be too slow to rein in inflation when these forces fade.”

He is, of course, right with one minor edit: not only will central banks not be able to rein in inflation, but they will welcome it which is also why the world is on the verge of a digital currency revolution where central banks will finally be able to literally print digital money which they can distribute, at their discretion, among the population.

We excerpt from his full note titled “Jay Powell is feeding the (dollar) bears again” below:

Between August and November 1636, just as what is now the Netherlands emerged from a long recession due to the resumption of the country’s war with Spain, an outbreak of the bubonic plague killed an eighth of the population of Haarlem. The boost that gave to incomes is cited as one of the reasons, along with the availability of credit in the country which invented fractional reserve banking, for the madness described as Tulipomania in Mike Dash’s excellent (short) book on the subject.

There will no doubt be comparisons of tulips and Bitcoin in the days/weeks/months ahead. In my mind the tulip mania became a speculative bubble, rather than an odd but harmless pastime for rich lovers of flowers, when people were buying in the hope of making a quick profit, and were mostly buying on credit. In this regard at least, Bitcoin is different because even now, most activity is “buy to hold” by people who believe it is the natural competitor to gold as a store of value in a time when central banks are playing footloose and fancy free with fiat money. Aficionados believe that central banks who have turned the monetary tap wide open at the back end of a historic era when a surge in the global labor force, and huge technological change have kept inflation at bay, will be too slow to rein in inflation when these forces fade.

I have a lot of sympathy for that view, and therefore for the idea that gold will remain in demand as long as policy rates remain very low. By the same token, Bitcoin has been around long enough that it probably isn’t going away. I certainly don’t however, have any desire to try to construct a fancy model to predict how high bitcoin prices might go. I’ll just make the point that if this does become a speculative bubble, it can get pretty wild before it bursts.

Of course, if there are bubbles around, they are being helped by Fed Chairman Jay Powell. The FOMC’s ‘dot-plot’, which I glanced at during half-time yesterday, looked hawkish. Mr Powell’s comments were anything but. Money’s staying way. Throw in hope that a fiscal package will be forthcoming, that an EU/UK trade deal can be struck now that fish, rather than the level playing field is the main obstacle, that the recovery Fund is up and running and of course, that vaccine deployment will continue, and the stage is set for the dollar to go on falling. The only problem is that it’s falling too fast. The last Bloomberg FX poll has a high forecast for Q4 2021 of 1.28. Our forecast is 1.27; that’s a 4% move, compared to the 3% the euro has risen in the last month alone.

All of that ensures that bitcoin – and gold – will go much higher, albeit with occasional bloodcurdling crashes.

via ZeroHedge News https://ift.tt/2KArVaK Tyler Durden