ETFs And Passive Investing Have Wildly Distorted S&P 500 Valuations, Study Finds

Academics are starting to arrive at a conclusion we have been talking about for years: the influx of ETFs and passive investing in today’s market could be more trouble than its worth.

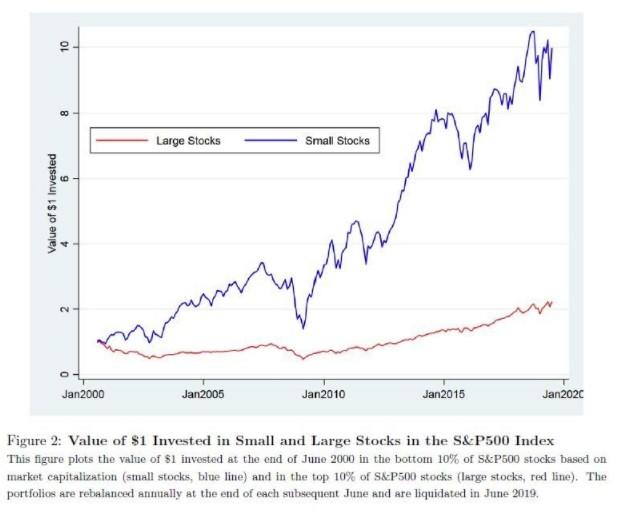

Many people currently believe that larger companies are in a bubble – and that small caps are the place to look in 2021. A new study supports this assertion. In fact, passive flows into the S&P 500 have “disproportionately pumped up prices of its largest members — paving the way for small companies in the benchmark to eventually outperform,” according to a new report from BNN.

The report, which cites a team from Michigan State University, the London School of Economics and University of California Irvine, analyzed data from 2000 to 2019. It was authored by Hao Jiang, Dimitri Vayanos and Lu Zheng.

The conclusion was that smaller members of the S&P 500 wind up becoming too cheap relative to the larger names. “Flows into funds tracking the S&P 500 index raise disproportionately the prices of large-capitalization stocks in the index relative to the prices of the index’s small stocks. The flows predict a high future return of the small-minus-large index portfolio,” the paper says.

The study found that “noise traders” (passive investors) “tend to push up the price of fashionably big companies as they enter the S&P 500”. This causes those companies to have higher weightings, which creates a self-fulfilling prophecy when new passive traders enter the market.

The paper notes: “When prices are distorted, weights of value-weighted indices are biased, and flows into index funds exacerbate the distortions.”

This obviously dictates that when there is reversion to the mean, smaller cap stocks will outperform. The study posits that the S&P 500 will eventually normalize. In fact, it suggests that a portfolio that goes long the smallest names in the S&P while shorting the larger names can return an average of 10% per year.

“If index-related price distortions become more significant over time, they may boost the profitability of active investing strategies that exploit these distortions and ultimately slow the shift to passive investing,” the paper concludes.

Tyler Durden

Sun, 01/17/2021 – 15:45

via ZeroHedge News https://ift.tt/3bOoF7a Tyler Durden