How Does This All End?

Authored by Lance Roberts via RealInvestmentAdvice.com,

Retail Investors Stage A Riot On WallStreet

For years, Wall Street has taken advantage of retail investors.

In 2000, they dumped companies with no earnings or revenue on unsuspecting individuals, eventually costing them their retirements. In 2008, it was outright mortgage fraud. From 2009 to the present, Wall Street has used algorithms, high-frequency trading, and user data purchases to front-run “the little guy” by scalping them for profits.

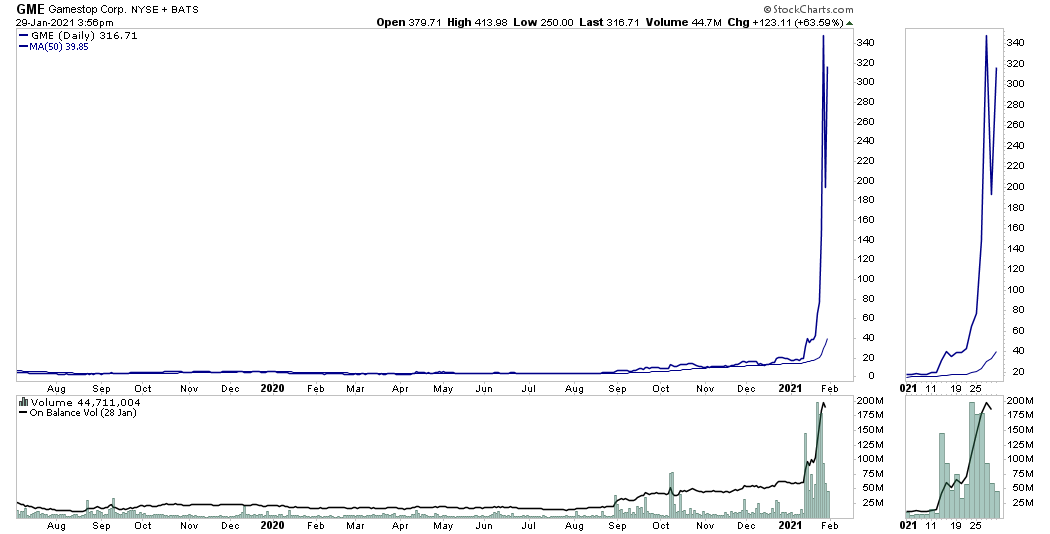

Interestingly, this past week, retail investors hit back. Just as individuals used social media platforms to organize protests and riots across the country, traders used websites like “Reddit” to organize a successful short-squeeze on Wall Street hedge funds. That short-squeeze, which forces hedge funds who were short stocks to cover the positions, has sent a handful of stocks to the moon. Notably, Gamestop, a retail store that is on its way to bankruptcy, has been the movement’s poster child.

If you happened to be visiting Mars over the last few days, here is what I am talking about.

That chart is what a “short-squeeze” looks like when those short a stock have to “buy to cover” at the prevailing market price. It hasn’t been pretty, and the “Wall Street Bets” Reddit group took credit earlier this week for forcing Melvin Capital, a hedge fund short Gamestop, to get a $2.7 billion bailout from its hedgefund friends.

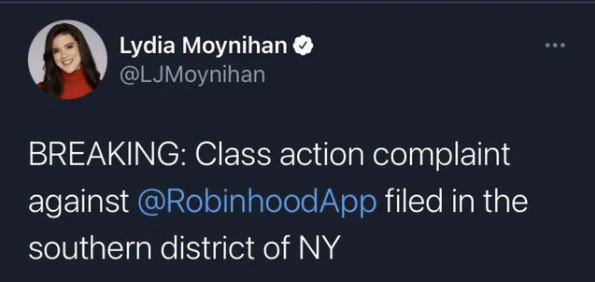

From that moment, it didn’t take long for Wall Street to show its true colors by locking retail investors out of being able to buy Gamestop. Robinhood, Schwab, WeBull, and others all restricted trading in the stock, which resulted in immediate class action lawsuits.

The Margin Problem

While Robinhood, and other brokers, took a lot of heat for restricting trading in shares of the most heavily shorted names, there was a reason – collateral requirements.

Without getting into all of the minutiae of capital requirements and margin accounts, the simple fact is that the NSCC is required, by SEC rules tracing back to Dodd-Frank, to make sure there is always cash to settle.

Depending on the net of buys and sells, the brokerage (like Robinhood) is on the hook to pay or receive the trading’s net cash. That is simply credit risk. The NSCC takes on that credit risk. To mitigate the risk of a brokerage failure, they demand firms post a deposit of 10% of the collateral.

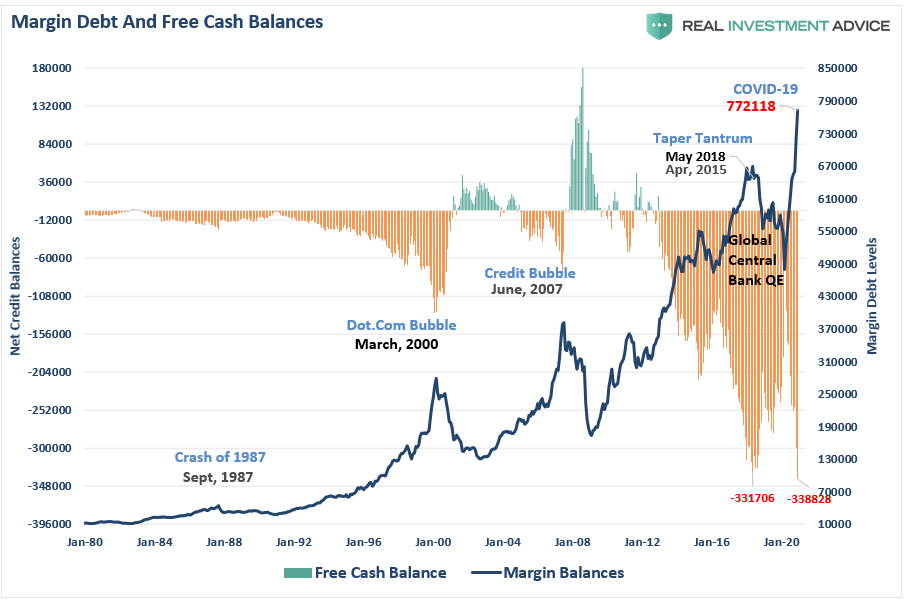

Here is where the problem comes in. When firms are already heavily on margin (currently at a record level of negative cash balances), sharp changes in the underlying collateral value can lead to immediate demands for more deposits from the brokers.

On Thursday, Robinhood had to raise nearly $1 billion in capital to secure the ability to cover collateral requirements. We also saw margin requirements being adjusted by the DTCC.

Of course, the risk to the markets is that with brokerage firms already running too lean, if a firm like Robinhood failed, the ripple effect through the financial industry would likely rival that seen during the Lehman bankruptcy in 2008.

Such are likely reasons the markets sold off this past week.

Strange Bedfellows

As I stated at the beginning, it is about time Wall Street got a little bit of what they have been dishing out on Americans for years. It won’t take long for Wall Street to “circle their wagons” and protect themselves, but maybe this is just the warning shot they needed to make some changes. However, I highly doubt it.

It is interesting, though, that Robinhood’s actions, which may just put them out of business, have also united an unexpected group of individuals. Who would have ever thought that Ted Cruz would agree on anything with A. O. Cortez?

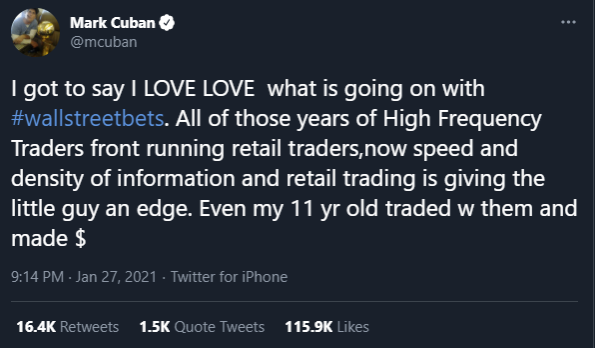

Even Mark Cuban, who benefitted greatly from Wall Street making him a billionaire, weighed in.

The mania is likely to get far worse before it ends. Such is particularly true if Citadel Securities, the hedge fund that pays Robinhood for user data to front-run trades, reloaded their short positions before making Robinhood shutter access.

Nonetheless, the “Wall Street Bets” clan are undeterred at this moment and are doubling down on their “bets.”

At least for now.

How Does This All End

The real question is what eventually happens. In Gamestop’s case, the company is effectively a “dead man” walking retailer. So, the only reason anyone is buying the stock is simply due to the short-squeeze conditions that currently exist. As of this writing, the percentage of shares “short” is 122%. (That isn’t a typo.)

The problem comes when the “Wall Street Bets” traders eventually do want to sell. Those traders are “paper rich,” however, to convert their shares back into cash, they have to sell. The question will be WHO will they sell to?

Such is where market dynamics come into play. As stated in “No Cash On The Sidelines:”

“Every transaction in the market requires both a buyer and a seller, with the only differentiating factor being at what PRICE the transaction occurs.”

Think about a crowded theatre. At the moment, everyone is going into the theatre (buying), and no one is selling. However, when they begin to try and sell their positions, no one will be there to buy from them.

Such is the equivalent of yelling “fire.” The smart ones will get out early. The rest will find themselves scrambling towards a very narrow exit. Once the price starts falling, the sellers will swamp the buyers driving the price lower. In Gamestop’s case, given the company’s value is around $10, where it was trading before the mania, the decline will be both brutal and fast.

While Wall Street is the villain, this is one of those stories where the villain gets away with the crime in the end.

Markets Take A Hit

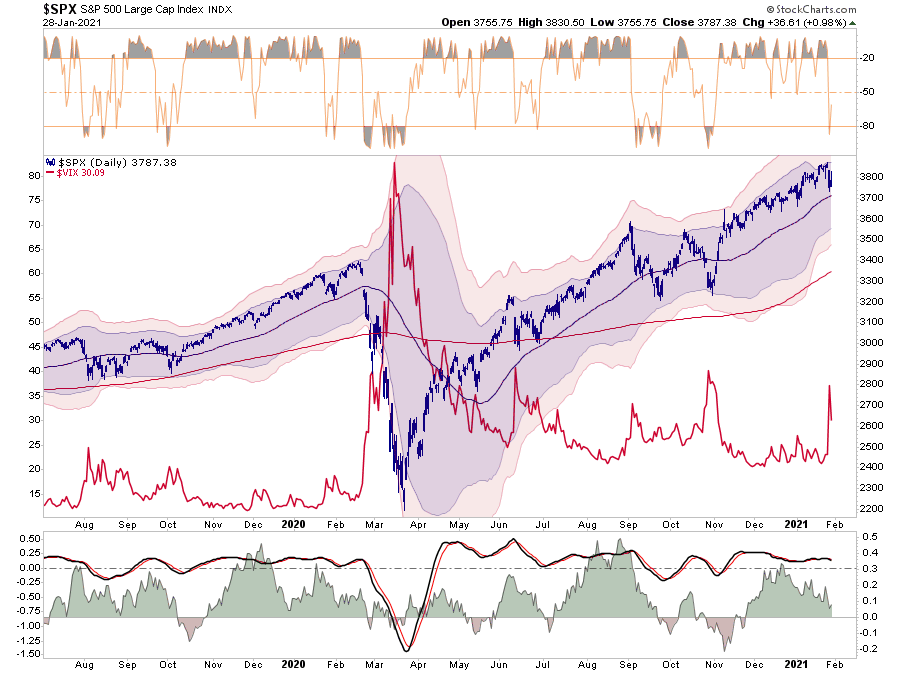

Last week, we discussed that our “money flow” signals were close to triggering, suggesting either a short-term correction of 3.-5% or an extended consolidation. (We publish a daily 3-minute video click here to subscribe)

Let me repeat that point from last week:

“Important Note: A correction can take on one of two forms. The market either declines in price to alleviate the overbought condition, or it can consolidate sideways.”

Such remains the case currently, as on Wednesday, the market declined by almost 3% in one day. That swift sell-off did trigger our money flow “sell signal,” as the volatility index spiked higher.

While the market did bounce on Thursday, it was a “suckers rally.” That bounce led to a retest of the 50-dma on Friday. Money flows have continued to weaken, suggesting there remains underlying selling pressure in the market currently.

While I fully expect a reflexive rally next week, that will likely be an opportunity to reduce risk rather than chasing markets. Such will be the case until we see money flows start to turn positive again, suggesting some underlying buying pressure.

For now, we are maintaining our higher level of cash. After selling last Friday, we have the luxury to be patient and look for opportunities to add to our core equity holdings at cheaper prices.

Greed Breaks Things

My colleague Doug Kass penned an excellent piece on Thursday discussing market conditions:

“‘If there is one common theme to the vast range of the world’s financial crises, it is that excessive debt accumulation, whether by the government, banks, corporations, or consumers, often poses greater systemic risks than it seems during a boom.’ – Carmen Reinhart

A grotesque level of speculation has taken us to where we are now. With a good perspective on history, we can have a better understanding of the past and present — and thus a clear vision of the future.

Like previous speculative cycles, this is about greed and trying to make money. Attempts to make trading seem like ideological notions and high minded intentions are fanciful to me. Such makes my point that mishappened levels of speculation usually occur in the later stage of a Bull Market and, more often than not, presage a Bear Market.

Speculation, as noted yesterday, is the outgrowth of undisciplined monetary policy.”

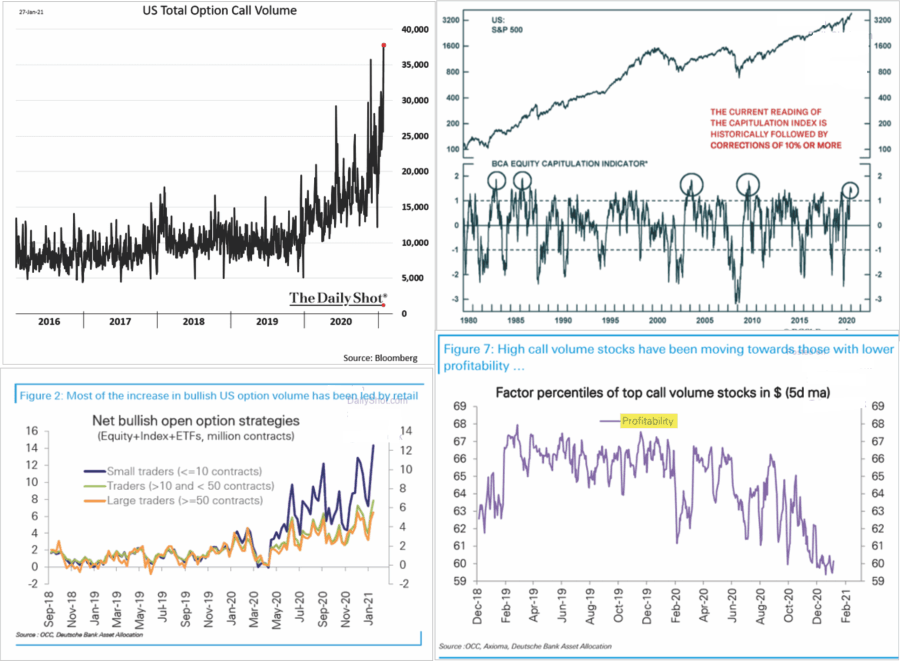

He is correct. The rampant speculation in the market is prolific, as shown in the charts below.

As Doug notes, speculation is the direct result of the “Moral Hazard” created by the Fed’s ongoing monetary interventions.

After a decade of injecting liquidity into the financial markets, it is no surprise that investors “believe” they have an “insurance” policy against loss. As noted in the linked article, such is the very definition of moral hazard. Every time the market “wiggles,” the Fed has expanded their monetary interventions.

However, at some point, the Fed may become trapped by the own policies. If the direct stimulus does cause an inflationary surge, the Fed may get forced to cut QE and increase rates.

The last time they tried that was in 2018.

It didn’t go well.

Tyler Durden

Sun, 01/31/2021 – 13:30

via ZeroHedge News https://ift.tt/3ajKUj8 Tyler Durden