Treasury Keeps Debt Auction Sizes At Record High, Will Reduce Bill Issuance To Drain Record Cash

One of the less discussed, but perhaps most ominous developments in recent months, has been the surge in US Treasury auction sizes which have hit all time highs as a result of the (just as surging) US budget deficit and the need to fund it somehow (well, not somehow, but rather by selling debt)…

… which is why bond traders were eagerly anticipating today’s Treasury refunding announcement which discloses the projected auction sizes for the given quarter, as well as gives further insight into the Treasury’s funding strategy.

And as we also await the outcome of the Biden stimulus deal, which may need as much as $1.9 trillion in new funding, the Treasury held steady its planned issuance of longer-dated securities at a quarterly debt auction next week as the department also awaits the result of the latest covid package.

Having boosted its so-called quarterly refundings in each of the last three quarters, pushing its stockpile of cash to an all time high, for the coming quarter, the Treasury’s latest refunding statement projects that the US will sell $126 billion in long-term debt next week, broken down as follows:

- $58 billion of three-year notes on Feb. 9, unchanged from January but $4 billion more than November

- $41 billion of 10-year notes on Feb. 10, the same as last quarter

- $27 billion of 30-year bonds on Feb. 11, unchanged versus November

The total amounts to $126 billion (and $63.1 billion net of maturities), or $4 billion more than the November refunding — a new record, thanks to moves the past two months boosting three-year note auctions.

Officials also followed through on plans detailed in November to lift auctions of inflation-linked securities this year. Consistent with the $2 billion increase in the January 2021 new-issue FRN auction size that was previously announced in November 2020, Treasury intends to increase the corresponding February and March FRN reopening sizes by $2 billion, resulting in a $26 billion auction size for each. Treasury anticipates no further changes to 2-year FRN auction sizes for the remainder of the quarter.

Separately, the Treasury also announcing no changes to nominal coupon auction sizes over the upcoming quarter, which means that we won’t see any new record auction sizes until at least May.

This was broadly in line with expectations, as the majority of Wall Street bond dealers had predicted the Treasury would make no changes to nominal coupon-bearing debt auctions.

Also as expected, the Treasury said it will reduce bill issuance, which surged as it rushed to fund pandemic-related spending. However, with Treasury cash levels now at a staggering $1.5 trillion, the aim now is to bring the share of bills in the nation’s debt back toward historic norms. Treasury Officials didn’t specify the amount by which bill supply will fall over the period. In August, the Treasury Borrowing Advisory Committee recommended allowing the share of T-bills to fall gradually to a range of 15% to 20% of outstanding debt, compared with nearly 24% now.

Here is what the Treasury said:

The substantial increases in nominal coupon and FRN issuance sizes over recent quarters will allow Treasury to gradually reduce bills as a percent of Treasury debt outstanding in a manner consistent with recommendations made by the Treasury Borrowing Advisory Committee at the November 2020 meeting.

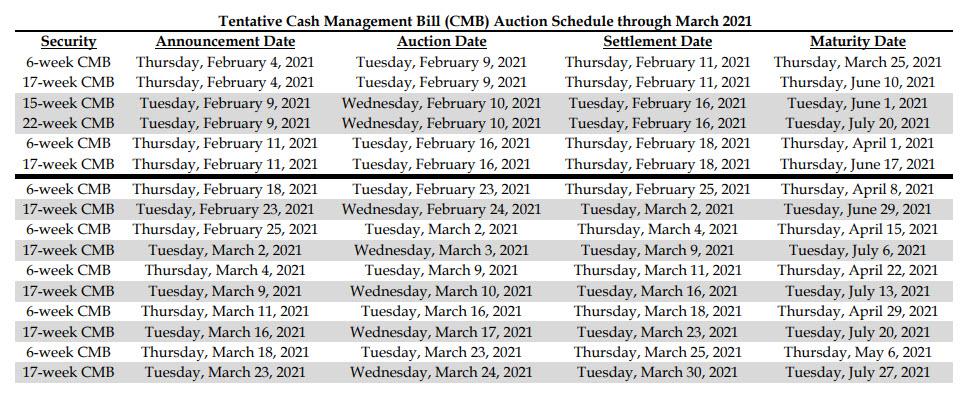

Accordingly, Treasury plans to modify its regular cadence of CMBs. Treasury anticipates that weekly issuance of the 15- and 22-week CMBs will cease after settlement on February 16, whereas weekly issuance of the 6- and 17-week CMBs will continue at least through the end of April. When this modification occurs, the 6-week CMB will remain as part of the Thursday settlement and maturity cycle, whereas the 17-week CMB will transition to the Tuesday settlement and maturity cycle. The remaining CMBs will continue to be announced as part of the regular Tuesday and Thursday bill announcement cycle.

Treasury may also increase the auction size of one or more of its remaining bill offerings to moderate the pace of decline in the aggregate supply of bills outstanding in anticipation of the existing 15- and 22-week CMBs maturing without reissuance.

The treasury published the following tentative transitional CMB schedule.

Separately, and also consistent with its guidance in the November 2020 refunding statement, the Treasury anticipates continuing to gradually increase TIPS issuance across all tenors in CY 2021. This gradual increase began with a $1 billion increase in the January 10-year new issue and will continue with $1 billion increases in the February 30-year new issue, the March 10-year reopening, and the April 5-year new issue, compared to their respective issuance sizes last year. Additional issuance size changes will be announced quarterly in subsequent refunding statements.

As Bloomberg notes, the department held off on making a decision on debt linked to the Secured Overnight Financing Rate, the heir to Libor as a benchmark for short-term dollar lending rates. The government has been analyzing the idea for months, and said Wednesday it “continues to actively explore the possibility” of a SOFR-linked issuance.

No decision has been made by Treasury regarding potential issuance of an FRN linked to the Secured Overnight Financing Rate. Treasury continues to actively explore the possibility of issuing such a product and will provide ample notice to market participants if it chooses to move forward.

This confirms that the system remains woefully unprepared for the massive shift from LIBOR to SOFR, which is the reference rate of hundreds of trillions in interest-bearing debt securities.

Today’s refunding statement follows a Monday forecast from the Treasury where as part of its quarterly borrowing estimates, it said it would reduce its cash balance to $800 billion by the end of March and to $500 billion by June, from about $1.5 trillion now.

As noted above, this cash drain will be achieved in part by trimming bill issuance. The Treasury said it’s modifying the “cadence” of its shortest-dated securities, called cash management bills, or CMBs.

- The 15-week and 22-week CMBs will cease after settlement on Feb. 16

- The six-week and 17-week CMBs will continue at least through April

- Other bill auctions could be boosted given the changes in CMB sales

The sharp drop in the cash balance will lead to a surge in bank reserves (which as we discussed on Monday will likely send stocks sharply higher) and also gets the government ready for the risk of a protracted battle over the debt limit, with the current suspension set to expire at the end of July. By law, the Treasury has to shrink its cash to the level when the suspension was put in place, back in 2019.

Tyler Durden

Wed, 02/03/2021 – 10:30

via ZeroHedge News https://ift.tt/2MnuwGw Tyler Durden