Facing Up To JP Morgan’s Leverage Relief Threats

By Nick Dunbar of Risky Finance

There is one very simple rule of banking. If you increase leverage, you increase shareholder returns – but at the cost of increased risk. That lesson of the 2008 crisis ensured that the Dodd-Frank Act included a supplementary leverage ratio limit.

When the pandemic sent markets into a tailspin one year ago, the US Federal Reserve temporarily suspended leverage restrictions on the biggest banks. This, and other forbearance measures, allowed them to function smoothly as the economy sharply contracted, then rebounded.

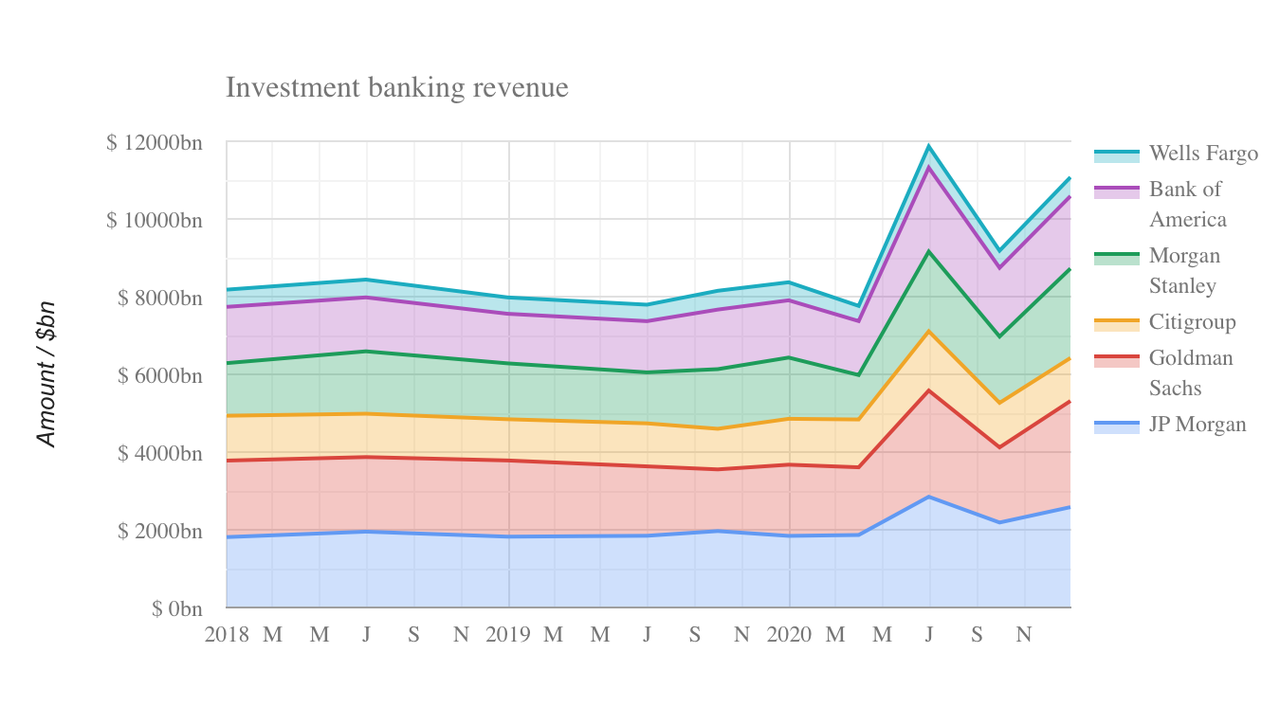

This had a predictable side effect – a bonanza for shareholders. During 2020, the six largest banks reported trading and investment banking revenues that were $27 billion higher than their pre-pandemic averages. It started out when corporate clients of the banks raised cash in a panic and issued hundreds of billions in new bonds. It continued with the latest frenzy in special-purpose acquisition vehicles that seems quite unrelated to Covid-19.

Now, the Fed will shortly announce whether the special Covid relief measures will continue or not. Led by JP Morgan, the banks lobbied for an extension, claiming that ending forbearance will increase market volatility. In response, US senators Elizabeth Warren and Sherrod Brown wrote a stern letter urging Fed chairman Jerome Powell and other bank regulators to ignore such pressure and allow the relief to expire on 31 March.

Risky Finance has compiled Q4 2020 disclosures from the banks allowing us to examine the issue. As we discussed in our previous article, the relief rule allowed banks to temporarily disregard holdings of Treasury securities and central bank cash balances in the denominator of the supplementary leverage ratio.

Tyler Durden

Thu, 03/18/2021 – 13:25

via ZeroHedge News https://ift.tt/2Qf76o5 Tyler Durden