Who Benefitted From The Euro And Who Pays The Piper Now?

Authored by Mike Shedlock via MishTalk.com,

Let’s take a look at the latest currency imbalances in the EU with a series of questions and answers. This discussion started from reader comments.

Euroscepticism Grows In Germany

A noteworthy reader-led discussion just took place in response to my previous article Euroscepticism Grows In Germany as 63% Say the EU is Excessively Bureaucratic

One of my readers, PecuniaNonOlet, commented “I thought Germany was the biggest beneficiary of the EU.”

That is (or was) an accurate assessment. The response from TexasTime65 was perfect.

“They were the biggest beneficiaries. But now they are potentially the biggest losers because all the other countries owe them a lot of money and have no real way to pay any of it back unless Germany becomes a net importer of goods and services (which is politically a no-go in Germany),” replied TT.

Trade Statements by German Finance Minister “Utter Lunacy”

I have commented on trade aspects many times before.

For example please consider my September 13, 2016 article Michael Pettis Calls Surplus Trade Statements by German Finance Minister “Utter Lunacy”

At that time the six largest deficit countries owe a collective 797.3 billion euros to the four creditor countries, primarily Germany.

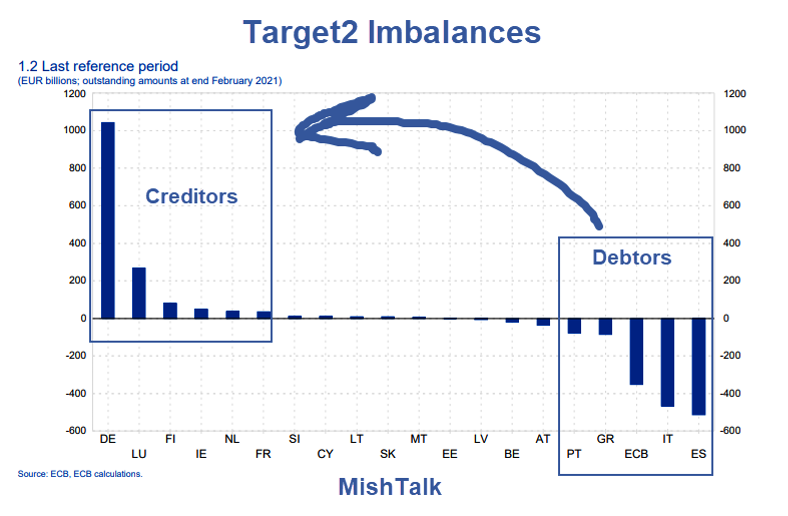

Target 2 Imbalances

It’s been a while since I reported on Target2 (what countries owe each other).

Spain, Italy, Greece, and the ECB now owe Germany (alone) over a trillion euros!

Tiny Luxembourg is a creditor to the tune of 267 billion euros.

The creditor total is over 1.5 trillion euros!

How can that be paid back?

It can’t. Target2 is one of the fundamental flaws of the Eurozone.

The ECB denies this and so does the pro-EU clan in general, but Target2 imbalances are a measure of capital flight.

Those imbalances can only be paid back in one of these ways: Default, forgiveness, monetary printing and handouts against Maastricht Treaty rules, or a very prolonged period in which Germany becomes a net importer of goods and services from Spain, Italy, and Greece.

Place your bets, but I rule out the last choice.

Euro What If?

Let’s explore another question “What if the UK had moved to the Euro?“

Undoubtedly the UK, like Germany, would have been a huge creditor country.

It would have then been stuck, like Germany is now, with bailing out the EU debtor states.

There would have been eventual pressure on the UK to pony up for bailouts even if the UK stayed in the EU but remained on the British pound.

This is yet another excellent reason the UK was wise to Brexit.

Income Transfer Schemes

Long-time readers will note that occasionally I mention a pending currency crisis.

Issues like the above are why it could start anywhere. The US, EU, Japan, and China all have serious issues.

Michael Pettis and I discussed a different form of “who pays?” in Income Transfer Schemes US vs China, Which Country is in the Worst Shape?

Pettis concludes that China is in the worst shape in at least one measure.

Demographically speaking, Europe and Japan are at the top.

Pettis made this accurate overall assessment regarding China: “Because these transfers must ultimately be funded by liquidating government assets, in the end they cannot help but represent a significant shift in the distribution of political power.“

In response to a my question regarding the EU, US, and Japan, Pettis replied” The extent and direction of the transfers are different, Mish, so I’d argue that the political implications are likely to be different, but one way or another we should expect political changes. You can’t shift income without affecting the distribution of power.“

Currency Crisis Starts When and Where?

The political repercussions of Target2 bailouts are still unresolved.

EU Traget2 imbalances will not grow forever, nor will the losing policy of Abenomics last forever, nor insane deficits in the US, nor numerous setups in China.

People who assume the next currency crisis is bound to start in the US are simply too US-centric.

A currency crisis could start in the US of course, but my belief is something blows up elsewhere first.

Since it is impossible to say where, when, or how, I will again be accused of making a pointless observation.

But I do have a practical point best addressed with a question: Got Gold?

Tyler Durden

Sun, 04/25/2021 – 08:10

via ZeroHedge News https://ift.tt/3gDw8bU Tyler Durden